Gaming Blockchain Research Report: Merit Circle is the Alpha Worth Investing in for Web2.5 Gaming

TechFlow Selected TechFlow Selected

Gaming Blockchain Research Report: Merit Circle is the Alpha Worth Investing in for Web2.5 Gaming

Merit Circle is a relatively standout project in this sector and offers higher investment value.

Secondary market fund Metrics Ventures GameFi industry research report overview:

-

Although the market currently holds a negative view toward Web2.5 games, we believe Web2.5 games will continue to attract game developers due to their unique advantages in game distribution and user acquisition. Growth on the supply and technology sides will eventually drive explosive demand-side growth.

-

Within the Web2.5 gaming sector, we are particularly focused on gaming platforms; gaming platforms offer greater narrative potential and longer lifecycles, playing a pivotal role on both the supply and demand sides of blockchain gaming.

-

Based on business models and token utility mechanisms, we classify gaming platforms into four types: tightly-coupled, moderately-coupled (public chain type), moderately-coupled (investment type), and loosely-coupled. We believe the moderately-coupled model is healthier and more scalable, establishing a positive alignment of interests with games.

-

We analyze leading gaming platform projects across three dimensions: strategic narrative, operational capability, and token economics. After comparison, we believe Merit Circle stands out as a bright spot in this sector and offers high investment value. Transitioning from a gaming guild to a gaming platform and now developing its own gaming public chain, Merit Circle demonstrates strong strategic vision, product development capabilities, and access to gaming resources, yet remains undervalued relative to peers, leaving significant room for growth.

Metrics Ventures GameFi Industry Research Report:

1 The Beginning: Why We Are Bullish on Gaming Platforms?

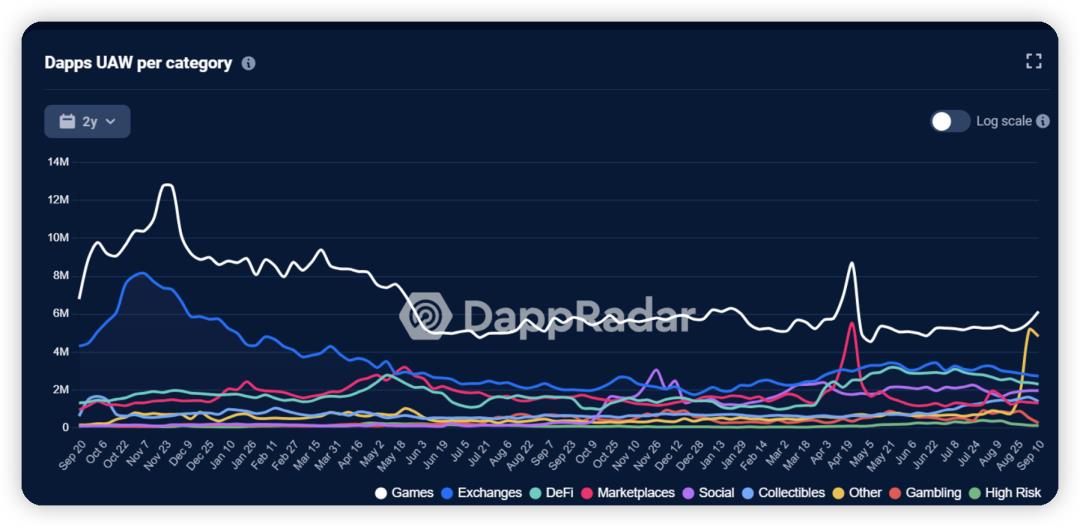

Despite the fading GameFi wave and declining dominance of blockchain game users, we observe that gaming remains the most active segment across the entire industry. According to DappRadar data, as of Q2 2023, daily unique active wallets in gaming reached 699,956, accounting for 36% of total industry participation—down from Q3 2021 levels but still ahead of other application categories.

Crypto games can be categorized based on their degree of blockchain integration.

The evolution from Web2 games to fully on-chain games (full-chain games) involves multiple steps: asset onboarding, transaction recording, achievement tracking, economic model integration, and core logic migration. Most current blockchain games have completed everything except core logic migration, thus being classified as Web2.5 Games.

Recently, full-chain games have gained widespread attention and become one of the hottest narratives in blockchain gaming. However, amid the enthusiasm for full-chain games, we believe the business model of Web2.5 games remains highly relevant to the broader gaming industry—even at its lowest point, Web2.5 games significantly reduce distribution and user acquisition costs through NFTs and token incentives, break geographical barriers, enable global traffic and capital liquidity from day one, and demonstrate clear advantages in improving distribution efficiency.

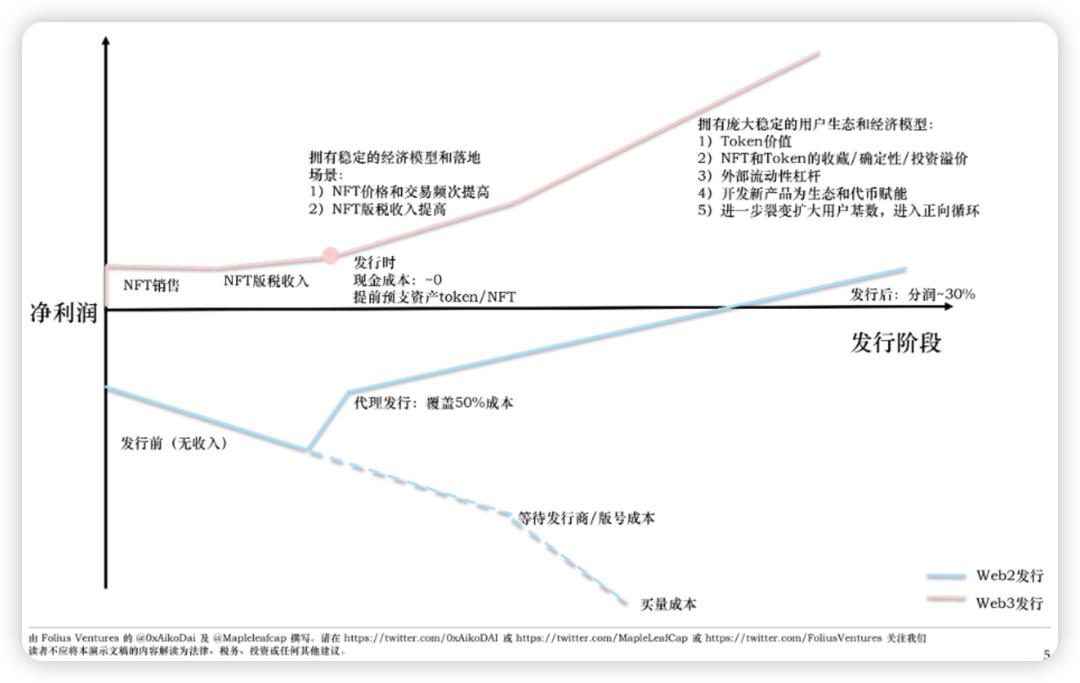

(For a full lifecycle comparison between Web2 and Web3 distribution, refer to the study by Folius Ventures below, original link)

User acquisition cost via NFT-based distribution approaches zero, whereas Web2 game user acquisition is far more expensive: RPG and SLG games typically cost $60–$150 per user, while strategy, casual, and mid-core games range from $6–$20 (data sourced from industry interviews, may differ slightly from official statistics).

