RWA Potential Exploration: The Next Large-Scale Application Sector After USD Stablecoins?

TechFlow Selected TechFlow Selected

RWA Potential Exploration: The Next Large-Scale Application Sector After USD Stablecoins?

For the current development of RWA, compliance risk, counterparty risk, and U.S. Treasury default risk are the main sources of uncertainty.

TL;DR

-

RWA assets, with characteristics such as high transparency and strong liquidity, are positioned to become the next major sector in DeFi after USD stablecoins to achieve scalable adoption;

-

There are roughly three development directions for RWA: public chains with permissionless DeFi-like experiences, public chains with regulated whitelisted trading, and private or consortium chains limited to closed networks. The first offers the highest composability and is the most desirable path forward;

-

Currently, DeFi lacks effective mechanisms to retain existing capital or attract new inflows. Traditional finance (TradFi) faces urgent challenges around liquidity, transparency, and transaction costs. Integrating RWA can help address these issues in both ecosystems and promote convergence between DeFi and TradFi;

-

By analogy with RWA, we can extend the concept to CWA (Crypto-World Assets), such as Bitcoin ETFs—financial instruments in traditional markets that provide exposure to crypto. The underlying demand for both stems from investors’ need for risk-matched, specialized financial products that enhance efficiency;

-

Considering factors like transaction costs, asset holding costs, and compliance barriers, U.S. Treasury ETFs represent the optimal early candidate for large-scale RWA applications. Key uncertainties include regulatory risks, counterparty risks, and potential U.S. debt default;

-

Through integration of RWA assets, MakerDAO currently achieves an adjusted yield of approximately 6.83%. Given the relatively low DAI deposit ratio, Maker can amplify the DSR (DAI Savings Rate) to 1.86x the yield from RWA. Currently offering a 5% yield to DAI depositors—slightly above Treasury ETF returns—Maker not only generates substantial revenue from RWA yields but also brings this income on-chain to benefit DAI holders;

-

As more CDP (Collateralized Debt Position) stablecoin projects follow MakerDAO’s lead by adopting RWA as collateral, the market for RWA-backed stablecoins could grow exponentially. Based on increasing market share and RWA allocation, the total addressable market could range between $15.96 billion and $21.50 billion;

-

With evolving regulatory clarity, RWA will likely progress from standardized assets to non-standard ones, converging with CWA to transform blockchain technology from back-end infrastructure to front-end application. RWA will serve as a critical bridge enabling scalable integration between DeFi and TradFi.

Overview of RWA

Real World Assets (RWA) refer to traditional assets tokenized via blockchain technology, giving them digital form and programmability. Under this framework, various asset classes—from real estate and infrastructure to art and private equity—can be converted into digital tokens. These tokens are not merely digital representations of value but also carry multidimensional data about their physical counterparts, including asset type, status, transaction history, and ownership structure. Broadly speaking, widely adopted USD stablecoins today are themselves a form of RWA—essentially tokenized fiat currency. This article explores how RWA could become the next major sector after USD stablecoins to achieve scalable adoption in DeFi.

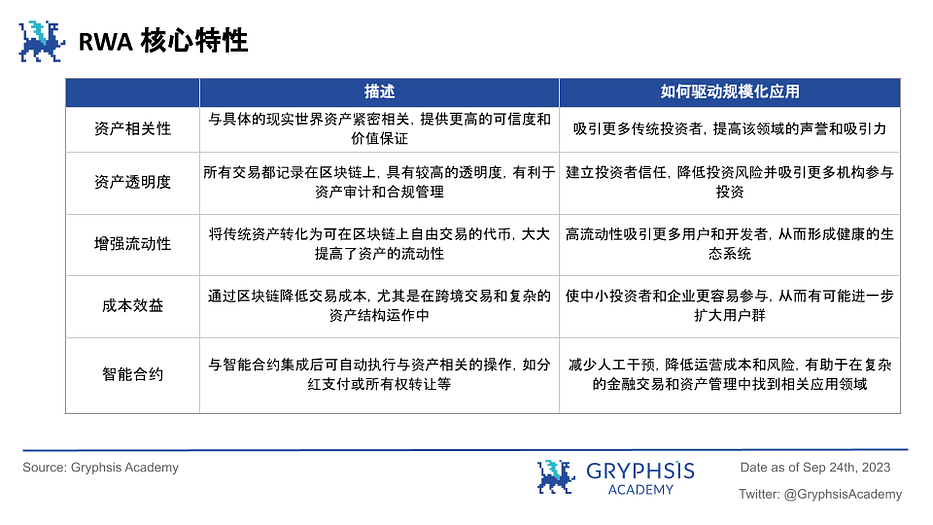

RWA assets possess unique multidimensional advantages that position them for mass adoption within blockchain ecosystems. Their strong asset correlation and transactional transparency foster investor trust, while enhanced liquidity and cost efficiency drive market activity and diversity. The integration of smart contracts further improves operational efficiency and simplifies compliance and auditing processes. Together, these core attributes pave the way for RWA to emerge as the next major scalable use case following USD stablecoins, signaling vast potential across blockchain and broader financial landscapes. That said, RWA encompasses many asset types—so which will be first to scale on-chain, and what are the associated risks and challenges?

