Opinion: The largest use case for stablecoins is hedging and cross-border payments, while other RWAs are gradually moving from crypto-native to mainstream adoption.

TechFlow Selected TechFlow Selected

Opinion: The largest use case for stablecoins is hedging and cross-border payments, while other RWAs are gradually moving from crypto-native to mainstream adoption.

The first wave of adoption for stablecoins and RWAs did not come from ordinary people, nor from those indifferent to crypto.

Author: Wang Qiao

Translation: TechFlow

In the past, stablecoins and other tokenized real-world assets (RWA) were believed to be the types of crypto applications that would attract mainstream adoption.

A decade ago, bitcointalk endlessly debated remittances. A few years ago, with the emergence of smart contract blockchains, our industry began envisioning Wall Street replacing DTCC (the US financial services company) by settling stocks on-chain.

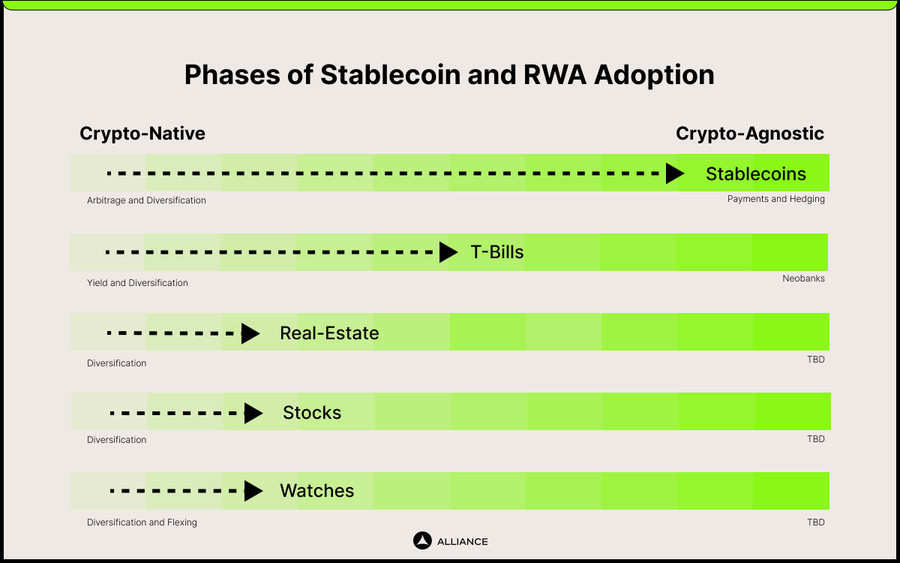

It turns out that the first wave of adoption for stablecoins and RWAs did not come from ordinary people or crypto-agnostic users. Instead, they first went through crypto-native use cases. For example, stablecoins initially found product-market fit among crypto-native users—such as those conducting cross-exchange arbitrage or needing a safe haven to hedge volatility in crypto assets. Once the stablecoin infrastructure was built and battle-tested, crypto-agnostic use cases could follow. These include payments, remittances, and inflation hedging against rapidly depreciating currencies like the Turkish lira or Argentine peso. While these use cases are not inherently crypto-native, on-chain and anecdotal evidence shows they are growing rapidly within the crypto ecosystem.

Other RWAs may follow a similar path. U.S. Treasuries found traction on-chain because after the Federal Reserve raised interest rates from 0% to 5%, crypto-native users sought stable yields. These users include DAOs like MakerDAO and crypto startups needing to diversify their treasury holdings. Crypto-agnostic use cases are now emerging here too. New crypto-native banks outside the U.S. now compete to offer their customers secure access to U.S. yield via USDC/USDT savings products.

This two-stage adoption curve—first crypto-native, then crypto-agnostic—is unsurprising in hindsight. For any crypto product, it’s natural that early adopters are those already familiar with crypto and who have essential infrastructure like self-custody wallets installed.

The question now is: where do today’s various types of RWA stand along this two-stage adoption curve? And what are the imminent use cases for these RWAs?

The short answer is:

-

Stablecoins are in the crypto-agnostic stage. The most important use cases at this stage are currency hedging and cross-border payments.

-

Other RWAs—such as government bonds, equities, real estate, and luxury watches—are still in the crypto-native stage. The most important use case here is diversification.

Stablecoins: Hedging and Payments

Stablecoins settle around $10 trillion annually on-chain, surpassing PayPal, rivaling Visa, and approaching ACH in scale—an astonishing achievement in just a few years.

