Bitcoin's Cryptocurrency Free Banking System

TechFlow Selected TechFlow Selected

Bitcoin's Cryptocurrency Free Banking System

This article covers the theories of full reserve banking and free banking, and applies these systems to technologies such as the Lightning Network (LN) and federated Chaumian minting.

Author: Eric Yakes

Translation: Block unicorn

There are strong reasons to support the existence of Bitcoin-based banks issuing their own digital cash currencies redeemable for Bitcoin. Bitcoin itself cannot scale to broadcast every financial transaction on Earth to everyone and include it in the blockchain. A secondary payment system is needed—one that is lighter and more efficient. Likewise, waiting for Bitcoin transactions to confirm is impractical for medium to large purchases.

Bitcoin-based banks would solve these problems. They could operate as banks did before national monetization. Different banks could have different policies—some more aggressive, others more conservative. Some could be fractional reserve, while others might be 100% Bitcoin-backed. Interest rates could vary. Some banks’ cash might trade at a discount to other banks’ cash. — Hal Finney

Block unicorn note: Hal Finney was one of the early supporters and participants in Bitcoin. He was a computer scientist with extensive knowledge and experience in cryptography, cryptocurrencies, and blockchain technology. Hal Finney was one of the first recipients of a Bitcoin transaction and interacted with Satoshi Nakamoto, Bitcoin's creator. He was highly active in the Bitcoin community and made significant contributions to the development and promotion of the technology. Hal Finney passed away in 2014 due to ALS (amyotrophic lateral sclerosis). His contributions had a profound impact on the development of Bitcoin and blockchain technology, and his name is often associated with Bitcoin's early history and evolution.

The future of Bitcoin is uncertain. We don't know how well it will scale, how privately it will be used, how it will be stored, or even how it will be used for payments. Beyond protocol and application advancements, the development of a Bitcoin financial system may have the most significant impact on the value of the Bitcoin asset, with a very wide range of potential outcomes. Consider two hypothetical extremes: in one scenario, all Bitcoin is held by third-party custodians, and users exchange receipts. In another, Bitcoin becomes a self-hosted peer-to-peer asset used by everyone worldwide, offering various financial functions.

Both extremes are unrealistic; at maturity, the system will likely settle somewhere in between. Many people will use custodial institutions to store their Bitcoin, while others will not. Some will use protocols allowing unilateral exit, while others will trade rights issued by third parties representing underlying Bitcoin.

What makes the emerging Bitcoin financial system unique is the application of cryptography to fundamental financial functions. Novel technologies are being built or theorized that will enable unprecedented functionality, resilience, and ultimately foster competition among Bitcoin financial intermediaries. The key feature of these new technologies is their peer-to-peer (P2P) exchange capability; Bitcoin financial intermediaries will certainly exist as commercial options, but new direct operations and exchanges will also emerge.

I will analyze the possibilities of such a system’s development but deliberately adopt a biased perspective: I assume a basic premise—that greater P2P (peer-to-peer) possibility is better. Better means I believe financial autonomy is a fundamental good worth pursuing; but also better in terms of Bitcoin’s overall stability and neutrality. Trustworthy third parties may emerge to offer convenience, but if they (governments, centralized organizations) dominate over P2P counterparts, the entire system will be threatened.

This article expands on my previous piece “Bitcoin Banks,” which covered theories of full-reserve banking and free banking and applied these systems to technologies like the Lightning Network (LN) and federated Chaumian mints. I will extend this analysis, introduce other emerging technologies, and focus on the possible economic characteristics of resulting hybrids. The best starting point is discussing trust.

You Only Need to Trust the Community

Few species cooperate as extensively as humans. We cooperate best with our closest kin because their genetic interests align most closely with ours, as genes compete to propagate into future generations. Evolutionary biologist John Maynard Smith proposed that when solving strategic problems under competition, genes evolve toward Nash equilibria. This is known as an evolutionarily stable strategy—our genes evolve to influence our behavior, generally leading us to help those who are genetically most similar to us.

Within limited geographic areas, community interests often align relatively well. For example, everyone can agree they want safety. Disagreements lie in methods and costs.

Genetic alignment varies geographically, but geographical alignment, by definition, does not change. Across the world, members of communities share highly aligned interests. Being part of a community brings many benefits.

As individuals gain more from their community, their risk of loss increases. The social risk hypothesis suggests depression is an adaptive, risk-averse response to threats of social exclusion, which critically impacts human survival and reproductive success. Humans are likely innately predisposed to avoid social exclusion.

Undoubtedly, humans are selfish, and their interests often diverge from community interests. No amount of evolutionary theory can stop littering, nor prevent someone from throwing a loud party for personal enjoyment, disturbing neighbors' sleep. While these examples may cause some social friction, they typically result in discomfort rather than risks severe enough to justify social exclusion. In contrast, if a community member is caught stealing someone else’s car, the social consequences could be far more serious.

In the absence of social exclusion costs, moral hazard frequently arises, as the benefits of betraying conflicting interests outweigh the benefits of maintaining long-term net positive contributions. Known as the principal-agent problem, conflicts of interest between principals and agents lead to moral hazard, all else equal. Community social costs do not resolve the principal-agent problem, but they do mitigate it.

