Within One Year, Three Major DeFi Protocols Have Abandoned the ve Model—Can DeFi Still Survive?

TechFlow Selected TechFlow Selected

Within One Year, Three Major DeFi Protocols Have Abandoned the ve Model—Can DeFi Still Survive?

Why Can Curve Still Survive?

Author: Pink Brains

Translation & Editing: TechFlow

TechFlow Intro: Within 12 months, Pendle, PancakeSwap, and Balancer each abandoned the ve-token model—protocols whose combined TVL once reached several billion dollars. This article delivers the most systematic post-mortem analysis available: where each protocol broke down, what replacement mechanisms they adopted, and whether their underlying failure logic was shared. The conclusion isn’t “ve tokens are dead,” but a far more precise assessment: which protocols can successfully deploy ve models—and which cannot.

Full Text Below:

Three major DeFi protocols abandoned the voting-escrow (ve) model within a 12-month span in 2025. Though their breaking points differed, Pendle, PancakeSwap, and Balancer ultimately reached the same conclusion.

The voting-escrow tokenomics model (ve tokens) was meant to be DeFi’s ultimate token-economic solution: lock tokens, gain governance rights, earn fees, and permanently align incentives—all without centralized governance. Curve proved it could work, and dozens of protocols replicated this model between 2021 and 2024.

That has changed.

Over the past 12 months, three protocols with a combined TVL exceeding several billion dollars concluded that the mechanism did more harm than good—not because the theory was flawed, but because execution failed: low participation rates, captured governance, emissions flowing into unprofitable pools, and token price collapse despite growing usage.

