RWA White Paper: The Value, Exploration, and Practice of Fund Tokenization

TechFlow Selected TechFlow Selected

RWA White Paper: The Value, Exploration, and Practice of Fund Tokenization

This article will analyze, through observed cases in the current market, the value of tokenized funds and the active exploration and practices by market participants.

Author: Will Wang

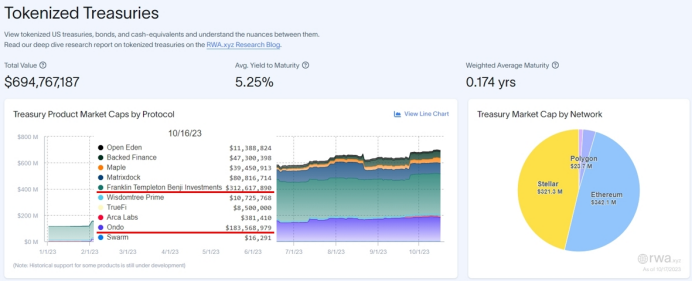

When discussing RWA, we often focus on underlying assets such as U.S. Treasuries, fixed-income instruments, and securities. In fact, currently the largest RWA project by asset scale—aside from stablecoins—is money market funds. The top three projects by asset size are: Franklin Templeton at $312 million (government bonds), Centrifuge at $247 million (asset-backed), and Ondo Finance at $183 million (government bonds).

Franklin Templeton is a fully tokenized fund; Ondo Finance also operates two tokenized funds, and Centrifuge has established tokenized funds within its RWA collaboration with Aave. This highlights the critical role of tokenized funds in bridging TradFi and DeFi. We believe that funds, as an asset class, are the optimal carrier for RWA due to (1) their regulatory oversight and (2) their relatively standardized digital representation.

Currently, discussions around RWA largely reflect crypto’s (or DeFi’s) one-way demand to capture real-world value. However, from the perspective of traditional finance (TradFi), tokenizing funds via blockchain and distributed ledger technology can unlock far greater value.

Therefore, this article analyzes, through observed market cases, the value unlocked by fund tokenization and the active exploration and implementation by market participants.

1. Fund Tokenization

Tokenization typically refers to the representation of digitized assets on a blockchain, leveraging the advantages of distributed ledger technology for accounting and settlement. Assets suitable for tokenization include not only financial instruments like stocks, bonds, and funds, but also tangible assets such as real estate, and intangible assets like music streaming copyrights. The tokens generated through tokenization serve as carriers of asset value and proof of ownership rights.

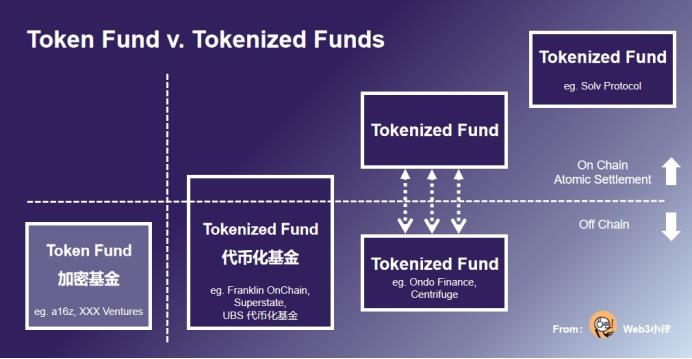

This innovation and disruption also apply to funds. When funds are tokenized, they become tokenized funds—meaning fund shares are recorded in digital token form on a blockchain-based distributed ledger, with tokens tradable in secondary markets. These tokenized funds differ from crypto-focused funds (Token Funds) that merely invest in primary or secondary crypto markets.

The global asset management industry is facing numerous challenges. While overall assets under management (AUM) have grown with market appreciation, fund management fees have been compressed due to competition and the industry's shift toward passive investment strategies. Beyond investment pressures, there is increasing demand for enhanced digital capabilities—from online distribution and asset reporting to regulatory compliance and personalization. Management costs are rising faster than revenues, squeezing profit margins.

For private funds, limited liquidity and high investment thresholds have long restricted investors to a small group of institutional players. The private fund market urgently needs to lower entry barriers and introduce product designs tailored to non-institutional clients such as small-to-mid institutions, family offices, and high-net-worth individuals.

Fund tokenization can address many of these global asset management challenges. Advocates believe that future blockchain- and DLT-based funds will not only increase AUM and expand into broader asset classes (including diverse RWA tokenized assets), but also attract new investor segments (e.g., unbanked investors from Africa, Asia, and Latin America accessing investments via crypto). It can enhance user experience (via KYC embedded in smart contracts), help funds win in the race for digital transformation, and significantly reduce operational and marketing costs by leveraging blockchain and DLT efficiencies.