Currently, the most feasible and already emerging sectors are fixed-income and precious metal tokenization. While the gold tokenization market has surpassed $1 billion (led by projects like $PAXG and $XAUT)), from DeFi’s current pain points—seeking standardized, yield-generating real-world assets—the most efficient starting point lies in fixed-income instruments such as U.S. Treasuries and Treasury ETFs.

Three Development Paths for RWA Based on Blockchain Type and KYC Strictness:

1. Public Chain with Permissionless Experience

The first direction emphasizes enabling permissionless trading of assets on public blockchains to deliver a DeFi-like user experience. In this model, real-world assets are tokenized and freely traded on public chains without centralized approval or restrictions on transfers. This maximizes liquidity and market participation while reducing transaction costs. However, it also introduces significant regulatory and compliance challenges, including AML and KYC requirements. While this approach offers clear benefits, it must navigate complex legal and risk landscapes.

2. Public Chain with Regulatory Whitelisting

This second path represents a compromise: assets may trade on public chains but under regulated conditions, such as address whitelisting to restrict participants. Only verified addresses added to the whitelist can engage in RWA trading. This balances openness with oversight, allowing regulators greater visibility while preserving some degree of liquidity and transparency—a middle ground between fully permissionless and fully controlled systems.

3. Private/Consortium Chains with Complex KYC

The third direction involves RWA transactions on private or consortium chains, typically involving rigorous KYC procedures and strict regulatory control, with little to no composability. Validator nodes are usually government-approved institutions, ensuring operations remain highly compliant and secure. While this limits liquidity and participation, it offers the highest level of regulatory adherence and data protection—making it the preferred model for many governments and traditional financial institutions.

Why Do We Need RWA?

From a DeFi Perspective:

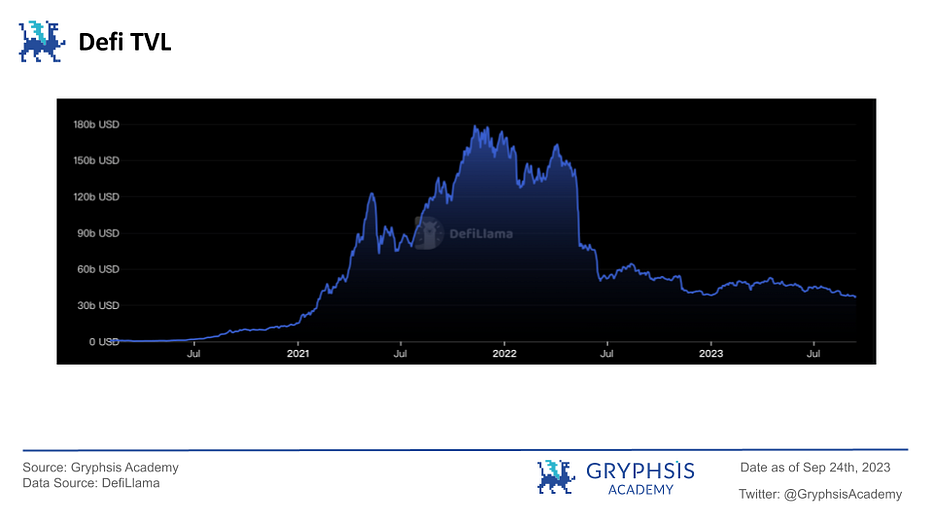

As shown in the DeFi TVL chart above, since the collapse of UST in May 2022 triggered market panic and massive sell-offs, DeFi TVL has been on a steady decline. Current narratives and projects struggle to attract external capital. Introducing new frameworks and participants is essential. Drawing from RWA's characteristics, bringing real-world assets on-chain to provide genuine asset backing may be the best solution available.

Moreover, to retain on-chain capital or attract off-chain funds, DeFi must offer competitive yields—an attractive metric for investors. However, the Ponzi-like yields seen with $UST have eroded trust. By incorporating real-world assets, RWA can restore credibility by providing verifiable, asset-backed yields.

From a TradFi Perspective:

1. Heavy Regulation and Limited Liquidity Tools

Although traditional finance has made progress in asset divisibility and liquidity through instruments like REITs and ETFs, these tools remain constrained by stringent regulations and structural limitations. For example, REITs and ETFs often require complex compliance procedures, increasing operational costs and limiting innovation and accessibility. Thus, despite improving liquidity to some extent, there remains significant room for enhancement.

2. Limitations in Private Credit Markets

In private markets—especially private credit—there are numerous constraints and unmet needs. These markets are often manual, slow, opaque, and expensive to operate. Capital matching involves multiple steps: identifying and vetting investors and opportunities, initial capital deployment, secondary trading, and ongoing management. These inefficiencies lead to suboptimal capital allocation and poor client experiences.

3. The "Black Box" Problem in Complex Financial Products

Creating complex financial products in TradFi often results in "black box" scenarios—lacking transparency and traceability, making it difficult to see through to underlying assets. This opacity increases risk and undermines trust. By mapping underlying assets onto the blockchain and using smart contract composability to package them into products, regulators only need to oversee custody of base assets. This ensures transparency throughout the product creation process, solving the black box issue. Such regulatory ease could enable greater product diversity and liquidity compared to traditional methods.

