Betting on RWA: Frax V3's Current Performance and Future Outlook

TechFlow Selected TechFlow Selected

Betting on RWA: Frax V3's Current Performance and Future Outlook

This article will focus on the latest version of FRAX v3, the native stablecoin.

Author: CHULIE, HUMBLE FARMER ARMY RESEARCH

Compiled by: TechFlow

Given the lack of on-chain activity, low trading volumes, insufficient leverage demand, and high interest rates in traditional financial markets, tokenized treasuries are currently the only sustainable source of real yield in the crypto space.

Therefore, we expect the RWA sector to continue growing strongly until some major shift occurs.

Frax Finance

Most readers are likely already familiar with frax.finance—an established DeFi protocol whose product suite spans multiple verticals: FRAX (a stablecoin), Fraxlend (a lending market), Fraxswap (an AMM), frxETH (a liquid staking protocol), Fraxferry (a cross-chain bridge), and eventually Fraxchain, their own L2 execution environment.

Given Frax’s broad footprint across various domains, it benefits from tailwinds across different sectors. For instance, FXS participated in this year's LSD season, and frxETH remains a healthy performer:

Is this time different? Can Frax also benefit from the RWA narrative?

This article will focus on FRAX v3, the latest version of their native stablecoin.

Historically, FRAX was partially backed by crypto collateral and partially by FXS. Over time, FRAX has been moving away from FXS backing toward becoming a fully collateralized stablecoin. With FRAX v3, this transition advances further as they introduce RWAs as collateral.

FRAX v3

By integrating FinResPBC—a public benefit corporation that primarily provides Frax with access to RWAs—Frax now has an integrated mechanism to bring treasury market yields into its ecosystem. This is the biggest update to FRAX since its launch at the end of 2020. Unlike MakerDAO, which relies on a series of counterparties to access "real-world" yields, FinResPBC acts directly on behalf of Frax, eliminating intermediary fees in the process.

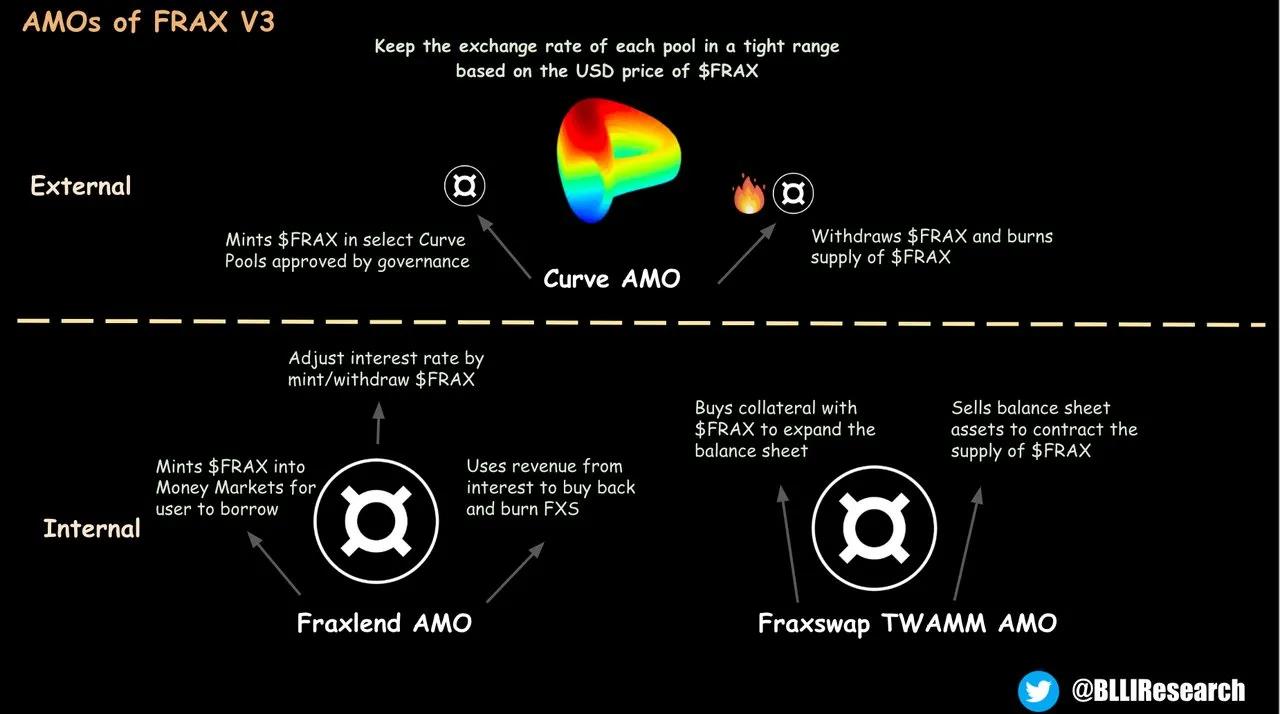

FRAX v3 will still rely on Frax’s AMO mechanism to maintain peg stability (as shown above) and leverage the DAO’s significant influence within the Curve ecosystem to incentivize liquidity. Similarly, FRAX v3 introduces fully on-chain governance via fraxGov (removing Frax’s reliance on multi-sig trust assumptions). However, for us, the more interesting developments in v3 revolve around the introduction of sFRAX and FXB.