Pendle: vePENDLE → sPENDLE

Where It Broke Down

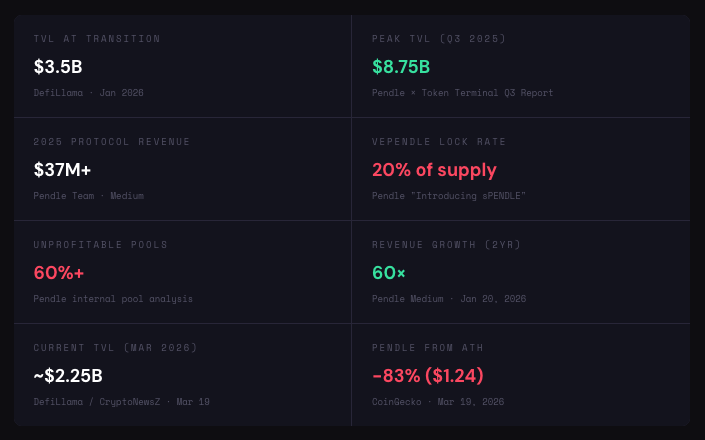

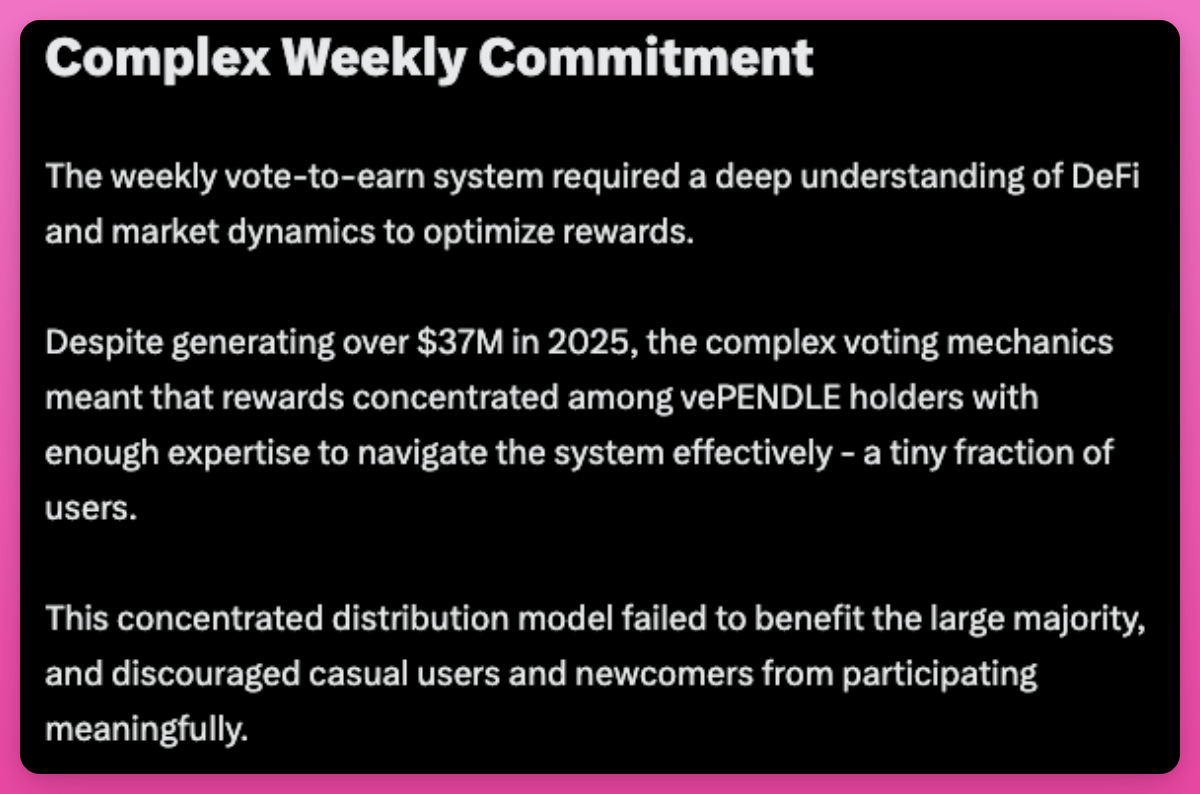

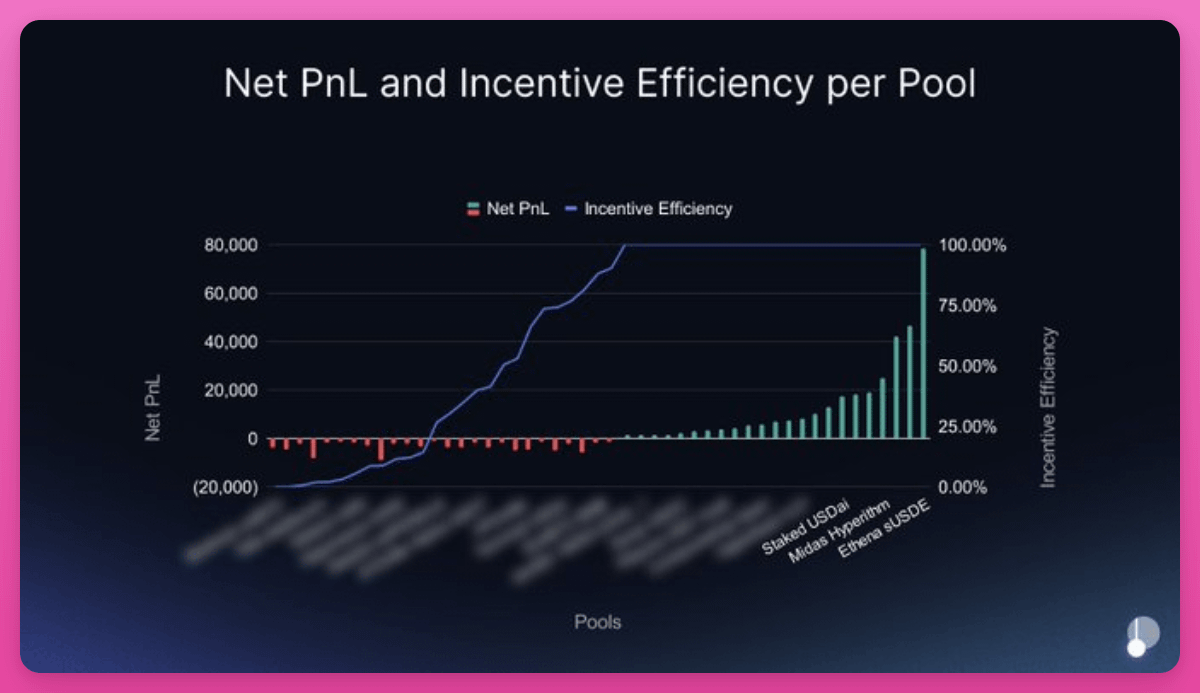

Pendle’s team disclosed that despite a 60x revenue increase over two years, vePENDLE had the lowest participation rate among all ve-token models—only 20% of the total PENDLE supply was locked.

This mechanism, designed to align incentives, excluded 80% of token holders. The fatal blow came from pool-level data: over 60% of emission-eligible pools were unprofitable.

A small number of high-performing pools subsidized the majority of value-destroying ones. Highly concentrated voting power meant emissions flowed to pools where large holders held positions—primarily wrapper products—before eventually reaching end users.

By contrast, Curve’s veCRV lock-up rate stands at over 50%, and Aerodrome’s veAERO lock-up rate is approximately 44%, with an average lock-up duration of ~3.7 years. Pendle’s 20% is simply too low. Compared to the opportunity cost of capital in yield markets, locking incentives lacked appeal. Meanwhile, Aerodrome has distributed over $440 million to veAERO voters as of March.

Replacement: sPENDLE

14-day withdrawal window (or instant withdrawal with 5% fee)

Algorithmic emissions (reduced by ~30%)

Passive rewards, limited to key PPP votes

Transferable, composable, and re-stakable

80% of revenue → PENDLE buybacks

sPENDLE is a 1:1 liquid staking token pegged to PENDLE, with rewards sourced from revenue-backed buybacks—not inflationary emissions. The algorithmic model cuts emissions by ~30% while directing capital toward profitable pools. Existing vePENDLE holders receive loyalty multipliers (up to 4x, decaying over two years starting from the January 29 snapshot). A wallet affiliated with Arca accumulated over $8.3 million in PENDLE within six days.

Not everyone agrees with this decision. Curve founder Michael Egorov maintains that ve tokenomics remains an exceptionally powerful mechanism for incentive alignment in DeFi.

PancakeSwap: veCAKE → Tokenomics 3.0 (Burn + Direct Staking)