Moreover, communities have evolved with the advent of the internet. This evolution has made geography less crucial to community cohesion while enabling globally distributed communities based on shared interests. Global online communities are not results of genetic or geographic alignment but form around common interests. There is great potential for new technologies and financial arrangements within online communities, discussed in detail below.

Where economic agents exist, community trust can reduce moral hazard. The internet has enabled new forms of community trust, which in turn can mitigate novel economic risks.

Community and Value

Community trust can be leveraged in multiple ways. For centuries (possibly millennia), informal financial groups have existed as mechanisms for saving and borrowing—such as savings and credit associations, village savings and loan associations, savings and credit cooperatives, etc. Today, informal financial groups remain the primary mechanism for saving and borrowing among populations disconnected from formal financial institutions.

Community trust is also leveraged through formal financial institutions. As of 2018, there were 85,000 credit unions globally, serving 274 million members. Before the financial crisis, commercial banks issued subprime loans five times the volume of credit unions, yet during the crisis, commercial banks were 2.5 times more likely to fail. Credit unions enjoy higher public trust, and small businesses report 80% lower dissatisfaction with credit unions compared to large banks.

According to the FDIC’s 2020 Community Banking Report, community banks are less likely to close, have performed better since the financial crisis, are major funders of local businesses (especially commercial real estate, small business, and agricultural lending), and are more prevalent in rural areas—the essence of community banking is localization.

As physical bank branches become economically unviable or inaccessible in many rural areas, people seek digital solutions to provide banking services to the unbanked. Bitcoin is an emerging digital currency system with characteristics enabling the formation and development of both informal and formal financial groups. As a monetary asset, Bitcoin uniquely allows individuals to self-custody, making participation in banking systems optional rather than necessary.

Additionally, Bitcoin’s nature as a natively digital currency enables globally connected populations to voluntarily form financial groups. Bitcoin’s programmability allows these groups to innovate new trust mechanisms. With this technology, community-based financial groups can form without geographic constraints. By using Bitcoin for transactions and various financial functions, geographically dispersed communities can achieve shared benefits.

Bitcoin’s technical characteristics enable voluntary adoption across widely distributed geographic communities. Novel organizational forms are emerging, with the potential to spawn new financial systems and economic value.

Fedimint is a protocol integrating four main technologies:

1. Federations: A group of individuals with computers capable of providing their own storage and processing power to the community. Their computers run identical software, enabling communication. Federations consist of leaders (“guardians”) who generate and control multi-signature Bitcoin addresses and possess software to communicate with the Fedimint protocol. When users wish to join a federation, they leverage its storage, processing capacity, and credibility. This allows them to use any applications offered by the guardians. The primary application will be Chaumian eCash (defined below), but theoretically, it could be anything, likely mostly financial applications. Federation technology offers users many capabilities, but its core value proposition is enabling guardians to faithfully execute protocols on behalf of users.

2. Multi-signature (multi-sig): Bitcoin is stored in a multi-signature address controlled by the federation’s guardians. To send a Bitcoin transaction, a certain number of signatures from the address are required. For example, a 3-of-4 multi-sig has four possible keys but requires at least three to send Bitcoin.

3. Chaumian eCash: A private representation of value tradable as quasi-bearer instruments. It uses a cryptographic construct called “blind signatures”: the issuer of eCash (in this case, the federation) does not know the identity of the recipient (user), but any third party can verify that the “signature” on the eCash originates from that federation. This allows the federation to issue eCash to users depositing Bitcoin into the federation’s multi-signature address. Users store eCash on their devices (and can back it up with the federation if they lose their device), making it a trust-dependent digital bearer instrument. eCash created by guardians exists off-chain; it resides only in users’ device memory, like smartphones, similar to physical cash, and can be backed up against loss. This eCash scheme provides a payment method preserving Bitcoin’s censorship resistance while enhancing privacy, though it remains vulnerable to inflation if a majority of Fedimint guardians collude maliciously and secretly increase supply.

4. Lightning Network (LN): The Lightning Network (hereafter “LN”) can ideally be used via Lightning gateways (discussed below) to forward payments between federations. This creates the ability to instantly exchange eCash (digital cash) for Bitcoin, with several implications. Importantly, it increases fungibility among eCash issued by various federations, reducing incentives for many people to join a single federation. Increased fungibility among different federations’ eCash combined with optimized community trust fundamentally incentivizes systemic decentralization.

The combination of these technologies forms a set of rules that Fedimint software users must follow—this defines the Fedimint protocol. As an open-source protocol, anyone can participate. The ecosystem includes the following participants:

Users: Individuals possessing applications capable of running Fedimint, possibly including Bitcoin and the Lightning Network (LN). They send Bitcoin to the federation’s multi-signature address in exchange for eCash. They can send eCash or LN payments between any applications connected to their wallet, limited only by sufficient eCash/LN balance and others’ acceptance of eCash/LN.

Guardians: Individuals selected by the community to establish nodes communicating with Bitcoin, LN, and Fedimint. They form federations, manage hardware, control Bitcoin in multi-signature addresses, and issue eCash. They can also serve as Lightning gateway providers, though this requires specialization (discussed below), so another entity called a Lightning Service Provider (LSP) may fulfill this role.

