27%!Is USDe, with an annual yield even higher than UST's, a Ponzi scheme?

TechFlow Selected TechFlow Selected

27%!Is USDe, with an annual yield even higher than UST's, a Ponzi scheme?

Arthur Hayes personally designed: a stable mechanism for hedging with equal amounts of spot ETH and futures ETH short positions.

Author: Nick Ford

Translation: Frank, Foresight News

On February 19, Ethena Labs, the issuer of the decentralized stablecoin USDe, launched its public mainnet with the goal of creating a synthetic dollar (USDe) based on Ethereum. At the time of writing, USDe's supply has already exceeded 285 million.

Meanwhile, the annualized yield of USDe is as high as 27%, reminiscent of the UST "death spiral" from Anchor Protocol that once offered a 20% annual return.

So what exactly is the mechanism behind USDe? Why does it offer such a high annualized yield? Is USDe a Ponzi scheme or the future of finance?

This article will analyze key topics including the challenges and market opportunities facing stablecoins, what Ethena Labs is, associated risks, and potential airdrop opportunities.

Challenges and Opportunities for Stablecoins

The vision of DeFi is to create a parallel financial system, but current stablecoins are fully dependent on the traditional world.

For example, in 2023, we witnessed firsthand the collapse of several prominent U.S. banks, including Silicon Valley Bank, highlighting that cryptocurrency can no longer rely on traditional financial systems.

This dependency creates systemic risk—existing stablecoin issuers could halt reserve backing, putting the entire industry at risk.

What then is the market opportunity? Imagine if we could create the next digital reserve currency for the world—what would that look like?

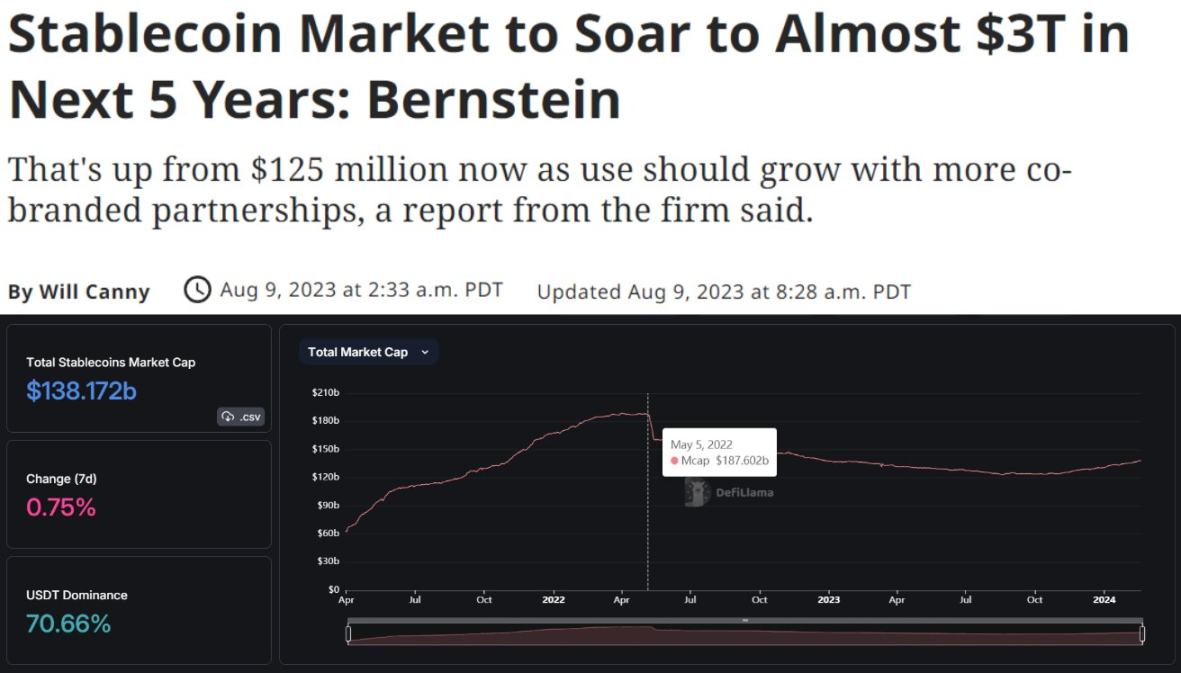

According to AllianceBernstein, a global asset management firm managing $725 billion in assets, the total market cap of stablecoins could reach $3 trillion by 2028.