Where It Broke Down

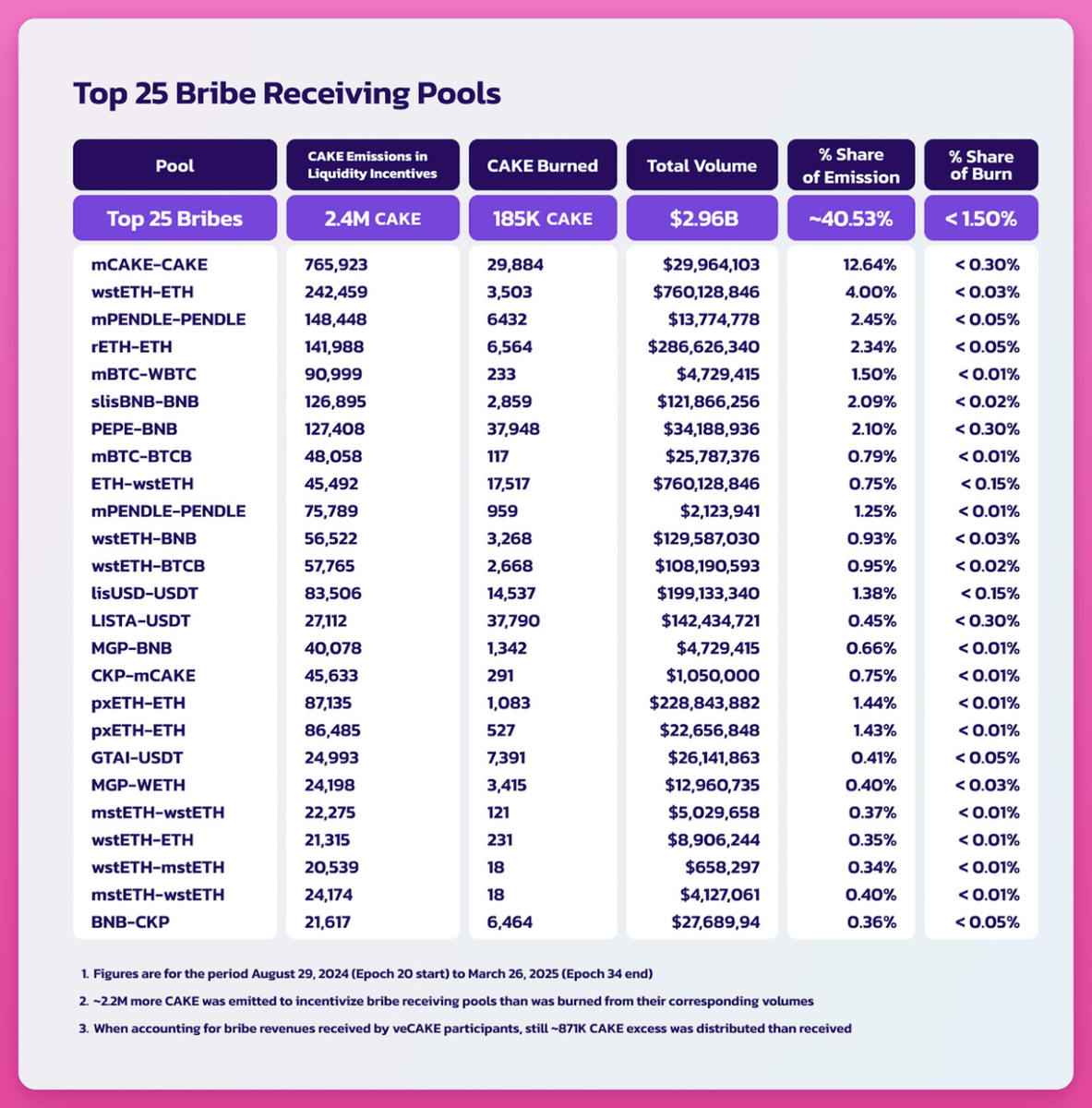

PancakeSwap’s veCAKE was a textbook case of bribery-driven resource misallocation. Its gauge voting system had been captured by Convex-style aggregators—most notably Magpie Finance—which extracted emissions while delivering minimal real liquidity benefit to PancakeSwap.

Data prior to shutdown: Pools receiving >40% of total emissions contributed less than 2% of CAKE burns. The ve model created a bribery market where aggregators extracted value, while fee-generating pools remained under-incentivized.

Yet this shutdown was deliberately engineered. Michael Egorov called it “a textbook governance attack,” suggesting insiders erased existing veCAKE holders’ governance rights—and potentially forced unlock of their own tokens post-vote. Cakepie DAO, one of the largest CAKE holders, challenged the vote citing irregularities. PancakeSwap offered up to $1.5 million in CAKE compensation to Cakepie users.

Replacement: 100% Fee Revenue → CAKE Burn

Team-managed emissions

1 CAKE = 1 vote (simple governance)

~22,500 CAKE per day (target: 14,500)

100% fee revenue → CAKE burn, no dividends

Target: 4% annual deflation, reaching 20% by 2030

All locked CAKE/veCAKE positions unlocked penalty-free, with a 6-month 1:1 redemption window. Dividend distributions replaced by burns; burn rate for key pools increased from 10% to 15%. PancakeSwap Infinity launched concurrently, featuring a redesigned pool architecture.

Post-transition results: Net supply decreased by 8.19% in 2025; 29 consecutive months of deflation; 37.6 million CAKE permanently burned since September 2023; over 3.4 million burned in January 2026 alone; cumulative trading volume: $3.5 trillion ($2.36 trillion in 2025).