These advantages strongly appeal to traditional game developers. Sustained interest from the supply side will enrich content creation within Web2.5 gaming, fostering truly playable and sustainable games in the Web3 space. With advancements in AA wallets, high-TPS, low-gas Layer 1, Layer 2, and even Layer 3 application-specific chains, the barrier to entry for Web3 will further decrease, becoming more user-friendly and seamlessly integrating on-chain operations into gameplay for smoother experiences.

Content enrichment driven by the supply side and UX improvements from technological advances will act upon the demand side of Web2.5 games, potentially triggering the next industry-wide boom. This synergy cannot be achieved in the short term by immature full-chain games, either on the supply or demand side. Therefore, we see this as a unique advantage of Web2.5 games and an ideal timing for positioning investments.

However, we must acknowledge the issues facing Web2.5 games and the challenges they face post-P2E wave. These games generally have short lifespans, especially P2E titles, primarily due to brief asset lifecycles, simplistic and unbalanced in-game economic designs, overly aggressive monetization, rapid capitalization, and highly speculative player behavior.

We believe Web2.5 games should emphasize two core principles:

-

Playability and game design quality

-

Advantages over Web2 games in distribution and user acquisition

The previous P2E cycle overly emphasized the second principle while neglecting playability. A healthier, more sustainable Web2.5 game should achieve both—richer content, stronger gameplay, scientifically designed and moderately complex economic systems, avoiding early-stage single-asset structures and premature capitalization. With such designs, we believe it’s possible to realize the previously mentioned dynamic where supply-side content growth and infrastructure development fuel demand-side expansion, driving the Web2.5 game industry forward—a direction the sector is already moving toward.

In summary, we believe Web2.5 games still hold substantial growth potential—an outlook that diverges significantly from current market sentiment. Market valuations for Web2.5 game projects are generally low, dominated by pessimism declaring "P2E is dead," especially amid the rising popularity of fully on-chain game narratives. In this context, Web2.5 games appear abandoned by the market.

Where others hear silence, we anticipate thunder. This gap between our perspective and mainstream opinion is precisely why we see investment potential and hidden value in this sector.

Within the development of Web2.5 games, we are particularly bullish on gaming platforms/ecosystems because:

-

Each Web2.5 game has its own lifecycle. Games themselves (both Web2 and Web3) naturally have life cycles, and crypto projects’ token economies also follow cyclical patterns. Compared to standalone game projects, gaming platforms and ecosystems have longer lifespans, are less affected by individual game cycles, possess greater resilience and risk resistance, and allow more time and space for experimentation to identify truly healthy and enjoyable games. The recent popular game Parallel TCG announced in January 2022 its integration into the Echelon Prime Foundation ecosystem, transitioning from a single game to a platform—a testament to this trend.

-

From the game developer's perspective (supply side): Gaming platforms and ecosystems provide funding, Web3 player communities, incubation capabilities, and other resources spanning multiple segments of the gaming value chain, serving as critical entry points for new games. During the current NFT bear market, cold-start financing and user acquisition through standalone NFT sales are increasingly difficult. Platform resources can further lower these costs, while platforms capture partial value from numerous individual Web2.5 game projects through well-designed tokenomics.

-

From the gamer’s perspective (demand side): Both Web2 and Web3 users benefit from curated game portals that help them discover suitable games. More importantly, blockchain infrastructure offered by platforms reduces friction during the Web2-to-Web3 transition, lowering barriers and enhancing user experience.

-

To escape the P2E trap, content creation and user acquisition must be decoupled—reducing the financialization of game content by extracting user acquisition (a financially driven function) into dedicated systems. This means professionalizing Web3 gaming platforms via tokenomic frameworks independent of direct game content, thereby reducing user acquisition costs. While current platforms haven’t fully achieved this separation, they represent the most promising path toward this goal within the GameFi space.

Currently, we define this sector as including the following categories:

- Game Development

- Publishing Platforms & Ecosystems

- Post-P2E Gaming Guilds

- Gaming Public Chains

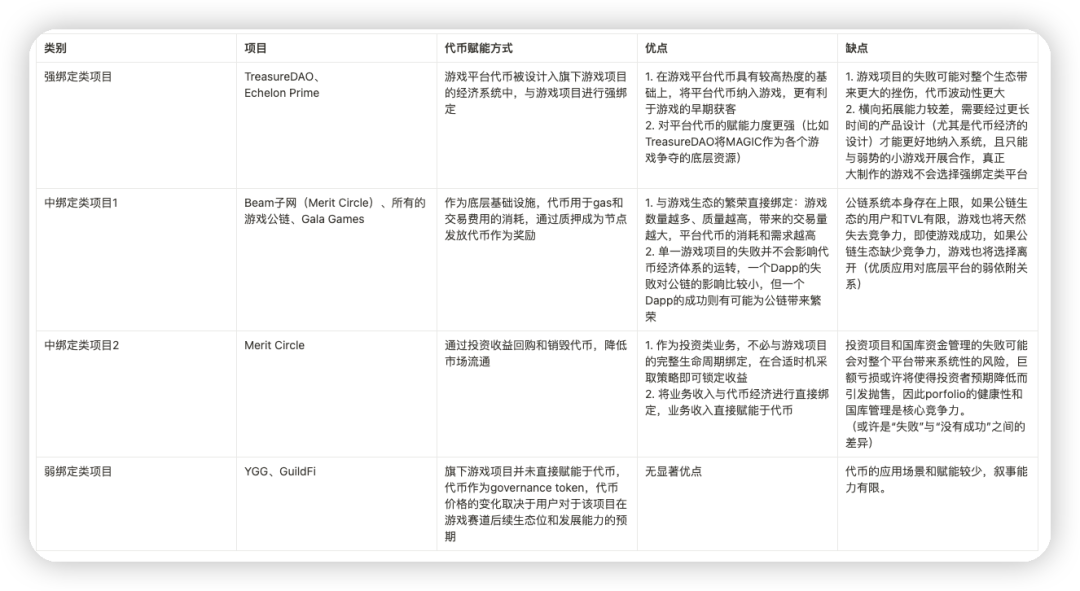

Among these, based on the strength of binding between gaming platforms and individual game projects—particularly regarding business models and token economy integration—we categorize these projects into four types. Xterio has not yet launched its token or disclosed its tokenomics, so we exclude it from classification here and only discuss its fundamental profile.