2. Tokenization Will Profoundly Impact the Fund Market

2.1 Tokenization Accelerates Fund Market Digitization

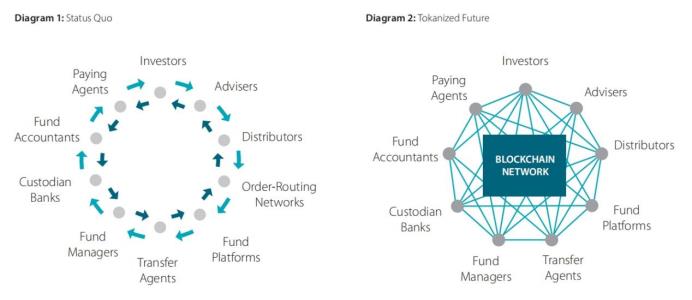

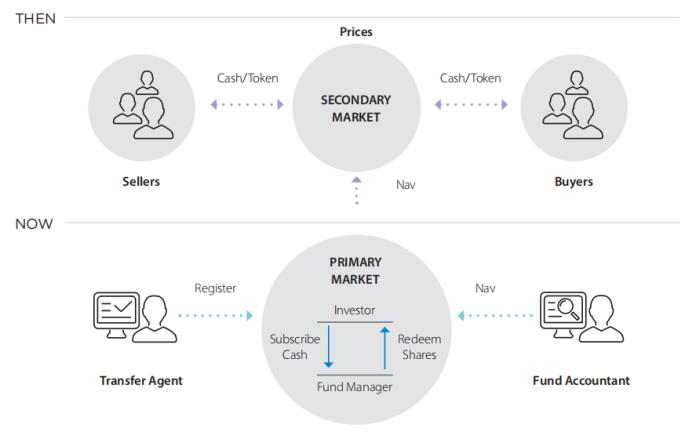

Currently, funds and investors are separated by layers of intermediaries. On the distribution side (Fund Distributors), these include financial advisors, fund platforms, and order-routing networks. On the service side, they include paying agents, custodian banks, and fund accountants.

Transfer agents coordinate between both ends, handling KYC, AML, CFT, economic sanctions screening, subscription and redemption settlements, reporting to managers, and maintaining investor registries.

The traditional fund operating process is inherently inefficient:

(1) Fund shares are created to fulfill subscriptions and canceled for redemptions;

(2) Fund pricing is not based on bid-ask spreads, but on net asset value (NAV) set by fund accountants;

(3) Transfer agents price orders based on NAV, aggregate them, settle via book entries in a centralized register, then reconcile with investor and fund cash positions;

(4) For three days prior to share and cash settlement, both funds and investors face market volatility and counterparty risk;

(5) Fund liquidity forces managers to retain cash buffers to cover rebalancing costs.

In contrast, tokenization can drastically simplify these complex processes:

(1) When tokenized funds are issued and traded on-chain, subscriptions and redemptions are settled directly via fund tokens and payment tokens into investor wallets, achieving finality and eliminating market and counterparty risks;

(2) All ownership changes are automatically recorded on the blockchain’s distributed ledger, eliminating the need for centralized registration;

(3) Since all intermediaries can access and view data on-chain, multi-party reporting and reconciliation become unnecessary.

Additionally, tokenization enables digitized interaction between fund managers and investors:

(1) Integrated KYC, AML, CFT, and sanctions checks accelerate investor onboarding;

(2) Atomic settlement on blockchain enables 24/7 real-time pricing and settlement;

(3) Shared access to a unified ledger allows real-time data sharing—investors can directly access fund data and trade;

(4) Fund managers gain richer investor and transaction data.