The deflationary model looks strong—but CAKE still trades near $1.60, down ~92% from its all-time high.

Balancer: veBAL → Risk Liquidation (DAO + Zero Emissions)

Where It Broke Down

Balancer’s failure was a cascading collapse combining governance capture, security incidents, and economic insolvency.

The whale war struck first. In 2022, whale “Humpy” manipulated the veBAL system to direct $1.8 million in BAL emissions to his CREAM/WETH liquidity pool over six weeks. By comparison, that pool generated only $18,000 in revenue for Balancer during the same period.

Then came the exploit. A rounding flaw in Balancer V2’s swap logic was exploited across multiple chains, draining ~$128 million. TVL dropped $500 million in two weeks, and Balancer Labs faced another wave of untenable legal risk.

Replacement: 100% Fees → DAO Treasury

BAL emissions reduced to zero

100% of fees allocated to DAO treasury

Fixed-price BAL repurchase program for exits

Focus areas: reCLAMM, LBP, stablecoin pools

Maintained lean team via Balancer OpCo

The old DeFi model—built around token rewards—is being phased out. Despite tokenomic challenges, Martinelli noted Balancer “still generates real revenue”—over $1 million in the past three months: “The issue isn’t that Balancer doesn’t work—it’s that the economics surrounding Balancer don’t work. And those are fixable.”

Whether a lean DAO can sustain $158 million in TVL without incentives remains an open question. Notably, Balancer’s market cap ($9.9M) currently sits below its treasury ($14.4M).

Underlying Mechanisms

These three exits are symptoms—the root cause is structural.

A recent analysis by Cube Exchange outlines three scenarios where ve token models may fail.

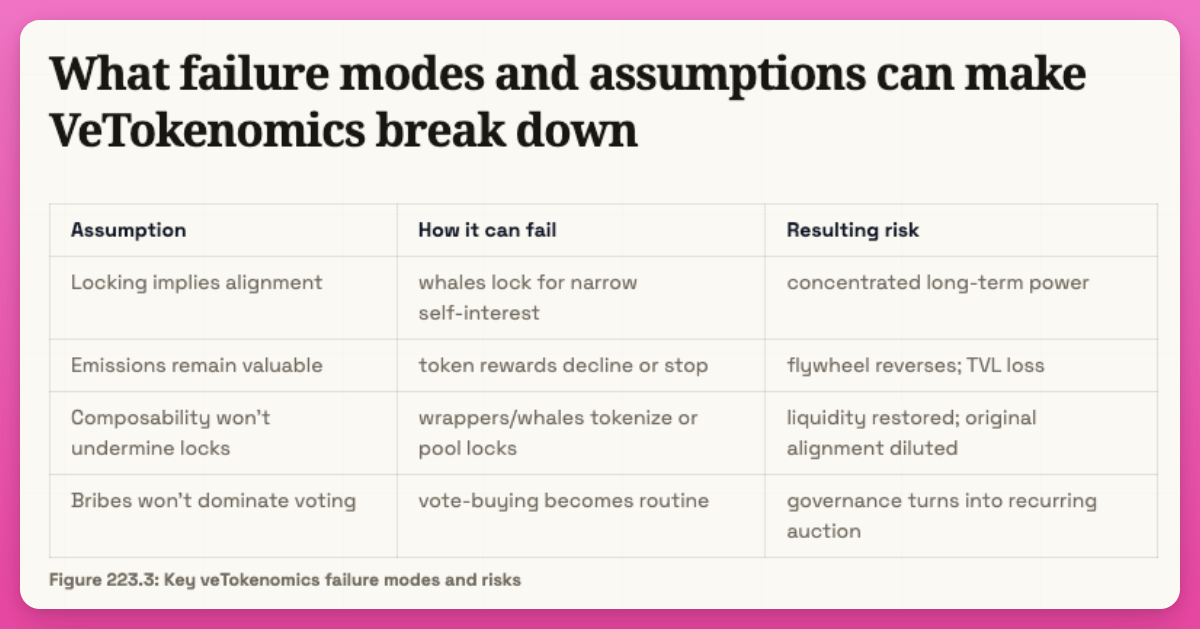

Hypothesis 1: Emissions must retain value. If token price collapses, emissions lose value → LPs exit → liquidity, volume, and fees decline → further selling pressure. This classic reverse flywheel has played out on CRV, CAKE, and BAL.

