Folius Ventures: Identifying the Competitive Landscape of Web3 Gaming Startups and Potential New Opportunities

TechFlow Selected TechFlow Selected

Folius Ventures: Identifying the Competitive Landscape of Web3 Gaming Startups and Potential New Opportunities

This report outlines the competitive landscape of the Web3 gaming industry and identifies currently viable entrepreneurial opportunities.

Report Summary

Against the backdrop of rising global gaming industry standards and overcapacity, Web3 has emerged as a cost-recovery channel for game developers due to its high profit margins across the full product lifecycle, attracting numerous web2 teams. However, today’s Web3 supply side faces overcapacity while demand-side liquidity has dried up. After two years of development, these structural issues are becoming increasingly evident. This report therefore analyzes the competitive landscape of the Web3 gaming industry and identifies viable entrepreneurial opportunities.

For teams still in the Web3 product development phase, it is critical to recognize that this is an industry with incomplete infrastructure but extremely high profitability—requiring multidisciplinary capabilities. Most mid-tier teams significantly lag behind top-tier players in strategic understanding and must quickly identify gaps and accelerate their learning and iteration speed. Meanwhile, new business models continue to emerge; teams that can creatively leverage Web3 monetization tools stand to gain first-mover advantage. Teams should also seize opportunities arising from shifts in distribution dynamics—either by capturing traffic via super apps and key entry points or by independently building their own super app ecosystems.

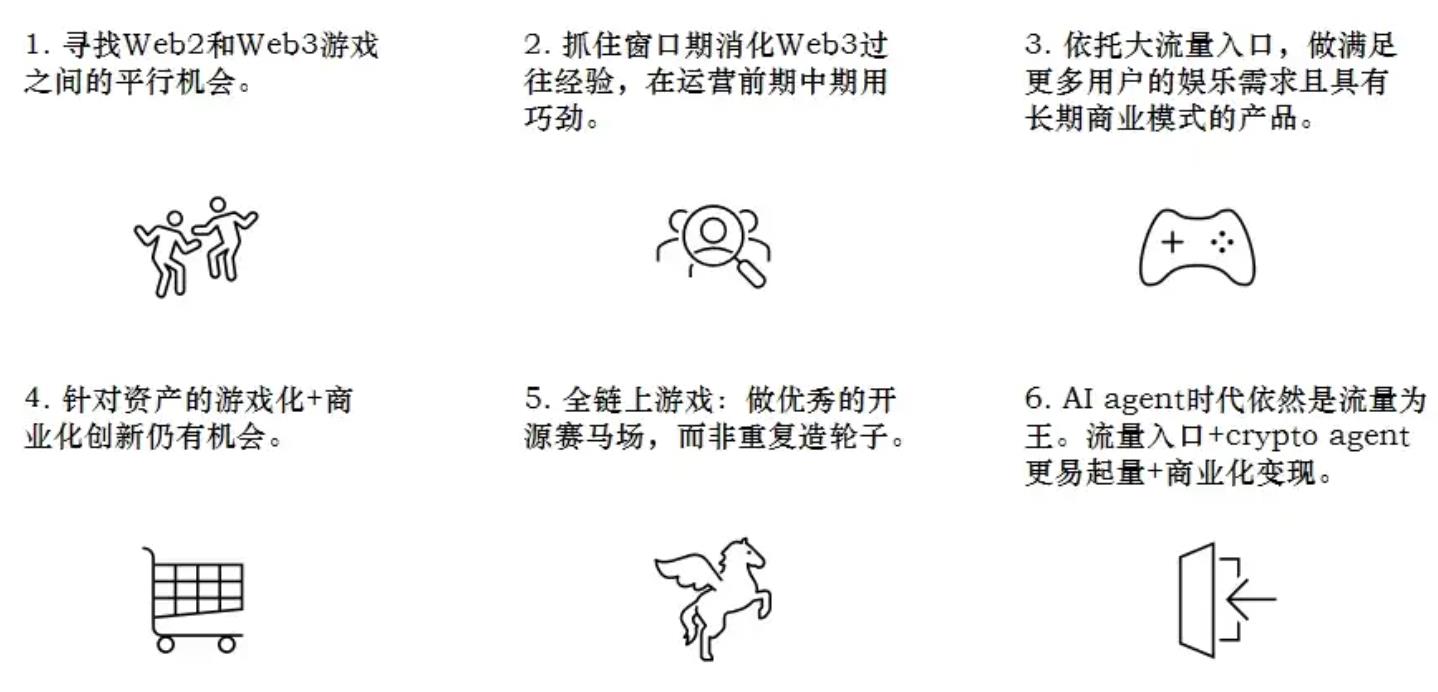

Additionally, for teams still exploring or observing the space: First, capitalize on parallel opportunities between Web2 and Web3 during a period when Web2 user acquisition costs remain high and traditional business models are hitting ceilings—especially leveraging casual games and AI-driven player growth. Second, study and internalize lessons from past successful/hot projects to extract actionable methodologies and apply smart operational tactics. Third, build products atop major traffic platforms that meet broader entertainment demands with sustainable long-term business models. Fourth, innovation around gamification and commercialization of new asset types remains promising. For fully on-chain games, we recommend focusing on creating excellent open-source playgrounds rather than reinventing the wheel—potentially sparking the next wave of adoption. Finally, in the emerging crypto agent (crypto + AI) domain, traffic will likely remain king. Teams should stick to traffic-centric strategies, as on-chain AI agents in the near future will naturally align with premium traffic gateways.