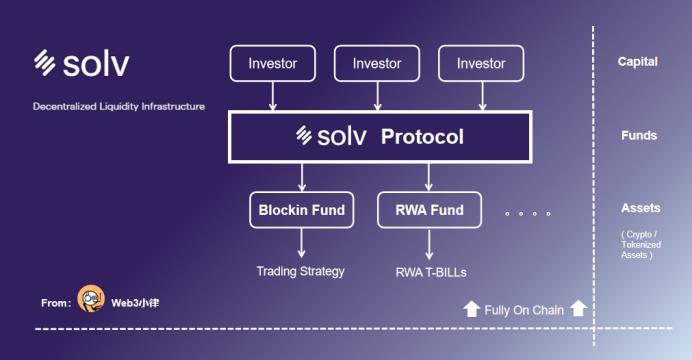

2.2 Solv Protocol’s On-Chain Fund Issuance and Fundraising Platform

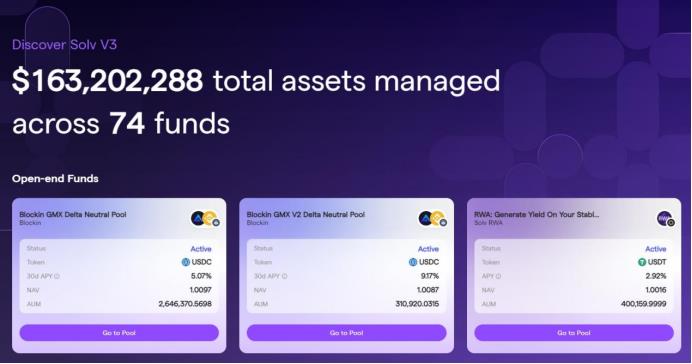

Founded in 2020, Solv Protocol aims to provide blockchain-based financial tools and diversified asset management infrastructure for the crypto industry. Recently, it secured $6 million in funding. Its latest product, Solv V3, sets a new standard for on-chain fund issuance. Through Solv Protocol, tokenized funds can achieve efficient capital flows via on-chain fundraising, issuance, subscription, redemption, trading, and settlement.

According to its official website, Solv Protocol has already launched and raised capital for 74 tokenized funds (including open-end and closed-end funds), serving over 25,000 investors and managing more than $160 million in assets.

Solv Protocol’s core mechanism allows fund managers to create on-chain funds, depositing raised funds (stablecoins, BTC, ETH, etc.) into Solv’s smart contract, and issuing NFT/SFT tokens representing fund shares to investors. This enables fund managers to deploy capital according to their investment strategy.

For example, Blockin GMX Delta Neutral Pool is an open-end fund managing approximately $2.6 million, following Blockin’s investment strategy. Another open-end fund, RWA: Generate Yield On Your Stable Coins, initiated by Solv RWA, raises USDT and invests in U.S. Treasury RWAs to generate yield for stablecoin holders.

Open-end funds have no fixed total number of shares—they can issue new shares or allow periodic redemptions at any time. Fund managers using highly liquid portfolios typically adopt an open corporate structure.

Fully on-chain tokenized funds issued via Solv Protocol raise capital in BTC/ETH/stablecoins and invest in native crypto or tokenized assets (such as U.S. Treasury RWAs). This fully on-chain tokenized fund architecture maximizes the value derived from tokenization. For instance, Solv Protocol’s tokenized funds:

(1) Enable direct manager-investor engagement, providing richer investor and transaction data;

(2) Eliminate friction from multiple intermediaries, reducing costs;

(3) Conduct fundraising, issuance, trading, and settlement entirely on-chain, recorded transparently on a distributed ledger;

(4) Offer real-time NAV updates and 24/7 subscription/redemption, among other benefits.

Solv Protocol notes that most current crypto asset management services come from CeFi institutions, whose opaque asset creation and fund management processes create trust issues. More decentralized solutions offer transparent and secure investment experiences, helping asset managers build trust and liquidity. Solv is building infrastructure and ecosystems offering full-service support including creation, issuance, marketing, and risk management—lowering Web3 entry barriers while advancing crypto market maturity.

Olivier Deng, Nomura Securities investor in Solv Protocol, stated: “Solv has built a trustless institutional-grade DeFi platform integrating brokers, underwriters, market makers, and custodians, creating the first liquidity financial infrastructure bridging DeFi, CeFi, and TradFi on blockchain.”

3. Settlement of Tokenized Funds

Tokenized funds can partially replace intermediaries (e.g., fund distributors) and elevate the digitization level of the fund market, but transformation won’t happen overnight. For fund managers and investors, the most immediate impact of tokenization will be on subscription and redemption settlement methods.

