The Risks of Restaking: Beyond Alluring Yields, a Fragile and Brittle House of Cards

TechFlow Selected TechFlow Selected

The Risks of Restaking: Beyond Alluring Yields, a Fragile and Brittle House of Cards

The EigenLayer airdrop could be the largest in crypto history.

Author: FRANCESCO

Translation: TechFlow

Restaking is a novel financial operation involving cryptocurrency, but it is not without risks. In this article, author FRANCESCO explores the concept of restaking, how it works, and the potential risks it entails. TechFlow has translated the full text.

This is my third article in the restaking series, initially focusing on EigenLayer, then delving deeper into the financial landscape of restaking.

Since then, we have seen new players emerge in the restaking space—such as Kelp DAO, Renzo, and $RSTK—that have attracted growing attention.

Restaking appears poised to become one of the key narratives driving 2024. However, despite widespread discussion about how restaking works and its benefits, it’s not all positive.

This article aims to step back and analyze restaking from a higher-level perspective, highlighting its risks and answering this question: Is it really worth it?

Let’s begin with a quick overview of the topic.

What is Restaking?

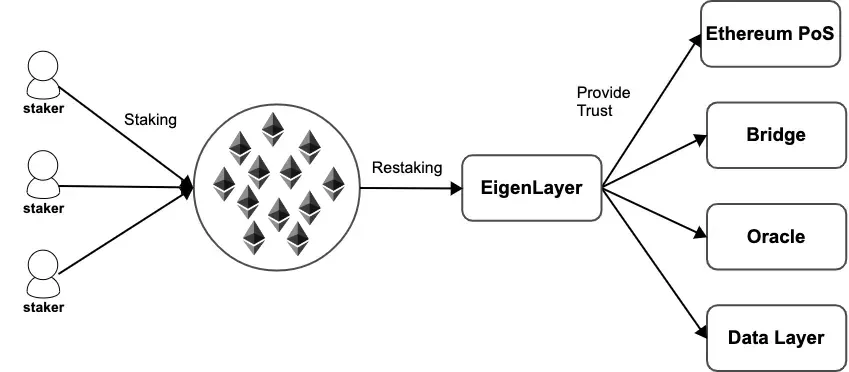

Proof-of-Stake (PoS) on Ethereum is a decentralized trust mechanism where participants secure the Ethereum network by committing their stake.