From a value chain and business model perspective, gaming platforms should serve as infrastructure supporting early-stage development, design, testing, and user acquisition for games, capturing value for these services rather than deeply integrating into game economic systems.

Moreover, early coupling of a game’s economy with a platform token may amplify speculation and financialization, accelerating the game’s lifecycle. Across existing tightly-coupled gaming platforms, interoperability scenarios between games remain limited despite shared base tokens, making claims of integrated ecosystems premature. Conversely, if platform tokens lack meaningful utility and are disconnected from operations, they lose compelling narratives for investors.

In conclusion, from both business structure and token utility perspectives, we believe moderately-coupled gaming platforms represent the healthiest model—featuring independent economic and operational loops, functioning as true standalone Web2.5 gaming infrastructure and service providers with strong horizontal scalability, whose token models ensure direct benefits from ecosystem success, creating a virtuous cycle of aligned incentives.

Next, we conduct comparative analysis across strategic narrative, operational capability, and tokenomics, concluding with valuation assessments and investment insights.

2 Strategic Narrative and Operational Capability: Sustainable Growth or Stagnation?

2.1 Strategic Narrative and Fundamental Analysis

TreasureDAO and Echelon Prime aim to build unified gaming ecosystems powered by a common base token and cross-game interoperability. TreasureDAO has been dubbed the “Nintendo of crypto” in several research reports.

Specifically, TreasureDAO originated from the Loot ecosystem before evolving independently into a decentralized gaming ecosystem built on Arbitrum, centered around MAGIC. Each project within the TreasureDAO ecosystem builds around the MAGIC token, though individual games may issue their own tokens. As a spin-off from Loot, TreasureDAO initially enjoyed strong community consensus. Later, by offering developer-friendly toolkits, it fostered a series of quality games, peaking in popularity with the breakout success of The Beacon.

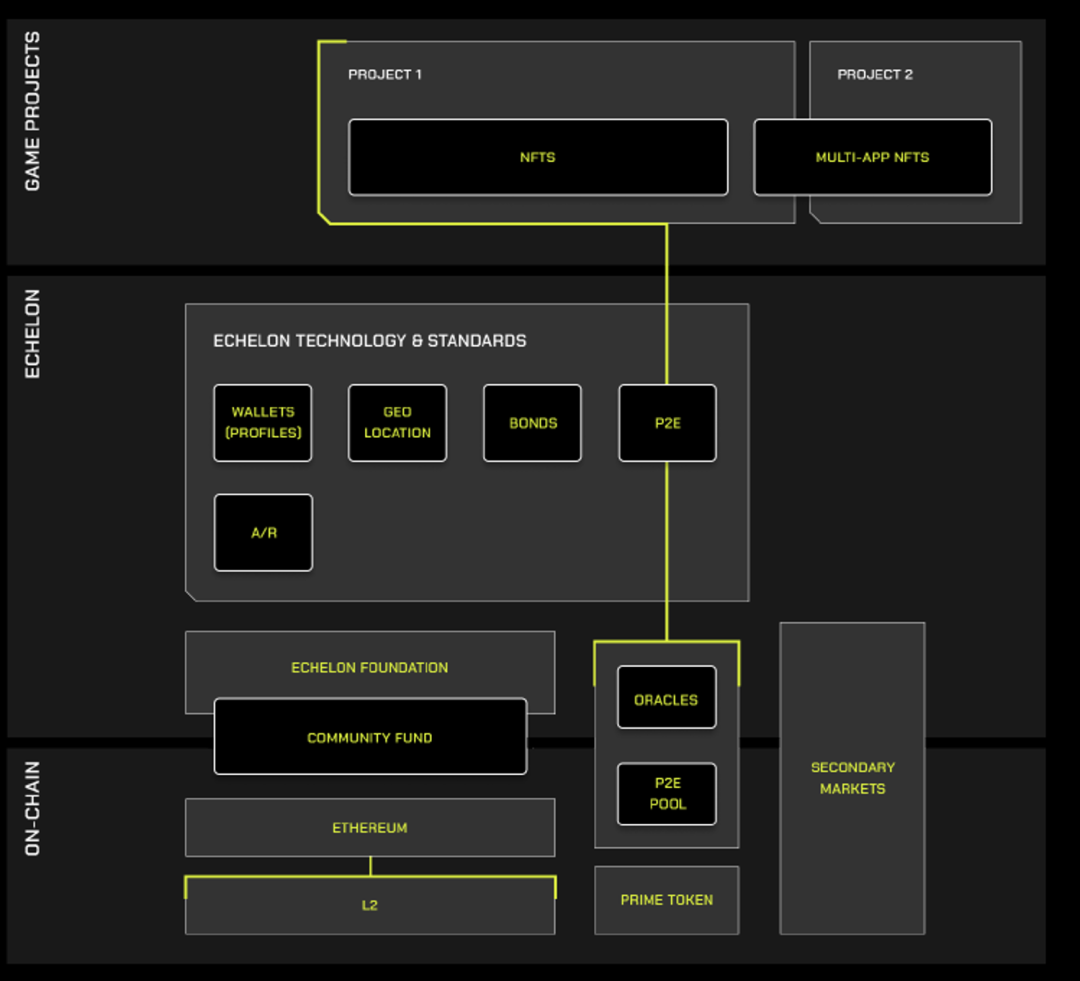

The Echelon Prime Foundation evolved from Parallel, aiming to advance gaming and P2E initiatives. It provides foundational infrastructure and a shared base token PRIME, offering tools such as Inb0x (secure wallet messaging), Bond (cross-game group creation), dedicated NFT distribution mechanisms, and oracles to support a larger gaming ecosystem. The Echelon ecosystem structure is shown below.

Echelon Prime originated from Parallel TCG, which received backing from Paradigm and top-tier game designers. Recently, it has drawn significant attention in the GameFi space. Its upcoming title Parallel Colony incorporates AI elements, yet still emphasizes the P2E narrative, potentially limiting future narrative flexibility. Currently, only two games exist in the ecosystem—Parallel TCG and Parallel Colony—leaving considerable uncertainty in its business trajectory. Indeed, PRIME speculation appears more tied to game hype than platform fundamentals.

Gala Games is an Ethereum-based game aggregation and publishing platform and was the leading platform during the last GameFi bull run.