3.1 Settlement of Tokenized Funds

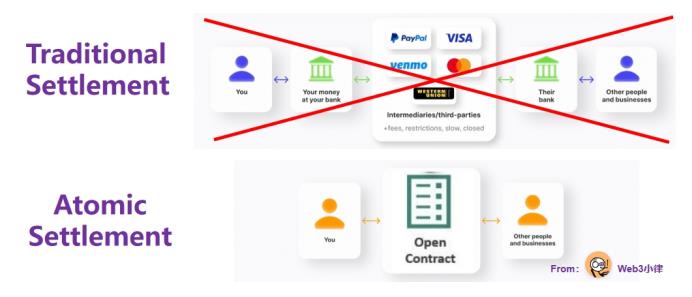

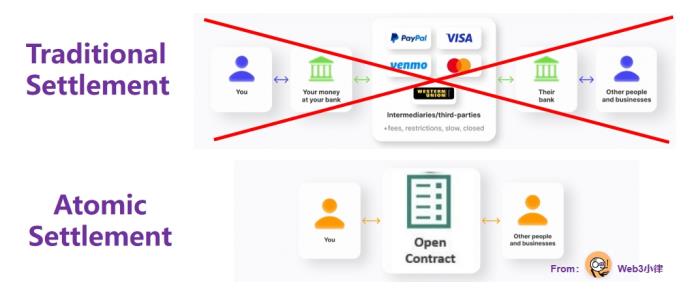

Traditional funds are priced based on NAV, with managers collecting or disbursing cash via banking systems to settle share issuance or cancellation after three days (T+3). In contrast, tokenized funds may reprice multiple times per day, and since subscriptions and redemptions are “automatically” settled on-chain, T+3 bank-based settlement becomes obsolete. As seen in Solv Protocol’s case, fully blockchain-based tokenized funds enable 24/7 real-time pricing and settlement.

This blockchain and DLT-enabled settlement method is known as atomic settlement, meaning the exchange of cash equivalents and fund shares is directly linked—when one asset transfers, the other does simultaneously. In other words, settlement requires both buyer and seller wallets to hold available cash and shares for exchange, with finality contingent on simultaneous transfer. If either cash or shares fail to deliver, the transaction fails. This eliminates counterparty risk and enables real-time settlement, greatly enhancing transaction efficiency.

Bitcoin was designed from the outset as a decentralized peer-to-peer electronic cash system. Bitcoin payments allow direct transfers between users without third parties like banks, clearinghouses, or payment platforms, avoiding high fees and cumbersome processes. Applied to cross-border payments, atomic settlement solves issues of high cost, inefficiency, and slow transfer speeds.

Another interesting use case is more efficient settlement of exchange-traded funds (ETFs). Since ETFs use in-kind subscriptions and redemptions, tokenizing the underlying securities (the basket of assets in an ETF) could dramatically streamline settlement and enable real-time clearing.

3.2 Use Cases for Tokenized Fund Settlement

This atomic settlement method has already been approved by the U.S. SEC and implemented in the Franklin OnChain U.S. Government Money Fund, which manages $310 million in assets. Similarly, Singapore’s Monetary Authority has pilot programs like UBS’s tokenized fund. While these are not fully on-chain tokenized funds, they leverage blockchain and DLT for accounting and settlement advantages, forming a hybrid tokenized fund model.

3.2.1 Franklin OnChain U.S. Government Money Fund

Franklin Templeton launched the Franklin OnChain U.S. Government Money Fund (FOBXX) in 2021—the first U.S. fund approved by the SEC to use Stellar blockchain for transaction processing and ownership recording. In April this year, it expanded to Polygon and may soon launch on Avalanche, Aptos, and Ethereum L2 solution Arbitrum.

To date, it manages over $310 million in assets, offering investors a 5.19% annualized yield. Each fund share is represented by one BENJI token, though BENJI currently shows no integration with DeFi protocols on-chain. Investors must complete compliance verification via Franklin Templeton’s app or website to join a whitelist, meeting KYC/AML/CFT requirements.

Franklin Templeton’s Head of Digital Assets stated: “We believe blockchain technology has the potential to reshape asset management, offering greater transparency and lower operating costs for traditional financial products. Blockchains like Stellar are vital for the future of asset management, and tokenized assets built on them will eventually achieve interoperability with the broader crypto ecosystem.” Reportedly, Franklin’s tokenized fund incurs only 1/10 the cost of a traditional fund.

3.2.2 Superstate Fund by Compound’s Founder

Fund managers with strong DeFi backgrounds will fully leverage blockchain and DLT advantages. For example, Robert Leshner, founder of Compound, announced on June 28, 2023, the launch of Superstate—a company dedicated to bringing regulated TradFi financial products on-chain.

According to filings with the U.S. SEC, Superstate will use Ethereum as an auxiliary tool for accounting and settlement, launching funds investing in short-term government bonds such as U.S. Treasuries and agency securities. In short, Superstate will establish off-chain SEC-compliant funds to invest in short-term U.S. Treasuries, using Ethereum blockchain for fund accounting, settlement, and ownership tracking. Superstate will operate a whitelisted investor model, so fund tokens cannot be used in DeFi platforms like Uniswap or Compound.