Hypothesis 2: Locking must be real. If locked tokens can be wrapped into liquid versions (e.g., Convex, Aura, Magpie), “locking” loses meaning—and creates exploitable inefficiencies.

Hypothesis 3: There must be a genuine allocation problem. ve models work only if the protocol faces recurring decisions about where to direct incentives (e.g., AMMs). Without that, gauge voting becomes unnecessary overhead.

Diagnostic test: Does the protocol face a real, recurring allocation problem such that community-led emissions generate significantly more economic value than team-led allocations? If not, ve tokenomics adds complexity without value.

Fees-to-Emissions Ratio

The fees-to-emissions ratio equals the dollar value of fees earned divided by the dollar value of emissions distributed. When this ratio exceeds 1.0x, the protocol earns more from liquidity than it spends to attract it. Below 1.0x, it subsidizes loss-making activity.

Here’s a detail revealed by Pendle’s exit: aggregate ratios mask pool-level realities. Pendle’s overall fee efficiency exceeded 1.0x (revenue > emissions). But when dissected pool-by-pool, over 60% of pools were individually unprofitable. A few high-performing pools—likely large stablecoin yield markets—subsidized the rest. Manual gauge voting steered emissions toward pools benefiting large voters—not those generating the most fees.

The same dynamic occurred at PancakeSwap—just reflected in CAKE burns instead of emissions.

Liquidity Locking Paradox

ve tokenomics creates a problem: capital locking is inefficient. Liquidity-locking products solve this by wrapping locked tokens into tradable derivatives. Yet in solving capital efficiency, they create governance centralization. This is the core paradox embedded in every ve tokenomic design.