Overall, TradFi’s key challenges lie in enhancing liquidity, transparency, and cost efficiency. RWA, through tokenization and blockchain technology, offers viable solutions—particularly in private markets and structured finance, where unprecedented levels of transparency and efficiency could overcome systemic bottlenecks. By integrating RWA, traditional finance could achieve higher capital efficiency, broader participation, and lower transaction costs, fostering a healthier and more sustainable financial ecosystem.

It's also evident that both traditional institutions and DeFi protocols have long been investing in RWA, seeking synergies and convergence. Recently, attention has turned to Bitcoin ETFs, prompting us to introduce a related concept by analogy: CWA (Crypto-World Assets).

RWA vs. CWA

As Bitcoin becomes a mainstream investment, major financial institutions are actively pursuing approval for Bitcoin ETFs. This trend marks growing integration of crypto assets into traditional finance and opens a new lens: the concept of CWA (Crypto-World Assets). Like RWA, CWA enhances standardization and liquidity—but whereas RWA focuses on tokenizing real-world assets, CWA refers to crypto-native assets and related financial products being standardized in the real world. The prototypes are clear: on-chain issuance of U.S. Treasuries and off-chain approval/trading of Bitcoin ETFs.

Like RWA, CWA faces regulatory and compliance hurdles. But due to crypto’s decentralized and cross-border nature, these challenges are even more complex. For instance, approving Bitcoin ETFs requires resolving issues around custody, price manipulation, and market surveillance. Yet CWA adoption could significantly boost crypto liquidity and participation. By bridging crypto with traditional financial instruments, CWA can attract more institutional investors into crypto while offering existing crypto investors better tools for investment and risk management.

At their core, both RWA and CWA respond to the same fundamental need: creating risk-matched, specialized financial products to improve market efficiency. Efficient markets encourage speculation, fueling demand for more assets and opportunities. In this context, both TradFi institutions and DeFi platforms need RWA and CWA to unlock capital flows, attracting more users and capital. As new forms of financial innovation, RWA and CWA not only meet demand for diversified assets and stable yields but also channel capital toward more efficient sectors. By breaking down barriers between TradFi and DeFi, they could push the entire financial ecosystem toward greater efficiency, transparency, and sustainability—providing better investment choices and risk management tools. This synergy underpins the case for RWA’s scalable adoption.

Why U.S. Treasury ETFs?

User Education Cost

Consider why USD stablecoins became the gateway to crypto mass adoption—why not Bitcoin, other native cryptos, or stablecoins pegged to other fiat currencies?

First, user education cost is a crucial yet often overlooked factor. Most users require time and effort to understand new financial technologies. Second, USD stablecoins enjoy global acceptance due to the U.S. dollar’s role as the world’s primary reserve and transaction currency. Its widespread cross-border usage drastically reduces user onboarding friction. Leveraging familiarity and trust in the dollar allows USD-pegged stablecoins to gain market confidence quickly. Moreover, the dollar’s global dominance means educational resources are easily standardized and localized, lowering barriers across languages and cultures. Low education cost is thus a key enabler of scalable adoption.

Similarly, this explains why U.S. Treasuries—not bonds from other sovereign nations—are preferred. U.S. Treasuries are globally recognized as among the safest assets, with high credibility and liquidity, reducing resistance to adopting new financial channels. High market transparency and audit standards provide robust information support, minimizing ongoing education and marketing costs. Additionally, the stability and global liquidity of U.S. Treasuries shorten learning curves, accelerating user adoption through community engagement and social validation. Transparency and auditing rigor cannot be overstated—U.S. financial markets are highly transparent and strictly audited, reinforcing trust in Treasury-backed assets.

Real Yields

Tether ($USDT), the most widely used USD stablecoin in crypto, has long faced criticism over reserve transparency and compliance. Lack of transparency creates room for Tether to potentially overissue $USDT without full backing, using proceeds for investments that generate profits retained entirely by the company—not shared with $USDT holders. This raises important questions in today’s DeFi landscape: How can such latent yields be fairly redistributed within the ecosystem?

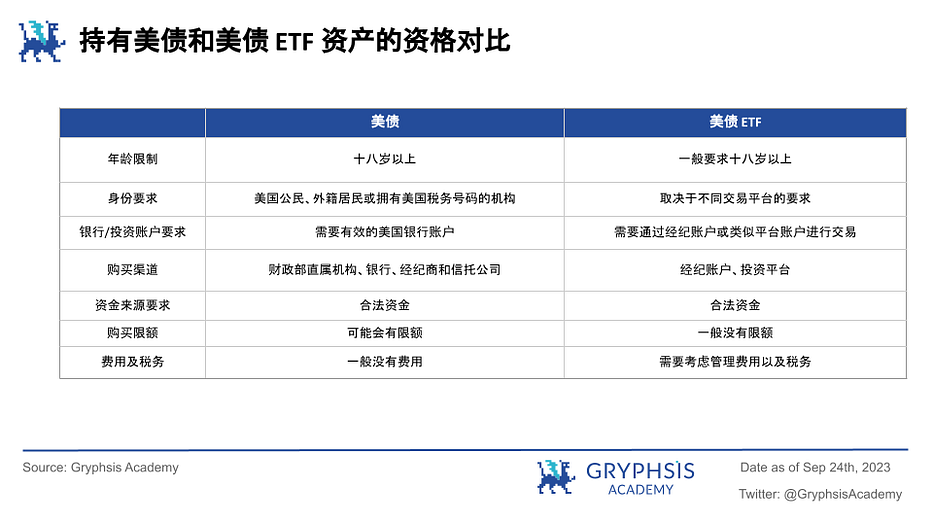

In this context, U.S. Treasuries—with their relative stability, standardization, and low risk—emerge as compelling candidates for stablecoin reserves. Treasury ETFs, compared to direct bond holdings, further reduce regulatory risk and make it easier for issuers to access these assets and yields (see comparison table below).