In a statement to Blockworks, Superstate said: “We’re creating an SEC-registered investment product that gives investors a verifiable record of ownership—just like holding a stablecoin or other crypto asset.”

While Superstate hasn’t discussed DeFi composability, a plausible path is that Superstate fund tokens could be staked in Compound’s lending pools to borrow stablecoins and build DeFi legos.

3.2.3 UBS’s Tokenized Fund Pilot

On October 2, 2023, UBS Asset Management announced the launch of a tokenized fund pilot. Through UBS Tokenize, fund tokens exist on Ethereum as smart contracts, representing equity in an underlying money market fund. Tokenization aims to enhance fund issuance, distribution, subscription, and redemption processes.

This pilot is part of Singapore’s Monetary Authority’s broader Variable Capital Company (VCC) umbrella initiative—“Project Guardian”—focused on tokenizing real-world assets. For UBS, this aligns with its global DLT strategy, leveraging public and private blockchains to improve fund issuance and distribution. In November 2022, UBS launched the world’s first publicly traded tokenized bond. In December 2022, it issued a $50 million tokenized fixed-rate note, followed by a $200 million CAD tokenized structured note for third-party issuers in June 2023.

The project lead stated: “This is a key milestone in understanding fund tokenization, building on UBS’s expertise in bond and structured product tokenization. Through this exploratory initiative, we’ll collaborate with traditional financial institutions and fintech providers to explore ways to improve market liquidity and investor access.”

3.3 Technical Barriers to Tokenized Fund Settlement

Tokenization represents a major shift in fund settlement, replacing the current reliance on transfer agents who record subscriptions and redemptions in shareholder registers. This cash-like atomic settlement involves no intermediaries—if either cash or tokens fail to deliver, the transaction fails. In other words, tokenized transactions only exist in a settlement-ready form; they cannot be pre-agreed, recorded, and later canceled. The key advantage is eliminating counterparty risk where buyers fail to deliver cash or sellers fail to deliver shares.

However, atomic settlement introduces a technical challenge: in most cases, blockchain wallets must be pre-funded before settlement, otherwise the transaction fails. Unlike traditional failed deliveries, there’s no grace period to buy or borrow missing assets. Transactions don’t go into pending status—they simply fail. This imposes additional costs on issuers and investors, requiring them to maintain excess wallet balances. Both parties must pre-fund their wallets with tokens or cash equivalents. Pre-funding carries cost, raising the risk that wallet maintenance costs exceed savings from streamlined transactions.

Yet, other cost-reduction measures exist: shared data ledgers on blockchain instead of multilateral reporting and reconciliation; elimination of transfer agent registry functions; replacement of centralized ledgers with self-maintained distributed ledgers; and use of smart contracts to ensure timely distribution of entitlements to token holders.

4. Issuance of Tokenized Funds

Despite the many benefits of real-time settlement, tokenized fund issuance applies only to new funds. Tokenizing existing funds would result in dual records—one on a blockchain ledger and another in traditional registers maintained by transfer agents—leading to duplicate registration costs. It would also create conflicts between legacy shareholders and tokenized share holders.

As of mid-2021, there were 127,913 global funds managing $68.6 trillion in assets. Rather than migrating all of them to blockchain, it may be more practical to add tokenized asset classes to existing funds (e.g., Hong Kong SFC’s upgraded virtual asset license allowing 100% allocation to crypto), or offer tokenized versions of existing assets (e.g., tokenized stocks, bonds, and funds).

4.1 Tokenization of Money Market Funds—Franklin OnChain, Ondo Finance, Centrifuge

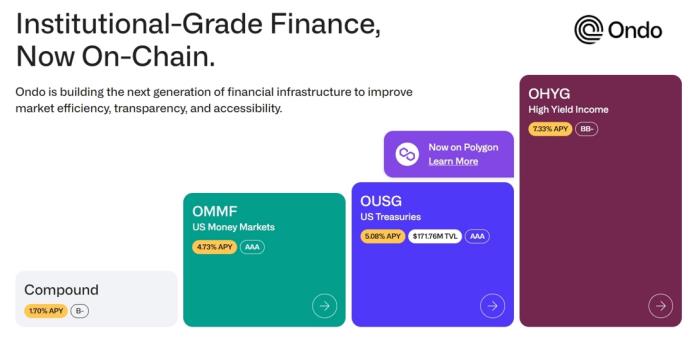

Aside from stablecoins, the largest RWA projects by asset size today are money market funds. Leading the list is Franklin Templeton at $312 million (government bonds), followed by Centrifuge at $247 million (asset-backed), and Ondo Finance at $183 million (government bonds).

