2023 Year in Review: Global CBDC Landscape and Implications for Digital Hong Kong Dollar and Hong Kong Dollar Stablecoins

TechFlow Selected TechFlow Selected

2023 Year in Review: Global CBDC Landscape and Implications for Digital Hong Kong Dollar and Hong Kong Dollar Stablecoins

This article provides an in-depth analysis of the current global landscape regarding central bank digital currency (CBDC) initiatives across countries and regions, and explains the differences between Digital Hong Kong Dollar and CBDC.

Author: Metaer,特邀作者, Meta Era

With the arrival of 2024, an increasing number of jurisdictions are beginning to explore central bank digital currencies (CBDCs). According to data disclosed by PwC, over 80% of central banks worldwide are considering or have already launched CBDCs. For instance, the People's Bank of China started exploring the digital renminbi as early as 2014 and is currently conducting large-scale pilots in several cities. It was also one of only three payment methods accepted at venues during the 2022 Beijing Winter Olympics. So, what is the current global landscape for CBDC development? This article from TechFlow will provide an in-depth analysis.

Global CBDC Development Status and Policy Landscape

Under the current mainstream framework, the CBDC sector is primarily divided into two categories: retail and wholesale. Retail CBDCs focus on digital currencies for use by the general public, while wholesale CBDCs are designed for financial institutions that hold accounts with central banks. This article will examine both models:

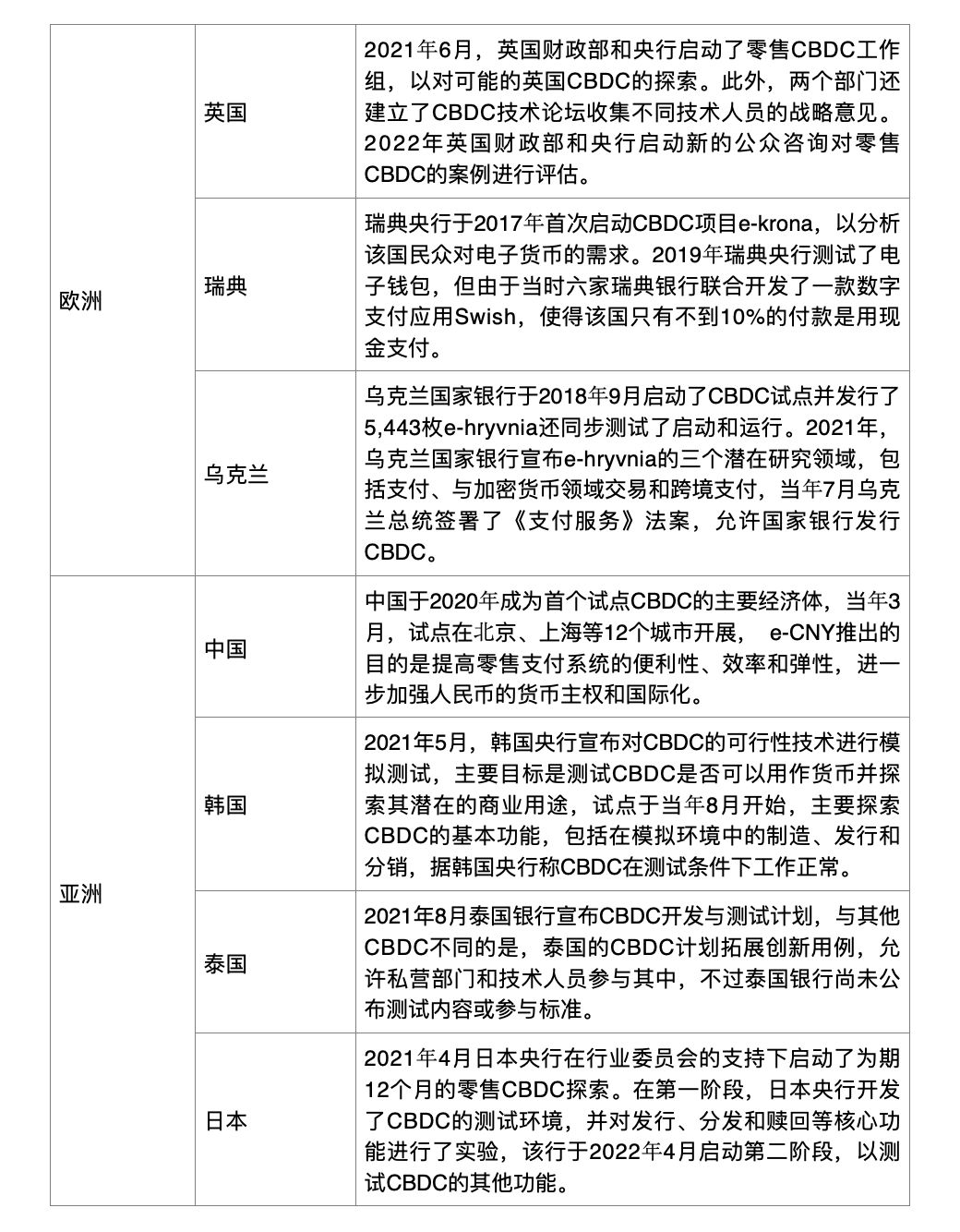

Retail CBDC

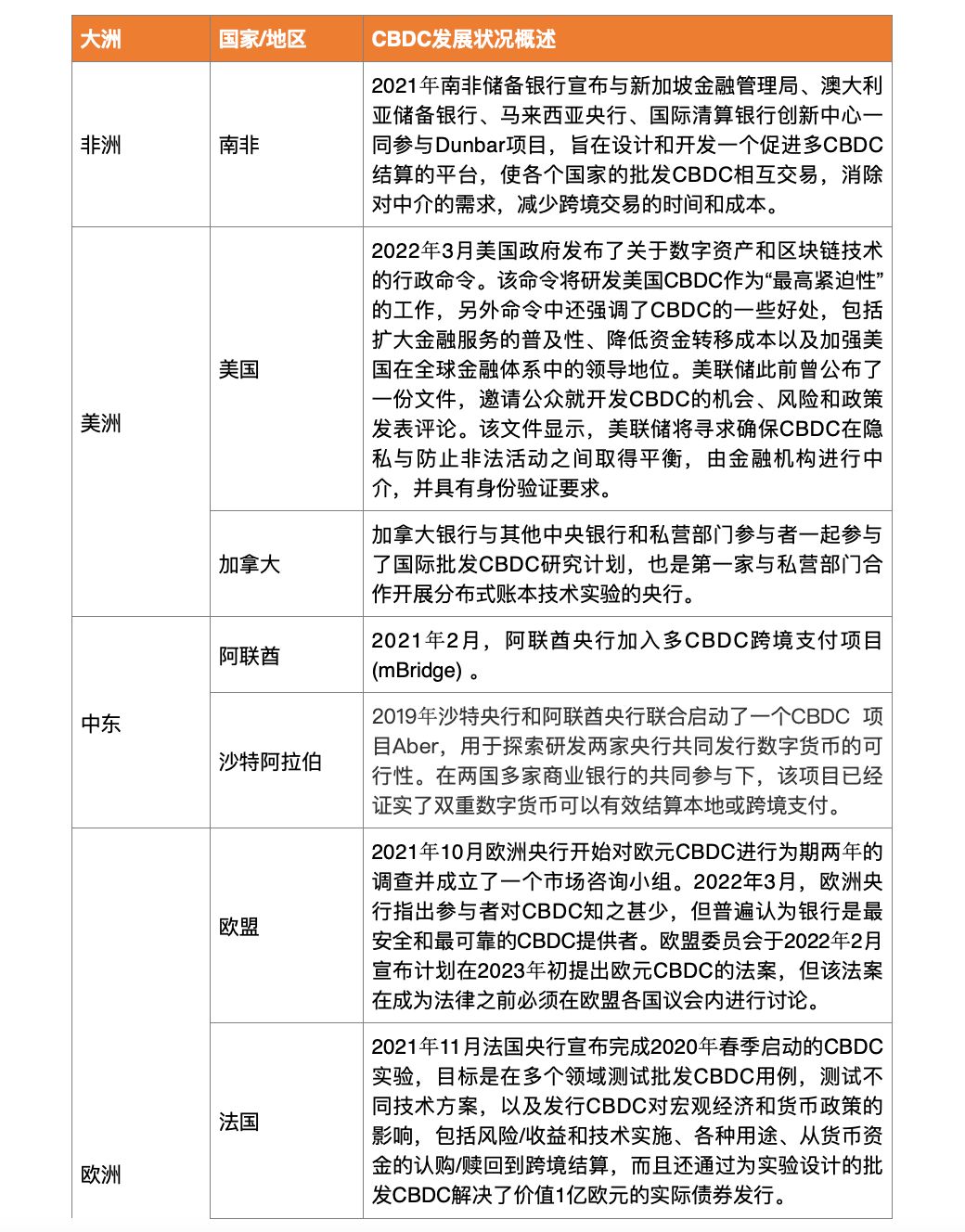

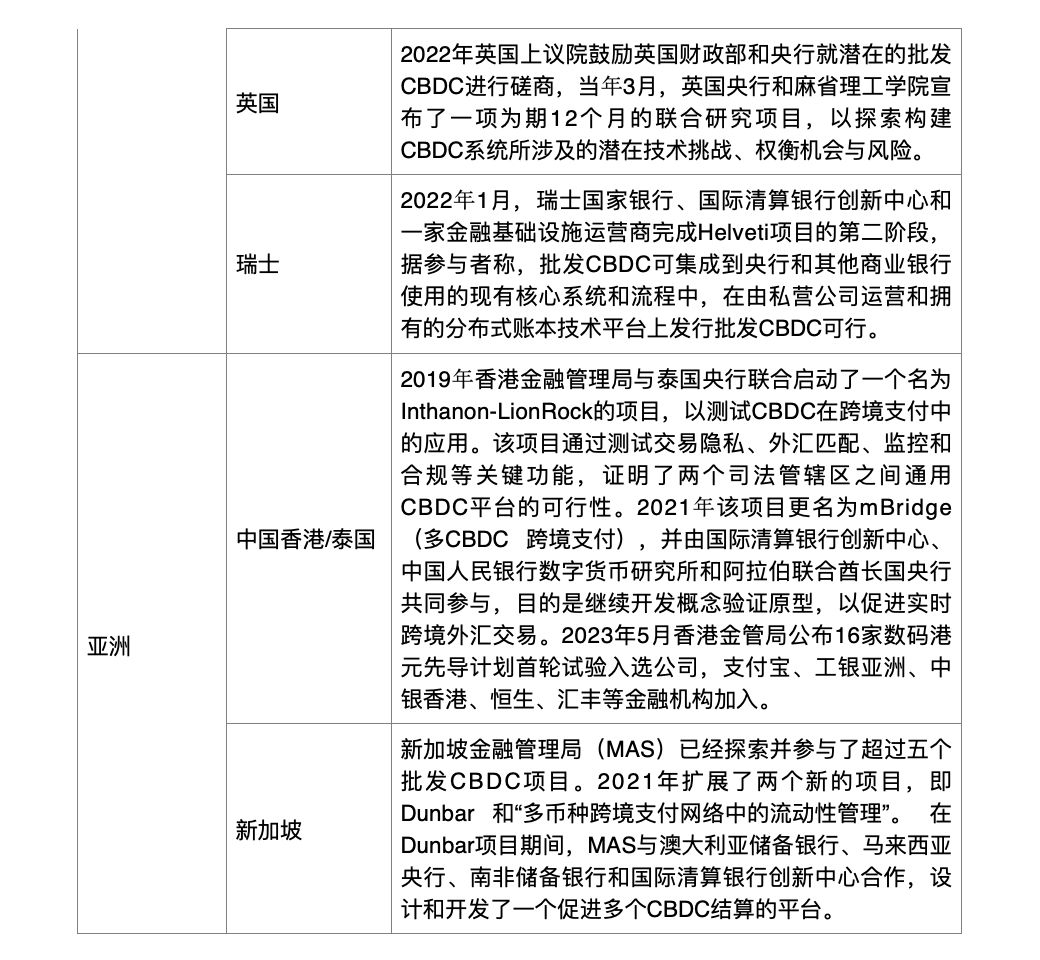

Wholesale CBDC

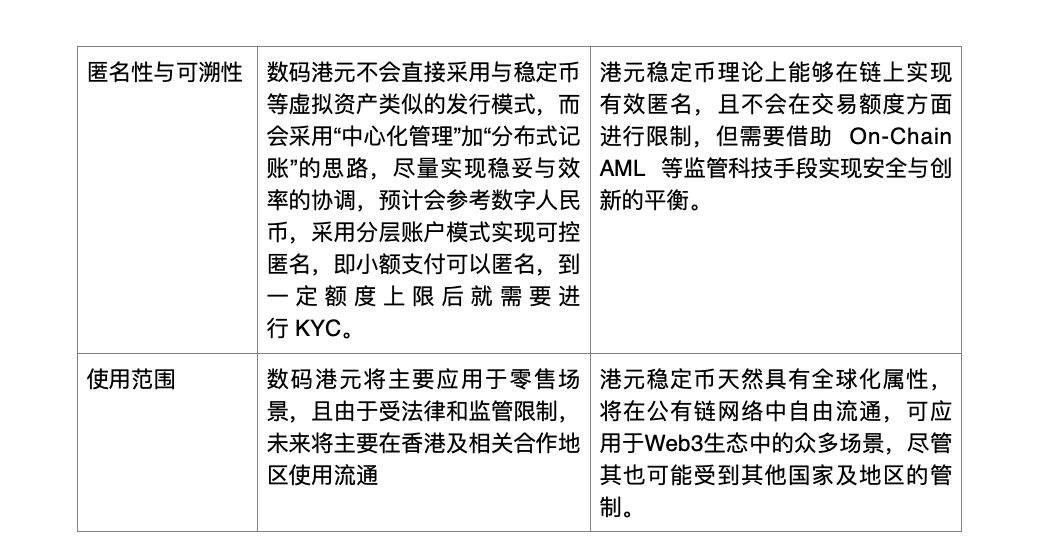

Is the Digital Hong Kong Dollar a Hong Kong Dollar Stablecoin?

At the end of 2023, the Hong Kong Financial Services and the Treasury Bureau (FSTB) and the Hong Kong Monetary Authority (HKMA) jointly issued a public consultation document seeking opinions on legislative proposals to regulate stablecoin issuers. The document formally proposed introducing new legislation to implement a licensing system, requiring all eligible fiat-backed stablecoin issuers to obtain licenses from the Monetary Authority. Only designated licensed institutions will be allowed to offer services for purchasing fiat-backed stablecoins, and only stablecoins issued by licensed entities can be sold to retail investors.

According to the HKMA, the purpose of issuing this consultation document on stablecoins is to provide clear guidance for the local regulatory framework, enhance market transparency and investor confidence, establish a regulatory regime for stablecoin issuers and service providers, promote the development of Hong Kong’s fintech industry, and attract more digital asset transactions.

