DeFi Ecosystem Outlook 2024: Key Industry Trends and Directional Predictions

TechFlow Selected TechFlow Selected

DeFi Ecosystem Outlook 2024: Key Industry Trends and Directional Predictions

Analyze the development trends of the DeFi ecosystem and explore the challenges and opportunities projects face in an ever-changing market.

By Jiang Haibo, PANews

Over the past few years, DeFi has experienced rapid development and evolution. From initial experimental projects to becoming an essential cornerstone of the crypto space, numerous protocols such as Uniswap, Curve, Aave, and Compound have risen to prominence. However, competition within this sector is intensifying—DEXs continuously lower trading fees to attract volume, lending protocols increase loan-to-value ratios to improve capital efficiency, and projects actively launch new products to capture more market share. What trends might DeFi exhibit in 2024? PANews outlines the following key trends and predictions for the DeFi landscape.

Protocol Platformization

As the DeFi space matures, leading DeFi protocols are no longer content with their core offerings. They aim to evolve from single-function projects into comprehensive platforms providing a full suite of services.

Over the past year, familiar DeFi protocols have made notable moves: MakerDAO launched Spark, a sub-DAO that reached $1.65 billion in TVL on Ethereum by December 29, establishing itself as a major lending protocol.

Curve and Aave introduced their own stablecoins, crvUSD and GHO, respectively. Uniswap launched its wallet app and previously acquired the NFT platform Genie. On the new Aptos chain, Thala independently developed a stablecoin, DEX, launchpad, and liquid staking functionality—essentially covering all common DeFi use cases except lending.

The platformization of DeFi protocols has become a clear trend, symbolizing both maturity and increasing internal competition. This trend is likely to continue and intensify in the future.

Dominant DEXs and Lending Protocols Will Maintain Their Lead

Top-tier DeFi protocols like Uniswap, Aave, and MakerDAO emerged before the last bull market. They have strengthened their positions through continuous market evolution, demonstrating strong network effects and brand influence while consistently innovating. For the foreseeable future, they will likely retain dominant market shares and remain difficult to displace.

Uniswap announced its v4 version, enabling customizable features via "hooks." Uniswap X proposes an off-chain order signing mechanism similar to Cowswap, with on-chain settlement via Dutch auctions. Aave v3 improves capital efficiency and expands across multiple chains, further solidifying its role as a primary lending platform in the DeFi ecosystem.

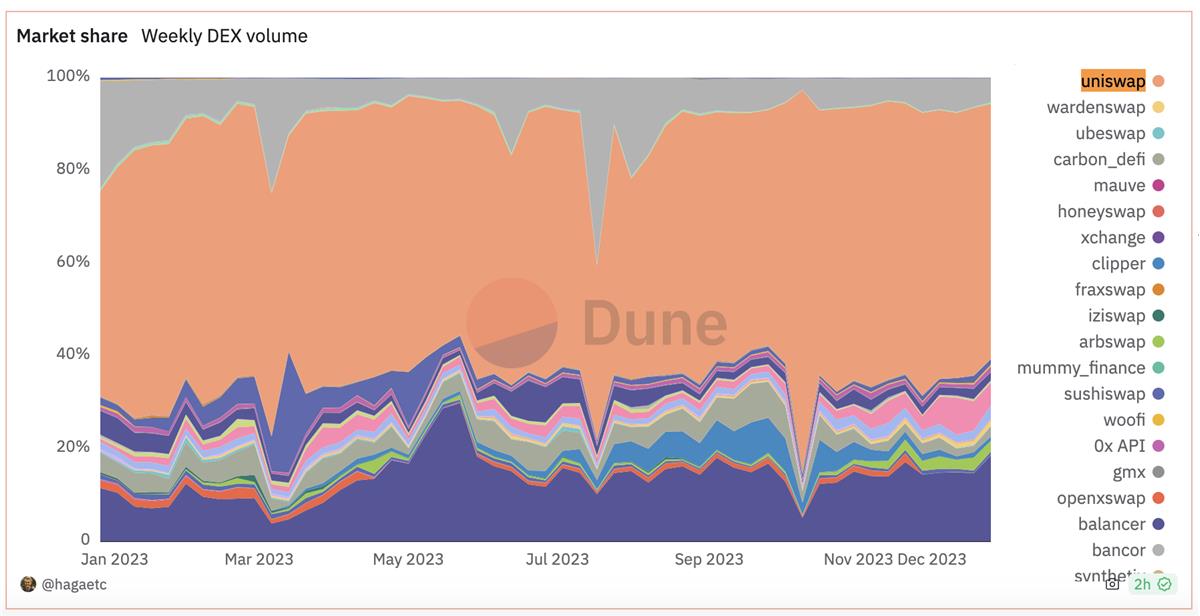

According to a dashboard by Dune co-founder hagaetc, Uniswap still holds around 55% of the DEX market share across major EVM chains.