Franklin Templeton is a fully tokenized fund; Ondo Finance operates two tokenized funds; Centrifuge has established tokenized funds within its RWA collaboration with Aave. This underscores the importance of tokenized funds in connecting TradFi and DeFi.

4.1.1 Ondo Finance OUSG / OMMF

Launched in January 2023, Ondo Finance aims to provide institutional-grade investment opportunities and services to professional on-chain investors. It brings low-risk/risk-free interest-bearing fund products on-chain, enabling stablecoin holders to invest in government and U.S. Treasury bonds. Ondo’s two tokenized funds, OUSG and OMMF, are backed by BlackRock’s short-term U.S. Treasury ETF and money market fund, respectively.

Investors must first pass Ondo Finance’s official KYC and AML verification before signing subscription documents. Eligible investors deposit stablecoins into Ondo’s tokenized funds, which are then converted to fiat via Coinbase Custody and used by compliant broker Clear Street to execute trades in U.S. Treasury ETFs.

For regulatory compliance, Ondo Finance enforces a strict whitelist, opening investment only to Qualified Purchasers. Investors must complete KYC/AML verification before signing up and depositing stablecoins.

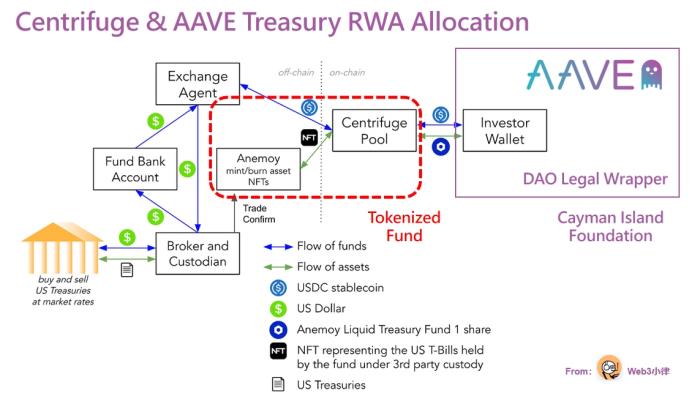

4.1.2 Centrifuge & Aave Treasury RWA Allocation

Centrifuge, a leader in RWA collateralized lending, recently helped Aave’s treasury capture yield from U.S. Treasuries through an RWA tokenization proposal. This solution also employs a tokenized fund structure.

In this design, Anemoy Liquid Treasury Fund—an off-chain BVI-registered fund—is first tokenized via the Centrifuge protocol. Then, Aave allocates treasury funds to the corresponding Centrifuge Pool, receiving fund token receipts. The pool routes Aave’s capital to Anemoy, which uses custody, on/off-ramps, and brokerage services to purchase U.S. Treasuries, thereby bringing Treasury yields on-chain.

4.2 Tokenization of Private Funds—Hamilton Lane, KKR

Historically, private funds have had high entry barriers for retail investors, limiting access to large institutions and ultra-high-net-worth individuals. Yet, a clear goal in asset management is expanding retail investor access. Persistent under-allocation stems from high minimums, long holding periods, limited liquidity (lack of developed secondary markets), poor price discovery, manual investment workflows, and insufficient investor education.

Although the tokenization market is still early, some private fund managers are testing the waters by launching tokenized versions of flagship funds. Notable examples include Hamilton Lane, KKR, and Apollo.

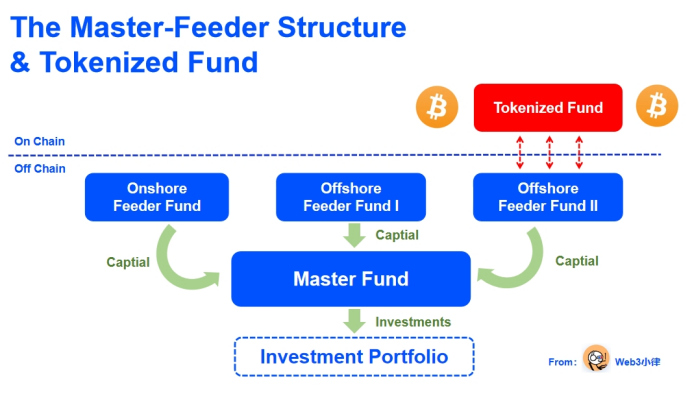

Due to constraints with existing funds, tokenizing only part of the shares would result in dual records—on blockchain and traditional registers—creating redundant registration costs. One solution is having transfer agents consolidate records. Another is using feeder funds to achieve tokenization.

