Circular Debt or Moderate Inflation: An Alternative Perspective on Restaking

TechFlow Selected TechFlow Selected

Circular Debt or Moderate Inflation: An Alternative Perspective on Restaking

Re-staking essentially reflects security in terms of the quantity of tokens staked.

Author: Zuo Ye

Ethereum has been a hotbed of innovation—at least it once was. Celestia introduced the concept of a data availability (DA) layer, and EigenLayer ignited the re-staking narrative. Technology-driven innovation eventually justifies price movements, and even Uniswap can still pump its token price by revisiting old topics like the fee switch.

However, growth driven purely by technology has its limits. Just as you might eat two extra bowls of rice in anger, but you can't punch through the Earth, the long-term ceiling for technological advancement is defined by "cycles"—most famously, the Kondratiev wave (or K-wave), which lasts roughly 50–60 years. If ChatGPT fails to open the door to the Fourth Industrial Revolution, we may have no choice but to face the Fourth World War armed with sticks and wood.

Ten thousand years is too long; we must seize the day.

We don’t have time for long cycles. There are shorter ones—like Bitcoin’s halving, which comes like clockwork every four years. Similarly, I anticipate that re-staked tokens on Ethereum will follow the price cycle I’ve summarized: Concept emergence → User attraction → Airdrop initiation → Listing → Short-term peak → Price correction → New catalyst → Surge again → Return to normalcy, repeating periodically until the market shifts to the next hype.

Even seizing the day may be too slow—understanding re-staking takes just five minutes.

-

Re-staking represents a classic debt-driven economy. From the outset, it faces pressure to generate returns. To retain value, it must deliver both LSD and ETH staking yields, making it more aggressive in pursuing high returns—offering higher yields than LSDs but also introducing greater risk.

-

Re-staking monetizes Ethereum's security. Previously, L2 rollups could only price services based on Ethereum’s block space—reflected in DA and gas fees. Re-staking standardizes and monetizes Ethereum’s security, offering equivalent security at a lower cost.

Let’s unpack the second point first. Only by understanding what product re-staking produces can we grasp the logic behind its pricing mechanism—and how it cleverly borrows your real ETH.

