This crypto cycle is different from previous ones—high-quality projects that have declined in price will still experience price recovery.

TechFlow Selected TechFlow Selected

This crypto cycle is different from previous ones—high-quality projects that have declined in price will still experience price recovery.

Downturns in the cycle are mostly driven by news and leverage; prices of good projects will eventually recover.

Author: Pantera Capital

Translation: TechFlow

Pantera Capital recently published a long-form article providing an in-depth and detailed analysis of their outlook for the 2024 crypto market, including investment strategies, key focus areas, and trend forecasts.

Due to the article's length, we have translated it in sections according to thematic content.

This is the third installment of the full series. In this section, researchers at Pantera analyze how the current bull market in crypto differs from previous cycles, noting that most downturns in this cycle have been driven by news events and leverage rather than fundamental issues—strong projects tend to recover, and blockchain fundamentals remain intact.

The current rally in cryptocurrencies is significantly different from prior market cycles.

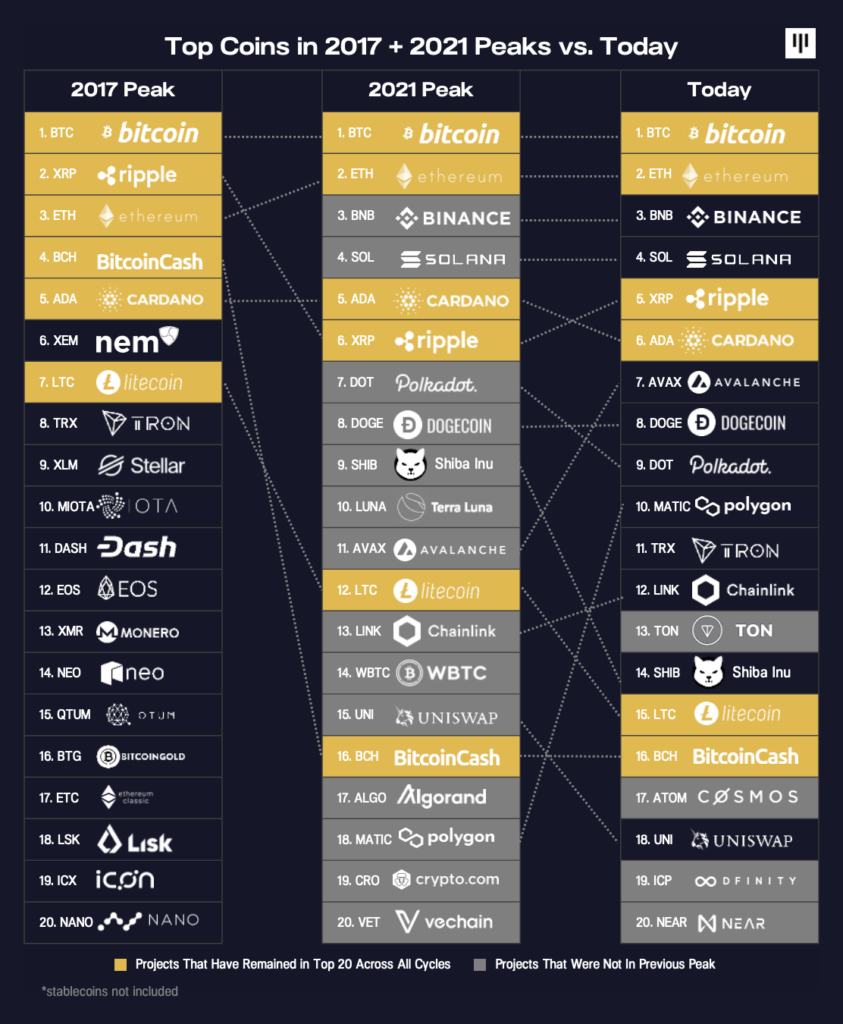

The peak of 2021 saw massive shifts among top tokens. During the ICO-driven boom of 2017, 14 out of the top 20 tokens quickly fell out of the top 20 rankings. Their declines were substantial. These fallen tokens now have an average market cap rank of 123 (Tron is the only project that dropped out and later returned). In hindsight, we can say this reflected a speculative bubble and hype around non-productive tokens.