Private funds can use a master-feeder structure, tokenizing the feeder fund to represent partial ownership of the entire private fund. Under this model, managers raise capital from various investors into a feeder fund, which then invests into a master fund. Investors pay fees at the feeder level, while trading and investing occur at the master level.

The master-feeder structure is preferred by large financial institutions launching funds across jurisdictions, accommodating different regulatory requirements and commercial terms such as fees, subscription rules, and investment strategies.

4.2.1 Hamilton Lane

Hamilton Lane, a globally leading private markets firm managing $823.9 billion in assets, has tokenized portions of its fund shares on the Polygon network, making them available to investors via the Securitize platform. In partnership with Securitize, the fund uses a feeder fund structure, with Securitize Capital managing the tokenized portion (registered under SEC Reg D 506(c)).

Securitize’s CEO stated: “Hamilton Lane offers some of the best-performing private market products, historically limited to institutional investors. Tokenization now allows individual investors to digitally participate in private equity for the first time and co-create value.”

From a retail investor’s perspective, while tokenized funds offer an “affordable” way to access top-tier private equity—lowering the average $5 million minimum to just $20,000—investors still must pass accredited investor verification via Securitize, retaining some access barriers.

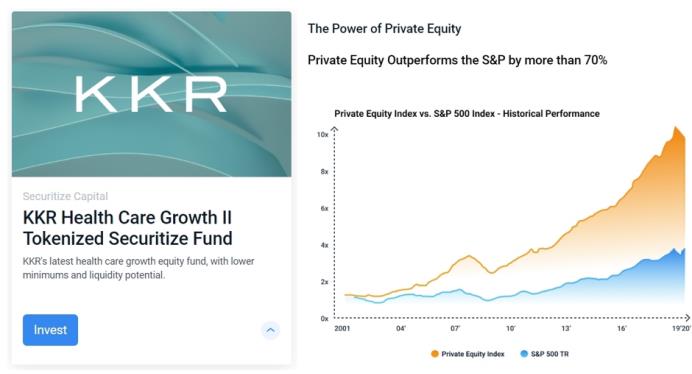

4.2.2 KKR

Similarly, KKR, managing nearly $500 million in assets, partnered with Securitize in October 2022 to tokenize shares of its closed-end fund Health Care Strategic Growth Fund II on the Avalanche network via a feeder fund structure.

From a private fund’s standpoint, the advantages of tokenization are clear: it provides real-time liquidity for fund shares (compared to traditional 7–10 year lockups) and enables LP diversification and flexible capital sourcing. This could help resolve current market difficulties—projects funded during loose liquidity and high valuations struggling to exit amid tightening liquidity and reduced risk appetite.

For investors, tokenized private funds offer low-barrier access to top-tier funds (private equity returns outperform S&P 500 by ~70%). While institutional and ultra-wealthy investors typically need millions to join KKR funds, individual investors can now enter via this tokenized feeder fund with a minimum of $100,000.

5. Trading and Investing in Tokenized Funds

5.1 Secondary Market Trading of Tokenized Funds

The most exciting prospect of tokenization may not be blockchain-based settlement and issuance, but secondary market trading of fund tokens.

As the tokenized market matures, active secondary trading of fund tokens can more accurately reflect true fund value, improving price discovery and informing valuation beyond the static NAV-based model used by ETFs. This enables investors to monitor trades, portfolio valuations, and performance in real time, adjusting risk exposure dynamically. Fund tokens will trade based on investor demand, currency trends, and arbitrage opportunities, with arbitrageurs eliminating price discrepancies between tokenized and non-tokenized fund versions.

Moreover, liquid fund tokens in secondary markets can supplement redemption liquidity. Funds can reduce low-yield cash reserves held against redemptions. Once investors can sell tokens instead of redeeming shares, fund AUM stabilizes and rebalancing costs drop. If underlying assets are also tokenized, managers won’t need to sell assets or borrow from banks to cover liquidity mismatches between subscriptions and redemptions—instead, underlying assets can be sold directly in secondary markets in tokenized form.

Tokenization itself cannot add liquidity to inherently illiquid asset classes—such as private equity and credit, infrastructure, real estate, art, and timberland—but it can leverage direct investor community engagement and DeFi integrations to reduce the steep discounts typically associated with illiquidity. Additionally, tokenization’s fractionalization feature allows splitting assets into smaller denominations, lowering investment thresholds and enabling participation from previously excluded investors, thereby generating additional liquidity. These benefits have already been demonstrated in crypto and DeFi markets.