Yield Farming Fades Into History; Capital Flows Toward Higher Efficiency

On mature blockchains like Ethereum, Solana, and BNB Chain, yield farming is gradually becoming obsolete. Projects now attract capital through "real yield," and funds increasingly flow toward more efficient opportunities.

Recently, rising SOL prices and ecosystem growth have fueled FUD about Ethereum and its DeFi ecosystem. Amid frequent meme coin trading, Solana’s DEXs have demonstrated strong capital efficiency. Today’s liquidity providers rely primarily on real income generated from trading fees, making these platforms likely short-term beneficiaries of capital inflows.

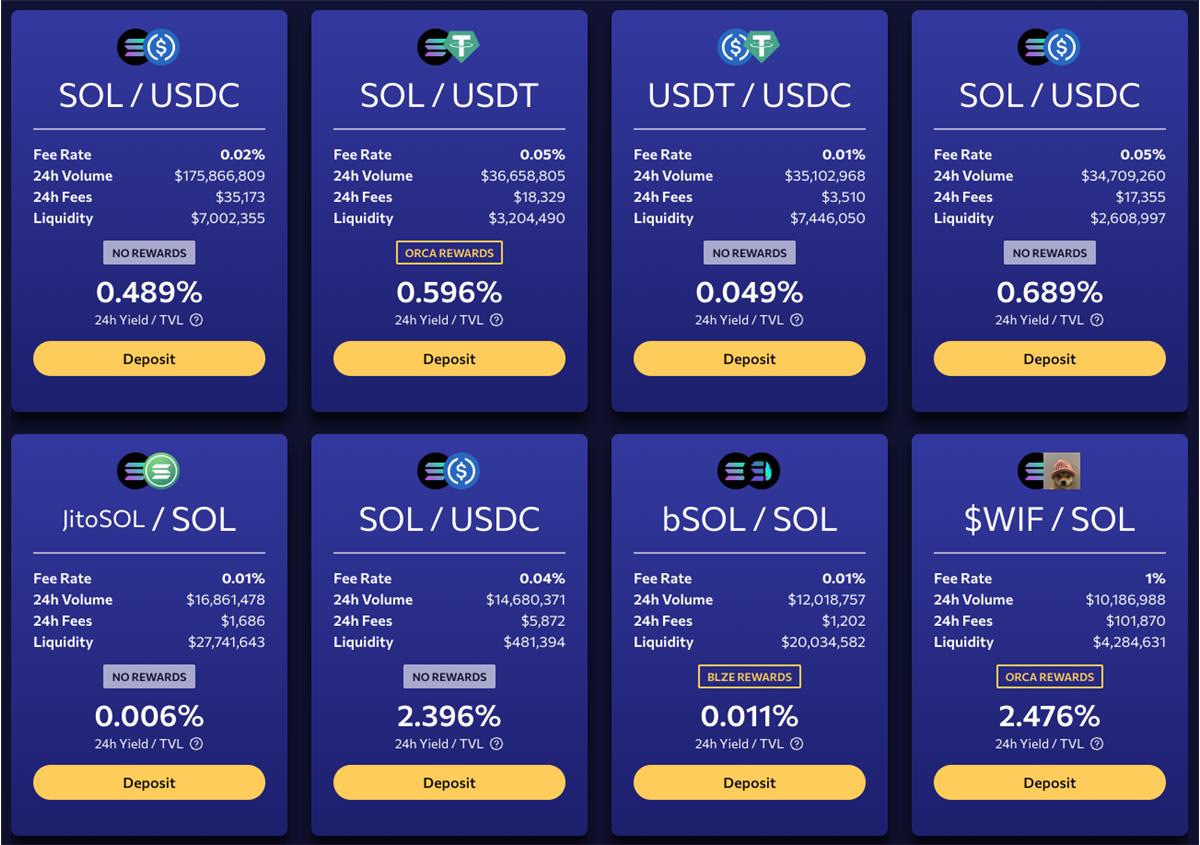

For example, as of December 30, Orca’s top liquidity pools—SOL/USDC and SOL/USDT—generated average daily returns approaching or exceeding 0.5% solely from trading fees. The SOL/USDC pool, with a 0.04% fee rate, collected fees amounting to 2.396% of its liquidity in a single day.