Its ecosystem consists of five components: gaming platform, games, database, random algorithm, and node network. The decentralized node network forms Gala Games' foundation. Users who hold Gala’s Genesis Nodes can vote on which games get listed and earn revenue from game operations. According to official data, there are currently 44,433 active Genesis Nodes. Additionally, the platform uses a randomized allocation algorithm to airdrop in-game NFTs to Genesis Nodes as rewards. Gala Games raised initial funds solely through Genesis Node sales without external fundraising. On September 4th, it announced plans to migrate the entire Gala platform to GalaChain by year-end—an update requiring further observation—as ecosystem progress has been slow, raising questions about future execution.

Xterio is a game development and publishing platform providing seamless tools and infrastructure to facilitate Web3 game creation, aiming to become a GaaS (Games-as-a-Service) platform.

Xterio’s technologies include CPDM (enabling cross-game NFT interoperability and privacy protection using ZKP) and AI (partnering with Palio to integrate AI into games and offer developers AI toolkits). Xterio maintains its own internal development team while also publishing and supporting third-party games, investing in Web3 studios like Overworld and GamePhilos, and securing partnerships with FunPlus, Com2us, and XPLA.

Gaming public chains represent a key category within gaming platforms. Their public-chain-level narrative often commands higher valuations, providing fertile ground for games with high TPS and low gas fees. Technologically, these include L1 blockchains, Ethereum L2s, Avalanche subnets, and emerging L3 solutions. However, the real moat lies in attracting and retaining quality game projects. Below we review leading gaming chains.

Wemix and Oasys are gaming public chains from South Korea and Japan, respectively.

Wemix was developed by Wemade, known for flagship title *MIR4*. Oasys founding members include YGG co-founder, CEO of blockchain game studio double jump.tokyo, President & CEO of Bandai Namco Research Institute, and Sega Co-COO, supported by 21 institutional nodes comprising major gaming companies and crypto investors.

Ronin Network, launched by Axie Infinity’s Sky Mavis, is an EVM blockchain tailored for gaming.

Immutable, developer of the blockchain game Gods Unchained, has built two Ethereum Layer 2 solutions for NFT and GameFi projects: Immutable X and Immutable zkEVM. Immutable X leverages StarkWare’s ZK-STARK technology, while Immutable zkEVM is a game-specific, EVM-compatible, low-cost, high-scalability chain launched in mid-August 2023, built on Polygon Edge as an Ethereum ZK-Rollup L2.

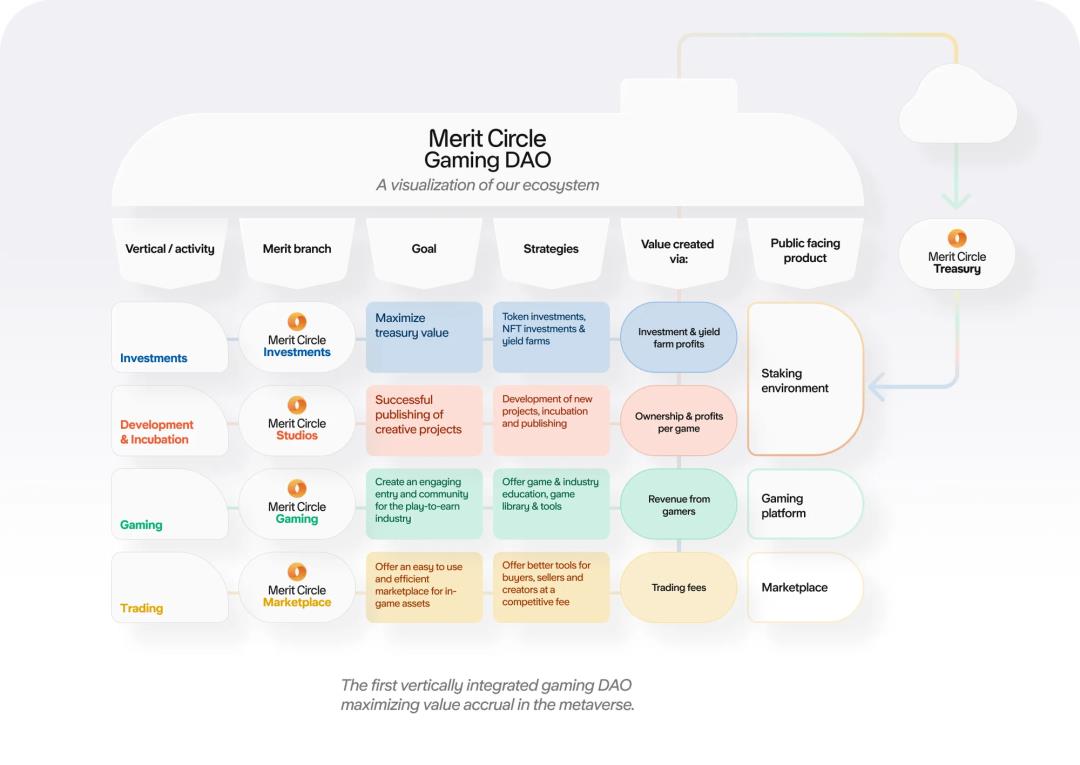

Merit Circle has undergone a dramatic strategic shift since the last GameFi bull market, transforming from an unsustainable guild model into a hybrid investment and gaming chain platform. Its decisive pivot reflects a clear strategic roadmap and high execution capability.

Merit Circle’s current operations span four main areas: Investments / Gaming / Studios / Infrastructure—covering multiple stages of the gaming value chain. Notably, it has completely shut down its scholarship program, signaling a firm commitment to transitioning from a gaming guild to a comprehensive gaming platform.

Investments remain Merit Circle’s core activity, encompassing token, NFT, and equity investments with staking operations. Studios focus on incubating innovative breakthrough projects. Gaming serves as an aggregated platform offering incentivized community activities, member education, and practical tools. The most critical infrastructure component is Beam subnet, recently launched. Merit Circle has approved a proposal to convert MC tokens into BEAM tokens, positioning the gaming chain narrative as its primary strategic direction going forward.

YGG and GuildFi have evolved beyond initial play-to-earn guilds, maintaining a guild-centric narrative focused on game investments, collaborations, incubation, player education, and expanding guild membership and community networks.

Beyond scholarship programs and collaborative incubations, YGG partnered with Nas Academy to launch Web3 Metaversity, enabling badge holders to acquire new skills and career opportunities. Initiatives like GAP (Guild Advancement Program) incentivize and unify members, while SubDAO expansions grow gaming communities. YGG has also ventured into esports. GuildFi, originating from Thailand’s largest gaming community, has developed an achievement system and Metadrop Launchpad to reward player engagement. Both guilds retain significant influence and value chain positions in GameFi, with YGG’s leadership status particularly notable. However, as previously analyzed, their narratives, operations, and token utilities remain loosely connected—raising concerns about whether business growth can translate into token price appreciation.