Currently, the stablecoin market cap stands at $138 billion, peaking at $187 billion, indicating a potential 20x growth ahead!

While U.S. citizens have free access to the $30 trillion Treasury market, users elsewhere lack access to dollar-denominated savings accounts with yield. Thus, when countries face recession or hyperinflation, the U.S. dollar becomes a safe haven for most of the world.

This very challenge presents crypto with a unique opportunity—to provide a fundamental monetary product accessible to everyone, permissionlessly, across the globe.

What is Ethena Labs?

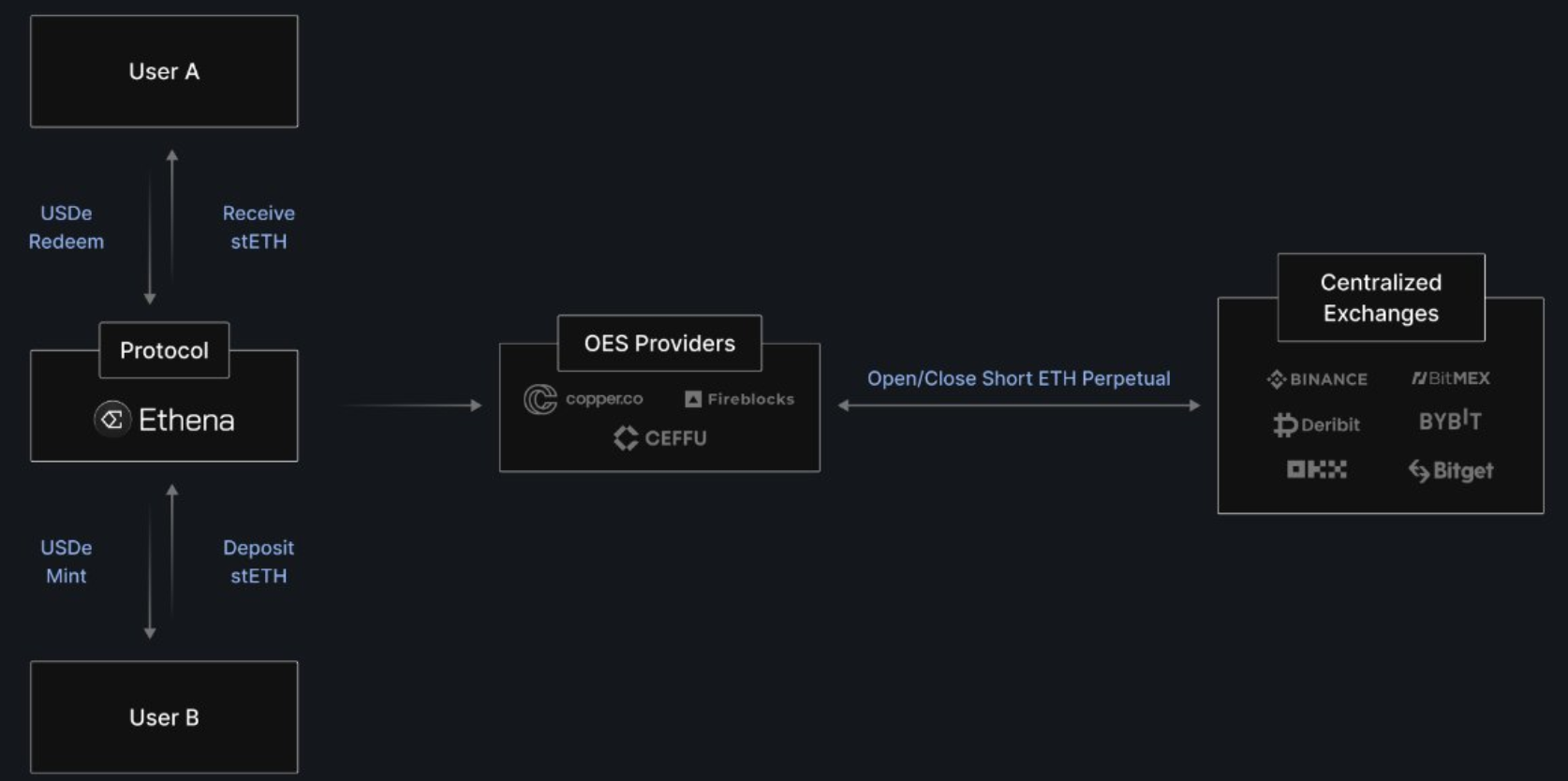

Ethena Labs is a digital dollar (USDe) protocol built on Ethereum that does not depend on traditional banking systems and offers fully transparent on-chain backing. It aims to provide a globally accessible savings option called the “Internet Bond” based on USDe.