The shrinking number of publicly listed companies—and the concurrent rise of private equity—has cut off retail investors from a range of investment opportunities. Tokenization can reopen access to asset classes currently reserved for institutions.

Unfortunately, most current tokenized funds remain closed to permissionless public chain trading due to KYC/AML/CFT compliance. For example, the largest tokenized fund by AUM—Franklin OnChain U.S. Government Money Fund—uses Stellar blockchain for transaction processing and ownership records but currently shows no on-chain trading activity. Similarly, tokenized private funds like those from Hamilton Lane and KKR only allow subscription and redemption through platform gateways (with strict KYC), with further trading likely occurring over-the-counter (OTC). In the future, secondary trading may occur via permissioned blockchains.

5.2 Tokenization Accelerates Personalized Investing

High investment thresholds in traditional finance reflect high capital costs. By reducing issuance, subscription, redemption, registration, and servicing costs, tokenization dramatically lowers entry barriers. Tokenization could also enable micro-investor funds targeting commercial/residential real estate, infrastructure, private equity/debt, art, and collectibles—currently inaccessible to mainstream investors.

Long-term, the impact of tokenization may extend far beyond lower transaction costs, better price discovery, increased liquidity, and broader investor bases. Tokenization could enable investment portfolios fully aligned with individual investor needs, preferences, and values.

Currently, funds are generic products promising returns, capital growth, or ESG alignment. Millennials, raised in the digital economy, have never known a world without smartphones—they demand direct, simple, transparent financial products. To them, mutual funds are complex, hard to understand, slow to purchase, and difficult to personalize.

Tokenization removes these barriers. Buying and selling fund tokens is cheaper, easier, and faster than traditional fund shares. Smart contracts embedded in fund tokens can automate due diligence, allowing young investors to open accounts (wallets) in minutes rather than days—similar to how they manage crypto wallets.

Most importantly, tokens enable personalized fund portfolios. Any asset can be tokenized and fractionalized, vastly expanding the investable universe—even enabling micro-investments—and allowing customization based on individual preferences. Over time, tokenized funds could offer each investor a tailor-made portfolio, managed as easily as a personal bank account. Above all, personalized tokenized investing holds intuitive appeal for a generation of young investors.

According to Newzoo, there are 2.9 billion gamers worldwide. The overlap between gamers and crypto enthusiasts means use cases already exist for buying and selling in-game items on blockchain. NFTs were, in effect, invented by gamers. Technologically, tokenized funds are already part of the lived reality for millennials and Gen Z.

6. Regulation of Tokenized Funds

Traditional funds are generally subject to strict regulation within their local jurisdictions, with clear operational guidelines and pathways. However, once tokenized, who regulates them? This remains an open question. Participants in tokenized funds must adapt to the reality that post-tokenization, funds may circulate globally via public blockchains (though currently limited to permissioned circulation), potentially facing scrutiny from regulators across all major fund markets and global crypto regulatory frameworks.

Although regulators worldwide have responded to the blockchain token financing boom since 2017, and international bodies seek global consensus on crypto regulation, laws governing tokenization remain jurisdiction-specific, unclear, and inconsistent. Regulatory scope ranges from legislative definitions of roles, rights, and obligations for issuers, investors, and intermediaries (e.g., Liechtenstein), to guidance on which crypto assets and activities require licensing (e.g., UK). In the absence of clear legal definitions for crypto assets and smart contracts—and supporting case law—tokenization faces ongoing legal and regulatory uncertainty.

Regulatory uncertainty makes asset managers hesitant. As regulated entities, they prefer not to act first and seek approval later. However, at least in the UK, guidance from the Financial Conduct Authority (FCA) has enabled the tokenization industry to develop on a foundational basis—specifically, crypto assets issued on private (not public) networks fall under existing securities and payment regulations.

First, issuing crypto assets on private blockchains (rather than public ones) enables fund managers to meet regulatory obligations, conduct KYC, AML, CFT, and sanctions screening—all prerequisites for investment. Second, fund tokens classified as securities are regulated by the FCA. This reassures investors that risks are managed, disclosures uphold market integrity, market manipulation and insider trading are curbed, and tokens are securely held.

Although these fund tokens are categorized as “security tokens,” in the UK they are regulated under the FCA’s Collective Investment Schemes Sourcebook (COLL) similarly to traditional mutual fund shares. In practice, fund

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News