Lightning Gateways: Liquidity providers operating Lightning nodes integrated with Fedimint. Readers can think of them as Lightning-to-eCash exchanges connected to Fedimint, integrating with Fedimint users as market makers ready to send LN payments and receive LN payments at a spread. Any federation user can do this, but operating well-connected, high-capacity Lightning nodes requires specialization, so this function may be provided by extended LSPs. If a user wants to “send eCash” to another Fedimint user, they send eCash to a gateway, which forwards an equivalent LN payment to another Fedimint’s gateway, which then sends eCash to the recipient user. eCash cannot leave a Fedimint; it can only be exchanged for Bitcoin or LN Bitcoin, which can then be received by another Fedimint’s gateway and converted back to eCash in the new domain. However, users can integrate with multiple federations and exchange eCash between users of these federations.

Modules: Applications within the Fedimint protocol. For a specific federation’s users to use a module, the federation must support it. Fedimints launch with three standard modules: Bitcoin, eCash, and Lightning adapter. Future potential modules include smart contract platforms and federated markets. Any federation can choose to support any module. Some federations will have high-performance infrastructure supporting demanding, potentially commercial-scale applications, while others will have minimal infrastructure supporting only basic functions like sending eCash and LN payments. Users can integrate with as many Fedimints as they desire and select the modules they want.

In summary, guardians form federations, and users can choose to join by downloading software supporting Bitcoin, the Lightning Network, and eCash. The federations a user integrates with will determine the functionalities accessible to them. Some federations will be simple community federations with limited default modules enabling payments. Others will have high-performance infrastructure supporting more challenging, potentially commercial-scale applications. Users can host funds within their community while connecting to commercial-scale federations to use more commercially oriented applications. I expect some federations to form around geographic communities, while others will form as commercial-scale entities supporting large cross-border communities. The system leverages Bitcoin, the Lightning Network, and eCash technologies, offering a satisfying consumer experience through applications and community custody.

Fedimint is an innovative solution addressing fundamental custody challenges. Traditional banking systems have seen little functional innovation in custody operations in recent history. As a basic banking function, custody operations have evolved primarily to enhance security in digital banking. Federation technology opens innovative frontiers in custody operations. Federation-based custody operations have significant growth potential, capable of restructuring organizational nature to better align with stakeholders’ interests. Centralized financial intermediaries now must compete—not only with self-custody systems but also with federation systems.

Fedimint combines federation infrastructure with Chaumian eCash, the Lightning Network, and potentially further integrated applications to support various communities, both established and novel.

eCash

Another implementation of eCash (understood as electronic or digital cash) is the open-source project Cashu—a non-federated version of Chaumian eCash. Cashu resembles Fedimint in that it issues eCash (digital cash), but differs in being a single server rather than a federation of servers. Although requiring more trust without a federation, this system avoids consensus algorithms, reducing transaction latency. Additionally, Cashu uses only LN (Lightning Network), lacking a federated approach, whereas Fedimint uses both on-chain Bitcoin and LN. Thus, Cashu’s use cases and demands as a protocol may differ from Fedimint.

Notably, Calle, Cashu’s creator, proposed a proof-of-liabilities scheme considered potentially widely implementable in eCash systems. Because eCash ownership is intentionally blind, auditing minted eCash supply is inherently challenging. This topic will be discussed in detail later.

Fedimint and Cashu are both very new; this discussion is forward-looking and theoretical regarding the ecosystem’s potential. Particularly, integrating LN (Lightning Network) via LSP (Lightning Service Providers) could lay the foundation for a native Bitcoin banking system. My initial article on this topic covered academic theory and ended with practical discussion. The remainder of this article will expand on that view by discussing what might emerge within this ecosystem.

Cashu is a standalone eCash protocol optimized for simplicity and speed. Cashu’s creator proposed a novel scheme to audit minted eCash supply while preserving privacy.

Monetary Function Trade-offs Require Different Payment Methods

So far, we’ve defined various protocols seemingly implementing monetary forms different from Bitcoin (e.g., eCash and LN). Theoretically, market participants converge on one monetary standard. Ideally, only one monetary form would exist. Yet historically, this never happened—why?

While I’m unsure conceptually whether this balances out, in my work, I define three main reasons for the existence of multiple monetary forms:

1. Information Opacity: Historically, many different forms of commodity money coexisted because adjacent societies weren’t economically integrated and knew nothing about each other’s monetary forms. Awareness matters because it enables individuals to verify a currency’s validity. People simply couldn’t verify foreign currencies and thus struggled to accept them in trade. As societies integrate globally, the internet creates global networks, greatly alleviating verification issues—but not perfectly. Not everyone is internet-connected. Awareness level and ease of verifying a monetary form are necessary for widespread adoption.

2. Sovereign Coercion: Today, users don’t choose money—governments do. If money were chosen in markets rather than imposed politically, the chosen money would differ from today’s enforced fiat currencies. We may be witnessing the early stages of this system’s decline, but any transition requires a sufficiently practical and decentralized alternative eliminating coercion possibilities.