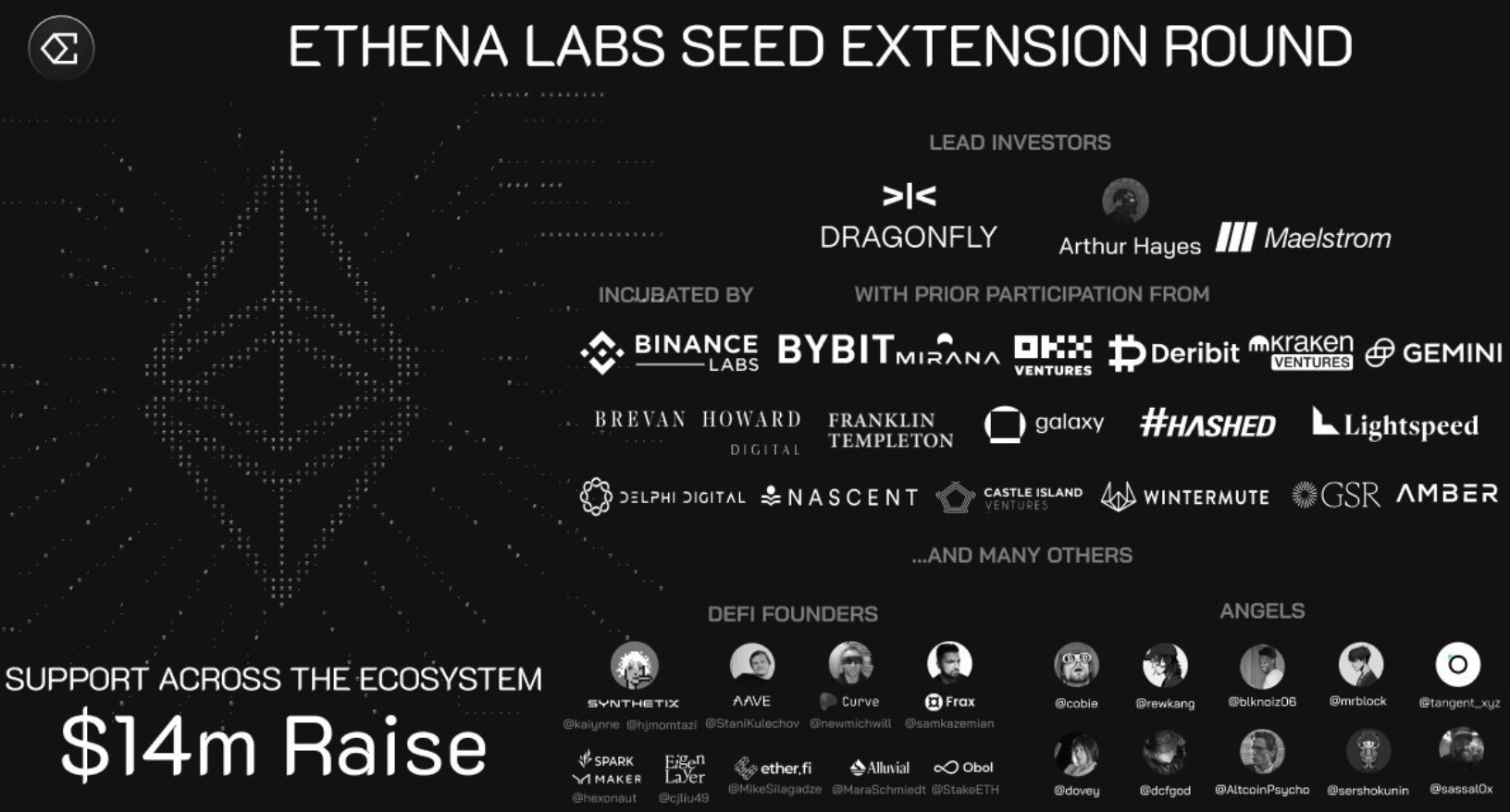

At the time of writing, Ethena Labs has raised over $14 million in funding from top-tier global investors, including Binance, BitMEX co-founder Arthur Hayes, Bybit, Mirana Ventures, Lightspeed, Franklin Templeton, and others.

