Why are new public blockchains viewed more favorably as the number of Ethereum L2s increases?

TechFlow Selected TechFlow Selected

Why are new public blockchains viewed more favorably as the number of Ethereum L2s increases?

L1 is currently innovating and becoming more specialized, while L2 appears to be following the same old path as earlier L1s—attracting forked protocols focused on airdrop farming, but lacking innovation and diversity.

Author: DefiIgnas

Translation: TechFlow

The more L2s there are, the more bullish I become on the previous generation of alternative Layer 1s (alt-L1s).

The last bull market was a beta phase for non-Ethereum L1s:

Alt-L1s competed by offering liquidity mining rewards on forked versions of protocols like Aave and Uniswap V2, attracting yield-hungry degens.

But there was almost no application-layer innovation outside Ethereum.

Even non-EVM chains launched EVM sidechains: Aurora on Near, Moonbeam on Polkadot, Kava on Cosmos. EOS EVM and Neon on Solana arrived late and missed the party.

The only differentiating factors among these L1s were:

1) Lower gas fees;

2) Speed;

3) Branding;

4) How much liquidity mining reward they could offer.

However, as the bear market began and liquidity incentives dried up, TVL flowed back to Ethereum.

To make matters worse, a new narrative around Ethereum L2s emerged with the rise of Optimism and Arbitrum, promising scalability without compromising security.

Moreover, these L2s attracted users with potential airdrops.

L1s needed to reinvent themselves—and I’m glad to see they did:

-

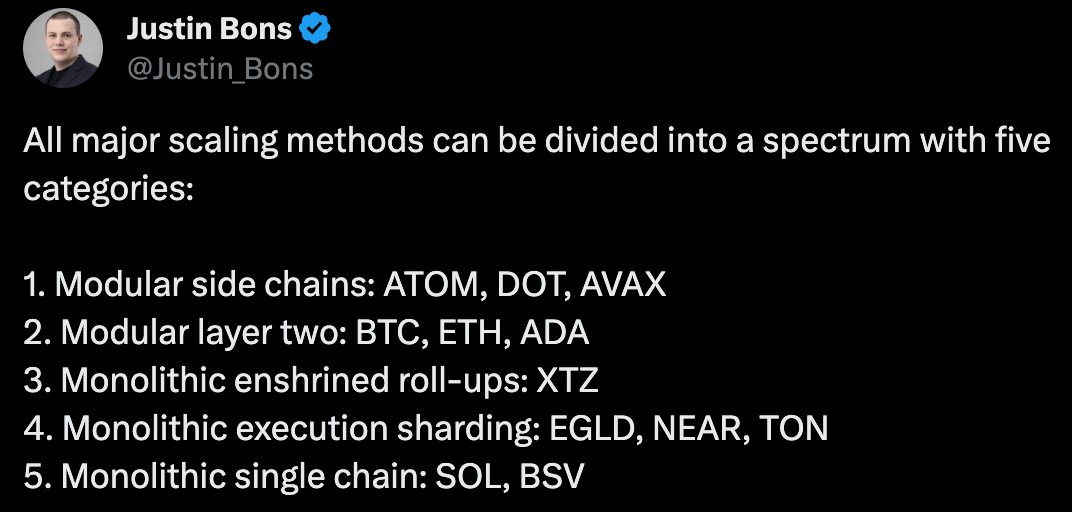

Avalanche: Doubling down on scaling via subnets, focusing on asset tokenization, bringing more stablecoins, becoming a forex trading chain, etc.

-

Polygon: Became a harbor for purpose-built L2s. The recent win in attracting OKX is a major success.

-

Near: Positioning itself as both a monolithic and modular blockchain. Partnering with Polygon to scale Ethereum at the DA layer, while also providing chain abstraction for L2s through unified UI (BOS) and L2 account aggregation.

-

Solana: Leading the wave of monolithic scaling, delivering fast transactions—speedy, without the fragmented user experience of modularity. I’ll share more on Ethereum vs. Solana in tomorrow’s blog post.

