Understanding "Minimum Viable Issuance" (MVI): Balancing Security and Inflation in ETH

TechFlow Selected TechFlow Selected

Understanding "Minimum Viable Issuance" (MVI): Balancing Security and Inflation in ETH

This article will explain why issuing beyond the "minimum viable issuance" reduces Ethereum's utility.

Written by: Anders Elowsson

Compiled by: TechFlow

Introduction

I believe achieving "Minimum Viable Issuance" (MVI) is critically important—a key commitment to ordinary Ethereum users. Staking should secure Ethereum, not act as an inflation tax that erodes utility and liquidity while creating oligarchic risks.

Ethereum continues evolving and may one day underpin the global financial system. We must assume that “ordinary users” will understand Ethereum’s internal workings about as well as most people today understand the current financial system.

Of course, we cannot assume ordinary users will be driven by ideological motivations, as was the case with Ethereum’s original creators. Our job is to ensure proper incentives are in place so Ethereum can grow unimpeded.

A core design principle from Ethereum’s inception has been “Minimum Viable Issuance” (MVI): the amount of ETH issued by the protocol should not exceed what is strictly necessary for security. This principle holds true under both Proof-of-Work (PoW) and Proof-of-Stake (PoS).

Under PoW, MVI prevented miners from charging ordinary users excessive inflation taxes. Thus, block rewards were reduced from 5 ETH to 3 ETH, and eventually to 2 ETH.

Under PoS, the MVI principle should also be upheld—avoiding excessive inflation taxes on ordinary users. Ordinary users shouldn’t need to understand staking details just to prevent their savings from being diluted or to avoid supporting potentially censoring validator sets.

Therefore, MVI means issuing just enough to keep the staking ratio (the proportion of all ETH used for staking) sufficiently high—but no higher. In this article, I aim to clarify how issuance beyond the “minimum viable” level reduces Ethereum’s overall utility.

Benefits of MVI for User Empowerment

For individuals, participating in staking involves various opportunity costs. It requires resources, attention, technical knowledge—or trust in third parties—and it reduces liquidity. Liquid staking tokens (LSTs) are less reliable than native ETH and less suitable as money or collateral.

Thus, individuals expect returns from staking. Define their minimum acceptable yield as the lowest return they’d accept (using their preferred staking method). The (inverse) supply curve of Ethereum then emerges from future holders’ minimum yield expectations.

A holder’s reservation yield can be seen as an “indifference point,” where the utility of staking equals that of not staking. This implies that reducing issuance can actually increase everyone’s utility—even stakers—as long as Ethereum remains securely safe.