Notably, angel investors include crypto researcher DCF GOD, crypto KOL Cobie, and even Ansem, an outspoken critic of Ethereum (Foresight News note: Ansem previously launched strong critiques against Ethereum during heated debates between ETH and SOL communities).

USDe’s Stability Mechanism

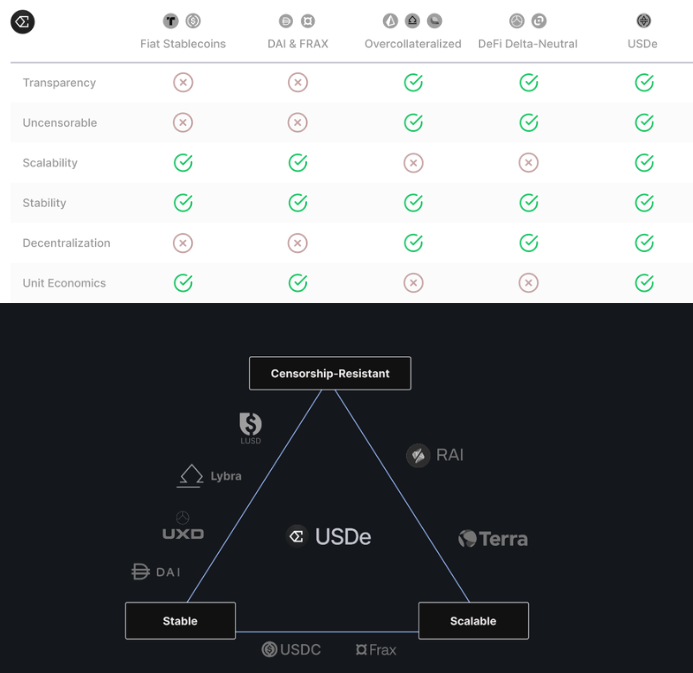

How is USDe different from other stablecoins?

Simply put, it aims to deliver the first censorship-resistant, scalable, and stable crypto-native solution—by using ETH as collateral and applying “delta hedging.”