2.2 Operational Capability Analysis

This report evaluates platform capabilities based on ecosystem size and development. For investment-focused platforms like Merit Circle, YGG, and GuildFi, performance and risk are heavily influenced by treasury stability. Thus, we compare their investment returns and treasury management.

2.2.1 Ecosystem Development

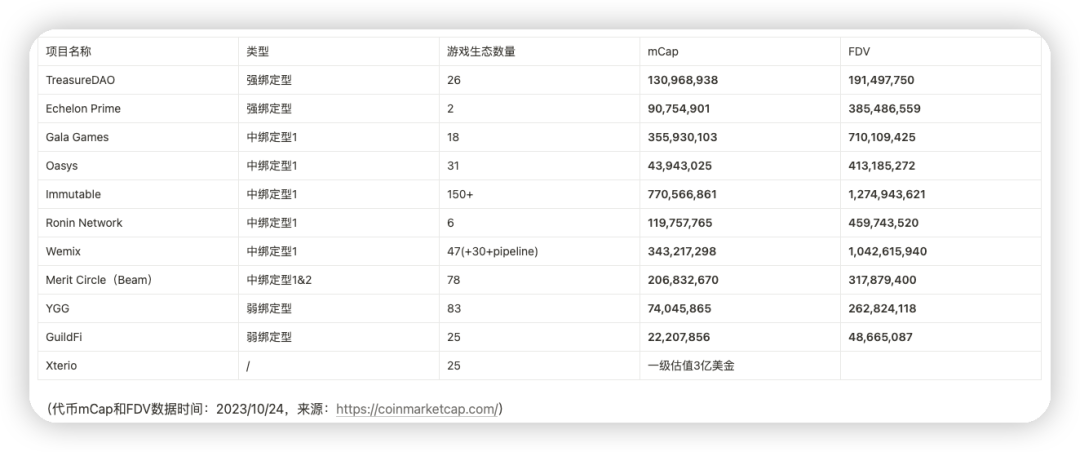

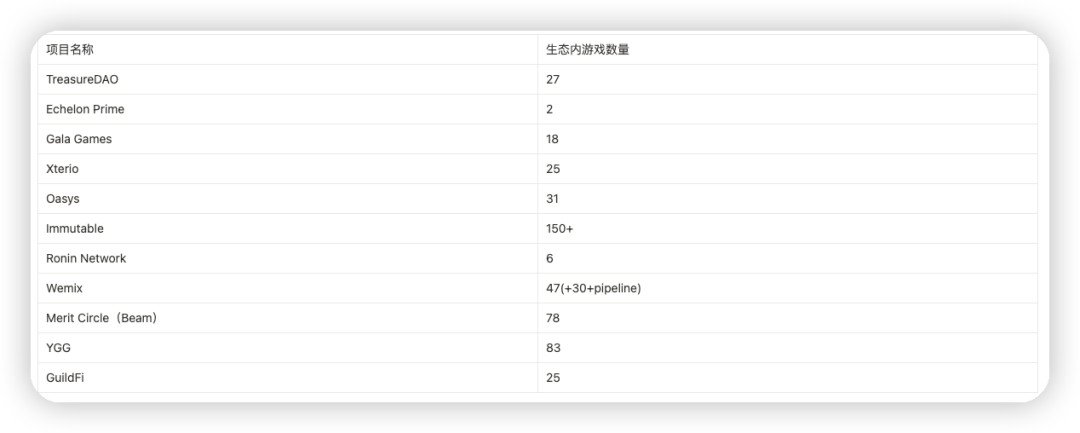

Below shows the number of games in each project’s ecosystem, with detailed analysis:

TreasureDAO officially showcases 27 games on its platform, including popular titles like The Beacon, Realm, and BattleFly. Current ecosystem infrastructure includes Bridgeworld (ecosystem hub), Trove, MagicSwap, TreasureTag, and an achievement system. TreasureDAO emphasizes cross-game connectivity, primarily through MAGIC as a shared base token. More advanced efforts include integrating games like The Beacon and Knights of the Ether into Bridgeworld via Harvester—but such implementations remain limited.

After The Beacon’s popularity faded, TreasureDAO’s DAU dropped sharply, with July MAU around 10,000—down from 90,000–100,000 at end-2022. Marketplace volume in July was approximately $1M, confirming that hit games drive massive but fleeting user growth, with limited game expansion capacity and rapid user attrition.

Echelon’s ecosystem includes only two games: Parallel TCG and Parallel Colony. TCG is in beta testing, while Colony remains in development. Parallel TCG is an Ethereum-based sci-fi NFT trading card game where players build decks to compete for rewards. Parallel Colony is a narrative-driven life simulation game incorporating AI and ERC-6551.

Gala Games hosts 18 games, but only 6 are live, with 12 still in development. Overall, ecosystem growth is slow, lacking consistent new releases or breakout hits. Although Gala announced Project GYRI (its own gaming L1, later named Gala Chain) in February 2022, updates have been scarce.

Xterio has announced 25 projects: 4 internally developed and 21 partnerships. Most remain in pre-registration or development phases, especially the self-developed titles, which require market validation.

Oasys hosts 6 Verses (L2s for DApps), totaling 31 games, with 17 currently playable.

Immutable’s ecosystem is growing rapidly. Through partnerships with GameStop, Warner Games, iLogos, Mineloader, and Secret6, it supports over 150 NFT and gaming projects, with 74 listed on its website—including new collaborations formed after launching Immutable zkEVM, though not yet publicly accessible. Notable breakout games include Illuvium and Gods Unchained. According to Footprint data, ImmutableX maintains stable leadership in gaming transaction volume over the past three months. With the introduction of Immutable zkEVM, its ecosystem is poised for further expansion.

Ronin still functions largely as an app-specific chain for Axie Infinity, listing only six games on its site. According to DappRadar, only Axie shows meaningful UAW. Despite Axie’s massive traffic keeping Ronin competitive in gaming chain volume, newer chains are encroaching on its space. Without new game integrations, Ronin risks stagnation.

Wemix currently supports 47 projects, including 32 games, 5 DeFi, and 9 NFT projects. Additionally, WEMIX PLAY has over 30 games in pipeline.

Merit Circle has invested in 78 projects across tokens and equity, covering standalone games, gaming infrastructure, and platforms—including high-profile ventures like OhBabyGames, Gameplay Galaxy, Delabs Games, and Roboto Games backed by major institutions. Notably, Merit Circle recently unveiled technical details of its Avalanche gaming subnet Beam. Partnering with Openfort on account abstraction, Beam launched the Beam Companion mobile app for managing in-game assets, Sphere NFT marketplace for internal trading, and Beam SDK for rapid developer deployment. These frictionless infrastructures significantly aid developer onboarding, enhance player experience, and improve retention—laying the groundwork for Beam’s ecosystem growth.