3. Monetary Function Trade-offs: Different monetary forms retain distinct characteristics, making them better suited for certain types of trade over others. Thus, we often see dual currency systems historically, like cattle and salt, or gold and silver. A modern analogy might be real estate and dollars, where real estate stores value while dollars facilitate transactions.

As a technological innovation, Bitcoin greatly alleviates these constraints, but it’s argued not to be a panacea for all problems. Bitcoin’s base layer network (before any scaling mechanisms) excels at storing value but faces two main issues:

1. Transaction Throughput: Bitcoin’s base layer lacks sufficient transaction throughput to support global payments.

2. Privacy: Bitcoin defaults to non-private transactions recorded on a public ledger. Achieving privacy requires significant effort.

The Lightning Network attempts to solve the throughput issue, though it introduces its own problems. The network is gaining adoption and may become—or at least significantly contribute to—the global payment network needed for Bitcoin. Although sending a time-locked, fully collateralized transaction via LN resembles sending a direct Bitcoin transaction, it indeed possesses different characteristics compared to on-chain Bitcoin transactions. LN is faster but requires channel capacity to receive payments.

Its security is weaker because participating requires holding Bitcoin in hot wallets. Moreover, Lightning is newer and more complex than Layer 1 Bitcoin, introducing unpredictable protocol risks. To mitigate trust requirements with channel partners, forced channel closures delay your ability to receive on-chain Bitcoin. For these reasons alone, one could argue Lightning payments have fundamentally different economic properties from on-chain Bitcoin payments. If people accept this view, Lightning could be considered a different monetary medium.

Though theoretically interesting, this may just be a semantic distinction. Practically, market participants seem to treat Lightning as interchangeable with Bitcoin, which may be what matters most.

Similarly, privacy issues can be addressed in multiple ways. eCash is one such way, offering near-perfect privacy at some cost to auditability. One must trust eCash issuers won’t overissue it (discussed in detail later). However, it does offer anonymity and convenience comparable to physical cash, perhaps even greater due to its digital nature. For similar theoretical reasons, this too could be defined as a different monetary medium—though again, we’ll see if it holds practical relevance.

It’s important to distinguish between medium of exchange and method of payment—as summarized by Yang:

“The former (a) refers to the set of assets commonly used in an economy to exchange goods and services (a ‘what’ concept), while the latter (b) is a method facilitating fund transfer from one party to another (a ‘how’ concept). It suggests money should be defined solely as a ‘medium of exchange,’ not a ‘method of payment.’ With this distinction, one can consistently explain why money, demand deposits, and smart cards are money (because they are media of exchange), while checks, drafts, debit cards, and credit cards are not money (because they are merely methods of payment, not media of exchange).”

Lightning Network and eCash can also be understood as different methods of payment, not different monetary media. One could argue eCash is a distinct asset whose value stems from market demand for its unique characteristics. However, its value ultimately settles on the Bitcoin blockchain. Whether eCash is viewed as an independent monetary asset or a payment method will depend on how the system operates at maturity. For example, if it’s fractionally reserved, its asset value depends on trust in the issuing federation; if it’s 100% reserved, its value depends on Bitcoin’s purchasing power. Similarly, even if dollars were partially gold-backed, they wouldn’t be considered gold, whereas 100% gold-backed receipts would be seen as closely interchangeable with owning actual gold (excluding political considerations). Since Lightning shares Bitcoin’s economic model and users and markets seem to treat it similarly, it’s likely describable as a Bitcoin payment method.

Setting aside theoretical and semantic issues, the described system will exist at the intersection of three or four protocols: Bitcoin, Lightning Network, Fedimint, and/or Cashu. Integrating these protocols enables economies with decentralized Bitcoin as a secure base-layer monetary asset, eCash as a private, high-throughput medium of exchange, and LN (Lightning Network) channels with unilateral exit as the technical enabler for this payment method.

Various protocols interacting with Bitcoin are forming new payment methods. Whether these protocols ultimately become independent media of exchange will become apparent as the system matures.