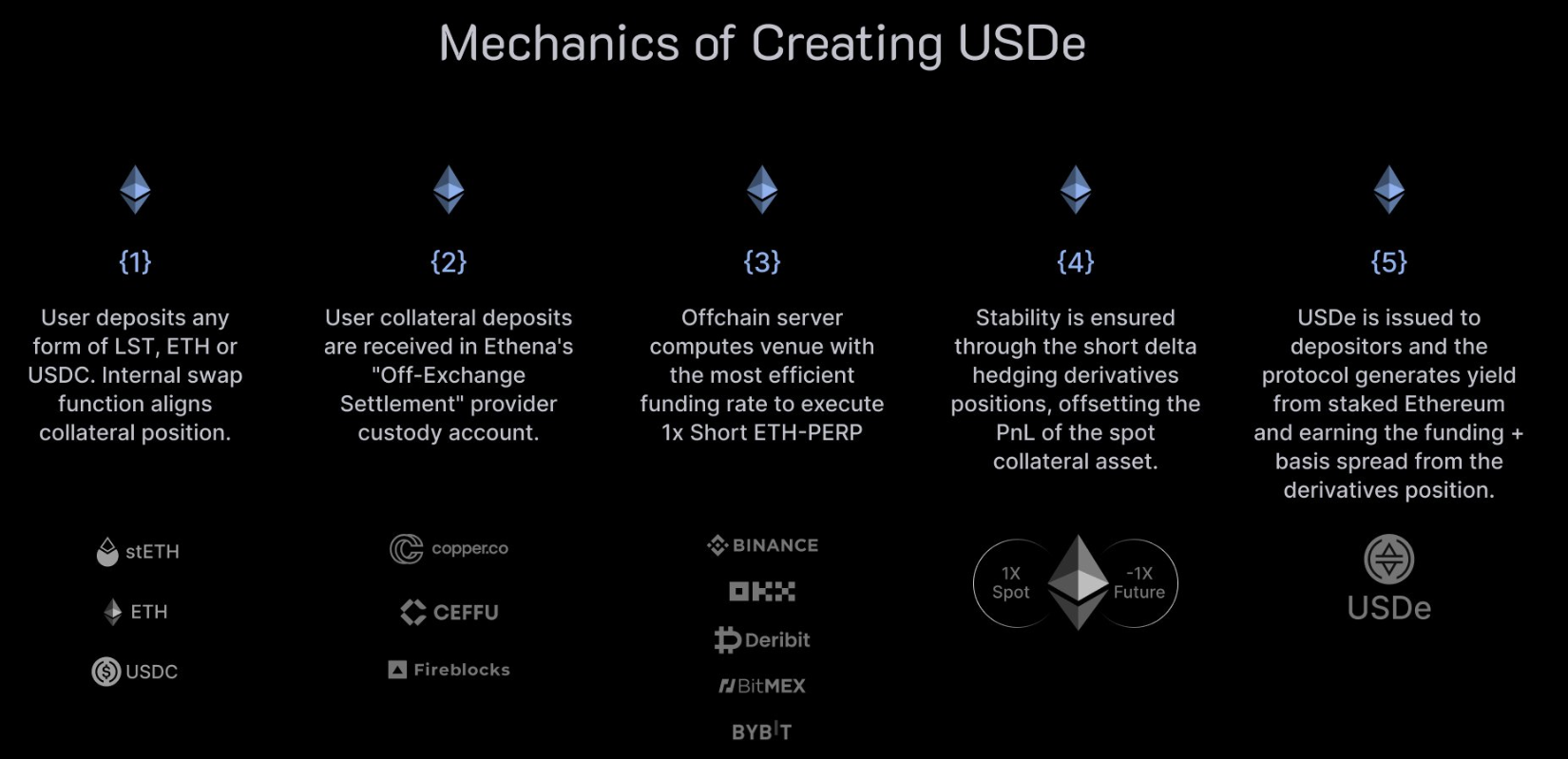

Specifically, how does USDe maintain its peg? It achieves automated pegging through programmatic “delta hedging” against the underlying collateral asset:

“Delta neutral” refers to an investment portfolio composed of related financial instruments whose value remains unaffected by small price movements in the underlying asset.

In short, USDe’s collateral consists of equal long positions in spot ETH and short positions in ETH futures.

Assuming ETH is priced at $1, buying 2 ETH in spot and selling 1 ETH in futures results in a net holding of 1 ETH, forming a “delta neutral” portfolio for USDe.

For example:

-

If ETH starts at $1, the total portfolio value is $1 + $0 = $1, so USDe = $1;

-

If ETH drops to $0.50, the portfolio value becomes $0.50 + $0.50 = $1, so USDe = $1 (same in case of price increase);

For more details on the anchoring mechanism and conceptual framework, see Arthur Hayes’ long-form essay “Dust on Crust.”

How does USDe generate a 27% annual yield? Ethena’s yield comes from two primary sources:

1. ETH LSD staking rewards;

2. Funding rate income from delta-hedged positions (i.e., short positions in perpetual futures);

Consider this example: After receiving 1 ETH, Ethena stakes it via LSD and earns an initial 3.5% annualized staking yield.