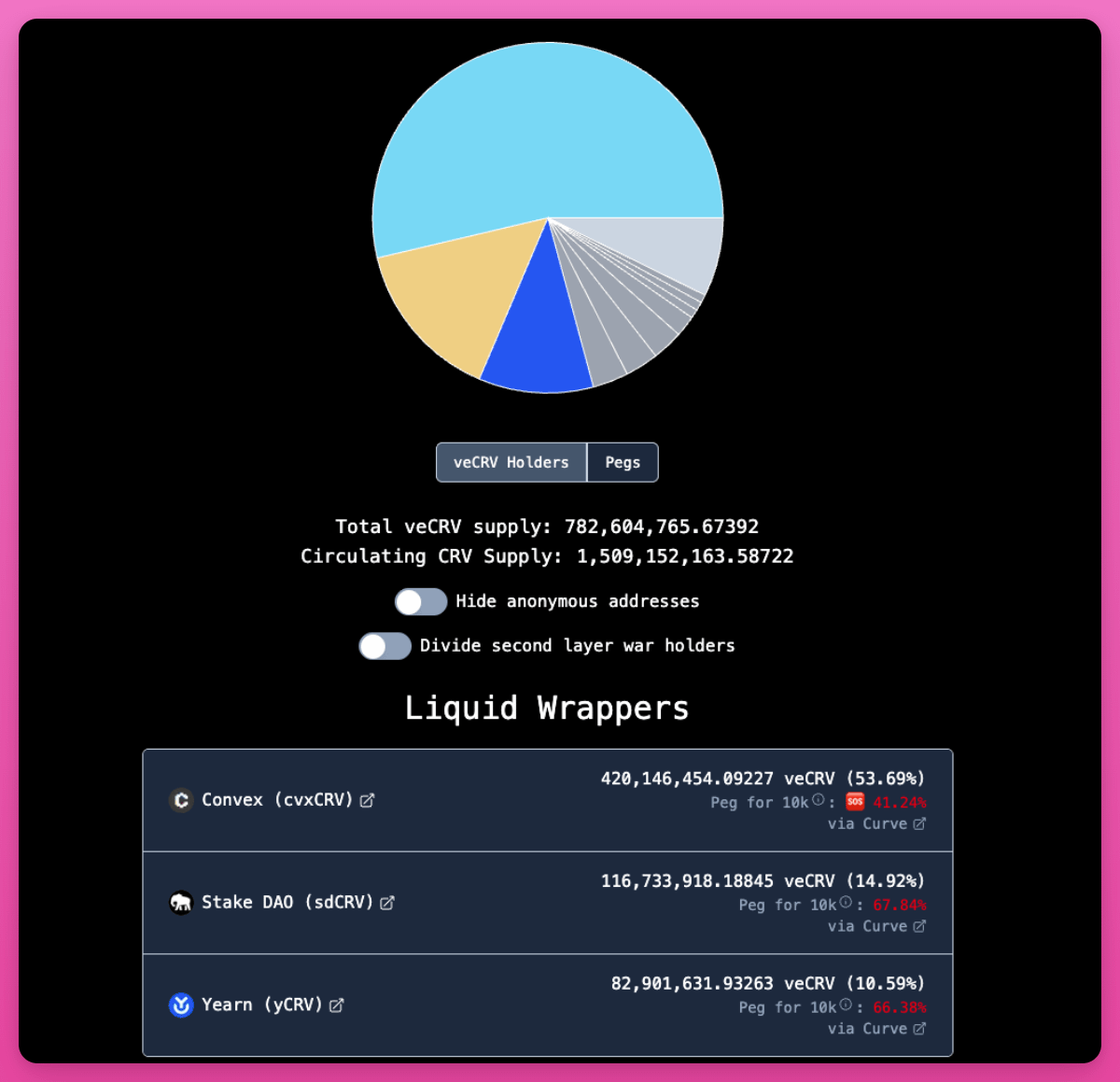

In Curve’s case, the paradox yielded stable—though centralized—outcomes. Convex holds 53% of all veCRV; StakeDAO and Yearn hold additional shares. Individual governance is effectively mediated through vlCVX voting via Convex. Crucially, Convex’s incentives are aligned with Curve’s success—its entire business depends on Curve functioning well. Centralization is structural, not parasitic.

In Balancer’s case, the paradox proved destructive. Aura Finance became the largest veBAL holder—and de facto governance layer. With no other strong competitors, a hostile whale (“Humpy”) independently accumulated 35% of veBAL and manipulated gauge caps to extract emissions.

In PancakeSwap’s case, Magpie Finance and its aggregators captured gauge voting via bribes—and directed emissions to pools delivering minimal value to PancakeSwap.

ve tokenomics requires locked capital to function—but locking capital is inefficient—so intermediaries emerge to “unlock” it. In doing so, they concentrate the very governance power that locking was meant to decentralize. The model creates the conditions for self-capture.