In sum, Treasury ETFs offer a strong solution: they help stablecoin issuers like MakerDAO mitigate opacity and counterparty risks associated with $USDT and other centralized stablecoins, while advancing crypto toward broader acceptance. Using Treasury ETFs as collateral provides a more transparent, regulated investment path and enables fairer distribution of returns to all participants. This benefits DeFi by aligning with public trust and regulatory expectations. Although issuers may sacrifice some “black box” profits, greater regulatory cooperation unlocks larger, more stable markets. For stablecoin adoption, RWA represents at least a triple-win: more transparent and equitable returns for investors, higher credibility for regulators, and expanded market reach for issuers.

Advantages of U.S. Treasury ETFs

Based on the comparison between Treasuries and Treasury ETFs, direct bond purchases impose high requirements on investors—especially challenging for decentralized stablecoin issuers facing compliance risks or DeFi protocols seeking real-world yields. Partnering with reputable ETF providers makes purchasing ETFs a lower-cost, higher-liquidity alternative to direct bond ownership. As shown in the table below, holding Treasury ETFs offers DeFi protocols multiple advantages over other real-world assets.

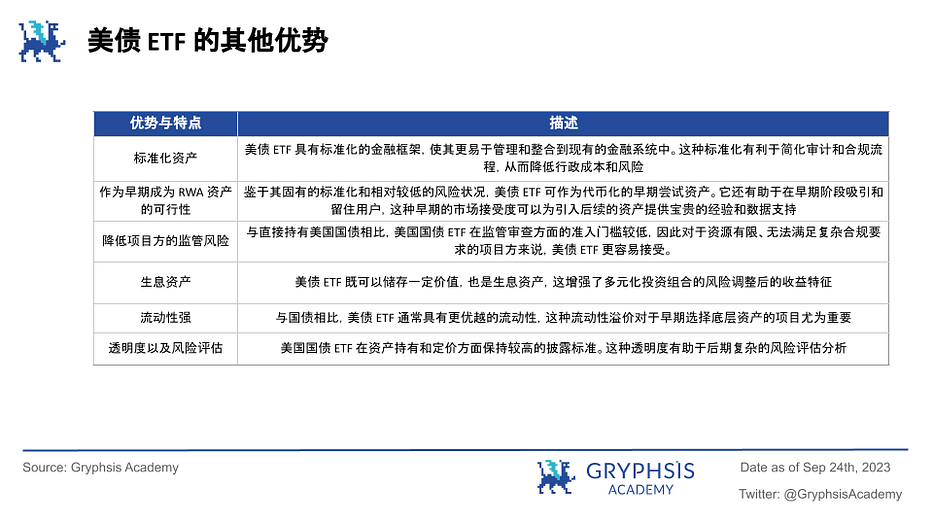

According to Mint Ventures researcher @Colin (see 'The Only Answer for Mid-Term RWA: Musings on Web3 Sovereign Bonds'), the main advantage of using Treasury ETFs as underlying assets is the significant simplification of asset management. In this setup, responsibilities such as liquidity management and bond rollovers are handled by the ETF issuer and manager, effectively reducing operational burden and risk for project teams. Treasury ETFs have so far avoided major incidents, requiring minimal risk monitoring. Teams simply need to select the largest, most liquid, and standardized ETFs for inclusion. Compared to managing direct bond holdings, ETFs allow teams to focus on core operations while delegating complex asset management to professional firms—reducing operational risk and increasing efficiency.

Overall, Treasury ETFs offer multiple advantages as on-chain assets: standardization, suitability as early-stage RWA pilots, relatively low compliance hurdles, and yield-bearing capacity. These traits make them ideal candidates—especially for projects exploring early-stage real-world asset tokenization. That said, given the current limited scale of tokenized assets, the Federal Reserve’s August report on asset tokenization warns that as scale grows, traditional ETFs may face pricing fragility due to the high liquidity and composability of tokenized assets—potentially transmitting crypto-style volatility into traditional markets. This remains a concern for investors and regulators alike, awaiting robust solutions. Additionally, declining Treasury yields may challenge DeFi’s ability to find comparable yield sources in the future.

How to Bring RWA On-Chain?

Though still in exploration phase, the RWA market has gained initial traction, with diverse players from DeFi and TradFi experimenting with different on-chain solutions. As outlined earlier, current approaches include MakerDAO’s near-DeFi experience with DSR yield pass-through, Ondo Finance’s whitelisted trading model, and Hong Kong’s government-issued green bonds via Goldman Sachs’ GS DAP platform on a private chain—demonstrating varied paths to RWA tokenization.