Equally striking is that the total supply of stablecoins is approximately $150 billion. In other words, each dollar circulates on-chain 60–70 times per year.

None of these statistics would be possible without a borderless, permissionless ledger. A common ideological critique of stablecoins (and RWAs in general) is their reliance on centralized custodians to hold off-chain assets and maintain the 1:1 peg. While this is a valid concern, it overlooks the fact that centralized custodians are unavoidable in any financial system. The U.S. Federal Reserve System and DTCC also depend on centralized custodians. The key difference is that blockchain technology enables a ledger that is open to anyone globally, rather than restricted to certain licensed institutions.

One might reasonably argue that much of this on-chain volume consists of speculative activity rather than “real-world usage” like currency hedging or cross-border payments. We’ll never know the exact split between speculation and real-world usage, but even if only 1% of the $10 trillion annual volume represents real-world use, that’s still a massive number. Moreover, our anecdotes align with the data.

For years, we’ve personally experienced the magic of on-chain payments by frequently funding startups using USDC. We also know many startups that pay employees or suppliers in USDC/USDT. But a year ago, when AllianceDAO alum Felipe introduced us to Colombia’s peer-to-peer stablecoin market, we became deeply interested in this space.

Over the following months, we evaluated over 100 stablecoin-related startups serving users in Latin America, Africa, Southeast Asia, and Eastern Europe. The most striking observation was that the majority of startups with launched products showed early signs of product-market fit (PMF). By PMF, I mean monthly growth exceeding 10%.

In contrast, the vast majority of crypto startups outside this vertical show no signs of PMF at all.

The founder of Accrue, an African payment startup we eventually invested in, told us that stablecoins are ubiquitous in his family. His sister saved nearly a year’s tuition in stablecoins, protecting herself from the 130% depreciation of the Ghanaian cedi. She then used a stablecoin-backed debit card to pay her master’s tuition in Sweden. His brother regularly transfers money from GHS to CAD via Accrue and Kraken using stablecoins. His parents in Ghana send remittances to relatives in Nigeria through Accrue’s agent network using stablecoins.

Another African stablecoin startup we funded, GoBankless, shared a life-or-death story. A South African hospital refused to admit a patient from Mozambique until payment was settled. Because the transaction was cross-border (Mozambique and South Africa) and occurred outside regular banking hours, fiat payment methods failed. The patient and hospital ultimately settled via stablecoin. This isn’t an isolated incident—patients from neighboring countries often travel to South Africa for medical care due to poor or nonexistent local healthcare infrastructure.

These are everyday examples of people using stablecoins to solve urgent problems in their lives. This is the crypto-agnostic phase of stablecoin adoption.

Other Real-World Assets: Diversification

Stablecoins are just the first and most prominent type of real-world asset. Other asset classes are now appearing on-chain.

Today, about $3 trillion—roughly 1% of global wealth—is stored on-chain. Again, this is a staggering figure. People holding this wealth have two choices: keep it as value storage, or exchange it for something else.

Throughout crypto history, when such exchanges happened, they were mostly into another crypto-native asset—either hoping to sell higher later or generate yield. The problem with these crypto-native assets is that they are highly correlated and volatile. As the crypto asset class reaches maturity in size compared to other asset classes, diversification becomes essential.

Diversification is a simple but proven need. Bridgewater, one of the world’s largest hedge funds, built its entire philosophy—the All Weather Portfolio—on the idea that combining uncorrelated return sources generates higher risk-adjusted returns. Their status as the largest hedge fund by AUM proves investor demand for diversification. Similarly, Bitcoin ETFs saw strong demand because they offered traditional financial asset allocators an uncorrelated return source.

Real-world assets are the answer to crypto-native users’ demand for diversification, offering them novel, uncorrelated, and less volatile return streams. RWAs for crypto-natives are what Bitcoin ETFs are for traditional financial asset allocators.

In 2023, we were surprised to see MakerDAO grow its RWA portfolio from nearly zero to $4 billion in under a year, mostly in U.S. Treasuries. Recently, BlackRock launched a $100 million tokenized Treasury project with Coinbase. Ondo holds $200 million in Treasuries. Franklin Templeton has a $300 million on-chain Treasury fund. Competition is intensifying.

$4 billion may seem small—insignificant compared to the $150 billion stablecoin market. But that’s mainly because stablecoins have existed for nearly a decade. In contrast, Treasuries only became attractive after the zero-interest era ended—just two years ago. Users need time to trust new products. Do they track the index correctly? Is minting and redemption smooth? Is there enough liquidity in secondary markets?