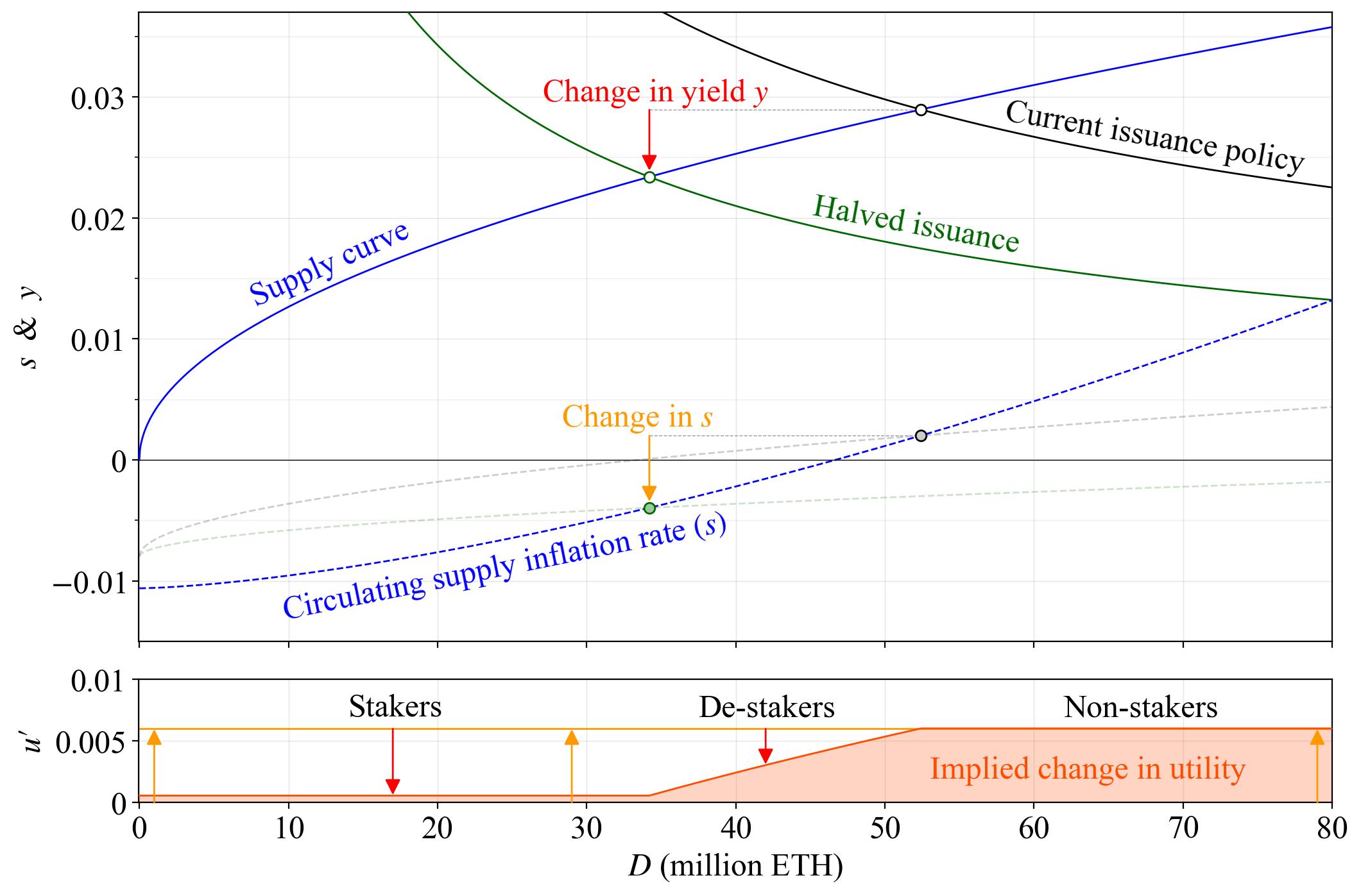

Consider a hypothetical supply curve with elasticity of supply at 2 (blue line). Here, I set it so that when staked amount D reaches 25 million ETH, the yield hits 2%—meaning the marginal staker demands at least a 2% return when 25 million ETH are staked.

Real-world supply curves are complex phenomena—we haven’t reached equilibrium yet—but we’ll start with this simple and fairly realistic scenario. We’ll also ignore compounding complexities.

The burn rate b is set at 0.008—representing the annualized fraction of ETH burned since The Merge relative to total supply. But this isn’t crucial, as our focus is on shifts between medium-term equilibrium points (circles), not long-term drift in total ETH supply.

Realized Extractable Value (REV)—slightly over 300,000 ETH per year—is added to protocol issuance to form the black demand curve (current policy) and green demand curve (halving issuance by reducing base reward factor F from 64 to 32).

Halving issuance lowers yield y (red arrow). This reduces issuance yield yi = y - yv (where yv is yield from REV), thereby lowering issuance i = yi×d and circulating supply inflation rate s = i - b (orange arrow).

Over one year, the change P in someone’s share of circulating ETH holdings depends on s and each holder’s yield y, according to: P = (1 + y)/(1 + s) - 1

Current issuance policy gives P₁; halved issuance gives P₂. Their relative improvement is: P′ = (1 + P₂)/(1 + P₁) - 1

Define utility change u′ = P′, but when calculating P₂, use each agent’s respective minimum acceptable yield for those who stop staking. Below that yield, they wouldn’t stake anyway, so further yield drops don’t impose additional utility loss.

By this definition, everyone gains higher utility under the new equilibrium. Stakers see lower yields, but the drop in supply inflation is greater, allowing them to gain a larger share of ETH.

Non-stakers clearly benefit more—their only change is receiving fewer newly issued ETH from stakers. Only those who cease staking lose proportional ownership of circulating ETH under the new equilibrium.

Yet due to frictionless utility gains, their situation still implicitly improves. For example, the marginal staker at the old equilibrium was indifferent to staking, so stopping allows full capture of deflationary benefits without downside.

Those who partially disengage still benefit from lower inflation, despite some income loss, until they become fully indifferent to staking or unstaking. We’ve shown issuance policy isn’t zero-sum from a utility perspective.

Moreover, any group’s utility gain broadly benefits all token holders.