-

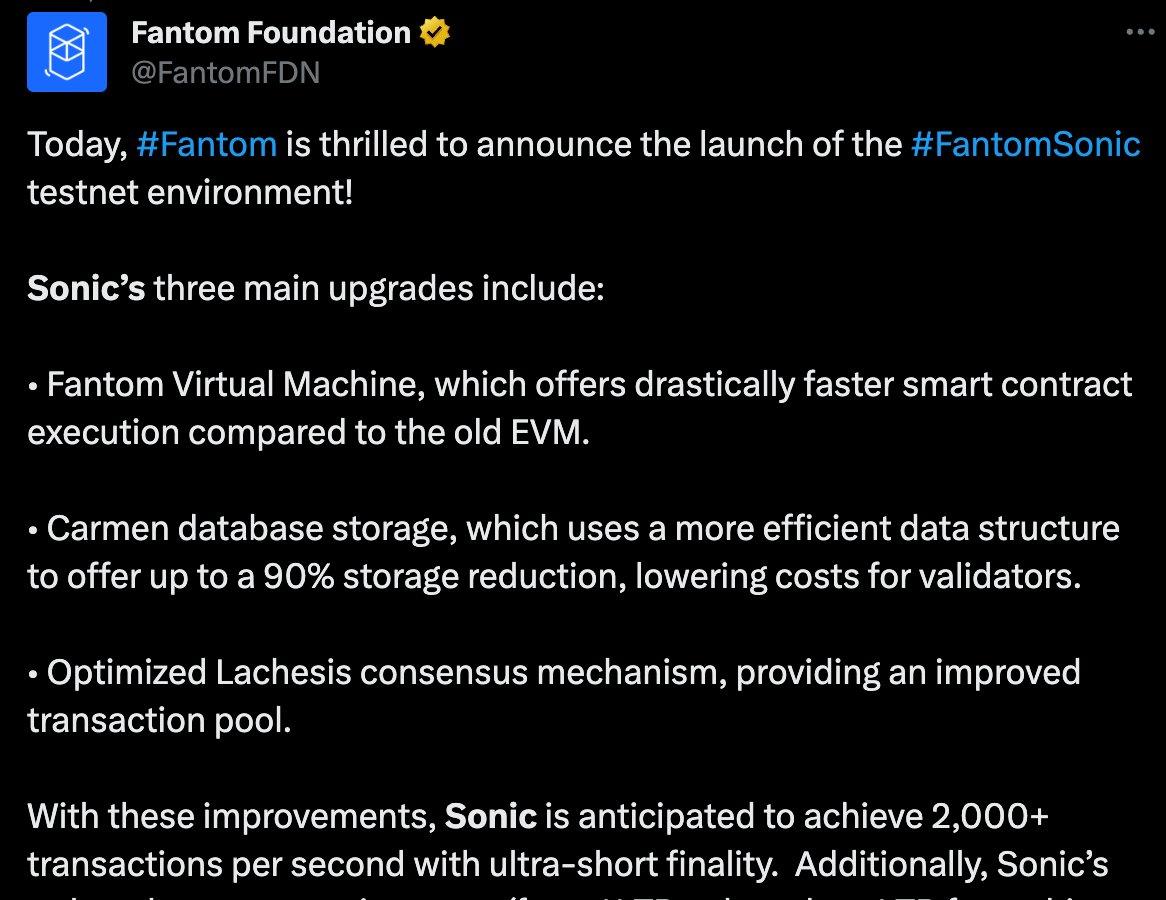

Fantom: Doubling down on monolithic design with the Sonic upgrade, achieving 2k TPS without sharding or L2s. Aiming to attract a new generation of dApps.

-

BNB Chain: Launched opBNB L2 to reduce fees, but the more important upgrade is BNB Greenfield, focusing on DataFi and decentralized AI (privacy-preserving large language model training) centered on data and IP monetization.

-

Cosmos: The ATOM token may appear to have lost its value proposition, but the Cosmos Hub is thriving thanks to the flourishing ecosystems of Osmosis, Injective, and Kuji.

L1s are now innovating and becoming specialized, while L2s appear to be retracing the old path of L1s—forking protocols to attract airdrop farmers, but lacking innovation and diversity.

Unfortunately, many L2 tokens suffer from poor tokenomics. Look at the problematic ARB token "staking" proposal.

Unsurprisingly, the old but solid L1 tokens are now rising. Compared to the previous bull run, they now offer more compelling value propositions.

Is this just a short-term reversal? I hope not.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News