Bitcoin-Native Money Markets

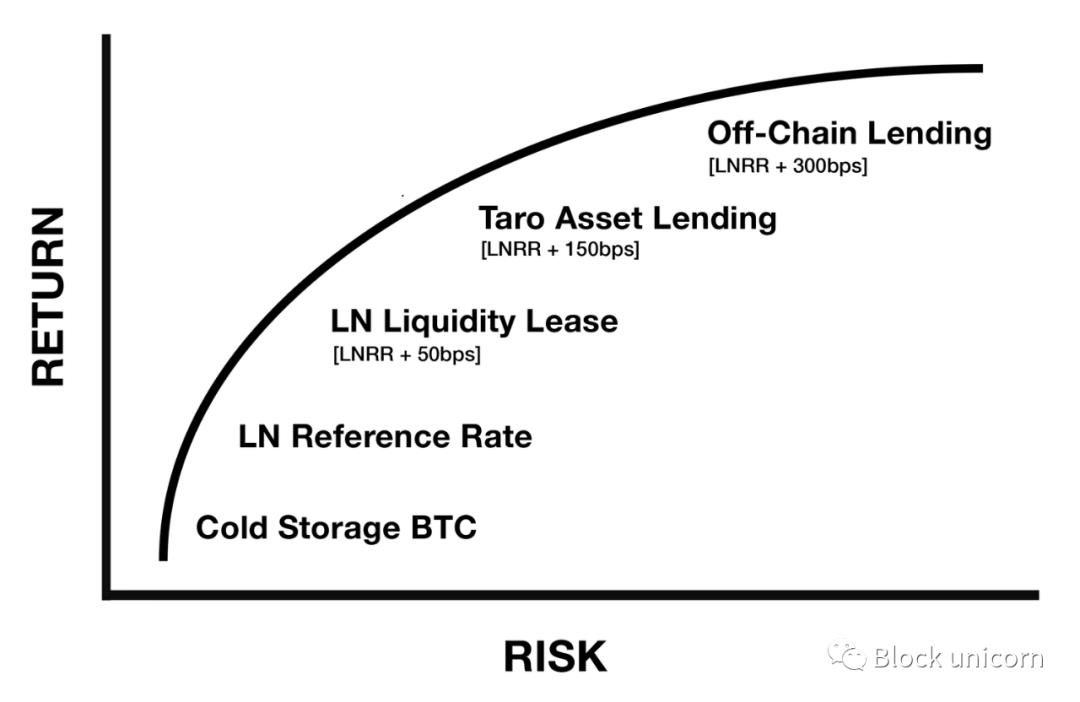

The described monetary system has broad implications for the emergence of digitally native markets. In a previous article, Nik Bhatia argued the Lightning Network represents a Bitcoin-native instance of a risk-free rate. Though similar to benchmark rates in fiat systems, Lightning’s nature is fundamentally different because earning yield on Bitcoin via routing fees and liquidity leasing involves no (economic) counterparty risk. Bhatia further generalized this theory to a risk curve with counterparty risk for lending:

Figure 1 - A novel term structure of interest rates applicable to a Bitcoin financial system

Through this lens, we can view the emergence of LN (Lightning Network) node operators as the rise of decentralized financial service/infrastructure providers native to Bitcoin. This will likely be a mix of self-hosted and custodial services. If custodial providers develop banking functions, it may be a mix of full-reserve and fractional-reserve banks. If LN (Lightning Network) node operators engage in lending, the market will determine the final system.

It’s certain that money markets are forming within Bitcoin, with market participants voluntarily joining for economic benefit. In the U.S. financial system, money markets account for about one-third of total credit market value.

What is a money market? Broadly, it’s a market for short-term cash lending and borrowing. Contrasted with capital markets, which handle long-term lending, equity investments, and derivatives. Both involve contracts, differing mainly in contract nature (though again, this distinction is somewhat subjective—we shouldn’t get bogged down in semantics). Capital markets include broader assets across more contract types with longer time horizons. Since non-Bitcoin assets haven’t emerged within the Bitcoin ecosystem, capital markets haven’t formed at scale. However, money markets are forming via LN (Lightning Network).