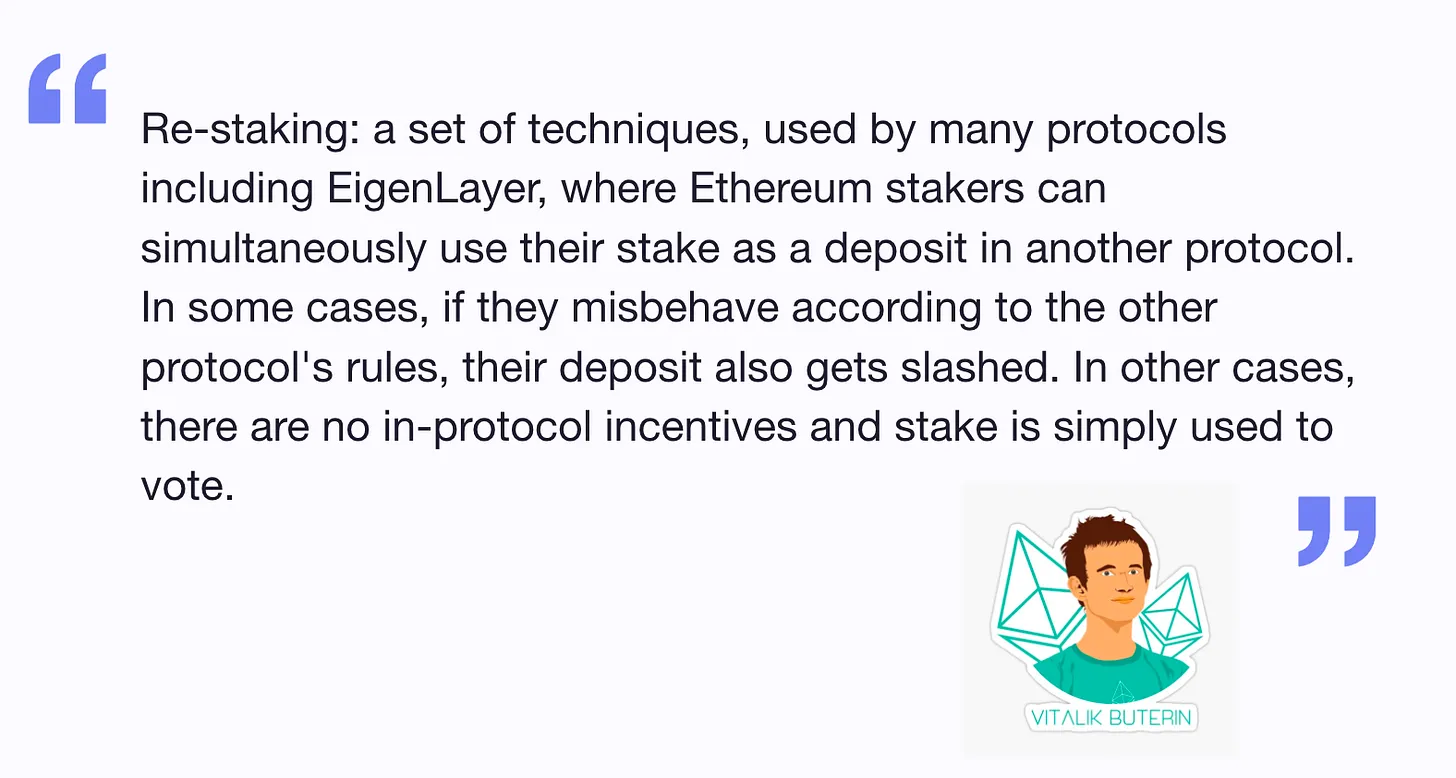

The idea behind restaking is that the same stake used to protect Ethereum's PoS can now also be used to secure many other networks.

Restaking can be understood as programmable staking, where users opt into various positive or negative incentives to secure other infrastructure.

In practice, EigenLayer’s restakers provide economic trust (in the form of staked ETH), so anything objectively verifiable can be subject to slashing.

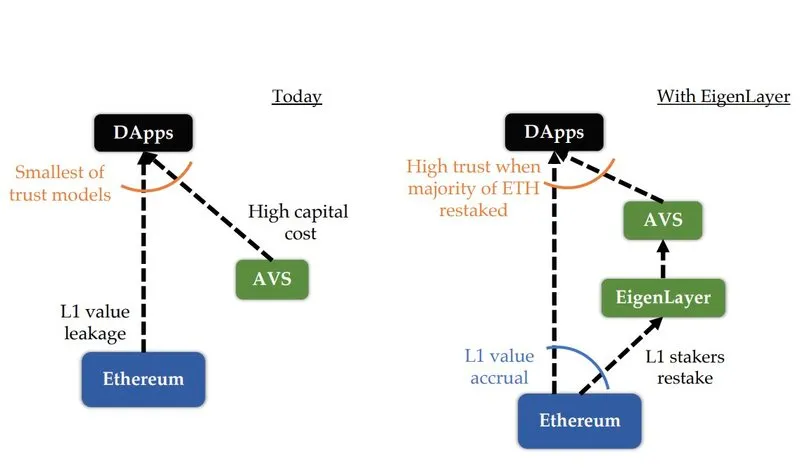

EigenLayer is "modularizing" Ethereum’s decentralized trust, allowing Actively Validated Services (AVSs) to leverage Ethereum’s security without needing to bootstrap their own validator sets—effectively lowering market entry barriers.

Typically, such modules require AVSs with their own distributed validation semantics. These AVSs are either secured by native tokens or are inherently permissioned.

Why Would Anyone Choose to Restake?

Simply put, it’s because of economic incentives and yield.

If standard Ethereum staking yields hover around 5% annually, restaking could offer an attractive additional return.