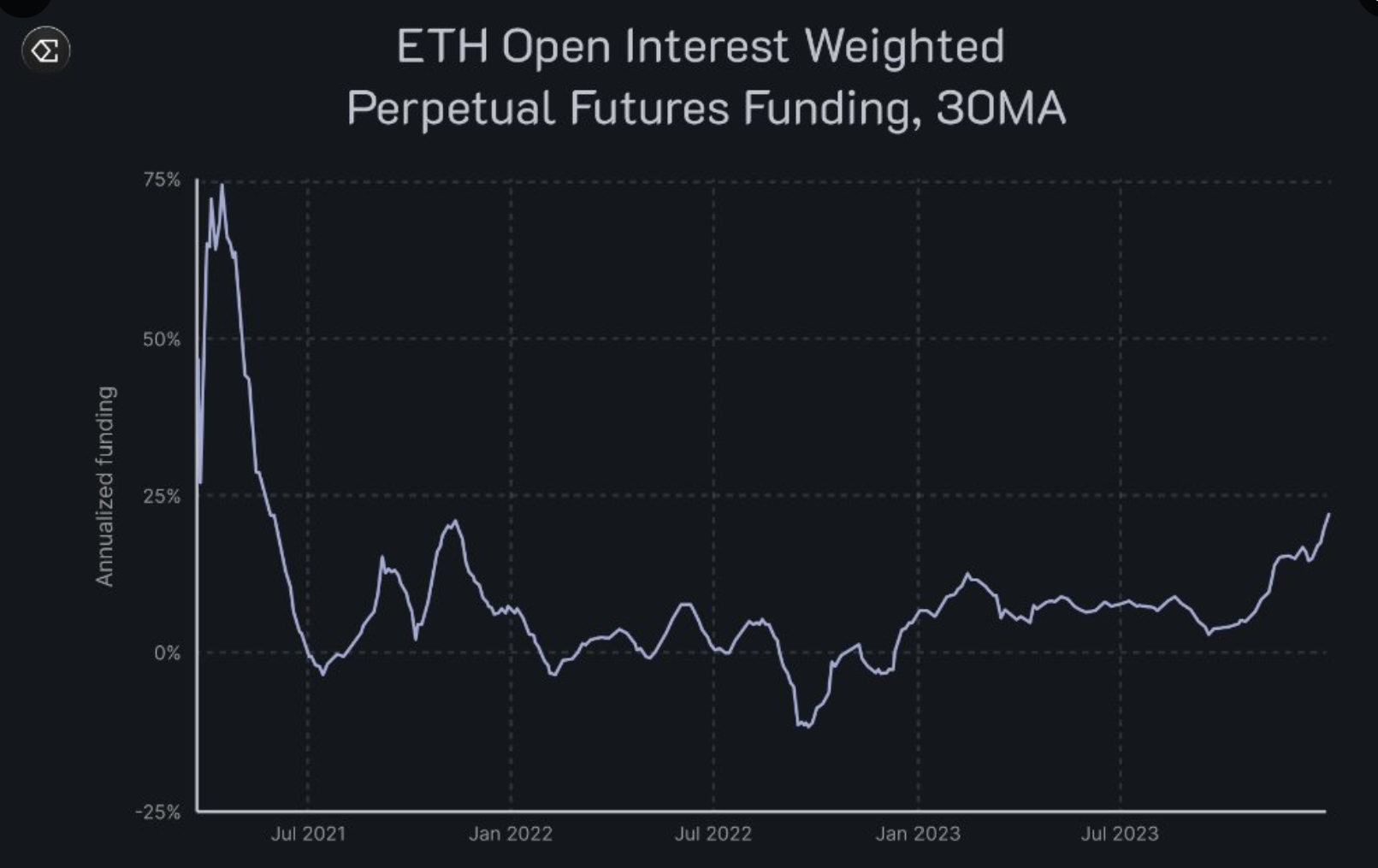

Simultaneously, Ethena opens a short position of 1 ETH in perpetual futures and earns funding rate payments from long-side traders (Foresight News note: historical data shows that funding rates are positive for most of the time, meaning short positions generally generate positive returns).

Combined, these two streams allow USDe to achieve a 27% annualized yield.

It follows that USDe’s high yield is especially secure when market participants are extremely bullish and eager to go long on ETH—because Ethena profits from being short during bull markets via funding rate income.

What are the risks involved?

As illustrated above, imagine if the market collectively begins shorting ETH—the funding rate income disappears, causing USDe’s annualized yield to become unattractive or negative, leading users to incur losses, with larger positions suffering greater losses.

What if we simply close the position then?

That might work, but opening and closing positions also incur costs. Moreover, Ethena has stated they believe negative yields won’t persist for long and expect a return to equilibrium.

Therefore, as the protocol evolves, it will be interesting to observe how Ethena handles such scenarios in the future.

If you're interested in deeper technical details, I encourage you to explore their documentation.

“Internet Bond”

Now circling back to another concept mentioned earlier—what is the “Internet Bond”?

I briefly mentioned that Ethena is building a dollar savings account. The “Internet Bond” combines ETH LSD staking yields with profits from perpetual contracts and futures markets (i.e., funding rate income).

In essence, it will be the first on-chain crypto “bond” serving global users just like a traditional dollar savings account.