Aligned with our previous two reports, this paper attempts to summarize cyclical industry trends and provide more universal, macro-level, and actionable guidance for entrepreneurs at different stages. While writing, we deeply recognized that the industry has entered deeper waters—infrastructure progress remains slow and market liquidity is scarce, making entrepreneurship particularly challenging. Nonetheless, we hope developers can find methodological insights and breakthrough inspiration here to navigate the current bear market. We sincerely salute all pioneers pushing forward relentlessly.

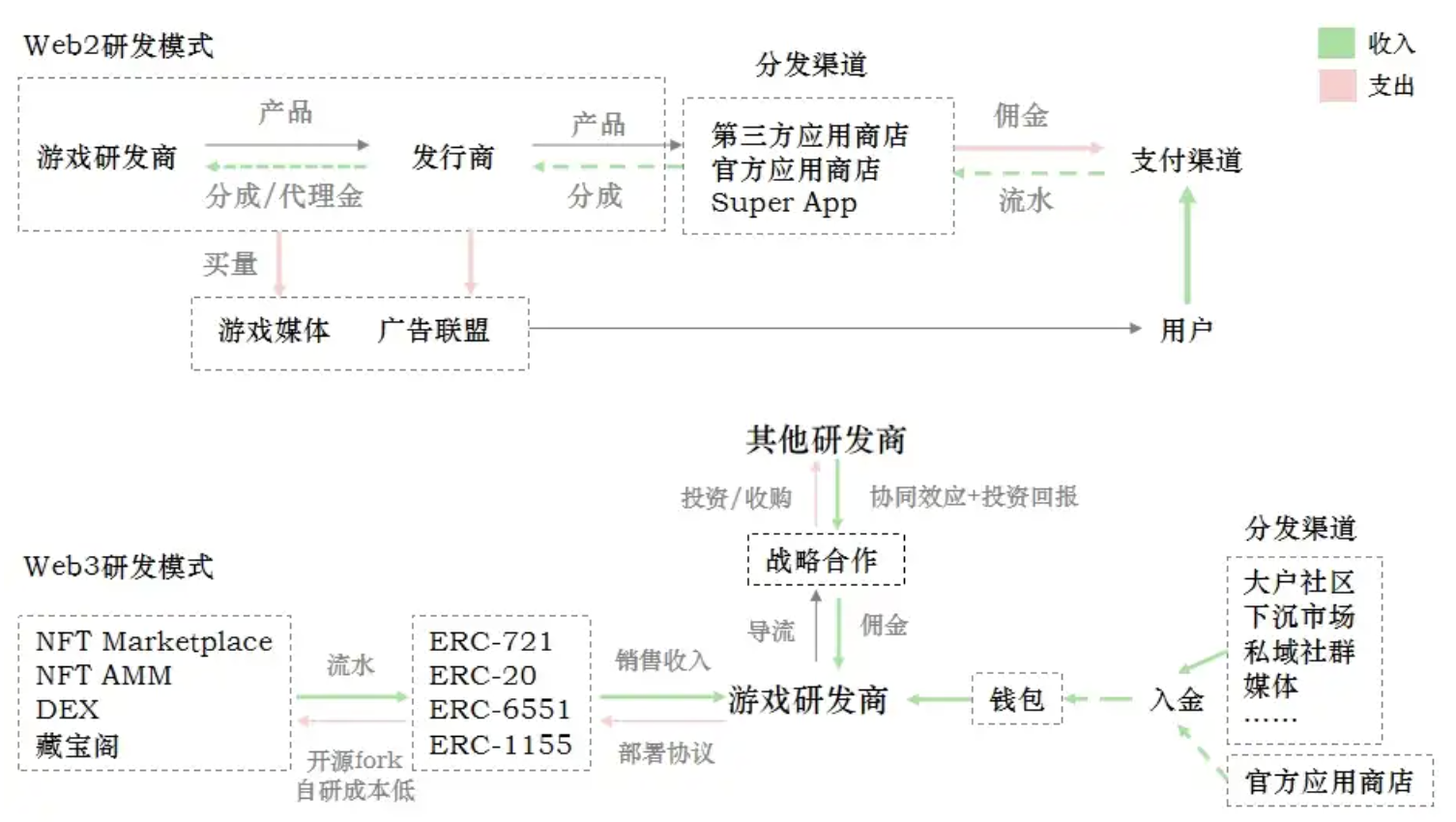

For many game studios constrained by publishing licenses and user acquisition costs, Web3 truly presents a compelling alternative

Web3 offers comprehensive monetization levers across the entire game lifecycle: NFTs, FTs, and taxation mechanisms. Compared to traditional development approaches, Web3 indeed enables higher profit margins and global reach.