Security Overcompetition, Capital Overflow

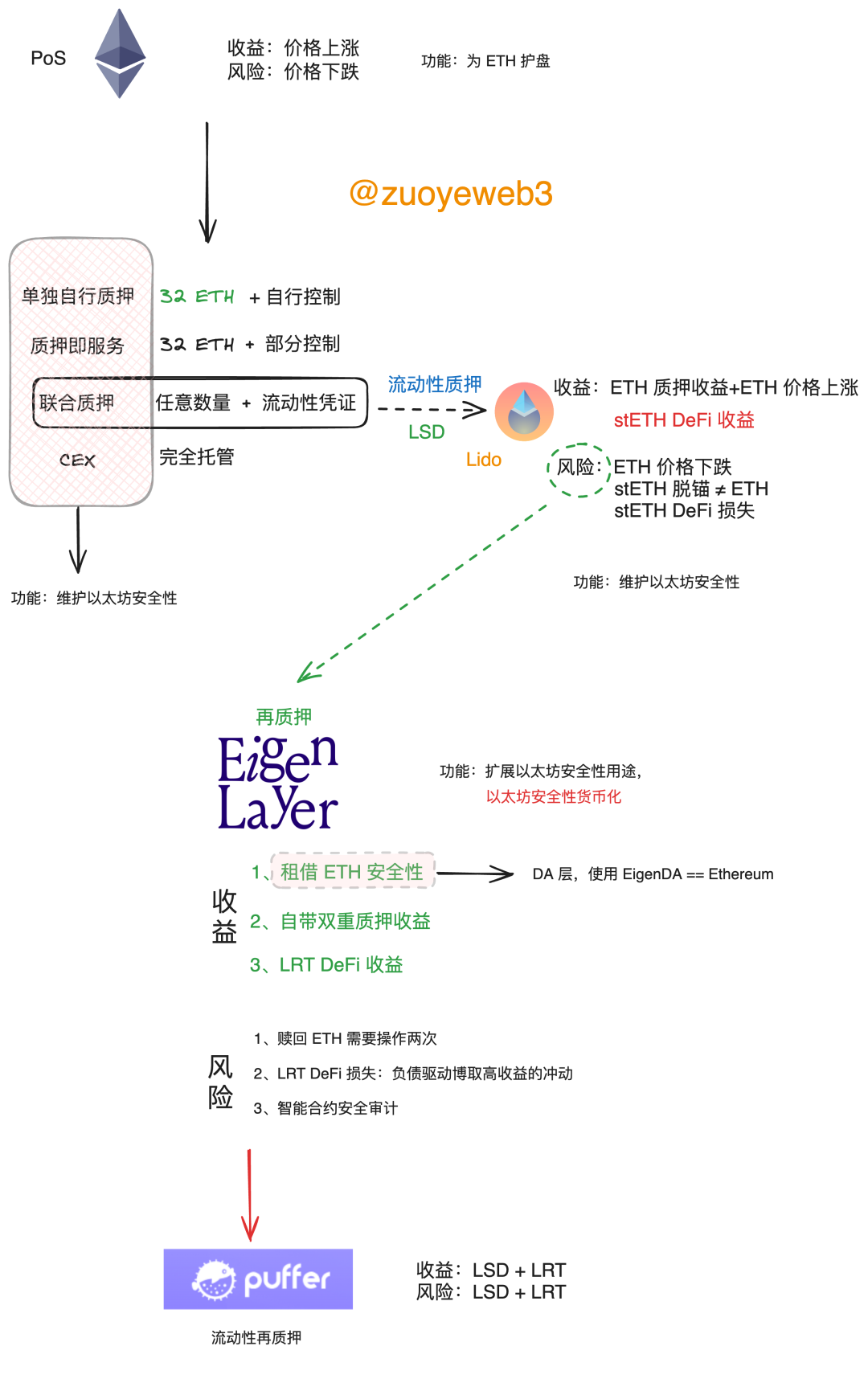

The product of re-staking isn’t complicated—it’s about leveraging Ethereum’s mainnet security. Whether ETH staking or LSD assets, they’re all part of Ethereum’s staking ecosystem. Previously, they contributed solely to Ethereum mainnet, indirectly supporting L2s and dApps. Re-staking isolates this security and directly allocates it to dApps or rollups in need, cutting out the middleman.

The logic behind re-staking

First, do not question the Proof-of-Stake (PoS) mechanism. Ethereum chose PoS, and re-staking extends from the principle that staking equals security. Right now, PoW and PoS stand roughly equal—Bitcoin dominates 50% of the market share, while nearly all other public chains default to PoS. The legitimacy of PoS is acknowledged by every major chain except BTC. This is the foundation of our discussion. Let’s recite together: PoS is secure, and the more ETH staked, the more secure Ethereum becomes!

At this point, the only real risk for ETH holders is depreciation in USD terms. In ETH-denominated terms, Ethereum is slowly moving toward de facto deflation—your remaining ETH will gradually become more valuable. (Ignoring risks like theft or confiscation.)

Second, to maintain network security and smooth operation, some ETH must be locked into the staking system—a necessary arrangement for network safety that everyone accepts. But taking people’s ETH without compensation would be unfair, so stakers receive rewards—interest.

The Ethereum Foundation outlines four staking participation models:

-

Solo home staking: Requires owning 32 ETH, purchasing hardware, setting up a node, and connecting to Ethereum. This is the most decentralized approach. The downside? It requires capital—over $100,000 at current prices.

-

Staking as a service: You own 32 ETH but don’t want to buy hardware. You delegate your ETH to a staking provider while retaining control. Downside: You still need to spend over $100,000 upfront.

-

Pooled staking—the familiar Lido-style liquid staking (LSD). You stake ETH and receive a 1:1 pegged token (e.g., stETH), redeemable back to ETH. You earn staking rewards and can use stETH in DeFi. No minimum required—ideal for retail. Risks include potential de-pegging of stETH and amplified losses in DeFi.

-

CEX: Deposit and earn yield. Simplest option. Risk is self-assumed. Won’t elaborate further.

Among these, Lido and CEX models dominate. Lido alone controls around 30% of the market, with Binance and Coinbase also leading. Effectively, Ethereum staking and liquid staking (LSD) have become synonymous. Even CEX offerings can be seen as a higher-trust variant of LSD.