As long as one holds underlying ETH, everyone benefits from MVI. This excludes CEXs and other staking service providers (SSPs) profiting from staking fees. They don’t benefit from reduced supply inflation and prefer high yields to maintain high fee revenue.

But issuance above MVI forces unwilling participants to either suffer utility loss by staking or face economic dilution by not staking. Even willing stakers fare worse under realistic supply curves. Note: this analysis doesn’t even include tax implications.

A PoS cryptocurrency with 5% yield, universal staking, and average 20% taxation on staking income, dedicates 1% of its market cap annually to taxes—more than Bitcoin will pay miners post-next halving.

The argument doesn’t depend on user views about tax levels or how staking rewards are interpreted. Still, we conclude: enforcing MVI keeps Ethereum more neutral across differing tax policies among nation-states.

PoS arguably requires lower rewards than PoW for equivalent security. Leveraging this to maximize user utility is vital. For instance, 2% yield on 25 million staked ETH gives total rewards Y = 0.02 × 25 = 0.5 million ETH.

The resulting “return rate” sustaining solid security is roughly r = Y/S = 0.4%—surprisingly low. We should leverage this fully to maximize user utility. The potential equilibrium under current issuance policy is marked by the black circle.

At ~3% yield with 50 million ETH staked, Y = 1.5 million ETH/year. A difference of 1 million ETH/year (over $1 billion at current prices) could instead be returned to users without diluting holders.

Under MVI, average 15% staking fees would give CEXs and SSPs ~$250 million in excess profits annually. Some goes to shareholders, some may fund lobbying to keep yields permanently above MVI.

Macro-Level Benefits of MVI

I often advocate for ETH penetration throughout the ecosystem. For L2s, bridging ETH binds L1 and L2 together and provides external capital to L2 users, enhancing their financial security.

If your system forces users to rely on opinionated ETH derivatives to avoid inflation taxes, the entire ecosystem becomes more fragile.

For example, consider users unable to self-stake delegating ETH to organizations running validators (SSPs). These SSPs issue LSTs usable as collateral on Ethereum.

If the protocol operates above MVI with high staking ratios, one or a few LSTs might replace ETH as the dominant currency across layers and applications. What would be the consequences?

First, positive network externalities from monetary dominance may allow an LST to maintain leadership even if its SSP offers inferior service (e.g., higher fees or worse risk-adjusted returns).

Second, and more importantly, LST holders—and any app or user relying on LST value—become fate-locked to the LST and ultimately to the issuing SSP.

This effectively requires Ethereum to undermine itself significantly. Affected users may reinterpret misbehavior or failure as something entirely different. Once you become Ethereum’s money, you become part of the social layer. We no longer care only about the fraction of ETH staked under LSTs, but the fraction of total ETH supply. Corrupt institutions sit one layer above the consensus mechanism.

As evident from The DAO, if the affected portion of total circulating supply becomes large enough, the “social layer” may waver in its commitment to the intended consensus process.

If the community can no longer effectively intervene during events like 51% liveness attacks, risk mitigation via Buterin’s discussed early warning systems may fail.

In such cases, the consensus mechanism, mediated through derivatives, becomes so vast and interconnected that its ultimate arbiter—the social consensus—becomes overloaded.

Now consider a different scenario under MVI. First, every LST faces stiffer competition from non-staked ETH. Thus, the ability to monopolize monetary functions and charge high fees or offer riskier products diminishes.

Second, the social layer stays natively tied to Ethereum and ETH—not to external organizations and their ETH derivatives. By keeping staking ratios low enough under MVI, participant risk calculations shift.

Under MVI, when staking ratios are low enough to prevent moral hazard, the principal-agent problem (PAP) of delegating to dominant LSTs can be more accurately priced. No LST grows so large in the eyes of Ethereum’s social layer that it becomes “too big to fail.”

This pricing reflects the fact that the larger the staked share controlled by an agent acting on behalf of principals (or anyone intervening), the better the opportunity for that party to degrade consensus for personal gain.

Delegators must always consider what security guarantees they truly have (e.g., the value-at-risk of the staking agent or intermediary), knowing they could lose everything in worst-case scenarios.

Removing ETH’s direct monetary dominance, assuming staking ratios under MVI grow to utility-maximizing scale, larger SSPs may find non-monopolistic strategies more profitable (i.e., increasing fees moderately).

This is merely a comment on the present. But importantly, it reflects the reality: for every “cartel layer” we eliminate, the value proposition of secure, value-aligned SSPs increases relatively.