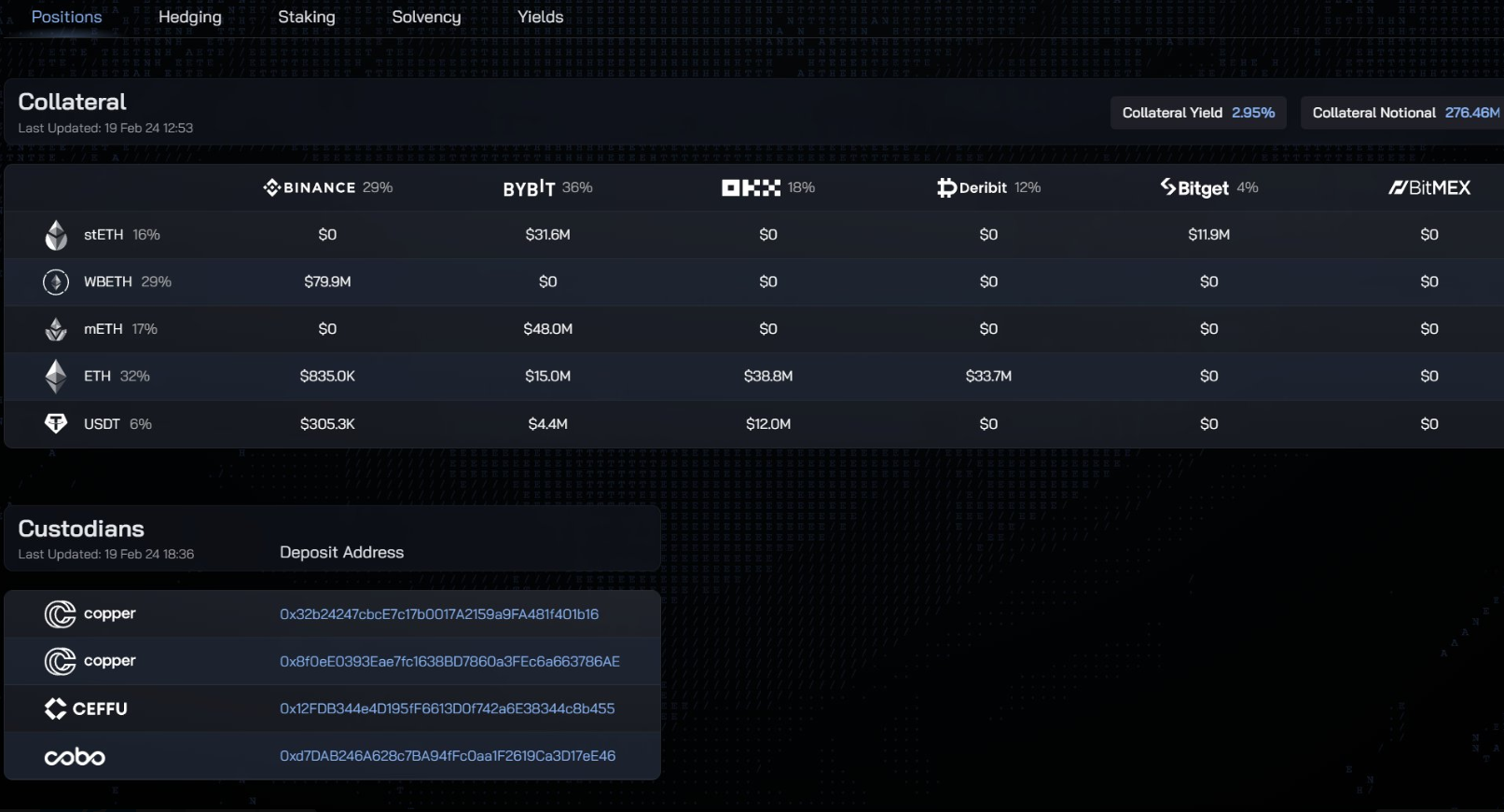

All information is fully transparent on-chain—we can view all open positions, wallet addresses, hedge positions, staking positions, and more via Ethena’s dashboard.

Potential Airdrop Opportunity?

Next, we’ll cover everything you need to know about maximizing potential airdrop rewards—this won’t be another grueling year-long grind.

Ethena has stated they aim to finalize the duration within three months, or once USDe supply reaches $1 billion—whichever comes first.

Users can earn “fragments” by purchasing USDe, staking sUSDe, or locking LP tokens.

Epoch #1

Epoch #1 will primarily reward users who provide liquidity to Curve’s USDe pools (USDe/USDC, USDe/crvUSD, USDe/DAI, USDe/mkUSD, and USDe/Frax).

Each dollar’s worth of LP locked earns 20 fragments per day.

Users will receive an additional 5 fragments per unlocked USDe, or 1 extra fragment per sUSDe held outside these LP pools.

Epoch #1 will end in two weeks, or once $100 million in LP tokens and an additional $100 million in locked USDe are reached—whichever occurs first.

The longer users participate in this epoch, the more fragments they accumulate.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News