But functionally, staking and liquid staking are identical—both provide security to the Ethereum network. The difference lies in liquidity incentives: LSD adds liquidity benefits on top of staking.

Re-staking enhances the original staking function—think of it as “moonlighting.” Through re-staking, the Ethereum staking network can now independently support dApps with security needs, while still securing the mainnet and earning staking rewards, LSD rewards, and re-staking rewards (depending on the collateral used).

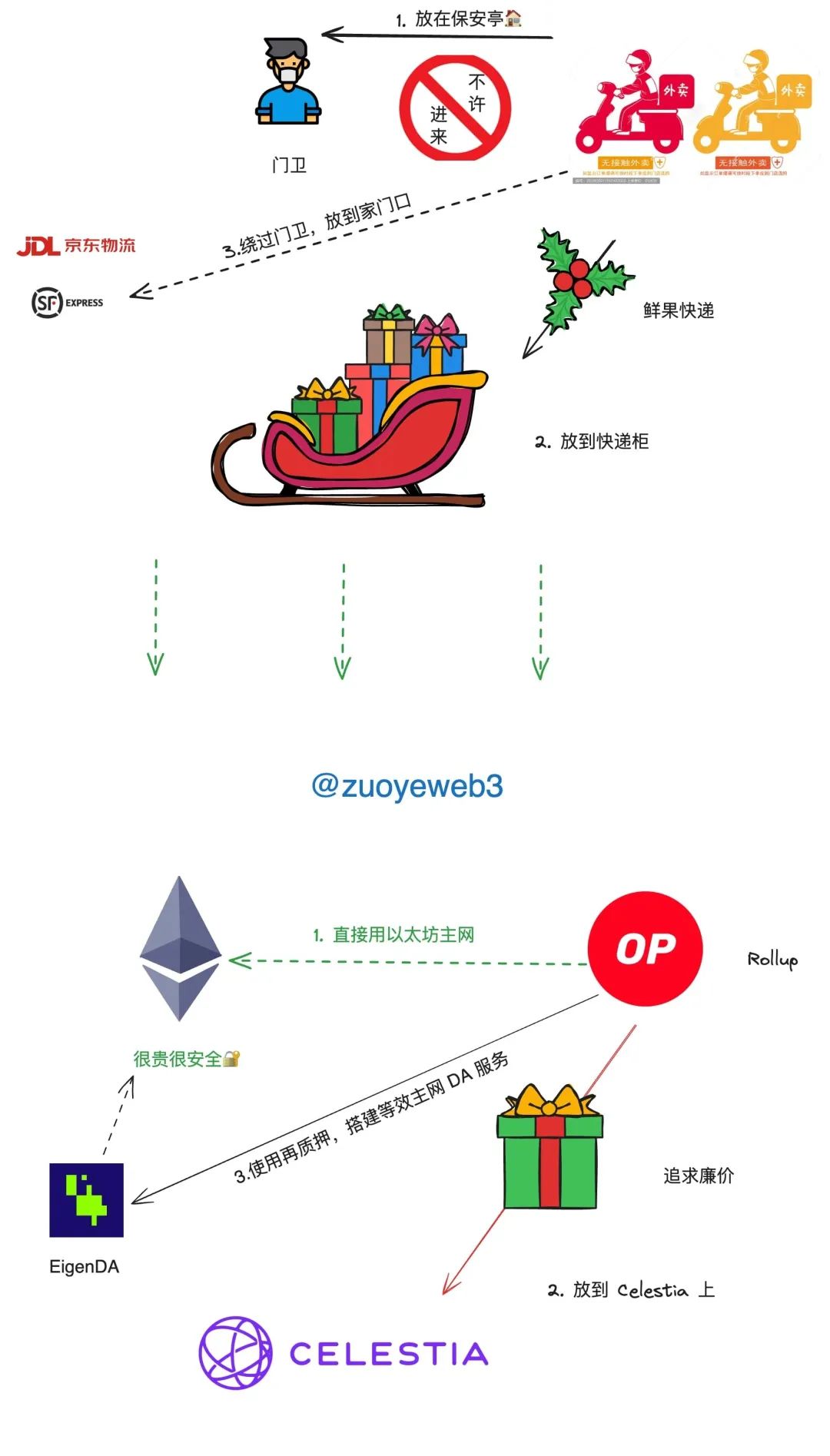

This repurposing of security isn’t hard to grasp. In real life, a security guard maintains neighborhood safety—but briefly holding a food delivery isn’t unreasonable. Leaving the package at the guardhouse is like entering the neighborhood. Rollups using EigenDA save money similarly. Placing it in a parcel locker is like using Celestia for DA—cheaper.