MakerDAO’s Path to On-Chain RWA:

Although MakerDAO began planning RWA as early as 2020, its progress has been shaped by regulatory developments. To date, it primarily captures yield from U.S. Treasury-focused RWA assets through third-party partners, passing this yield through DSR to select DAI holders. This amounts to tokenizing economic rights rather than full ownership. Still, as the closest approximation to a DeFi-native RWA yield experience, it holds promise. With clearer regulations, MakerDAO and its partners may eventually tokenize full RWA ownership with greater composability. Below, we examine two major vault types—RWA007-A (Monetalis Clydesdale) and RWA015 (BlockTower Andromeda & Centrifuge)—to understand how current Treasury ETF on-chain projects operate.

I. Monetalis Clydesdale

Following MIP65, we gain insight into how third-party firm Monetalis helps MakerDAO hold Treasury ETFs. Initially, MakerDAO proposed addressing three key issues stemming from having over 50% of its balance sheet in non-yielding stablecoins like $USDC and $USDP: lack of yield, concentration risk, and negative PR. The solution: directly holding short-term Treasuries to generate positive returns while reducing exposure to centralized stablecoin issuers.

MakerDAO’s initial proposal involved setting target debt ceilings and minimum/maximum ranges for each fiat-backed stablecoin ($USDC/$USDP, etc.). When a stablecoin’s PSM pool exceeds its ceiling, excess funds are converted to cash and invested in short-term investment-grade bond ETFs—reducing risk exposure while potentially boosting returns. Conversely, if below the minimum, human intervention (typically by MKR holders) is allowed. This mechanism aims to balance DAI supply and demand while diversifying risk and enhancing yield. Bond ETFs were chosen for their liquidity, simplicity, cost-efficiency, and risk management benefits (comprehensive rationale). ETFs offer high liquidity and diversification, lowering overall risk. Though initially offering modest returns, they proved simpler and cheaper than managed accounts. Moreover, being overseen by professional asset managers and regulators, ETFs provide a degree of transparency and security. From MIP65 alone, focused on risk mitigation and yield generation, it’s hard to discern MakerDAO’s broader RWA ambitions. But its collaboration with Monetalis and the MIP68 initiative reveal deeper strategic goals.

According to MIP68, Monetalis states that MakerDAO’s vision for RWA is to integrate diversified, high-quality RWAs through entities like Monetalis to bridge Maker with TradFi—enabling more flexible, innovative, and responsive credit assessment—and ultimately realize the “Clean Money” vision. More ambitiously, Maker aims to build and operate high-quality integrated services connecting TradFi and DeFi, becoming a full-stack operator for RWA tokenization and on/off-chain integration. This vast market opportunity is undeniably compelling. Now let’s see how Monetalis executes this.

First, identify a solid integration point that doesn’t drastically alter existing DeFi or TradFi workflows, enabling rapid volume growth. Then, with substantial capital flow established, gradually move toward deeper, on-chain integration. Ultimately, tightly couple DeFi with traditional finance—evolving from experimentation to mainstream adoption. In essence, this outlines Monetalis’ foundational RWA strategy, complementing efforts by Centrifuge, Maple, TrueFi, and others.

So how is this achieved? According to MIP68, three key entities are involved:

-

ARENA focuses on resolving complex interactions between TradFi and DeFi—identifying viable integration points for breakout growth across compliance, operations, and technology—to enable organic integration and long-term synergy. It acts as a bridge between the two worlds.

-

On the TradFi side, Clydesdale manages relationships with financial institutions, builds trust, analyzes and matches suitable products and needs, and implements these connections. It resolves practical conflicts between DeFi and TradFi. Given both sides’ entrenched interests and limited tolerance for compromise, Clydesdale serves as an intermediary solution—especially valuable for DeFi protocols like MakerDAO seeking gradual entry into large-scale institutional finance.

-

Meanwhile, Lusitano is an asset management platform designed to attract and integrate teams with proven expertise in specific asset classes. By creating a flexible environment, it fosters deep fusion between DeFi and TradFi and serves as a proof-of-concept for DeFi’s viability and innovation. The platform particularly encourages ESG and green economy initiatives, building broader, more diverse collaborations between DeFi and TradFi.

In short, through this framework, MakerDAO and Monetalis jointly pursue RWA adoption as collateral—securing real-world backed returns for the DAO—while targeting a much broader market. Next, we examine how BlockTower Andromeda and Centrifuge operate in partnership with MakerDAO.

II. BlockTower Andromeda and Centrifuge’s Approach

If MakerDAO and Monetalis represent aligned visions pushing RWA forward, then the tripartite collaboration among MakerDAO, BlockTower Andromeda, and Centrifuge offers nearly a complete blueprint for other projects to adopt RWA—especially since the latter two see their mission as building repeatable, scalable, and reliable frameworks for RWA investment, a critical step toward mass adoption. We can also glimpse MakerDAO’s bolder ambition: a grand plan to expand MakerDAO and DAI into wider societal and commercial domains, especially in emerging markets and real-world applications.

Through its partnership with Centrifuge, MakerDAO achieves indirect ownership of real-world assets like U.S. Treasuries—an innovative fusion of TradFi and blockchain strengths. First, asset manager BlockTower Andromeda creates SPVs, each linked to a funding pool on the Centrifuge platform. This ensures pool independence and grants each a legal identity, mitigating compliance and operational risks.

Borrowers issue NFTs via SPVs representing their real-world assets (e.g., U.S. Treasuries). These NFTs serve as on-chain representations of the assets and are locked in Centrifuge pools to draw loans. This step is crucial—it adds blockchain-enabled transparency and traceability, facilitating audits and risk assessments. These NFTs form asset pools, which are then split into two token classes: $DROP and $TIN. $DROP represents senior tranches with lower risk; $TIN represents junior tranches with higher risk.