Exact reward estimates are currently unavailable, as they will depend on supply and demand dynamics within the Eigen Marketplace.

However, this introduces additional risks for stakeholders.

Beyond the inherent risks of staking ETH, when users choose to restake, they effectively delegate authority to the EigenLayer contract to slash their holdings if any AVS they’re securing experiences faults, double-signing, or similar issues.

Thus, restaking adds another layer of risk, as restakers could be slashed on ETH, on the restaking layer, or both.

Are the extra rewards worth the added risk of restaking?

Risks of Restaking

For stakers, restaking means you can choose to participate in multiple networks and increase your returns—which is why EigenLayer describes itself as the “Airbnb of decentralized trust.”

But it’s not all positive, as restaking introduces several significant risks:

-

ETH must be staked (or LSTs must be staked, meaning tokens are illiquid)

-

Smart contract risk associated with EigenLayer

-

Protocol-specific slashing conditions

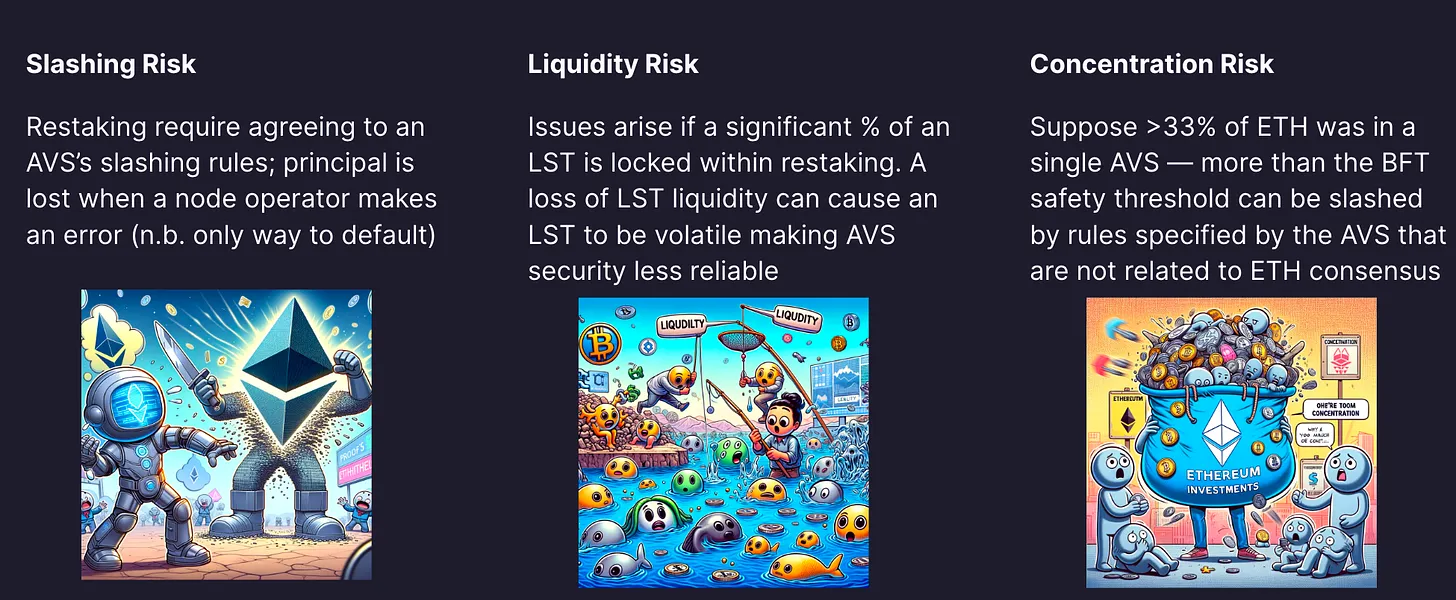

-

Liquidity risk

-

Concentration risk

Indeed, through restaking, users are leveraging a token already exposed to risk (from staking) and adding further layers of risk on top—resulting in cumulative risk exposure, as illustrated below.

Moreover, any additional narrative built on top of these foundations introduces further complexity and added risks.