Supply Side: However, as quality benchmarks rise globally, Web3 has become a sole outlet absorbing excess production capacity. After two years of evolution, systemic problems have gradually surfaced.

Demand Side: We’ve now entered an era of liquidity scarcity. The existing market is limited, attention is fragmented and highly volatile. Therefore, teams should currently focus on refining products and incentive models, aiming to break out beyond niche audiences and position themselves to ride the next wave of abundant liquidity.

What does the current competitive landscape of Web3 gaming startups look like?

Analyzed through four dimensions: industry profitability, team awareness, business models, and market dynamics.

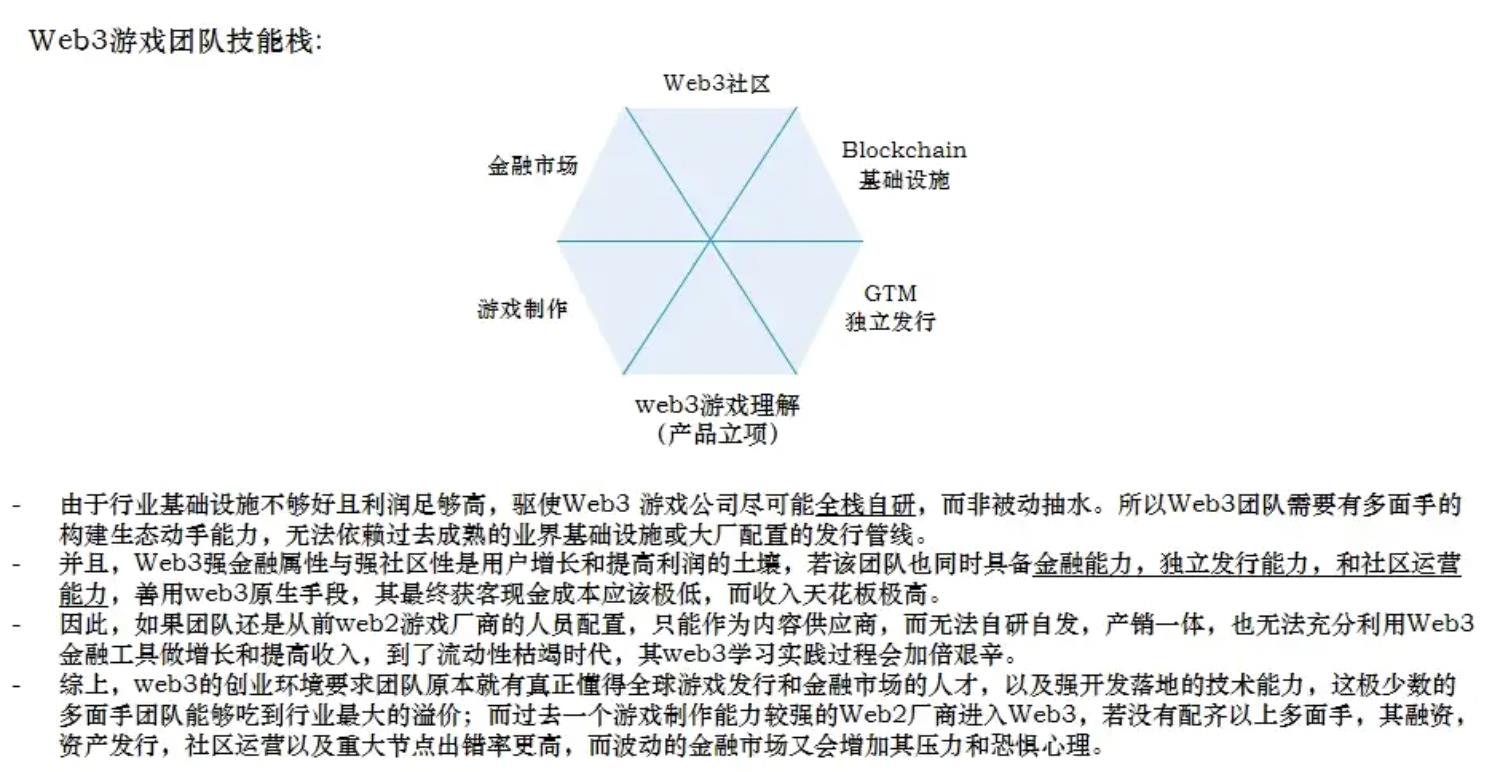

1. As an industry with immature infrastructure yet exceptionally high profit potential, generalist teams capture the most value—while those lacking diverse skill sets face amplified challenges and higher error rates.

2. The gap between mid-tier and leading studios is enormous—many may not even meet the baseline required to compete, demanding exceptional adaptability and rapid iteration capability.