sFRAX allows FRAX holders to participate in the short end of the yield curve (money markets), while Frax Bonds (FXB) represent exposure to the long end. The yield on sFRAX fluctuates with the overnight repo rate, tracked via an oracle based on the Interest on Reserve Balances (IORB). The yield paid by Frax Bonds will vary according to the interest rate of the underlying bonds matched in term. Each week, based on the amount of FRAX staked in sFRAX and the IORB rate, Frax will use FinResPBC to transfer the necessary amount of RWA assets. The FXB process follows a similar model, where Frax uses FinResPBC to deploy RWA strategies matching the duration of bonds sold on-chain. Ultimately, Frax is creating an on-chain representation of the yield curve.

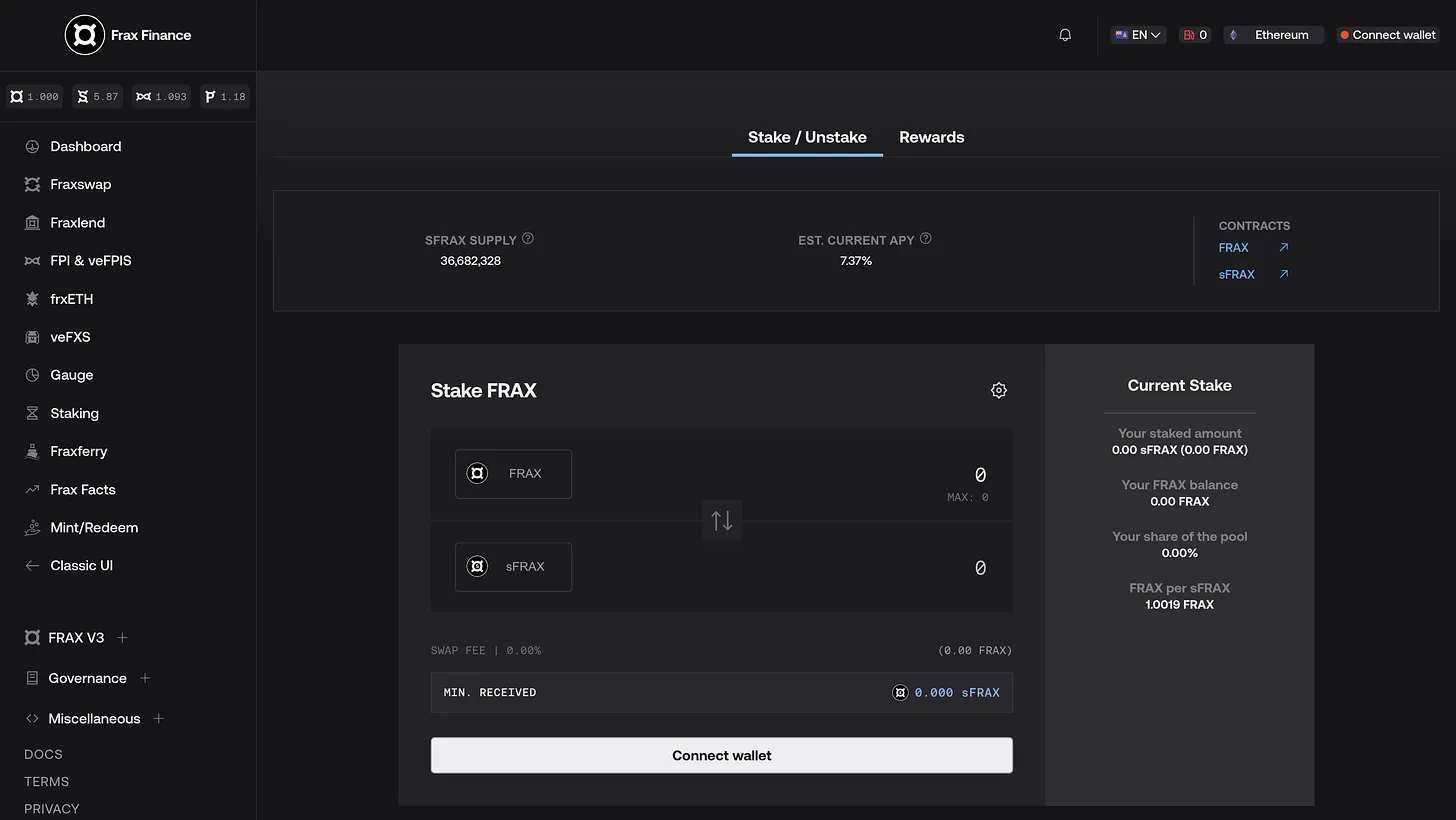

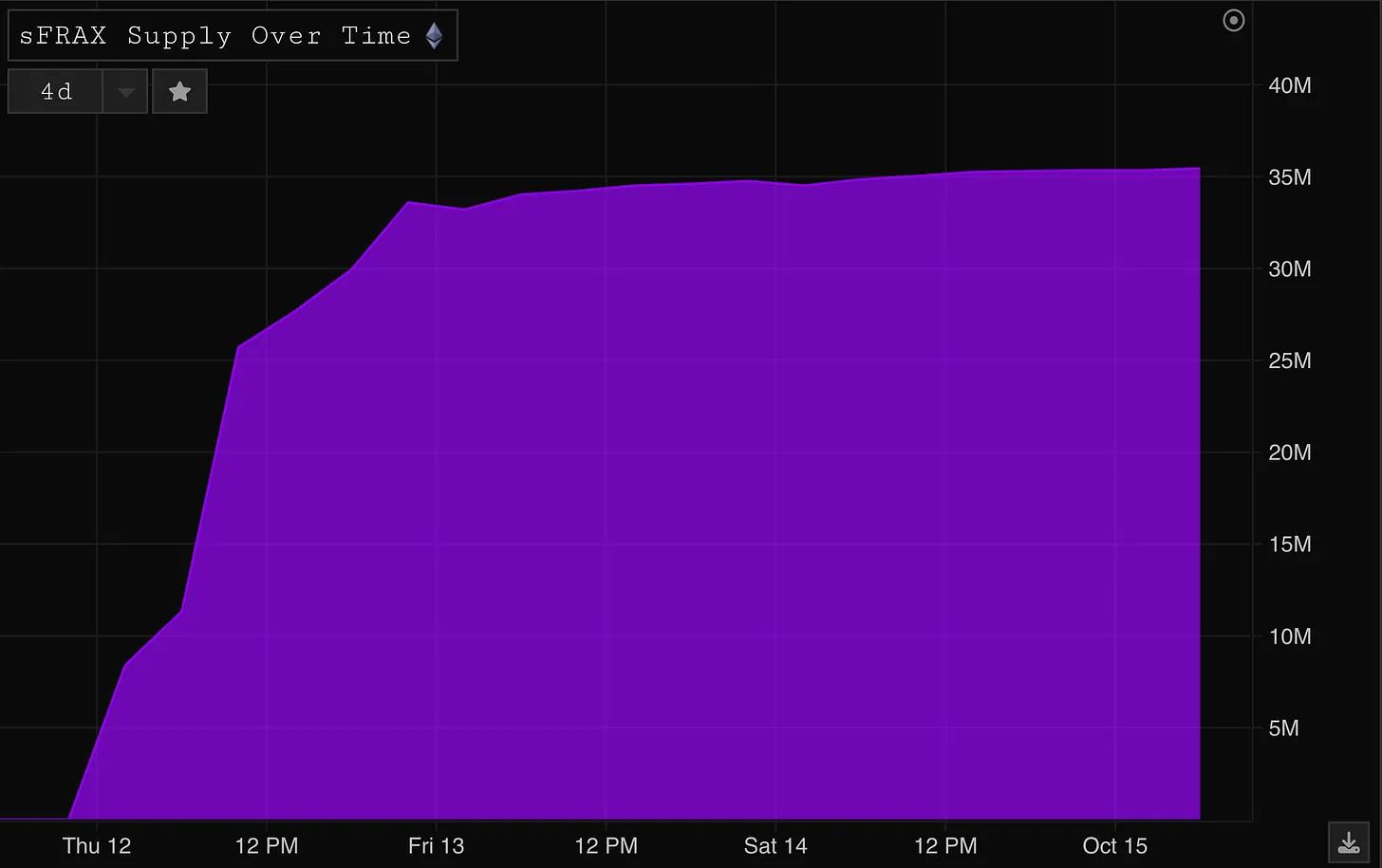

The first version of FRAX v3 went live Wednesday evening (ET), with sFRAX offering a 7.37% yield—off to a strong start:

Of course, as more FRAX flows into sFRAX, this yield will decline over time, but the initial adoption is promising and supports our argument that interest-bearing USD has strong product-market fit.

Looking Ahead

Just as DAI growth signaled MakerDAO’s success, increases in FRAX market cap will be a simple metric to gauge progress. Likewise, growth and expansion of sFRAX as collateral will be critical. There is anticipation that Curve will enable sFRAX as collateral for crvUSD minting, which could provide strong momentum. FXB has not yet launched, but similarly, supply expansion and usage as collateral will be key performance indicators.

TVL is often a low-signal metric for crypto projects, but in this case, growth in stablecoin market cap drives increased RWA backing, which directly correlates with higher yields, protocol revenue, and profitability. While initial surplus profits will go toward achieving 100% collateralization of FRAX, FXS will ultimately benefit. If FRAX v3 succeeds and we see meaningful growth, we expect the market to reflect this in the FXS price.

Historically, Frax has been criticized for doing too many things without leading in any single vertical. However, their products are highly synergistic and typically operate cohesively—for example, sfrxETH can be used as collateral to borrow FRAX on Fraxlend, which can then be staked as sFRAX. We believe labeling them as “narrative chasers” or similar is reductive; the Frax team maintains a long-term vision and builds different parts of their tech stack as needed over time.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News