As Centrifuge’s primary debt buyer, MakerDAO integrates directly with its funding pools, extracting DAI against $DROP tokens from its vault. This direct integration streamlines debt acquisition and management, boosting system efficiency. Through this, MakerDAO earns stable returns from real-world assets while better optimizing its balance sheet. To ensure safety, Centrifuge employs sophisticated risk layering: “Minimum Subordination Percentage” ensures sufficient buffer for senior tranches ($DROP); the “Epoch Mechanism” allows redemptions based on cash flows, with $DROP holders having priority. Together, these provide extra safeguards for MakerDAO.

However, risks remain. Multiple counterparties and complex contracts increase compliance, counterparty, and legal risks. While SPVs and pools reduce centralization risk, interaction with real-world assets introduces liquidity and market risks. Moreover, as a novel model, governance attacks and other security threats require further study.

Undoubtedly, not every project can replicate MakerDAO’s path via Monetalis-like partners. But accessing real-world assets indirectly through dedicated RWA infrastructure like BlockTower Andromeda and Centrifuge simplifies processes, cuts costs, avoids legal overhead, and exposes protocols to diverse assets. Such infrastructure is vital for RWA’s scalable vision. Still, MakerDAO has only tokenized economic rights—not full ownership. For a purer RWA implementation, Ondo Finance’s approach may be closer.

Ondo Finance’s Whitelisted U.S. Treasury Token Model:

$OUSG is a cryptocurrency token representing investor shares in the Ondo I LP fund. Ondo I LP is a Delaware-registered limited partnership that attracts on-chain investors to hold assets like ETFs. Unlike typical crypto tokens, $OUSG is directly tied to specific fund holdings.

Technically, $OUSG runs on Ethereum smart contracts, tracking investor shares and enabling subscription and redemption. To invest, users must pass Ondo I LP’s KYC/AML process—submitting ID and financial documents. Once verified, their wallet address is whitelisted, allowing them to send USDC to the fund’s smart contract. The contract automates fund receipt and share allocation.

After receiving USDC, the contract transfers funds to Coinbase-hosted fund accounts. Ondo Investment Management (Ondo IM) converts USDC to USD and sends it via partner banks to Clear Street (a securities broker and qualified custodian). There, Ondo IM buys ETF shares. Upon completion, investors receive $OUSG tokens reflecting their fund share. These tokens can be stored in wallets, used across platforms (composability), or redeemed later.

For redemptions, users send $OUSG to the contract. The system logs the request. Ondo IM sells corresponding ETF shares via Clear Street, converts proceeds to USDC, and sends it back to the investor’s wallet via Coinbase.

Ondo Finance has found a balanced middle ground, demonstrating the next step for RWA: token composability. However, given current regulatory constraints, optimism about whitelisting models should be cautious.

Hong Kong Government’s Evergreen Project:

In the Evergreen project, bond tokenization occurs in stages, some on Goldman Sachs’ GS DAP platform. Access is restricted to platform participants: the Hong Kong SAR government, HK Securities Clearing Corporation (CMU), distributors, custodians, and secondary market dealers—each assigned specific roles. Non-direct participants hold权益 through custodians (akin to banks with pre-KYC clients).

Some steps occur off-chain, like book-building and pricing. On pricing day, CMU deploys on-chain smart contracts representing tokenized bonds and HKD cash tokens. Verified participants (e.g., distributors) transfer funds to CMU’s RTGS account to join the subscription via smart contracts.

The digital platform combines Canton blockchain (for smart contract execution) and Hyperledger Besu (for inter-node communication and consensus ledger), both private chains ensuring high security and privacy. Notably, visibility into certain smart contracts depends on whether a participant is a signatory or observer.

Throughout the bond lifecycle, payments like interest and principal are settled via HKD cash tokens issued by the HKMA on the digital platform. Smart contracts automate these operations. Unlike other digital securities using non-central bank-issued tokens (often custom-designed per trade), which pose counterparty, operational, and liquidity risks, using uniform HKD cash tokens ensured smooth execution of the Evergreen project.

Among the three models, Hong Kong’s approach is highly compliant and controlled—yet may reflect traditional institutions using blockchain merely to improve efficiency rather than evidence of scalable RWA adoption.