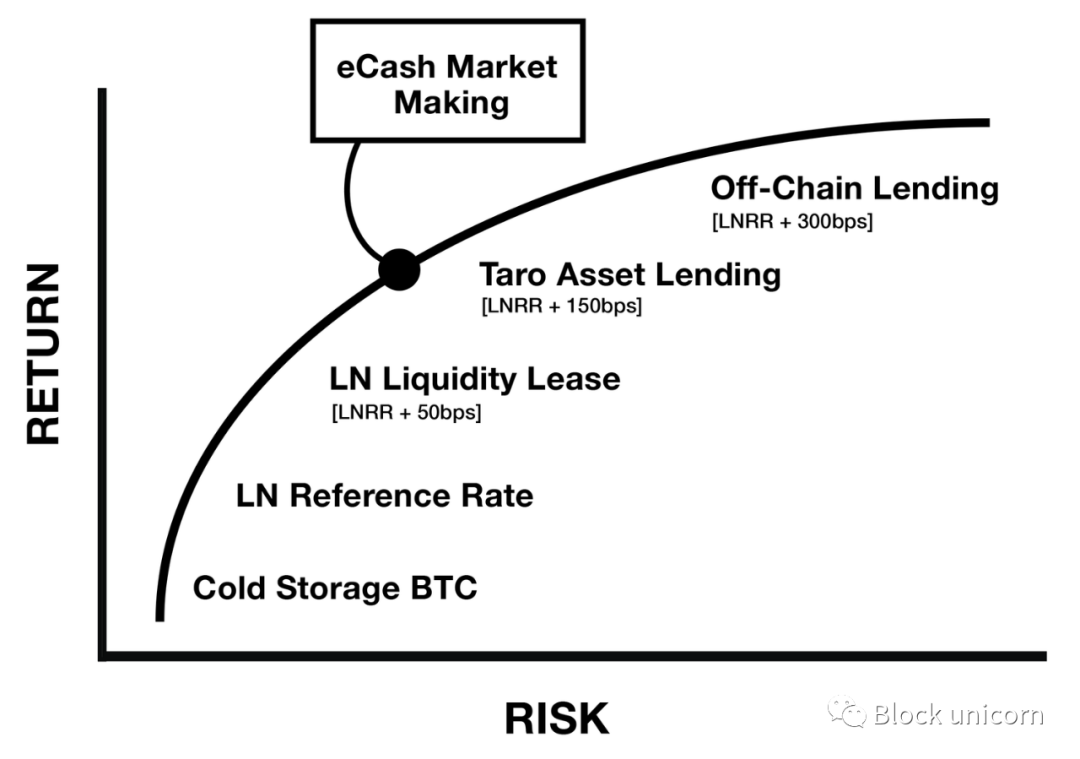

If federated Chaumian eCash mints scale, competitive markets trading eCash interchangeable with underlying Bitcoin will also exist. Markets will determine this interchangeability, with Lightning gateways as primary players. They’ll accept eCash and forward equivalent Lightning payments to transaction recipients. In doing so, they’ll differentiate various eCash issued by mints. In return, they’ll earn spreads on each transaction, forming a money market. Thus, Lightning-to-eCash market makers can earn spreads by pricing risk, assumed to follow a risk curve like this:

Figure 2 - Market transactions between Lightning gateways and federations, conceptualized as a novel source of economic yield akin to a term structure of interest rates

In other words, if federated Chaumian eCash finds market fit, the Bitcoin ecosystem will witness a new money market. Markets will form trading between Bitcoin or Lightning and various eCash forms issued by mints. LSPs (Lightning Service Providers) can act as brokers, earning competitive spreads across eCash and Lightning market transactions.

Ultimately, these markets’ value will stem from adoption of the payment methods they represent. This creates a virtuous growth cycle. Money markets offer interest rates, attracting capital. Investment in these markets increases utility of supported features, which should in turn boost technology adoption.

Bitcoin-native money markets are emerging alongside their supporting protocols. Over time, these markets will attract investment and create a cycle of adoption.

Risks of Federated eCash Systems

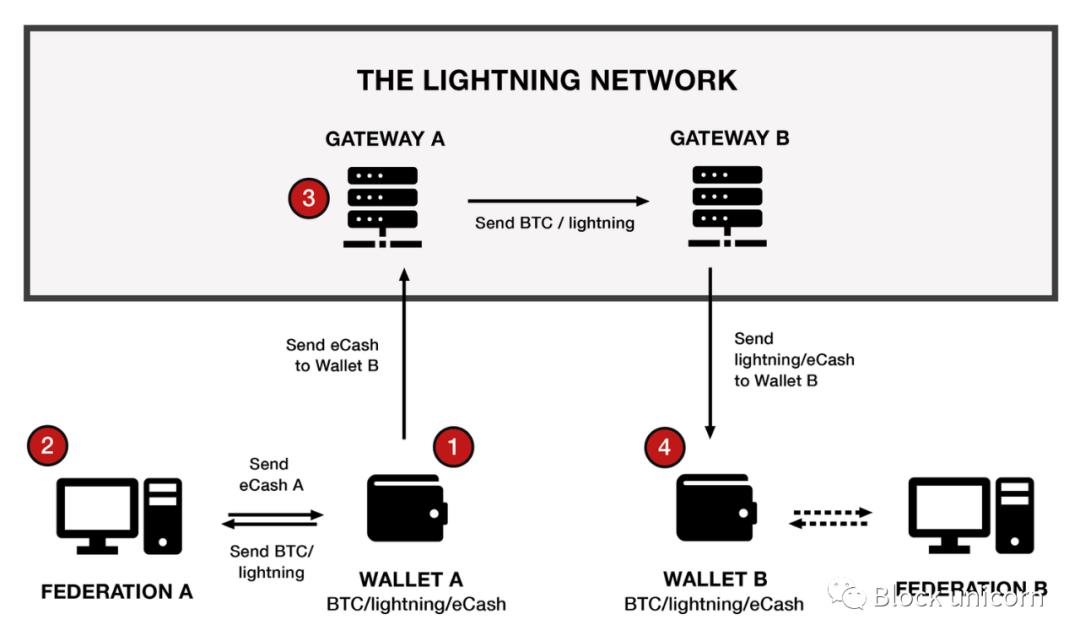

eCash aims to be exchangeable for Lightning or Bitcoin via mints, with Lightning gateways forwarding payments between mints, theoretically making various eCash forms interchangeable. The system can be visualized as follows:

Figure 3 - Simplified visualization of interactions between user wallets, federated Chaumian mints, and LN gateways (Chaumian refers to an anonymous and privacy-preserving protocol and technology first proposed by David Chaum in 1983, designed to protect the privacy of digital transactions.)

1. Wallet A supports Bitcoin, Lightning, and eCash from Federation A, sending Bitcoin to its community’s federation.

2. In exchange, the federation sends eCash to Wallet A without knowing the owner’s identity. Any member of Federation A can easily receive eCash payments from Wallet A. However, if Wallet A wants to send eCash to someone in Federation B, they need to use a Lightning gateway.

3. Lightning gateways act as market makers, ready to send/receive any Bitcoin/Lightning/eCash and earn a spread on each transaction. Thus, when Wallet A sends eCash to it, the gateway accepts it and sends Bitcoin/Lightning to another gateway connected to Federation B where Wallet B resides.