After U.S. Treasuries come U.S. equities and U.S. real estate. Legal challenges are real, but once resolved, there’s no fundamental reason not to meet demand for tokenized U.S. stocks and real estate—just as with Treasuries. We expect most demand for U.S. stocks and real estate will come from abroad. A startup we funded, Dinari, which offers tokenized U.S. stocks, is seeing strong demand from China and Russia. Currently, international demand for U.S. equities and real estate remains largely unmet due to capital controls, difficulty opening brokerage accounts, and friction in cross-border fund transfers. For example, in China, capital controls make opening a Binance account easier than a U.S. stock brokerage account. In Russia, individuals face U.S. sanctions due to the Ukraine war, barring them from accessing American markets. If U.S.-based assets could trade freely on-chain, international investors would only need a fast fiat-to-crypto on-ramp.

A common economic objection to these products is that crypto-native assets and yields offer better returns. The reality is that the gap between these crypto-native assets and yields is too narrow. For instance, Ethena is effectively just ETH beta, as basis expands when ETH rises. In contrast, stocks and real estate are uncorrelated return sources capable of absorbing capital from the $300 billion on-chain wealth pool.

Once the infrastructure for these RWAs matures, we believe crypto-agnostic use cases will emerge. Examples include using stocks and real estate as loan collateral, or allowing anyone to construct global portfolios on-chain without navigating complex legal frameworks for each asset. But that will be the second stage—the crypto-agnostic phase of RWA adoption.

Conclusion

For years, we’ve asked ourselves: what will be our first non-speculative killer app? Mainstream media, traditional finance, and even the crypto community itself have failed to realize—we already have one. It’s stablecoins being used by crypto-agnostic users to hedge currency depreciation and conduct cross-border payments. Yet, because stablecoins don’t exhibit dramatic price movements and are often adopted in emerging markets, they’re largely ignored in Twitter discourse.

But stablecoins are only the first type of RWA. Demand from crypto-native users for tokenized on-chain Treasuries has been suppressed. The natural next steps are tokenizing equities, real estate, and even luxury watches. These historically uncorrelated, high-quality return sources are now accessible to trillions in on-chain wealth hungry for diversified investment opportunities.

Appendix: ALL12 Startups from the Stablecoins and RWA Alliance

Accrue is building an agent network for fast and affordable cross-border payments across Africa. Individuals or businesses interacting with the network transact in local fiat, while settlements occur via stablecoins. They have positive cash flow, payment requests growing over 20% monthly, and companies like Opera and Eco are building on their infrastructure for Africa.

GoBankless is another stablecoin-powered payment network in Africa. Just months into operations, they process over $1 million in transactions monthly. Demand is so strong they’re constrained by working capital.

Lulubit is a neobank in Central America. Beyond other offerings, they provide on- and off-ramps for stablecoins, cross-border payments, and credit cards enabling users to spend crypto on real goods and services. They’re growing 30% monthly.

Fractal Payments offers enterprise payment solutions, starting with crypto-native businesses. Unlike traditional financial cash flow products reliant on SWIFT, they leverage stablecoins to enable cheaper, faster cross-border payments. Their product has facilitated over $5 million in transaction volume, grows 30% monthly, and is used by leading global firms like Aragon, Zerion, and Orange DAO.

Villcaso: Most previous real estate RWA startups tokenized individual properties as NFTs, resulting in illiquidity. Villcaso instead tokenizes a basket of real estate assets. This fungible approach brings greater liquidity. Additionally, the token is legally structured to be DeFi-compatible. In other words, investors can seamlessly transfer, trade, collateralize, and stake their tokens within existing DeFi frameworks.

ZwapX: There’s a surprising overlap between luxury watch collectors and crypto investors. By tokenizing watches, ZwapX enables faster and more secure trading than traditional OTC markets, while also allowing collectors to digitally showcase their watches, much like NFT collectors. Their current TVL exceeds $1 million.

Dinari: Previously, most stock-based RWAs took derivative forms. At Dinari, tokens are 1:1 backed by actual shares. Like stablecoins and Villcaso, these tokens are DeFi-compatible. The founder previously built a unicorn in biotech—a field as regulation-heavy as crypto.

Fig: Similar to Ethena, Fig productizes vetted hedge fund strategies. Ethena is marketed as a stablecoin but is effectively a tokenized hedge fund generating yield via perpetual contracts. Likewise, Fig generates yield through options, making previously inaccessible strategies more widely available.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News