Such performance is unimaginable on other chains. On Ethereum, the top three ETH/stablecoin pools generate daily returns of just 0.068%, 0.077%, and 0.127% of their liquidity, respectively.

Given such stark profitability disparities, professional liquidity providers will naturally shift toward higher-yielding, more capital-efficient venues. This does not contradict the earlier point—leading DeFi projects offer stronger fundamentals, security, and stability—but their growth rates are relatively slower. Emerging projects may grow faster during favorable conditions, and expectations of future growth can reflect in token prices. However, how long such growth can be sustained remains uncertain.

LSTs Will Drive TVL Growth on New Blockchains

Although liquid staking solutions have existed on many proof-of-stake blockchains for some time, liquid staking tokens (LSTs) only began gaining concentrated attention after Ethereum's Shanghai upgrade. Today, Lido, the leading liquid staking protocol, stands unchallenged as the project with the highest TVL.

A similar trend is unfolding on Solana, where two liquid staking projects—Marinade and Jito—rank first and second in Solana’s ecosystem TVL. These liquid staking protocols have driven recent TVL growth on Solana: Jito’s pre-launch airdrop incentives attracted staked assets, while Marinade, Jito, and others continue incentivizing the use of LSTs within Solana DeFi protocols, boosting overall ecosystem TVL.

Other blockchains aiming to boost TVL appear to have discovered the secret power of LSTs. In the Sui ecosystem, the haSUI-SUI pool on Cetus offers an APR of 49.04%, with 48.09% coming from official SUI token rewards. On Avalanche, lending leader Benqi has also launched an LST product, with LST-related TVL already surpassing its lending business.

Competitive Perp DEX Projects May Emerge

Decentralized perpetual contract exchanges (Perp DEXs) have long been seen as promising, spawning projects like dYdX, Synthetix, and GMX. dYdX uses an order book model, while Synthetix and GMX operate with liquidity pools. Despite being leading Perp DEXs, each has distinct trade-offs in user experience.

GMX v1 was criticized for imbalanced long/short ratios during one-sided market movements, disadvantaging liquidity providers. Additionally, it charges borrowing fees for both long and short positions and imposes high trading fees, making it less trader-friendly—though its zero-slippage liquidity remains a unique advantage.

GMX v2 introduces trading slippage to balance long/short exposure, compensating balanced trades and penalizing imbalanced ones. However, users cannot predict whether the market will be balanced when closing positions, introducing uncertainty. Penalty slippage can reach up to 0.8% or more per trade. With leverage—for example, 10x—the effective cost could wipe out 8% of principal in a single round-trip trade.

Compared to GMX v2, Synthetix suffers from greater funding rate volatility, which can erode user profits after opening positions. Moreover, Synthetix relies on Pyth’s off-chain oracle, resulting in an 8-second delay between order placement and execution, preventing true “what you see is what you get” trading.

Recent Perp DEXs show compelling characteristics. For instance, Drift’s DLP pool reports 30-day liquidity provider returns of 2000% for BONK-PERP and 439% for HNT-PERP. While leveraged liquidity provision on Drift carries extreme risk—including total loss of principal—it also offers potential for outsized returns. Meanwhile, projects like Aark Digital and MXY Finance are introducing more capital-efficient Perp DEX designs.

Real-World Assets (RWA)

Real-world asset (RWA) projects remain controversial. Since they involve off-chain components, they often depend on centralized entities and face regulatory risks—factors at odds with DeFi’s decentralized ethos.

While we believe there are significant opportunities in tokenizing real-world assets, U.S. Treasuries currently appear to be the only RWA category achieving large-scale adoption. Other assets like real estate and art can technically be tokenized, but due to their non-standardized nature and inherent illiquidity, they remain illiquid even on-chain.

With expectations of U.S. rate hikes ending, short-term Treasury yields are expected to decline significantly in 2024, directly impacting the yields of RWA products like those offered by MakerDAO. Meanwhile, if the crypto market enters a bull run, demand for stablecoins may rise, potentially reducing the relative appeal of these yield-bearing RWA products. Indeed, recent data shows DAI issuance has been declining since late October.

Nonetheless, this won’t deter crypto entrepreneurs from exploring the space. The journey may bring powerful traditional financial institutions into partnership roles—an ambitious narrative worth pursuing.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News