Beyond individual risks to restakers, concerns have also been raised within the Ethereum developer community. As highlighted in Vitalik’s article on avoiding overloading Ethereum’s consensus, restaking raises important questions. The core issue is that restaking introduces new risk vectors for ETH staked to secure Ethereum’s mainnet by redirecting part of it to secure other chains.

Thus, if protocols with potentially flawed or weak security rules misbehave, their deposits could be slashed.

Developers and EigenLayer are working to coordinate and ensure these technological advances do not undermine Ethereum. Reusing the most critical layer to secure Ethereum is indeed no simple task.

Additionally, a key concern lies in the degree to which restakers can manage their own risk exposure.

Many restaking projects delegate the AVS whitelisting process to their DAOs. However, as a restaker, I would prefer to personally audit and decide which AVSs to stake to, in order to avoid malicious networks and reduce the likelihood of new attacks.

In summary, restaking is an interesting narrative worth exploring.

Yet, concerns raised by Vitalik and others should not be dismissed. When discussing restaking, it’s crucial to consider how it may impact Ethereum’s core security model.

It is fair to characterize restaking as layering additional risks atop Ethereum’s most fundamental security mechanism.

Ultimately, whether restaking is worthwhile is a personal decision.

Risks of Restaking:

-

Collusion risk: Multiple operators may simultaneously attack a group of AVSs and compromise security

-

Slashing risk: Restakers face slashing penalties from both ETH and AVS layers

-

Single point of failure: Withdrawal credentials derived from ETH credentials pose systemic risk to the mainnet

-

Validator centralization risk

-

Adding additional risks atop the mechanism securing Ethereum

Institutional Appeal of Restaking

Surprisingly, many institutions have expressed interest in restaking, viewing it as an additional reward layer on top of staking ETH.

However, they may conduct restaking through custodians rather than joining services that expose them to additional slashing risks.

Given the previously mentioned risks, it will be interesting to see whether retail or institutional investors show greater interest in restaking.

For those already involved, the extra yield on top of native ETH staking is appealing—but considering the risks, the returns may not justify the exposure for those seeking extreme gains.