An important step toward MVI is MEV burning, which may also help eliminate cartel layers more significant than monetary function. MEV burning helps reduce reward variance for solo stakers, which increases if issuance yields fall.

It also enables more precise targeting of MVI by removing a revenue source that can vary unpredictably over time.

Notably, future mechanisms may address certain aspects of the principal-agent problem in delegated staking (e.g., single-slot finality). But fundamental issues around trust, monopoly incentives, and censorship capacity may remain difficult to escape.

Another benefit of MVI is improved conditions for (independent) staking, related to the direct link between staking scale, number of validators, and validator size. If staking scale changes, so do validator size or count (network load).

This effect cascades across protocol design space, influencing any parameter possibly adjusted for higher or lower network load—such as those linked to variable validator balances.

This is a fundamental property of the current consensus mechanism. If issuance policy leads to d=0.6 instead of d=0.2 at medium-term equilibrium, independent staking would require three times more ETH under unchanged conditions to maintain the same network load.

Ultimately, I believe MVI’s greatest benefit lies in empowering ordinary users. Ethereum is uniquely positioned to make native crypto into global money—a valuable opportunity worth pursuing.

When nations implement price inflation by expanding monetary base, they control ordinary people’s intertemporal choices—and assume this control remains viable in a digital, globalized world.

Ethereum should not control ordinary people nor force them to sacrifice liquidity. We should let them access Ethereum’s monetary utility as seamlessly as possible. Ethereum’s “risk-free rate” should simply be holding (and transacting) ETH.

Addressing Potential Concerns About MVI

Having outlined MVI’s potential benefits, the second part addresses common criticisms—such as reduced economic security and the belief that lowering yields will cause delegated staking to replace all independent staking.

Regarding the first point, it's true: higher staking ratios do force attackers to spend more resources, e.g., to reverse finality. This is not trivial.

Our goal isn't “minimum issuance”—it must always be “viable.” Buterin offers intuitive guidance on how expensive a 51% attack on Ethereum should be.

We might also interpret the nearly 14 million ETH securing Ethereum at The Merge as the ecosystem’s “preference” for a staking level deemed sufficiently secure under the current consensus mechanism (resilient against long-range attacks, not just super-committee accountability).

Meanwhile, having a healthy margin is good. Current staking ratio (d ≈ 0.2) vs. post-Merge (d ≈ 0.1) may meaningfully improve resistance to long-range attacks.

The reward curve shouldn’t be too steep—that’s why we may want to operate somewhat below the preference point, eventually determining d through probabilistic analysis of staking supply and demand.

Some argue delegated staking makes attack resource allocation easier—an “apparent” security. But by penalizing all staking and eliminating moral hazard (via MVI), delegators must be very cautious when delegating, as previously noted.

In this setup, markets determine appropriate capitalization ratios for staking operators and price staking risks. Ethereum’s role is to punish misbehavior and preserve ETH’s value relative to secured value.

By ensuring ETH penetrates the real economy and all consensus participants have real skin in the game, we set a price for attacks harder to bypass via financial engineering.

I mention this because interesting alternative proposals exist—where Ethereum intervenes in delegation so principals bear no risk. Then contributors to consensus degradation face far lower risk.

Or so it seems. When Ethereum forks or requires social intervention to survive, risk-free delegators might be surprised at how the social layer assesses their delegation and perceived damages in worst-case outcomes.

Again, I echo Buterin’s plea: don’t overload consensus. My point—and a theme of this article—is that when the fraction of ETH involved in consensus is too high, everyone gets drawn in, making “neutral” outcomes impossible.

Conclusion on the first concern: d under MVI must stay large enough for security; delegation does reduce security somewhat, but as long as stakes carry risk, agents will assess risks and delegate wisely.

Preserving independent stakers is indeed a complex puzzle. Economies of scale are hard to eliminate by design, and we haven’t focused enough on liquidity in staking. But there are nuances in the current debate favoring MVI that I hope to highlight.

Independent home stakers incur certain costs when staking. They front-load much of the cost, including knowledge acquisition. They also bear variable costs like bandwidth, troubleshooting time, and outage risk.

Many SSPs also incur significant design costs and shoulder operational expenses independent stakers don’t face. Yet they leverage economies of scale to reduce per-validator operating costs.