Data Analysis

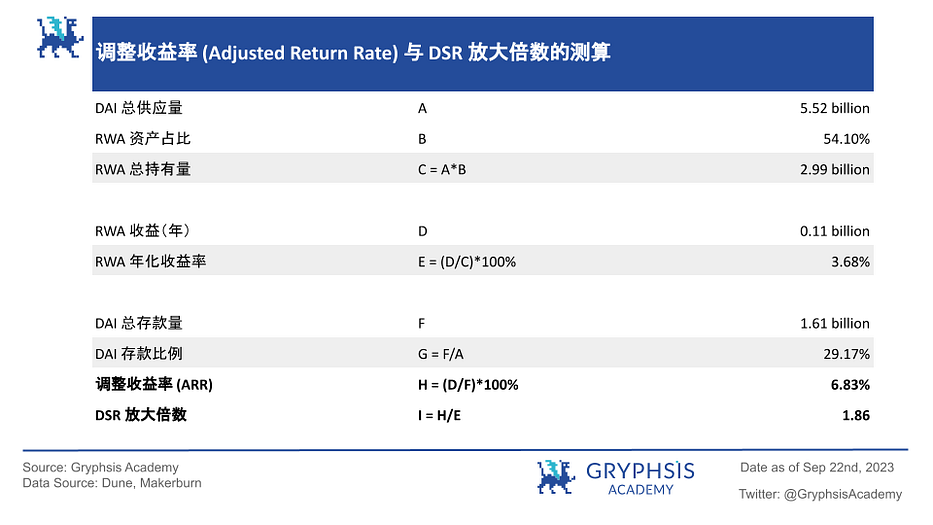

With the Fed’s rate hikes beginning in early 2022, U.S. Treasury yields surged—from an average of 0.15% at end-2021 to 4.5% by end-2022. MakerDAO’s decision to adopt Treasury assets closely followed the Fed’s tightening cycle. Unquestionably, MakerDAO has earned substantial returns from RWA and passed part of it to DAI holders. Let’s quantify the adjusted return rate (ARR) for DAI depositors and the DSR amplification effect through RWA yield pass-through.

As shown, the Adjusted Return Rate (ARR) is calculated by dividing annual RWA income (D, $0.11B) by total DAI deposits (F, $1.61B). This ARR reflects the theoretical yield DAI depositors could earn via MakerDAO, albeit indirectly through RWA. The DSR (Dai Savings Rate) amplification factor is derived by dividing ARR by the annualized RWA yield (E, 3.68%). This ratio shows how much higher the DSR yield is compared to direct RWA ownership. A 1.86x multiplier means DAI depositors earn nearly twice the yield of direct RWA holders. This amplification highlights the value and yield advantage offered by the DSR mechanism, delivering superior annual returns.

Why is ARR nearly double the RWA yield? Because the current DAI deposit ratio is low—MakerDAO can distribute RWA earnings to a relatively small pool of depositors. This explains why Maker can offer an 8% DSR. Is this a Ponzi? We argue that as long as underlying assets and profit/costs remain transparent, a DSR historically below actual RWA yields indicates real-world asset backing. Higher yields attract more DAI deposits—increasing total deposits and the deposit ratio—thus lowering ARR and the DSR multiplier, as the same RWA income is shared among more people.

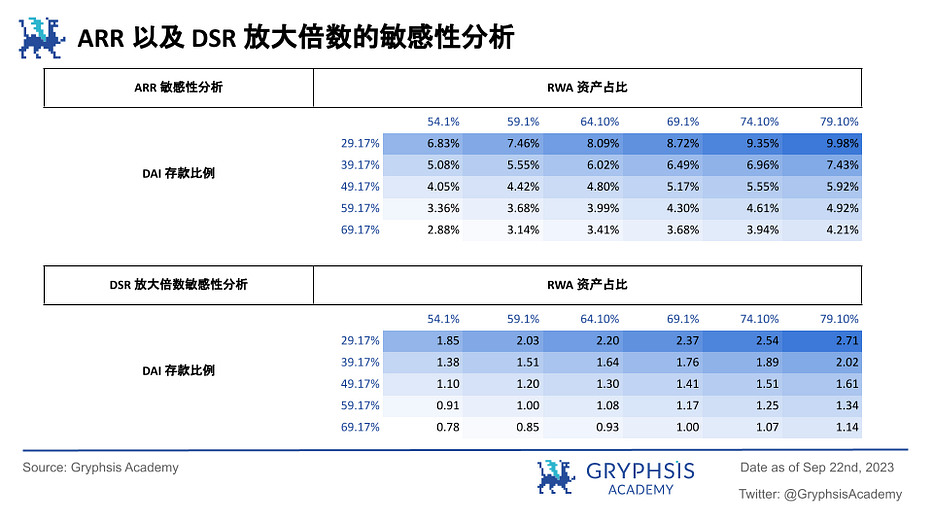

Ultimately, MakerDAO’s success in passing stable RWA yields to depositors is notable. Transparent, real-world-backed yields fill a critical gap in DeFi and could form the foundation for future RWA scalability. Of course, Treasury rates won’t stay high forever. Assuming MakerDAO maintains a 3.68% annual yield, we conduct sensitivity analysis on ARR and DSR multiplier as RWA allocation and DAI deposit ratios change.

As shown, left axis shows varying DAI deposit ratios; top shows different RWA asset ratios. As deposit ratio rises, depositor yield and DSR multiplier fall—meaning DAI returns converge toward or below MakerDAO’s actual RWA yield. Conversely, as MakerDAO allocates more RWA assets, its real yield increases, raising deposit rates and DSR multipliers.