4. Wallet B can then accept this amount in Bitcoin or Lightning, or if desired, convert it to BTC from Federation B.

Users’ trust requirements toward their chosen federation rely more on professional management and enable private transactions. For ordinary individuals, self-custody may be complex, and since Bitcoin maintains settlement finality, losing private keys permanently risks losing funds. Thus, individuals might trade the risk of trusting their community federation against benefits of reduced Bitcoin loss risk and transaction privacy.

However, users don’t just trust their federation won’t lose or steal Bitcoin. Users also trust the federation won’t issue more eCash than received Bitcoin. Since no cryptographic link exists between eCash and received Bitcoin, the federation can unilaterally issue eCash. Privacy benefits mean supply is hard to audit via traditional methods. This creates risk of federation devaluing eCash—what prevents this?

If a community trusts federation managers won’t steal their Bitcoin, they also believe managers won’t devalue it. Malicious managers might simply collude to steal Bitcoin rather than devalue eCash. However, managers could exploit supposedly trustworthy custody schemes to gradually devalue eCash (detailed later). Still, this imposes high costs on community interests, making community custody inherently less trustworthy than third-party custody.

On the other hand, what if a community’s interests align with devaluing its eCash? Theoretically, Federation A could convene its community, announce devaluing its eCash to exchange for goods/services from Federation B, and distribute acquired goods equally among members. The community agrees because they prefer getting something valuable for nothing. However, if such systems scale, countervailing measures will likely emerge to reduce improper incentives. To understand this, we can look to history.

Indeed, improper incentives exist to independently devalue eCash, but natural market incentives can mitigate this risk.

Bitcoin and Free Banking

Free banking systems, discussed in prior works, can serve as a benchmark for assessing competitive dynamics among custody systems. Applying this understanding to federated eCash systems provides a framework for grasping this technology’s potential.

In free banking systems, banks freely issue paper money, and markets decide its value. If a bank issues paper money beyond its reserves, it risks bankruptcy. Applying this risk to a competitive market limits overall paper money issuance. Credit expansion via paper money can only go so far before systemic bank runs become inevitable. However, maintaining solvency within the system aligns not only with banks’ self-interest but also with stakeholders’ interests. Rational customers won’t use banks they suspect are insolvent, as this effectively means they themselves are bankrupt as unsecured creditors of an already bankrupt institution. Yet practically, most customers seem to assume banks are solvent, regardless of accuracy.

In free banking systems, information asymmetry is significant, historically leading to bank failures while customers remained unaware until too late. Thus, parties with more time or natural access to bank-related information act as system watchdogs. Three main groups limit paper money issuance beyond natural levels due to their perceived self-interest:

Competitors: Competition between banks limits how much one bank can expand its paper money issuance relative to others. Through the practice of “note dueling,” more conservative banks use their capital to acquire competitors’ paper money suspected of overissuance, then redeem them en masse, potentially pushing them toward bankruptcy. Competitors can acquire failing institutions cheaply, gaining market share conservatively. This practice was more common early in banking systems, decreasing as systems matured and clearinghouses (discussed later) emerged.

Brokers: Groups able to access more bank-specific information speculate on bank solvency and profit through arbitrage trades. They buy discounted paper money not widely accepted, then redeem it at full gold value from the issuing bank, profiting. They can do this because they spend time acquiring specific information about banks they intend to broker. This practice expands paper money acceptance, imposes limits on risks banks can take, and increases information transparency in the system. These broker roles were more common early in system development. Once systems reach maturity, clearinghouses provide similar functions.

Clearinghouses: As systems mature, clearinghouses emerge to facilitate brokers’ functions and increase information transparency. This constant process of gross note redemption is complex and operationally intensive, so banks need a way to net-settle their obligations, reducing operational burden by settling debts in fewer locations. This leads to clearinghouse establishment, where all banks settle interbank liabilities, netting only account differences. Centralizing debt settlement places clearinghouses at the system’s center, often developing additional functions like: credit monitoring, facilitating reserve ratio, interest rate, exchange rate, and fee agreements, and assisting banks during crises (lending or acquiring intermediaries). Clearinghouse membership is reputation-based; only institutions meeting certain standards can join the “club.” This matters because trust is inherent to the system, and reputation is crucial for maintaining trust.

Given this, let’s return to the previously mentioned issue: Federations might have incentives to devalue their eCash and trade it for valuable goods/services from another federation. Briefly, this is a classic “tragedy of the commons,” where the commons is trust—whether one federation’s eCash is interchangeable with another’s. Independently, this incentive seems fatally threatening to system success, but considering emergent actors and the checks they impose on the system, natural market dynamics may exist to mitigate this risk. Several participants in federated eCash systems like Fedimint can provide these functions:

Federations: Most federations exist solely for custody and payments, but some exist to provide commercial-scale functions. We can imagine cities where not everyone can have their own roads. Custody will eventually evolve into community streets, city roads, and highways. Fedimint (and LN gateways) provide architecture and functionality to scale custody into a network of streets and highways. Individual federations will compete to build trust within the broader ecosystem. For streets, this will be community-level trust; for highways, it will be system-level trust, where large federations’ reputations are crucial to their success.