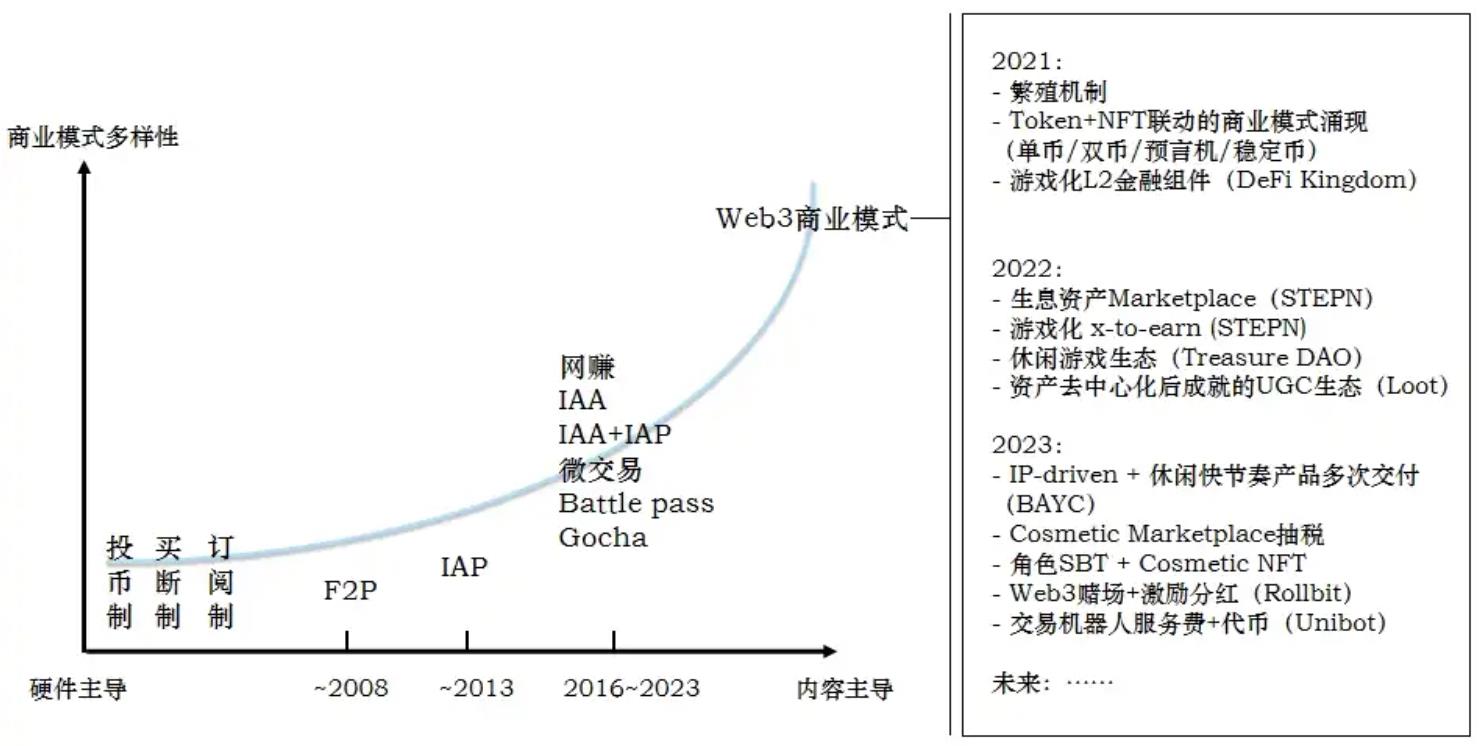

3. Business model innovation continues to surge. The more liquidity dries up, the greater the need for novelty and change. Web3 business models evolve alongside shifting market trends and new asset forms—teams must innovate based on deep market and economic modeling insights.

4. The traffic-driving power of L1/L2 chains and platforms is waning. Super-ecosystems and traffic gateways transcending individual L1/L2s are rising and preparing to compete in the next cycle. Projects must either align early with strong ecosystems or proactively establish new user acquisition pathways.

So, what directions are worth exploring for Web3 gaming teams during this liquidity drought?

1. Identify parallel opportunities between Web2 and Web3 gaming—especially when Web2 customer acquisition costs are high and monetization models are stagnating—by catching up with new consumer habits and AI experiences.

Trend 1: For the same user base, Web2 acquisition costs have risen again.

In 2023, much of Web2's global market growth stemmed from casual genres like match-3, simulation management, and casual casino games. However, user acquisition costs in these categories are high. After the breakout success of *Xun Dao Da Qian*, H5 mini-game acquisition costs tripled. Web3 targets the same user behaviors but with lower acquisition costs and higher margins. Recommendation: Casual game teams should avoid platform-centric retention battles. Instead, leverage the large traffic volume and fast attention cycles typical of casual games—launching successive titles and using cross-promotions combined with token swaps on self-built DEXs to funnel traffic and liquidity into new games.