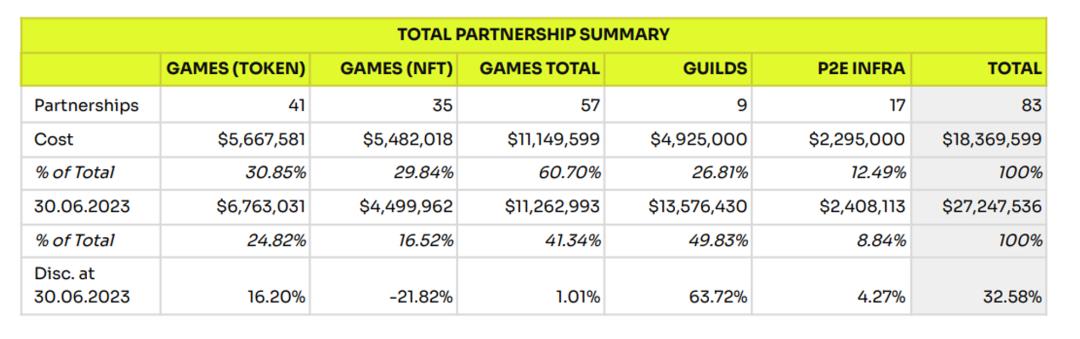

YGG has partnered with 83 projects: 57 games, 17 P2E infrastructure, and 9 gaming guilds. Notably, as of June 30, 2023, gaming guild stakes yielded the highest returns for YGG.

GuildFi hasn’t disclosed specific early investments or strategic game partnerships. Its Games Portal lists only 25 games, mostly older titles, suggesting weaker external collaboration and ecosystem expansion compared to peers.

2.2.2 Comparative Investment Capabilities: Merit Circle vs. YGG vs. GuildFi

We conduct a horizontal comparison of investment capabilities among Merit Circle, YGG, and GuildFi.

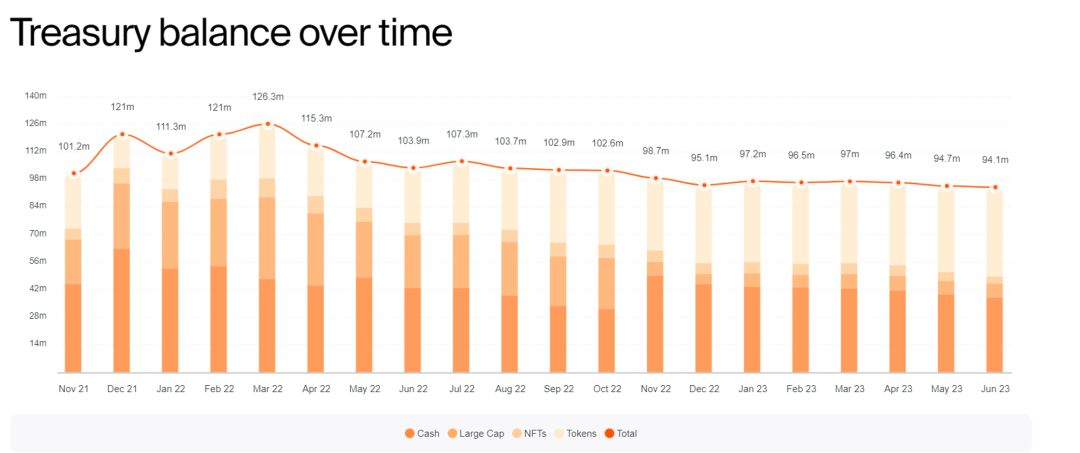

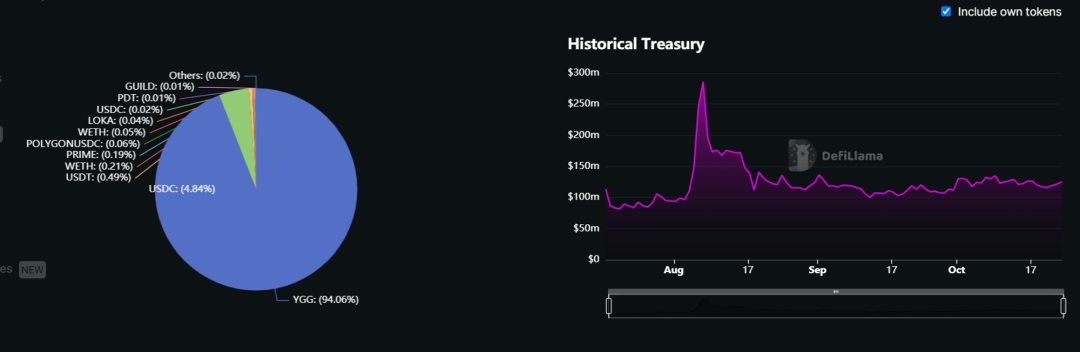

Regarding treasury composition and management, Merit Circle holds a substantial treasury ($94.1M) and transparently discloses allocations. As of June 23, 2023, its AUM had declined only 25.49% from ATH—one of the smallest drops among gaming guilds. Stablecoins make up $38.1M (40.49%), with the remainder mainly in private equity investments. According to Defillama, 94.05% of YGG’s treasury ($123.77M) consists of YGG tokens, indicating extremely weak risk resilience. Due to sharp declines in YGG’s token price, its treasury AUM has fallen over 90% from peak. GuildFi’s treasury AUM stands at $92.68M, with stablecoins, BTC, ETH, and LP positions totaling $71.89M (77.57%)—the highest proportion of stable and blue-chip crypto assets among the three. Based on disclosed wallet addresses and Debank data, GF tokens constitute a large share of its token holdings.

Thus, Merit Circle leads in treasury management with balanced stablecoin and investment allocations. YGG’s >94% YGG token concentration is clearly unreasonable. While GuildFi’s high stablecoin ratio minimizes risk, it raises concerns about its ability to invest in and collaborate with gaming projects. (Below are treasury compositions for Merit Circle, YGG, and GuildFi respectively.)

-

On investment mechanisms and risk control, Merit Circle has established clearer protocols. MIP-6 introduced a de-risking evaluation framework allowing DAOs to exit investments under predefined conditions (e.g., selling principal upon 10x gain). Neither YGG nor GuildFi has similar mechanisms.