We must assume SSPs seek profit maximization and consider what fees they might charge under different equilibria. How do economies of scale differ between d=0.2 and d=0.6? It’s reasonable to assume SSPs have much lower average costs at d=0.6.

Recall that at d=0.2, independent stakers might run validators one-third the size compared to d=0.6. This could mean the difference between attracting independent stakers with 32 ETH versus 96 ETH (or 11 ETH vs. 32 ETH).

Thus, not only does higher d force independent stakers to hold more ETH for the same network load, they also compete against SSPs capable of charging lower fees. While fees reflect market strategy, average costs should ultimately matter.

If we reduce yields, SSPs may raise fees to properly recoup and amortize costs. Delegated staking costs are variable—PAP and fees. Delegators can easily walk away from increased fees.

The argument that lower yields will drive independent stakers to leave (before delegated stakers) deserves attention. But since existing home stakers already incurred fixed costs, their individual supply elasticity may currently be low.

However, if we lower yields so much that home staking becomes infeasible (including for new entrants), their short-term low elasticity won’t help. If we wish to preserve independent staking, there exists a floor below which total staking yield must not fall.

Assume total cost of independent home staking (in ETH) is C, and consider other factors like annual risk R on capital. Then yield must satisfy y > C/32 + R, requiring a reasonable margin even with re-staking improving liquidity.

Here I also want to discuss DeFi yield effects. All stakers earn endogenous staking yield y—derived from issuance, MEV, and priority fees. Some may also earn exogenous yield yc outside the consensus mechanism.

One cannot simply sum y + yc for LST holders and conclude LST holders always win over independent stakers regardless of y’s decline. Expectedly, native ETH offers higher utility than LSTs (excluding their endogenous yield).

Delegators weigh y(1−f), where f is fee percentage, against risks/costs including PAP and inherent disadvantages of LSTs vs. native ETH—and only stake if y(1−f) (not y+yc) exceeds these costs.

When y=0, agents won’t delegate. They get better liquidity or higher yc from native ETH and face severe adverse selection by delegating to SSPs operating at a loss. Independent stakers may also refrain.

For those who want to hold ETH anyway, the decision may not hinge on whether yc is 1% or 5%. At 5%, ETH is expected to deliver +5%. Of course, that 5% carries risk—it’s not free money (nor should it be, hence MVI).

As y rises, potential independent and delegated stakers gradually find staking compelling—starting with the most ambitious/risk-tolerant. Here we form a supply schedule where each agent decides based on individual circumstances.

The distribution of minimum acceptable yields between potential independent and delegated stakers remains unclear. At d=0.2 medium-term equilibrium, independent stakers’ share may be lower than at d=0.6—but the reverse is also plausible.

Higher d may allow SSPs greater diversification, but cartel pressures on monetary function counteract this. The pool of individuals with enough ETH for independent staking is limited, setting a soft cap on total independent stakers.

This is indeed a topic worthy of further study. Crucially, staking opportunity costs must always be fully accounted for—scale economies and monopolies affect baseline equilibrium analysis in complex ways.

Finally, re-staking has potential to make independent stakers more competitive. It lets them “re-stake” their stake when desired (though they themselves may face principal-agent problems if providing economic security).

One benefit of re-staking is that if active validation services (AVS) can quantify decentralization, they can assign economic surplus value to it—something Ethereum as an open protocol cannot do.

The previous arguments also apply to re-staking on out-of-protocol EigenLayer functions. At very low yields, users are better off using non-staked ETH (“free staking”). For many use cases, AVSs likely prefer a token that won’t easily vanish.

Also note: if PEPC expands beyond “block production use cases,” generated revenue may become more endogenous, depending on residual utility provided.

Looking Ahead

With this, the discussion on MVI’s pros and cons concludes. While concerns about solo staking persist, MVI remains a fundamentally sound design policy—one that gives Ethereum a real chance to deliver the best digital currency ever created for users.

Every argument has nuance, and some discussions can’t be condensed into tweets. But I believe, weighing all factors, we should accept MVI as a favorable design principle under PoS as well.

We must always prioritize the “ordinary user”—requiring micro-founded research and evaluating how we maximize utility for regular people as Ethereum (hopefully) becomes their new financial system.

So the question becomes: how do we achieve MVI? This is what I’ve been deeply researching. Dietrichs recently emphasized communicating current issuance policy research on a dev call—my journey began with that tweet.

Changing issuance policy is sensitive. We seek a policy that maximizes utility without needing further developer intervention—one that autonomously delivers optimal MVI forever.