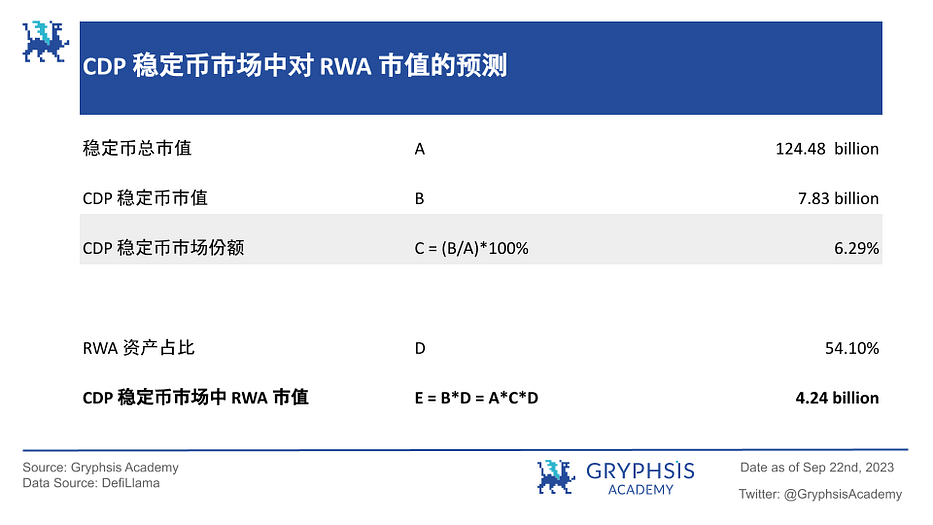

Currently, earning near-risk-free yields by holding DAI deposits appears a promising path for CDP stablecoins—especially in today’s high-Treasury-yield environment. Building on this, we estimate the future market cap of RWA in the CDP space.

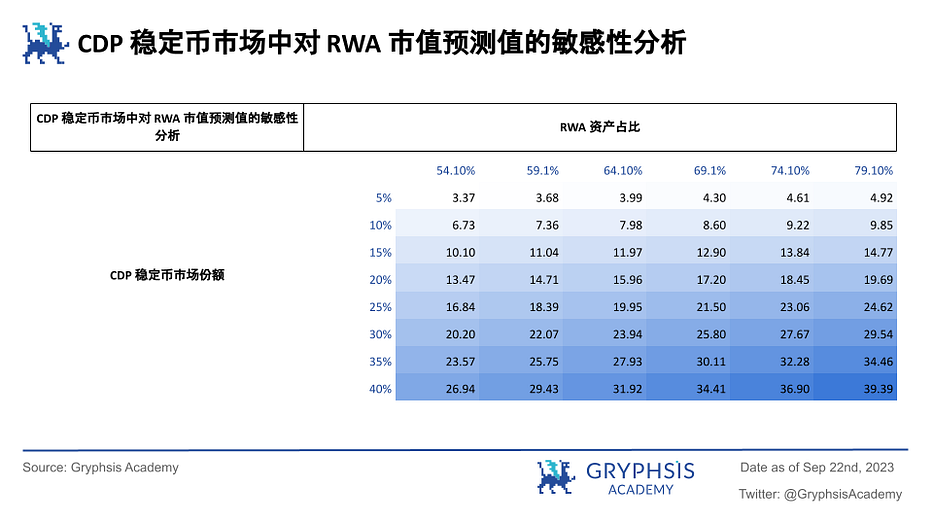

With MakerDAO’s current 54.1% RWA allocation, RWA’s market cap in the CDP stablecoin sector stands at $4.24 billion. As RWA adoption scales, CDP stablecoins—which transparently distribute stable yields to depositors—will likely gain market share. Below is a simple sensitivity analysis of RWA market cap in the CDP space (in billions):

Left axis shows CDP stablecoin market share; top shows RWA collateral ratio. As both rise, RWA market cap grows substantially. Compared to dominant stablecoins like $USDC, these yield-bearing CDP stablecoins offer greater transparency and fairer returns—suggesting more projects will emulate MakerDAO by shifting to RWA collateral. Yet this may only represent a fraction of RWA’s full scalable potential.

Conclusion and Outlook

Through in-depth analysis and data-driven insights, we believe RWA demonstrates immense market potential and long-term growth prospects. As RWA scales, both DeFi and TradFi will unlock new opportunities—even partial integration. However, unclear regulatory and compliance frameworks remain the primary barrier to scalable adoption. While we hope RWA can eventually achieve a DeFi-like public chain, permissionless experience, excessive optimism in the short term should be tempered.

Observing practices from MakerDAO, Ondo Finance, and the Hong Kong government, we’ve seen early RWA solutions and their feasibility. As RWA scales, we expect it to increasingly leverage its strengths to solve pressing issues in both DeFi and TradFi.

Looking ahead, RWA lays the groundwork for financial innovation. Initially, it will focus on standardized assets—U.S. Treasuries, Treasury ETFs, gold, REITs, and high-grade corporate bonds—due to their mature markets and high liquidity, providing a solid foundation. As technology advances and markets mature, RWA will expand into non-standard assets like art, real estate, and private equity—requiring innovative valuation models, risk frameworks, and supportive regulation.

In terms of user adoption, RWA should first meet demand for standardized assets before gradually introducing non-standard ones. This requires careful market education, investor research, and product design to ensure real value delivery.

Furthermore, the convergence of RWA and CWA could shift blockchain from back-end infrastructure to front-end applications—mirroring the internet’s evolution from servers/databases to user-facing apps—greatly enhancing usability and accessibility. Together, RWA and CWA can break down traditional financial barriers and offer investors more and better options. Achieving this demands coordinated efforts: asset standardization, infrastructure development, market education, and regulatory support.

In conclusion, RWA is poised to become the next major scalable sector after USD stablecoins—driving integration between DeFi and TradFi. We will continue monitoring RWA and regulatory developments to provide timely and accurate market insights.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News