Curve’s Counterargument: Why ve Tokenomics Still Matters

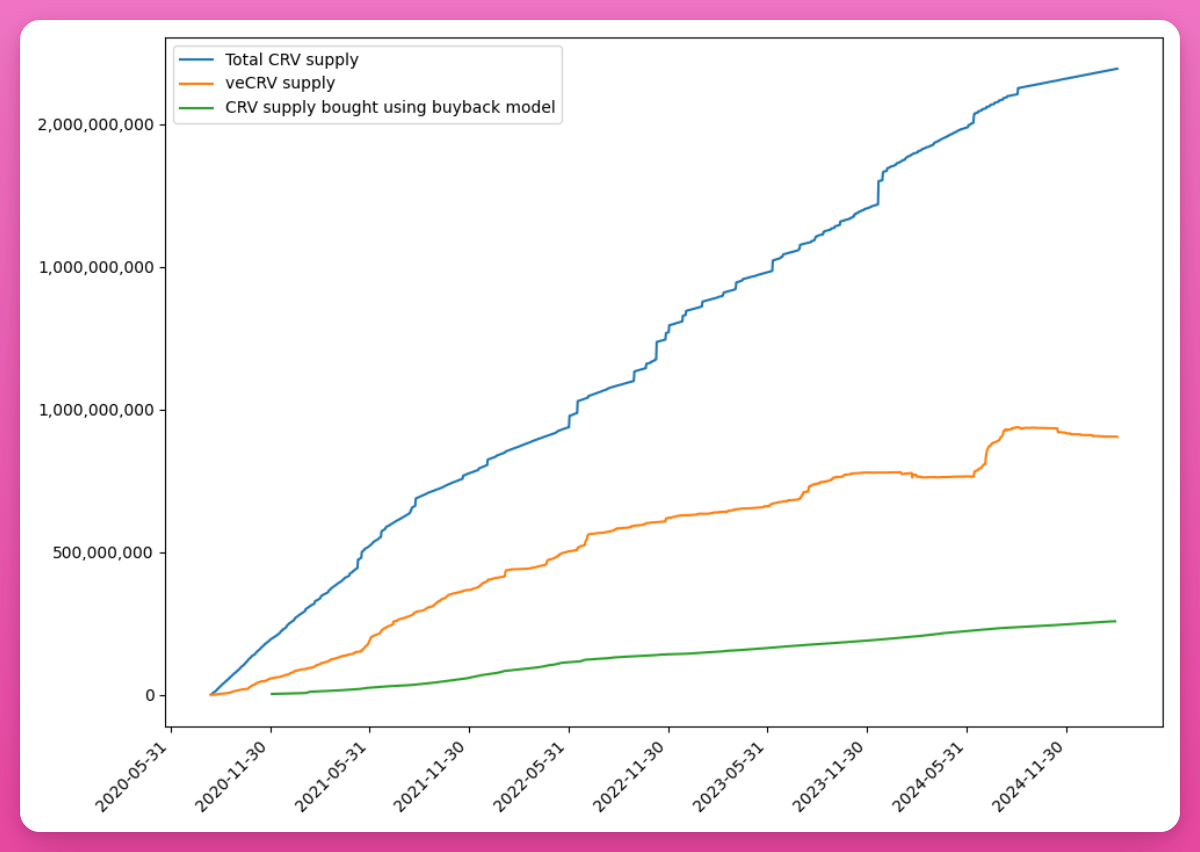

Curve’s conclusion: The amount of veCRV consistently locked remains roughly triple what a comparable burn mechanism would remove.

Scarcity derived from locking is structurally deeper than scarcity derived from burning—because locking simultaneously enables governance participation, fee distribution, and liquidity coordination—not just supply reduction.

In 2025, Curve’s DAO removed the veCRV whitelist, broadening DAO governance access. Protocol metrics remain impressive: trading volume rose from $119B in 2024 to $126B in 2025; pool interactions more than doubled to 25.2M transactions; Curve’s share of Ethereum DEX fees surged from 1.6% at the start of 2025 to 44% by December—a 27.5x increase.

But here’s a counter-counterargument: Curve occupies a unique position as Ethereum’s stablecoin liquidity backbone—and 2025 was the year of stablecoins. Gauge-directed liquidity reflects real, market-driven, organic demand. Stablecoin issuers like Ethena structurally require Curve pools—creating a bribery market rooted in genuine economic value.

The three protocols abandoning ve tokenomics lack this. Pendle’s value proposition is yield trading—not liquidity coordination; PancakeSwap’s is a multichain DEX; Balancer’s is programmable pools. None possess the structural reason for external protocols to compete for their gauge emissions.

Conclusion

ve tokenomics hasn’t died universally. Curve’s veCRV and Aerodrome’s ve(3,3) continue to function well. But the model works only when gauge-directed emissions can create real, economically driven liquidity demand. Meanwhile, other protocols are turning to revenue-backed buybacks, deflationary supply mechanics, or liquid governance tokens as alternatives to ve tokenomics.

Perhaps it’s time for DeFi to adopt a new incentive mechanism—one that genuinely serves both protocol health and long-term tokenholder interests.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News