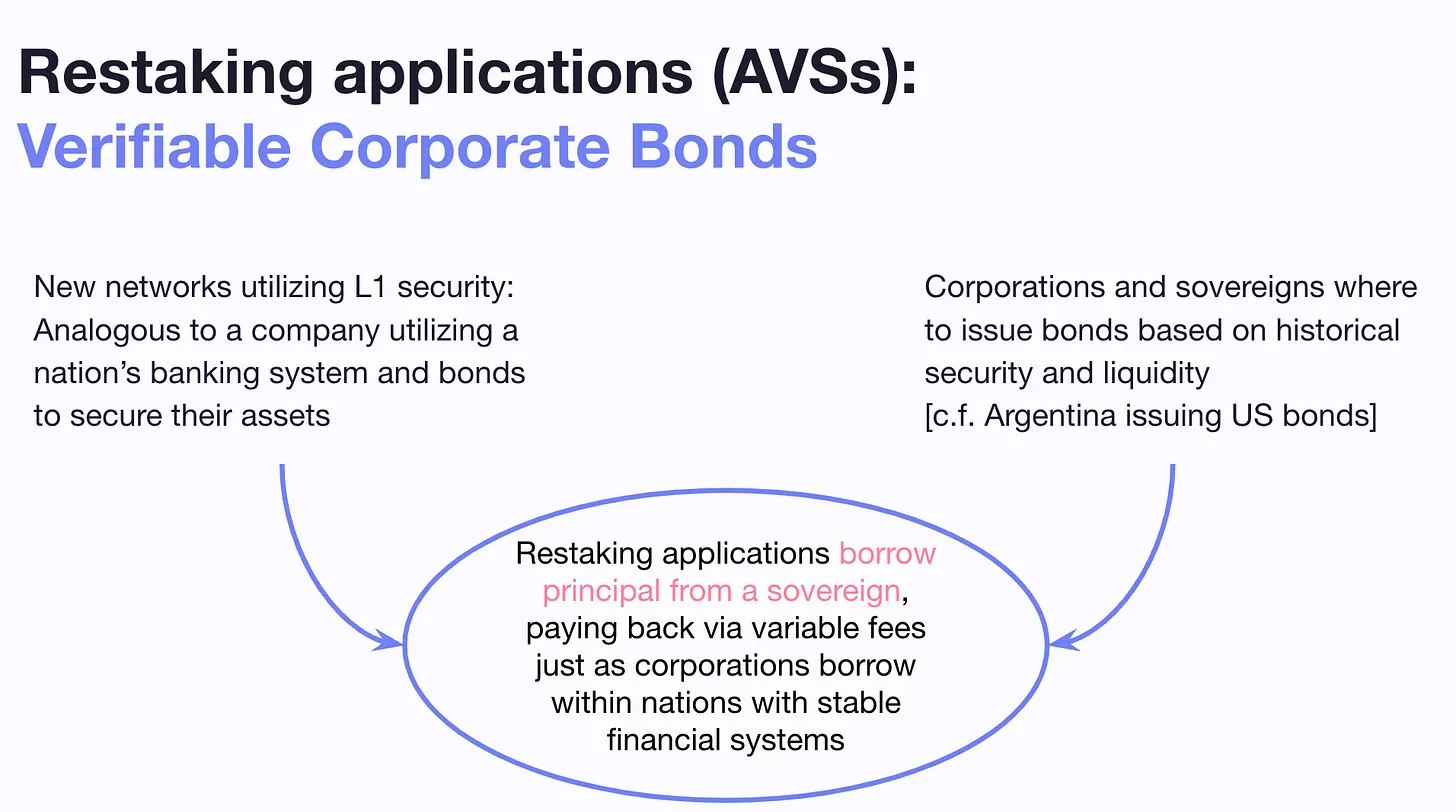

Restaking opens up new use cases for Ethereum as a financial instrument. Interestingly, some compare restaking to corporate bonds.

New networks seeking L1 security resemble how companies or nations use their financial systems to issue bonds and safeguard assets.

In crypto, Ethereum—with its broadest reach, highest liquidity, and strongest security—may be the only network capable of sustaining such a market, much like the safest nation within traditional financial economies.

Currently, much of the interest in restaking seems driven by speculation around the EigenLayer airdrop—one potentially the largest in crypto history.

How will things change after the airdrop?

Perhaps a realistic risk-and-return analysis may push some toward more productive alternatives.

I’d argue that much of the capital in restaking consists of mercenary capital that may exit post-airdrop.

To assess genuine user interest in this new narrative, the speculative component must first be separated out.

Personally, I believe the restaking narrative is somewhat overhyped and requires careful evaluation of current risks.

Key Takeaways on Restaking

-

Restaking allows AVSs to access Ethereum’s robust security layer at lower cost, reducing entry barriers

-

Users can restake ETH to improve capital efficiency and earn additional staking rewards

-

Restaking introduces additional risks on top of existing ones

Restaking is an exciting narrative that could unlock a wave of new use cases.

While full development of the Eigen marketplace may take about a year, some promising restaking experiments are already underway.

Some of Vitalik’s concerns relate to the centralization of staking power, which comes at the expense of independent stakers’ interests.

It will be interesting to observe how EigenLayer collaborates with the Ethereum Foundation to address these issues. But beyond these, other challenges remain.

How can we mitigate these risks?

Potential solutions include optimizing restaking parameters (TVL caps, slashing amounts, fee distribution, minimum TVL, etc.) and ensuring diversification across AVSs.

A direct step restaking protocols could take is enabling users to select different risk profiles when depositing for restaking.

Ideally, every user should be able to evaluate and choose which AVSs to restake into, without delegating this decision to a DAO.

This requires close collaboration between AVSs and EigenLayer to ensure ongoing efforts to minimize these risks.

The EigenLayer team is already working with the Ethereum Foundation to further coordinate and ensure restaking does not introduce systemic risks to Ethereum, LSTs, or the AVSs that rely on it.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News