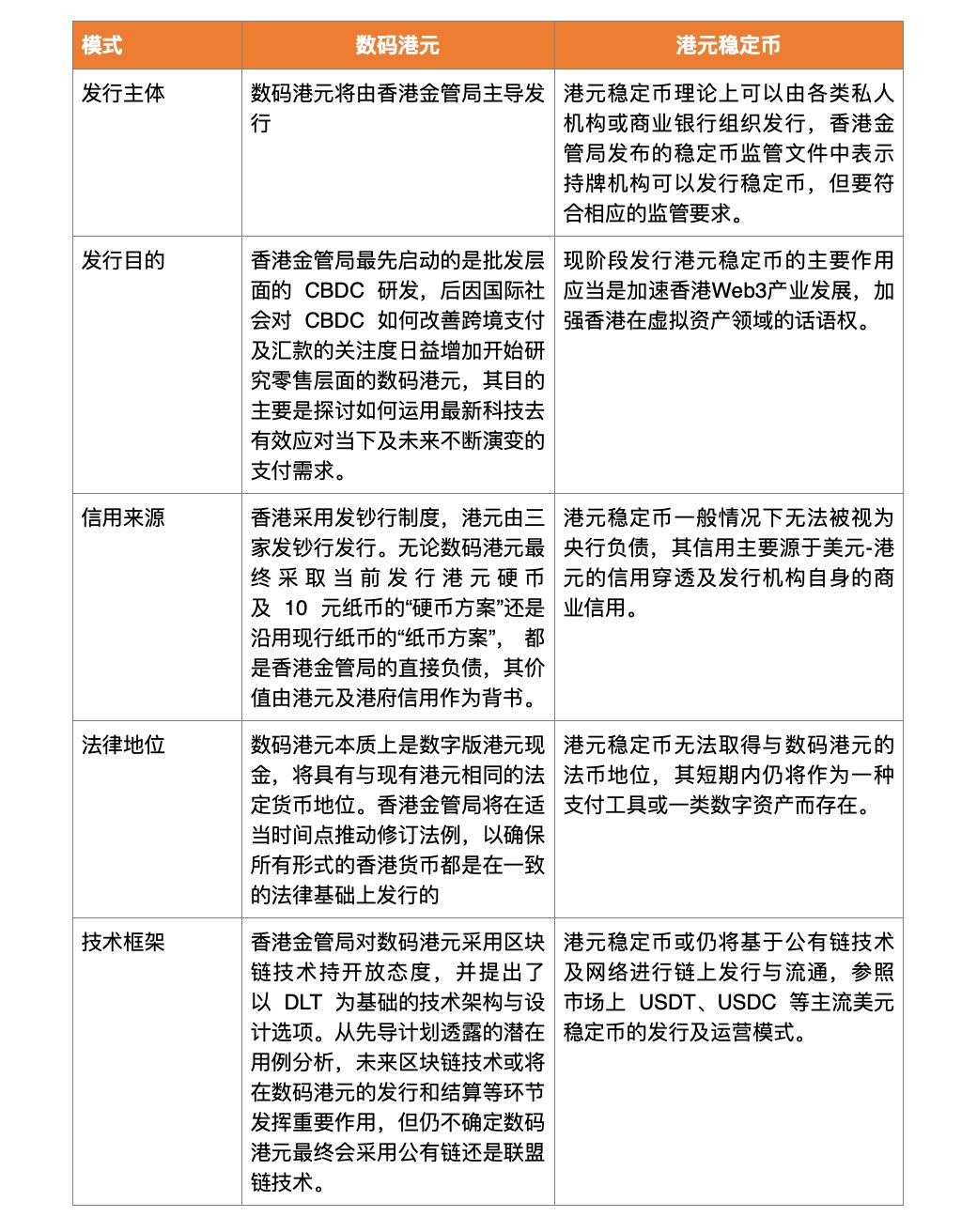

So, what are the differences between Hong Kong dollar-backed stablecoins and the CBDC known as the digital Hong Kong dollar?

Frankly speaking, many people easily confuse these two concepts—the digital Hong Kong dollar and Hong Kong dollar stablecoins. TechFlow provides a brief explainer across seven aspects:

Based on the HKMA's requirements for stablecoin issuer licensing, referencing international regulatory practices, companies are recommended to have a minimum capital requirement of HK$25 million or 2% of the outstanding amount of fiat-backed stablecoins, whichever is higher. Institutions and senior management must be based in Hong Kong and comply with anti-money laundering regulations, along with disclosure and audit requirements.

As Eddie Yue, Chief Executive of the HKMA, stated, stablecoins have the potential to become an interface between traditional finance and virtual asset markets. Whether stablecoins truly meet the condition of being "stable" will therefore become particularly important. According to the consultation document, only stablecoins issued by licensed entities can be offered to retail investors. This means that stablecoins currently used in the market for investing in virtual assets—such as Tether (USDT)—will no longer be available to retail investors if their issuers fail to obtain a license from the HKMA. Until now, stablecoins have lacked an independent regulatory framework and, like other virtual assets, related purchase services could only be provided to professional investors.

It is especially important to note that issuing or promoting stablecoins without a license in Hong Kong may constitute criminal offenses. Yes, you read that correctly. The HKMA’s stablecoin consultation document states that issuing stablecoins without a license or advertising stablecoins issued by unlicensed entities in Hong Kong are both criminal offenses. The document further recommends introducing a range of civil and regulatory sanctions. Depending on the severity and duration of violations, the HKMA may consider appropriate penalties, including temporary or permanent suspension or revocation of licenses, fines up to HK$10 million, or fines equivalent to three times the profits gained or losses avoided due to the violation, whichever is higher.

One thing is certain: Hong Kong is providing clear guidance for the regulatory frameworks of both CBDCs and stablecoins. These guidelines not only outline a series of requirements for stablecoin issuers, exchanges, and wallet service providers but also cover risk management, auditing, and investor protection—thereby promoting the development of Hong Kong’s fintech industry and attracting more digital asset transactions.

Conclusion

Overall, CBDCs can not only promote more efficient, lower-cost, and 24/7/365 payments within the financial services industry but also benefit cross-border transactions and economies across relevant jurisdictions. For example, the European Central Bank has confirmed that CBDCs can be effectively applied in online payments and peer-to-peer transactions, with additional potential roles in tax payments, welfare disbursements, income receipts, and transaction settlements.

At the same time, stablecoins are increasingly serving as a complement to existing payment ecosystems, offering most of the same utilities as CBDCs—such as transferability, continuous settlement, traceability, cross-border interoperability, low transaction fees compared to traditional payment infrastructure, and programmability—without the same restrictions.

From this analysis of the global CBDC and stablecoin landscape, it is evident that Hong Kong is one of the few jurisdictions globally actively exploring both CBDCs and stablecoins. The digital Hong Kong dollar, following China’s digital renminbi, represents another major economy launching a central bank digital currency, signaling that CBDCs are transitioning from conceptual stages to practical applications and encouraging other countries to accelerate their own CBDC research and pilot programs. As an international financial center, Hong Kong’s CBDC—the digital Hong Kong dollar—will serve as a platform for collaboration among central banks and regions, promoting cross-border usage and interoperability of CBDCs.

In the coming years, the development of Hong Kong’s CBDC and stablecoin markets will depend on factors such as the regulatory environment, market trends, and technological innovation. A series of proactive measures will help enhance market transparency and investor confidence.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News