Trend 2: Gacha monetization models are hitting bottlenecks with little room for innovation.

The gacha (pay-to-draw) business model, imported from Japan to China nearly a decade ago, has recently shown signs of fatigue—especially after domestic license approvals resumed, revealing weak consumer spending and declining overall payment volumes. On the other hand, games like *Justice Mobile* have succeeded with light monetization and massive DAU. Recommendation: Web3 offers multiple monetization levers ideal for experimentation. We recommend reviewing our prior two reports to maximize profit potential through combinations of NFTs, tokens, and tax systems.

Trend 3: Simplified experiences with high-frequency stimulation.

Games that are easy to pick up and addictive—like *Vampire Survivors*, *Shell Strike*, and *Crazy Knight Brigade*—have spawned multiple top-ranking WeChat mini-games from a single prototype. From competing on AAA realism pipelines to industrial-scale anime-style content, users are increasingly turning to fast-paced, high-stimulation microgames to pass fragmented time as aesthetic fatigue sets in. Recommendation: Designing simplified gameplay loops with effective incentives better suits Web3 teams’ strengths. The closer a game feels to primal mechanics like loot boxes, the more aligned it is with Web3’s intrinsic economic thrill. This implies more applicable templates and overlapping user profiles. Web3 games could also incorporate idle mechanics, giving them a “digital worry bead” effect rather than requiring 24/7 grinding. Hence, our previously mentioned "energy system" design remains crucial.

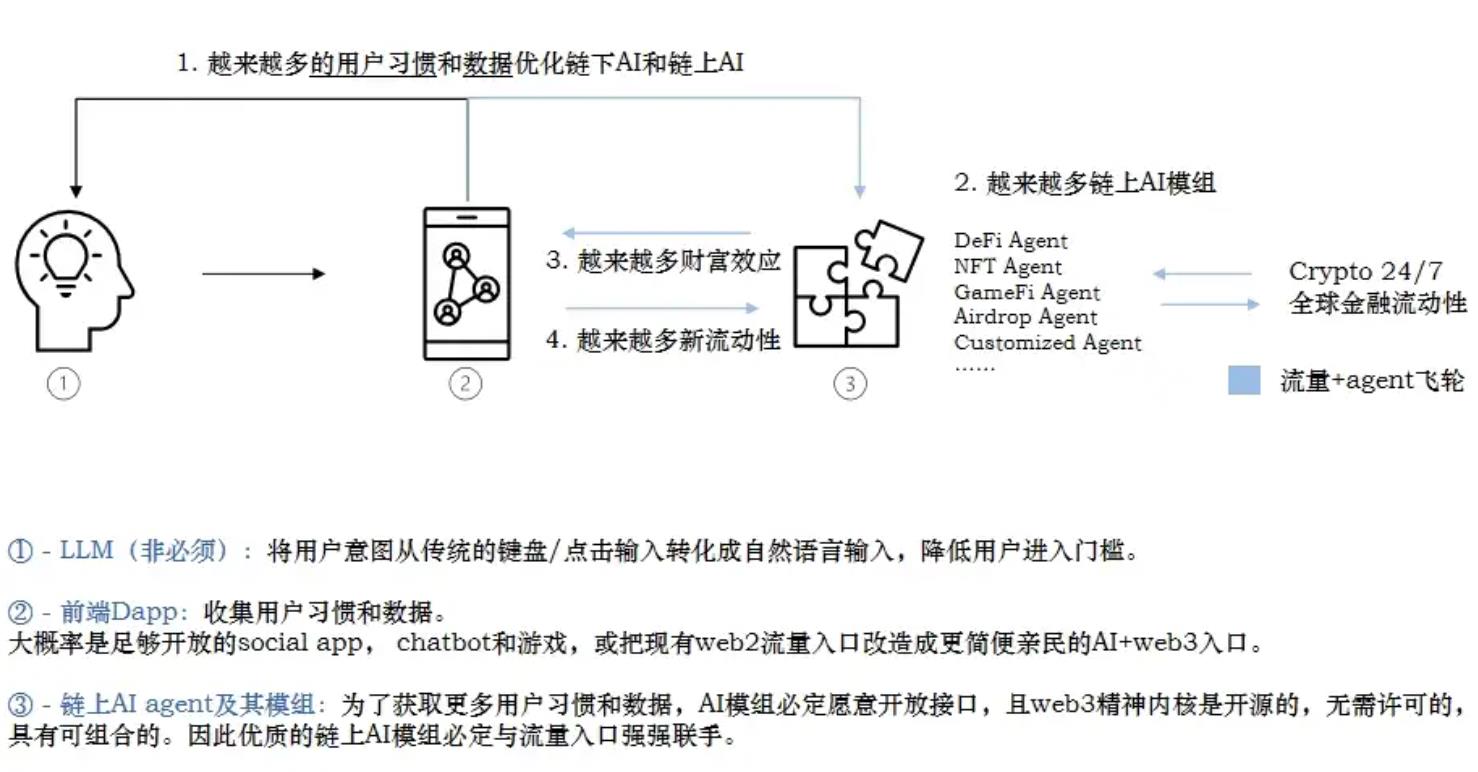

Trend 4: Advancing hand-in-hand with AI and the gaming industry.