-

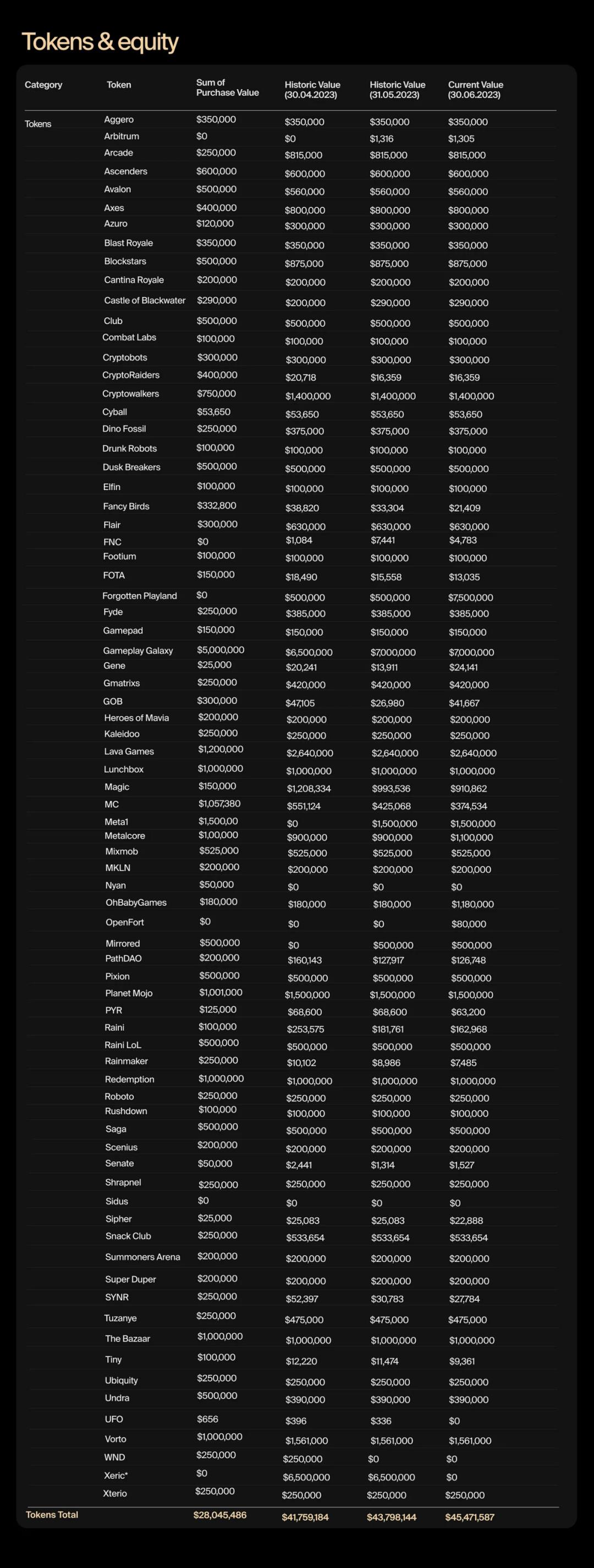

In terms of investment returns, Merit Circle’s latest financial report shows token and equity investments with a total purchase value of $28,045,486 now valued at $45,471,587 (62% unrealized gain); NFT investments purchased for $4,834,000 are now worth $3,404,852 (loss), resulting in a combined unrealized gain of 48.65%. YGG’s total investment purchase value is $18,369,599, now valued at $27,247,536 (32.58% gain), showing solid returns from game and token investments. GuildFi has not disclosed specific returns or investment details.

-

Therefore, Merit Circle shows slightly better returns. However, given the overall downturn in GameFi, differences in investment performance are relatively small, with all suffering NFT-related losses. Hence, we place greater emphasis on underlying capabilities—treasury management, risk controls, and ecosystem depth.

3 Tokenomics: How to Share in Gaming Success?

In terms of token circulation and future unlocks, only TreasureDAO and Merit Circle currently have high float ratios. Most other projects have less than 50% circulating supply. From a potential sell-side pressure perspective, Merit Circle and TreasureDAO face lower downside risks.

On token issuance and utility, gaming ecosystems and chains follow similar models: users earn tokens via mining (staking on chain or in-game), then spend them as payment mediums (for NFT trades or gas) or in-game consumables. Some tokens re-enter circulation after use (e.g., PRIME returns to reward pools), while others are burned (e.g., GALA, WEMIX). TreasureDAO exhibits tighter integration—MAGIC serves as direct in-game rewards, a participation requirement across multiple games, and a contested resource among projects.

Gaming guild platforms differ slightly. Merit Circle, having undergone major strategic transformation, offers richer token utilities with four main use cases:

-

Governance: Any MC holder can submit and vote on MIPs. Notably, Merit Circle maintains high DAO governance standards, having conducted 29 MIP votes guiding strategic direction. MIP-2 formed an investment committee; MIP-6 created structural risk mitigation for early-stage liquid investments; MIP-4 guided platform and NFT market development; MIP-17 restructured the DAO. Recently passed MIP-28 and MIP-29 approve converting MC to BEAM tokens.

-

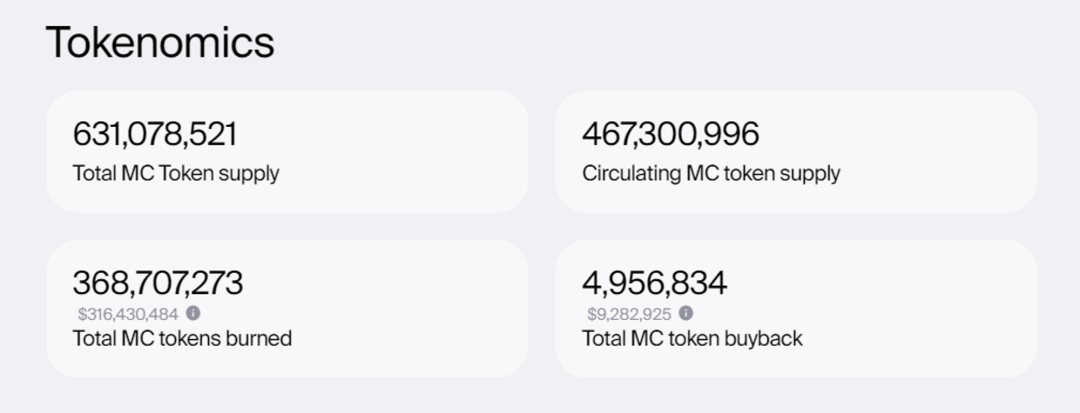

Buyback and Burn: Merit Circle uses investment profits to buy back and burn MC tokens, reducing circulating supply. To date, 368,707,273 tokens have been removed from circulation.

-

Gas Fee on Beam Subnet: Beam is Merit Circle’s Avalanche-based gaming subnet using MC (BEAM) as gas fee. This greatly expands MC’s utility, adding a public chain narrative to complement its strong investment track record. MIP-28 and MIP-29 approved converting MC to BEAM at a 1:100 ratio, strengthening the chain narrative’s impact on the MC ecosystem.