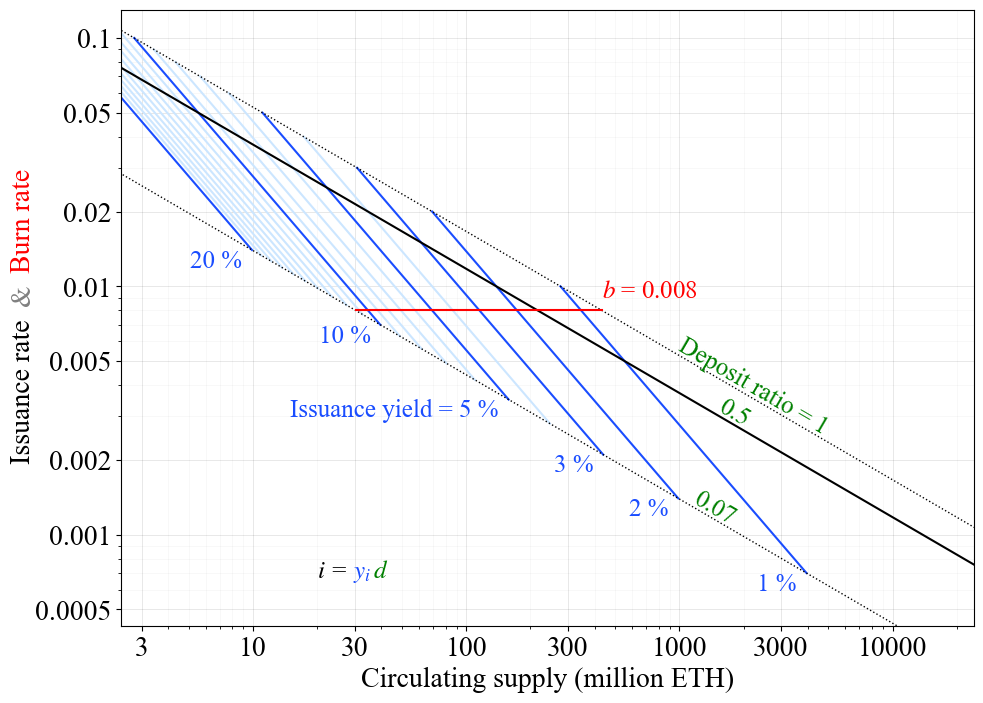

But the current reward curve ties issuance to staking scale (D), not staking ratio (d). Medium-term, these correlate closely; long-term, they diverge as circulating supply drifts.

This was the topic of my 2021 EthResearch post and Devconnect talk: define how circulating supply S drifts toward equilibrium (i=b), enabling us to improve the reward curve and achieve Minimum Viable Issuance under PoS.

Since under the current reward curve, issuance i can be expressed as i = cF√d / √S, it varies with circulating supply (with staking ratio d offering some buffering). The chart shows Ethereum’s issuance rate diagonal and average b since The Merge.

Burn rate b does not depend on circulating supply—demand for block space doesn’t change because the monetary unit changes. If i > b, S rises and pulls i down until equal to b. If i < b, S falls and pulls i up until equal to b.

In 2021, stakers didn’t have REV, so I directly used minimum acceptable yield y⁻ to derive Ethereum’s security as d = b/y.

Today, we simply add the “REV rate” v to get d = (b + v)/y. This means we cannot control staking ratio and security long-term unless we’re prepared to periodically adjust F.

We can cut F temporarily to avoid overpaying for security (to be discussed next). But Ethereum will eventually return to the same long-term equilibrium staking ratio at a lower circulating supply (ceteris paribus).

That’s why we ultimately want to change the reward curve to depend on d rather than D. Simply replacing D with S₀d (where S₀ is current circulating supply) seems tempting—it moves us toward autonomous issuance policy, but still doesn’t guarantee it.

Assume MEV burning: then the protocol fully adapts to revenue changes, but still cannot adapt to permanent shifts in expected yield—i.e., supply curve movements. This could be handled by allowing the entire reward curve (demand curve) to slowly drift.

The ultimate goal is a dynamic equilibrium where, absent external shocks, circulating supply changes at a constant rate. Whether inflationary or deflationary depends on the supply curve and how block space value reflects in ETH’s market cap.

Thus, we achieve what Polynya calls “constant” security—I think this aptly describes our end goal: finally removing issuance control from developers and making Ethereum autonomous under MVI.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News