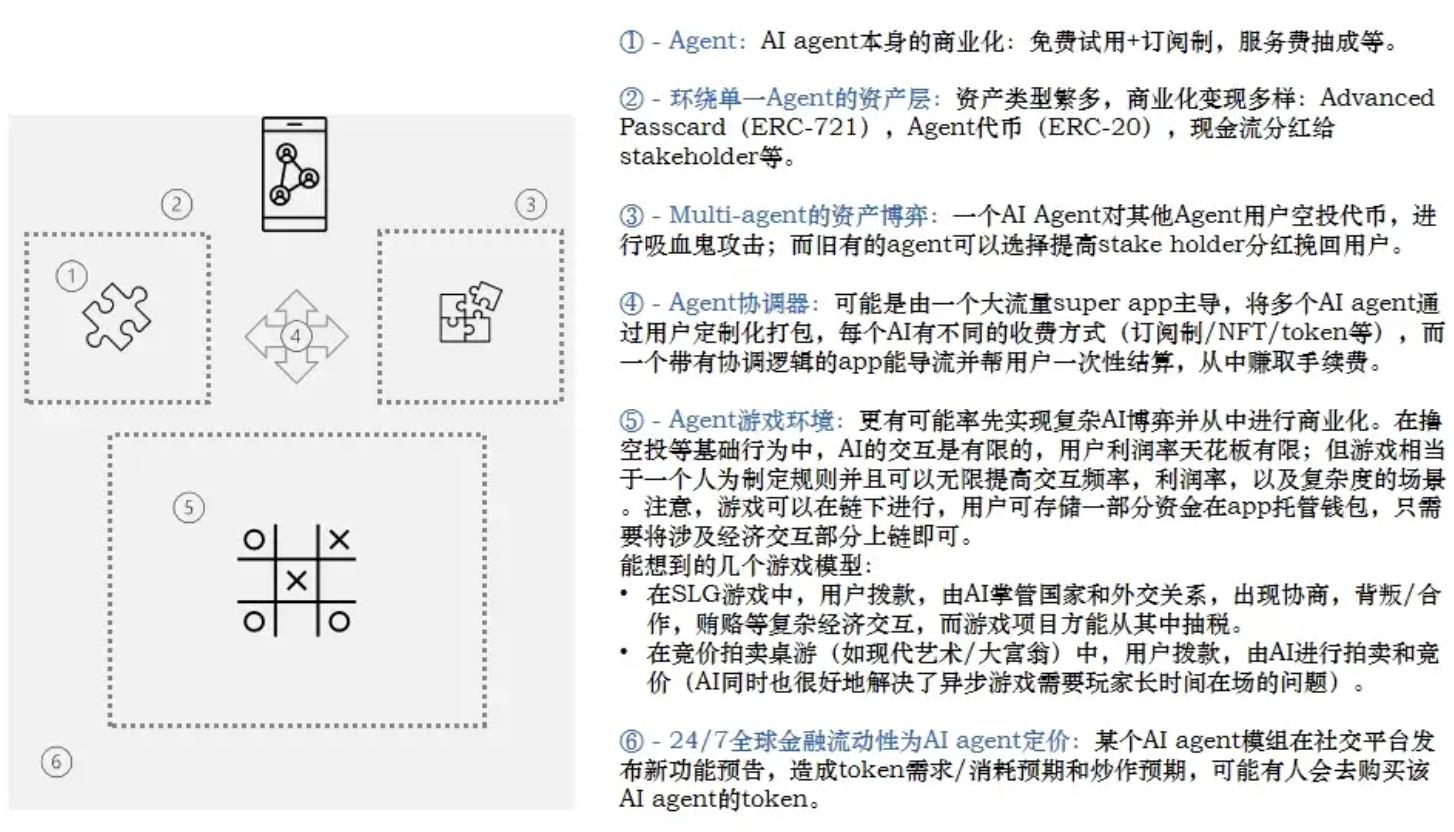

Parallel opportunities enabled by AI do exist—but follow Occam’s razor: entities should not be multiplied unnecessarily. Teams that previously failed in traditional markets or moved to Web3 due to fierce competition should reevaluate this transformative moment. Especially under China’s regulatory constraints limiting access to foreign large language models, the optimal path may be leveraging AI to create novel experiences and next-gen products while simultaneously using Web3 for global distribution and leveraged monetization. Recommendation: Focus design efforts on economic, diplomatic, or agency layers—for instance, agents within SLG games, as mentioned in earlier articles. This opens up more transactional and profitable AI applications.