Lightning Gateways: For a Lightning gateway to integrate and forward federation payments, it must hold that federation’s eCash balance—accepting eCash and forwarding Bitcoin via Lightning to another federation. This won’t be indiscriminate. The gateway will only act as a market maker for various federations if it believes and can potentially verify the federation’s solvency. If a gateway notices eCash balances increasing while on-chain data shows Bitcoin balances remaining relatively stable, it may grow concerned. Terminating their service could be fatal to a federation’s transactional utility. Thus, gateways will only cooperate with federations they’re comfortable holding eCash from, acting in self-interest to monitor interchangeability of eCash issued by various federations.

eCash Brokers: A class of brokers will likely emerge, functioning like Lightning gateways but instead of forwarding Lightning payments, they’ll only exchange eCash from Federation A with eCash from Federation B. By acting as direct market makers, they’ll replace the Lightning Network with a centralized, account-based ledger for transaction throughput. Brokers will continuously monitor and determine which eCash they want to hold balances in and which they want to avoid or buy at a discount. This market-making activity will provide another check on eCash interchangeability and prevent federations from arbitrarily devaluing their eCash.

Proof of Reserves: Companies building technology to monitor institutions’ reserves can also play a key role, effectively acting as credit regulators for federations. Their emergence can provide some form of verification, though not perfect. They can certainly monitor on-chain multi-signature addresses (assets), but liabilities will be more challenging. A federation doesn’t know who owns its issued eCash, but it knows how much it has issued. A federation can grant third-party credit regulators access to detailed records of its issuance and redemption history, sufficient to assume full reserves or strong solvency (as described below). Thus, credit regulation and large federations’ reputations are crucial for ecosystem integration. However, this doesn’t eliminate risks of a federation issuing off-book liabilities, requiring third-party audits. For this reason, proof-of-reserves companies will likely collaborate with or offer services to auditing firms to increase assurance against this risk. Web-of-Stakes (33) is an emerging concept in the Civ Kit protocol that could mitigate this risk in specific applications.

Solvency Speculators: A class of risk-taking entities similar to hedge funds may emerge, speculating on the solvency of various eCash notes. This would exist only in commercial organizations where funds can execute redemption attacks and hope to profit. This resembles note dueling between competitors, where the fund doesn’t benefit from gaining competitors’ market share but profits from short positions against the federation’s value. This category might appear last, as its existence depends on a mature liquid capital market forming within the system.

Crucially, the system’s digital nature will enable participants to profit quickly and cheaply from currency devaluation. By eliminating devaluation as a viable long-term business model—and possibly even unprofitable short-term—it incentivizes participants to act prudently. No financial system in history has ever had such incentive structures.

If such a system scales, we’ll likely see integration of these functions among various service providers. I expect LSPs to not only act as Lightning gateways but also adopt eCash brokerage services, possibly acquiring or leveraging credential companies and protocols. Just as brokerage and credit monitoring functions consolidated into clearinghouses in traditional free banking systems, I also expect integration of these functions in community eCash systems. However, all this assumes such a system can actually scale—which undoubtedly will take a long time or may never happen. Fortunately, technical solutions have the potential to emerge soon and mitigate eCash devaluation risks.

Free market incentives align agent and consumer interests where trust already exists. This alignment of interests increases as the system matures, because the system’s value attracts market participant engagement.

Liability Proof Schemes for Federated eCash Mints

Federated custody systems reduce risks of custodians misappropriating user funds. They also reduce risks of mints lowering eCash supply. Free market systems further reduce motivations to devalue eCash, but for free markets to operate most efficiently, information transparency is essential. Improving information transparency about outstanding eCash from mints is crucial for efficient markets. Higher mint information transparency strengthens auditability. But this involves a trade-off—higher auditability might reduce eCash privacy, which is eCash’s purpose.

Calle, developer of the Cashu protocol, proposed a liability proof (“PoL”) scheme for eCash mints aimed at increasing transparency of eCash issuance without significantly reducing eCash’s privacy advantages. This can be achieved by enabling system-level auditability while allowing participants to maintain privacy at the individual level. The system requires mints to take three main voluntary actions:

1. Publicly commit to regularly rotating their eCash private keys at predetermined intervals (“epochs”). This allows all circulating eCash to roll from old epochs to the current one.

2. Generate a publicly auditable list of all issued eCash tokens in the form of a mint proof.

3. Generate a publicly auditable list of all redeemed eCash tokens in the form of a burn proof.

Maintaining this system enables eCash mint users to verifiably detect whether the mint issued unsupported eCash in a past epoch. This effectively sets an expiration date for users’ eCash, forcing users to refresh their eCash to the latest epoch. eCash expiration forces users (via automation in wallet software) to participate in behaviors that ultimately compel the mint to report past eCash issuance and redemption. This is somewhat analogous to simulating periodic “run risks” at eCash mints. In Calle’s words:

Join TechFlow official community to stay tuned Telegram:https://t.me/TechFlowDaily X (Twitter):https://x.com/TechFlowPost X (Twitter) EN:https://x.com/BlockFlow_News