By contrast, YGG and GuildFi—despite originating as gaming guilds—have weaker tokenomics, relying mostly on staking for yield. YGG Reward Vault is central to its token utility: members holding Guild Badges can stake YGG tokens to earn game token rewards (LOKA, THG, GHST, RBW). GuildFi rewards LP stakers.

4 Conclusion: The Next Alpha in Gaming Platforms

We summarize and synthesize our evaluation of these projects. From token utility and business model perspectives, we favor moderately-coupled gaming platforms for their sustainability and health. Within this group, Gala’s ecosystem growth is sluggish, GalaChain migration remains uncertain, and team controversies have damaged investor confidence—similar to earlier Wemix issues. Oasys boasts strong traditional gaming industry backing but lacks a breakout title; its ecosystem requires further validation. With only ~10% token circulation, it carries potential downside risk. Immutable, building two Ethereum L2s, hosts 150+ game partners and leads in daily transaction volume among gaming chains—making it one of the fastest-growing ecosystems with notable star projects. However, it commands the highest valuation—roughly double that of peers. Ronin’s ecosystem grows slowly, remaining largely tied to Axie Infinity’s single-game narrative.

In sum, Merit Circle stands out as a standout performer with superior investment value in this sector.

-

Fundamentally, Merit Circle’s transformation from guild to platform to public chain reflects a clear strategic vision and exceptional execution. It combines investment and public chain narratives with highly scalable operations. Its strengths in ecosystem development, treasury management, team direction, and DAO operations surpass peers. Beam subnet development now drives Merit Circle’s next phase, evident in the MC-to-BEAM token migration. As a priority within the Avalanche ecosystem, Beam—with Merit Circle’s gaming resources—is better positioned than competing app chains to attract developers and achieve initial traction.

-

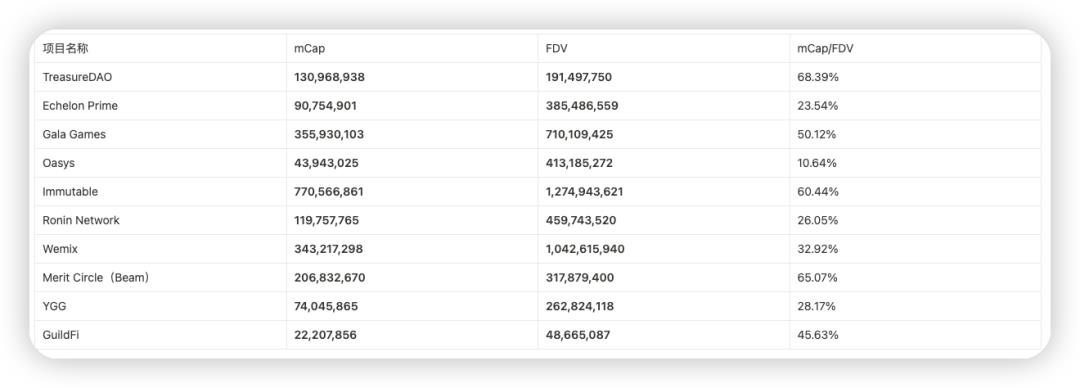

Second, from a valuation standpoint, MC’s current FDV is $317,879,400—relatively low among gaming platforms. Given its fundamentals and narrative strength, it remains undervalued, offering attractive investment upside.

-

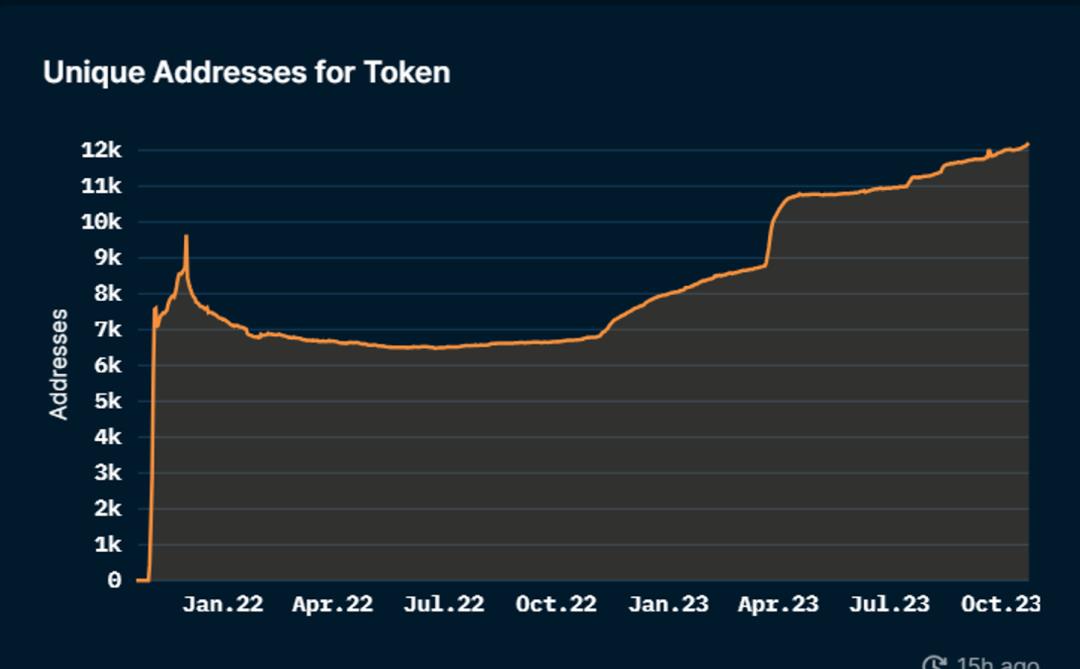

Third, regarding token distribution, MC already has high circulation, minimizing future unlock pressure. On-chain data shows holder count has steadily risen since end-2022, doubling to ~12,000 today, with continued modest growth. Nearly all holdings exceed one month in duration, indicating strong long-term commitment. Among early adopters, 85 of the first 100 addresses remain holders. Top 5 holdings remain stable at ~25%.

In conclusion, we believe Merit Circle is a compelling project worth positioning in both the Web2.5 gaming platform space and the broader Web2.5 gaming sector.

Additionally, among other project types, TreasureDAO exemplifies a deeply crypto-native gaming ecosystem. Leveraging The Beacon’s success, it became Arbitrum’s largest gaming ecosystem—an evolution we’ll continue monitoring.

Echelon Prime remains in early stages as a gaming platform, achieving peer-level FDV primarily through a single card game narrative.

Xterio possesses technological advantages and solid gaming industry connections. With a relatively high pre-launch valuation, we will closely monitor XTER’s economic model rollout, secondary market performance, and game development progress.

YGG and GuildFi, as veteran gaming guilds, continue innovating in community building and retain deep value chain roots—warranting ongoing attention. Potential expansions in token utility could drive future price appreciation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News