2. Seize the window to absorb proven Web3 patterns and apply smart tactics during early and mid-stage operations.

Early Stage:

- Target the right data pool: (e.g., Friend.tech) When incentivizing creators on X (formerly Twitter) generates social media virality, integrating with such open data sources (via API or crawlable data) allows rapid financialization of influencers (Shares). Entrepreneurs might explore similar data pools elsewhere. The core idea is selecting off-chain proof-of-work and traffic metrics, packaging them meaningfully, and bringing them on-chain to extract rent from valuable data, information, and individuals.

- Phased invitation rollout: (e.g., STEPN, Friend.tech) Use staged invitations to gradually onboard users while conducting iterative product testing. Let FOMO and social virality build momentum before activating economic incentives—slowing initial user inflow actually extends the project’s operational lifespan.

- NFT manipulation expertise: (e.g., Memeland, Matr1x) Given the abundance of case studies and tactics left by previous NFT cycles, launching an NFT-driven game today offers many playbooks—and even a mature ecosystem centered around NFT manipulators, whitelist brokers, and KOLs. (1) Early marketing via Twitter and alpha communities, psychologically encouraging users to grind for whitelists to deepen community engagement; (2) Small, illiquid markets allow easier price control and pump-driven wealth effects; (3) Series of upcoming NFT drops maintain positive price expectations; (4) Both issuance and hype enable revenue generation at zero cost; (5) Ultimately solidify with product quality, FT airdrops, and cash flow.

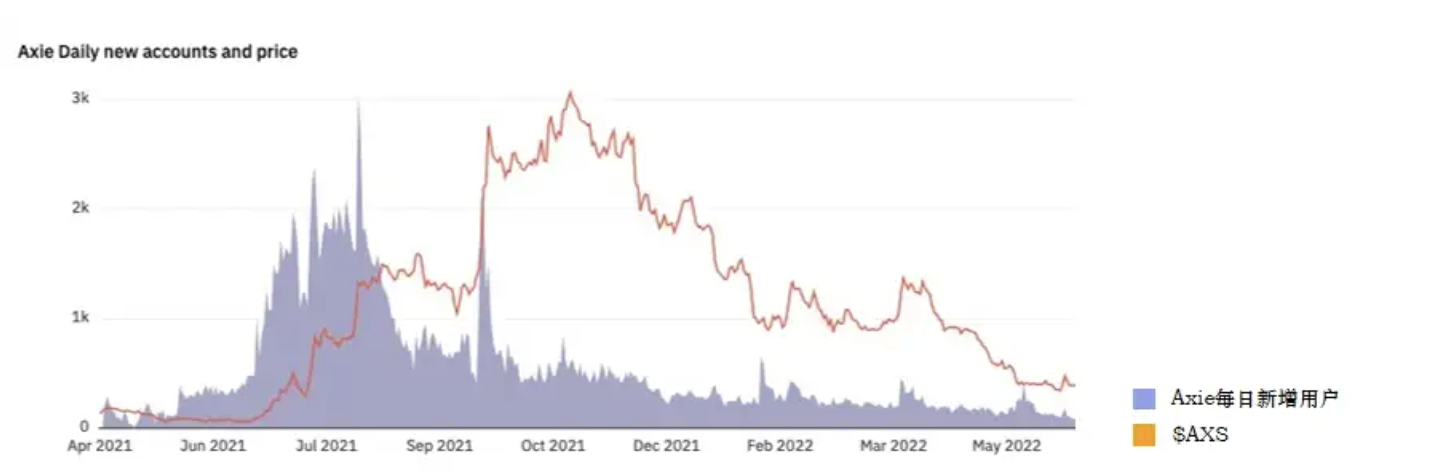

- User acquisition/geographic arbitrage: (e.g., Axie, Hooked) Conduct extensive UA channel testing, targeting low-CPI regions where users can be converted onto chain for yield farming. Establish local grassroots and distribution networks (guilds), layered with token incentives. In areas with lower average incomes, the perceived value of tokens creates stronger wealth effects, enabling organic spread and breakout potential.

Mid-Stage:

- Server-rolling logic: (e.g., STEPN) Many now pitch “Web3 distribution” to Web2 IP holders—but few realize that beyond global reach, you can relaunch the same IP across multiple chains. Given significant differences in liquidity, user demographics, and traffic support per chain (especially during high-TVL eras), launching new assets on new chains feels like opening fresh “early mines.” Users flock to earn first-mover advantages. Alternatively, akin to server rolling in traditional games, players restart on a new chain to test strategies and gain validation.

- Casualized/fragmented operations: (e.g., BAYC) For established IPs, games serve as tools to strengthen community cohesion and capture attention. Frequency and asset FOMO matter most—there’s no need to pursue AAA complexity or lengthy gameplay.

3. Leverage major traffic gateways to build products satisfying broader entertainment needs with sustainable business models—in other words, take existing entertainment demands and proven Web2 business models, distribute them via new traffic channels, and layer on Web3 incentives.