If you demand door-to-door delivery, you pay extra—like premium couriers such as JD or SF Express. That’s equivalent to using Ethereum as a DA layer: the safest but most expensive option. For technical details on how re-staking builds DA, see my previous article: Ethereum Rollups (STARKNET) War Ends, New Narrative DA Emerges.

Function diagram of re-staking

Before re-staking, choices were stark: use expensive but secure Ethereum mainnet or cheaper but less orthodox solutions like Celestia. Now, re-staking lets users leverage Ethereum’s security while reducing costs—all while preserving multi-layered staking yields and LRT liquidity.

DA is just one example. EigenLayer is essentially a bundle of smart contracts—not a blockchain or L2. Using EigenLayer means leveraging Ethereum itself. This may be hard to grasp at the software level, but analogies help.

Take Dogecoin: though PoW-based, it long lacked dedicated miners. Instead, LTC miners came bundled with Dogecoin mining—called merged mining. Similarly, Solana’s Saga phone sold poorly at $1,000, but when paired with the surging BONK token, it attracted buyers even at $10,000. This is another form of "merged mining"—mine Saga, get BONK free.

To recap: theoretically, rollups can use Ethereum’s security without re-staking, but direct interaction with mainnet is costlier and slower—well-known issues. Re-staking quantifies security via post-staking token amounts:

-

Re-staking tokens consist of ETH or LSD. Any dApp using them to build a validator network inherits Ethereum-level security;

-

The more re-staking tokens staked, the higher the security of Actively Validated Services (AVS)—same logic as more ETH staked = more secure Ethereum;

-

Re-staking services can issue their own tokens as participation proof—similar to stETH, though differences exist (discussed later).

Ultimately, EigenLayer has pushed re-staking’s security provision to its limit. Other projects merely iterate—supporting more chains or tweaking security models. For instance, Puffer shares both LSD and LRT yields, while ether.fi transitions from LSD to re-staking.

Yet our journey isn’t over. EigenLayer’s TVL exceeds $10 billion, Lido’s surpasses $30 billion, and total staked ETH sits around 30 million (~$100B). If derivatives should exceed spot value, both have room to grow—by multiples or even tens of times. But unlike universally recognized assets like USD, gold, or oil, Ethereum’s capital overflow will take time. This explains why LSDs haven’t fully succeeded and why re-staking hits ceilings—value needs time to mature.

Triangle Debt or Mild Inflation?

Re-staking expands functional boundaries and introduces stronger profit-seeking economics—not pejorative, just descriptive. Starting from ETH, moving to staking/LSD, then to re-staking, the three are interlocked: ETH provides security and yield assurance, staking/LSD offers liquidity tokens, and re-staking delivers quantifiable security—all ultimately tied back to ETH.

Note: ETH’s security and yield are embedded within LSD and re-staking. Even if LSD tokens enter re-staking systems, they can be unwound back to LSD and ultimately to ETH.

But here lies the problem: re-staking wraps two layers of staking. Each layer demands higher returns to cover costs. Suppose ETH staking yields 4%. To attract LSD tokens, re-staking must promise >4%. Thus, re-staking yields significantly exceed mainnet staking. If not, ETH won’t flow into re-staking.

This leads to a model where staking functions as an inflationary system. Three scenarios emerge:

-

Mainnet ETH staking yields are most secure—every ETH holder contributes to profits, akin to seigniorage. Holding ETH or USD means gradual erosion of purchasing power via inflation.

-

Liquid staking (e.g., Lido) issues 4%-yielding “corporate bonds.” stETH is a creditor note. Lido must sustain >4% yield to stay solvent. Each stETH minted creates a 1.04 ETH liability for Lido.

-

Re-staking stETH means the re-staking network buys this “corporate bond” at >1.04 ETH. With this reserve, it mints its own “currency”—various LRTs. This is credit creation. Crucially, re-staking creates tokens based on credit, unlike LSDs which create credit against real ETH (retailers’ hard cash). In short, re-staking plays the role of a bank.