All of the top 20 tokens from 2017 have since been completely replaced by tokens that didn’t even exist back then—an astonishing transformation.

What’s interesting about this cycle’s rebound is how little has changed—contrary to the previous cycle.

This time, the top six tokens, which account for 83% of market cap, are all unchanged. Eight out of the top ten remain the same. Fourteen tokens have stayed within the top 20.

Across all these cycles, Bitcoin remains constant. Only six tokens appear on all three lists (highlighted in gold above). Since Litecoin launched twelve years ago, only four tokens have held the second position: Litecoin, XRP/Ripple, Ethereum, and BCH.

Throughout 2022, we repeatedly discussed the idea that although the magnitude of this downturn resembles prior bear markets, it is unique because blockchains themselves did not face existential threats. Most price movements were driven by headlines related to leverage and bad actors. That’s why it’s not surprising to see the same projects making a comeback. They declined not because they were poor projects, but because they moved in sync with the broader market. Solana is a particularly strong example.

Three Main Types of Blockchains

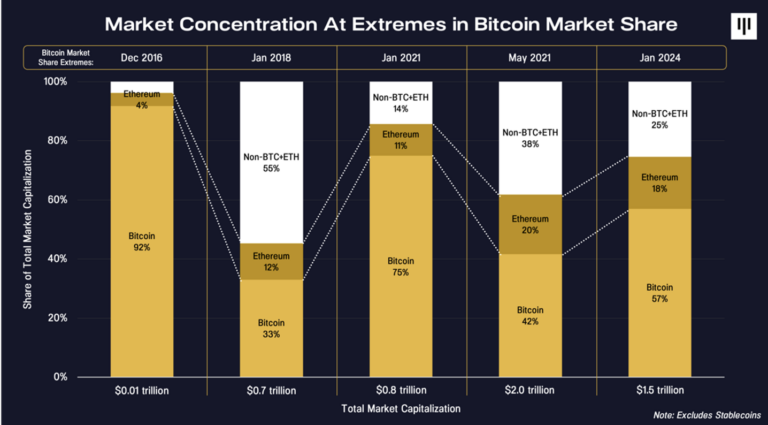

If we abstract the three main types of blockchains—Bitcoin, Ethereum, and the combined group of all other projects—we can observe their respective cycles.

First, note that Ethereum’s share has remained relatively stable since its establishment post-2017–18. The only significant drawdown occurred during the 2020–21 bull run, when competing highly scalable Layer 1 blockchains such as Solana and Avalanche gained notable market share.

Thus, it is Bitcoin and other tokens that fluctuate more dramatically.

One of the earliest non-Bitcoin tokens, Pantera’s first venture investment Ripple and its XRP token, reached an astonishing 27% market share on May 17, 2017.

The chart below shows the three main components of blockchains under Bitcoin’s most recent extreme market share scenarios since 2016.

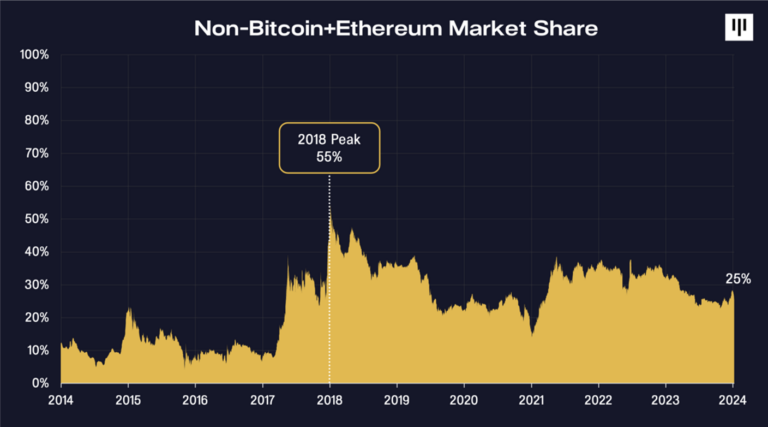

When Bitcoin and Ethereum’s market share hit their all-time lows in January 2018, the non-Bitcoin + non-Ethereum segment accounted for 55% of the market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News