Telegram bots:

After Unibot’s rapid rise, many entrepreneurs rushed into cloning Telegram bots. Yet most only tweak trading bots or GPT-like assistants in minor ways. While trading bots gained traction by serving crypto traders’ needs, they suffer from单一business models, low ceilings for UI/UX and strategy optimization, and user bases under 10,000—far from true breakout scale. New TG bot founders must broaden their thinking, designing products aligned with mainstream consumer habits and establishing durable revenue models. One low-risk approach is porting proven Web2 models (e.g., gambling) onto new distribution channels (Telegram), enhanced with Web3 incentives (tokens + NFTs)—exemplified by Rollbit. Additional ideas include:

Examples:

Gaming: Consider tg bot gaming capabilities through the lens of WeChat mini-program evolution—from technical foundation to user education depth. Run frequent ad tests, aligning with key regional user distributions (India, Russia, Middle East, etc.) and game preferences to refine targeting. Hypothesis: tg’s broad user base accepts elemental games; breakout growth relies on social and viral mechanics, while crypto-native users prefer character-building and PvP card mechanics. [Basic elementals] – Match puzzles, Tetris. [Social party games] – Pictionary, Werewolf. [Competitive virals] – Jump, Sheep Game. [Idle card RPGs] – Top-ranked WeChat mini-games like *Xun Dao Da Qian*, *Lord of Saltfish*, etc.

Lottery: With increasing valuable assets—from consensus-backed blue-chip NFTs (BAYC/punk), IP collab items, to real-world assets like Pokémon cards being tokenized—combined with diverse lottery formats and reward-sharing mechanisms, there’s rich design space. [One-dollar raffles] – Pay $1 for a chance to win high-value items or NFT mystery boxes. [Game-based blind boxes] – Play tree-planting games to earn fruit mystery boxes; play NFT games to enter NFT draws. [Group discount buys] – Pool-buy fractionalized blue-chip NFTs, or launch a TG launchpad bot where sharing links reduces prices or grants lottery entries—replicating Discord whitelist-grinding dynamics.

Private community: Both above models involve TG group propagation and viral loops. Since TG’s content ecosystem is still nascent, teams can build private domains combining DAOs and creator economies before full content matrices form. [Link monetization] – Earn commissions whether posting in groups or channels, tracking view-click-download-share funnels, and directly rewarding users via wallet payouts. [Creator leaderboard bot] – Build voting bots within creator communities, publicly rank participants, and reward top performers with tokens.

4. Asset gamification + commercialization innovation still holds promise: The Treasure Pavilion

Background 1: Overall NFT market liquidity has dried up—new narratives and trading catalysts are needed.

Background 2: At the application layer, complexity of NFT-driven game assets has increased dramatically. Within single IPs, asset types multiply, interconnect, and ultimately derive value from the underlying product and token. Yet players still rely on off-platform community trades or manually hunt and purchase qualifying NFTs—one by one—an archaic process.

Background 3: At the protocol layer, with ERC-6551 and ERC-4337 emerging, although core wallet abstraction issues remain unresolved (e.g., stability with private-key wallets), infrastructure improvements are paving the way toward finer-grained accounts and assets. Just as ERC-721 and ERC-20 differ fundamentally in interaction and financial logic, future assets will likely be multi-agent, multi-layered, nested structures—harder to uniformly price. Financial interactions and use cases around such assets will become far more intriguing.

5. Fully on-chain games: Build outstanding open-source racetracks, not redundant wheels. Identify innovative mechanisms with strong wealth effects, productize and gamify them, then break out to attract external liquidity.

Background 1: The fully on-chain narrative inherited liquidity from NFTs and GameFi. Loot emerged alongside BAYC and Punk NFTs, peaking when Dark Forest—the pioneer of on-chain gaming—had its highest community participation. Fully on-chain gambling games (e.g., Wolf Game, Sunflower) followed Axie and the GameFi summer, yet all had FDVs below $5M—just 0.4% of Axie’s and 0.5% of STEPN’s peak valuations. This suggests that without sustained liquidity from NFTs or GameFi, breakout potential for social-betting on-chain games remains slim.

Background 2: To prevent fully on-chain games from devolving into raw PoS/PoW competitions and to improve UX, teams are diving deeper technically—building custom Appchains/L2s. These games often run in closed testnet environments with only dozens of testers, prone to reinvention without broad applicability. No notable open-sourcing exists yet—true permissionlessness and interoperability remain distant goals.

Analyzing three past innovations in fully on-chain games reveals common traits: 1) Innovation may not lie in main quests but side quests. Identifying valuable side mechanics, productizing them, and potentially building universal infrastructure—if further gamified and financially incentivized to lower barriers—can drive breakout adoption and new liquidity inflows. 2) Simple, FOMO-driven asset mechanics with clear wealth effects are more likely to spark widespread innovation: Examples include Fomo3D’s prize pool distribution and CryptoKitties’ breeding-induced deflation that increased asset value—both became excellent racetracks.

6. The AI agent era will still be ruled by traffic. Traffic-led + crypto agent combos will scale faster and achieve better monetization, while backend AI can continuously optimize, modularize, and seek partnerships with top-tier traffic gateways.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News