I know this sounds abstract. Consider the infamous “triangle debt” crisis in late 1990s China, especially among state-owned heavy industries in Northeast China:

-

Large industrial firms couldn’t sell goods, so had no revenue to pay suppliers;

-

Small suppliers held unpaid invoices, lacked capital for expansion, fell into debt crises;

-

Both large and small firms turned to banks. Small private firms struggled to get loans; large firms got loans but still couldn’t sell, worsening inventory;

-

Bank NPL ratios soared. Firms found lending harder—near economic collapse, triggering mass unemployment.

On the surface, banks failed due to poor risk controls—loans were political mandates, not economic guidance. Deep down, it was a production failure: firms didn’t respond to market signals. Production and consumption were decoupled. Large firms ignored quality; small firms didn’t explore consumer markets.

From their view: large firms easily got loans, so no need to adapt; small firms believed selling to big firms guaranteed eventual payment via government-backed bank loans.

Though “resolved,” triangle debt was really offloaded—banks relieved, past debts forgiven. Only after crisis did firms start responding to market signals—but too late. Winners emerged from Yangtze and Pearl River Deltas.

Analogously: ETH is the large firm, LSDs are small suppliers, re-staking is the bank. It’s not just leveraged ETH—it’s a cycle: ETH → credit instruments → token creation → feeding back to ETH. The key? Yield across the loop must exceed ETH staking yield. Otherwise, insolvency looms—when debt outpaces growth, interest can’t be paid, let alone principal. This is today’s path for the US, Japan, and Europe—with the US faring best because dollar inflation (via USDT) is borne by everyone.

Debt economies aren’t sustainable, but they make sense. ETH exists because of staking—the ultimate political truth. Critics can attack re-staking for low deposits, centralization, or security flaws, but cannot challenge PoS itself.

Triangle debt vs. re-staking analogy

As producers, ETH sets the baseline yield. LSDs and re-staking must meet or exceed it. LSDs pass credit instruments to re-staking, which uses them to strengthen reserves and chase higher yields. As value flows from ETH to re-staking, circulating LRTs exceed 104% of underlying ETH. As long as users don’t redeem, wealth inflates invisibly—boosting re-staking’s buying power and solvency.

But risks follow closely. Re-staking is a credit-based monetary system—it must maintain trust to avoid runs. Luna-UST is a recent warning. Hence, EigenLayer accepts ETH, LSD, LP assets, etc.—diversification mitigates extreme risk.

LSD risk centers on stETH-ETH exchange rate. Theoretically, sufficient reserves or a white knight can ensure redemption during crises. But re-staking must promise high yields *and* guarantee redemptions. Accepting only ETH-correlated assets is safe but limits yield. Too many exotic assets raise solvency concerns.

EigenLayer’s TVL remains below Lido’s because excessive layering creates uncontrollable risks. Imagine: Lido can retreat to ETH base. EigenLayer must retreat to stETH, then to ETH. With other tokens, rollback and conversion get more complex. (Though actual mechanisms may simplify this.)

Like triangle debt, re-staking appears to run on promised yields—but its core is ETH’s strength. Excluding contract vulnerabilities, as long as ETH remains strong and EVM ecosystem TVL grows, the staking and re-staking networks can keep printing. With $100B in staked ETH, 10x scale means $1T.

As long as more individuals and institutions embrace ETH, re-staking becomes an efficient, mild inflation engine. We’ll enjoy a warm boom period—ETH-related assets rise together—until the tower collapses.

Conclusion

Re-staking monetizes Ethereum’s security. Its economic model is mild inflation—a slow, upward leverage, not violent 125x contract explosions. ETH-related asset appreciation won’t be as explosive as DeFi Summer.

But this has little to do with LDO (Lido’s token) or EigenLayer’s native token price. Ethereum’s core is ETH alone—no other mainnet-linked asset is tolerated. This is the final底线 for PoS Ethereum, and why Vitalik harshly criticized Celestia. All rewards go to ETH.

Compared to Bitcoin, Ethereum must create yield sources for ETH, whereas BTC is its own yield—a fundamentally different scenario. For other chains’ staking and re-staking, they must first justify their base chain’s necessity—or else it’s just a fast-paced gambling game.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News