RWA in the Eyes of the Fed: Tokenization and Financial Stability

TechFlow Selected TechFlow Selected

RWA in the Eyes of the Fed: Tokenization and Financial Stability

This paper aims to provide background on asset tokenization and discuss the potential benefits as well as risks to financial stability.

In a Federal Reserve working paper on tokenization released on September 8, tokenization is described as a novel and rapidly growing financial innovation within the crypto market, analyzed from the perspectives of scale, benefits, and risks. The paper first introduces the concept of tokenization—the process of creating a digital representation (cryptographic token) of non-crypto assets (underlying assets). This process establishes a link between the crypto asset ecosystem and traditional financial systems. At sufficient scale, tokenized assets could transmit volatility risks from the crypto market to markets for traditional underlying assets.

Below is a compiled translation of this 29-page paper to help readers better understand RWA and tokenization, underlying assets and crypto assets, regulation, and financial stability. As one university president once said: "All financial technologies come with inherent risks; regulatory technology and the deep integration of RWA with DeFi will be a key focus area for future iterations of cryptographic technology development."

This follows previous translations of reports including Binance (Real-World Asset Tokenization: Bridging TradFi and DeFi), Citi (The Next Billion Users and Trillion-Dollar Value in Blockchain: Money, Tokens, and Gaming), and our own research report RWA Research Report: In-Depth Analysis of Current RWA Implementation Pathways and Outlook for Future RWA-Fi. Here is another RWA-focused research report—enjoy:

1. What Is Tokenization?

"Tokenization" refers to the process of linking the value of an underlying asset (reference asset) to the value of a cryptographic token. Strictly speaking, tokenization allows token holders legal rights over the underlying asset. To date, most tokenization projects have been initiated by small venture capital-backed crypto firms. However, traditional financial institutions such as Santander Bank, Franklin Templeton, and JPMorgan Chase have also announced pilot programs related to tokenizing assets using crypto technologies.

Like stablecoins, tokenization varies significantly depending on design choices. In general, tokenization typically includes five key features: (1) based on blockchain; (2) backed by underlying assets; (3) a mechanism to capture the value of the underlying asset; (4) a method for storing/safeguarding the asset; and (5) a redemption mechanism for tokens or underlying assets. Overall, tokenization connects the crypto market with markets for underlying assets. The design of tokenization schemes differentiates various tokens and affects traditional financial markets to varying degrees.

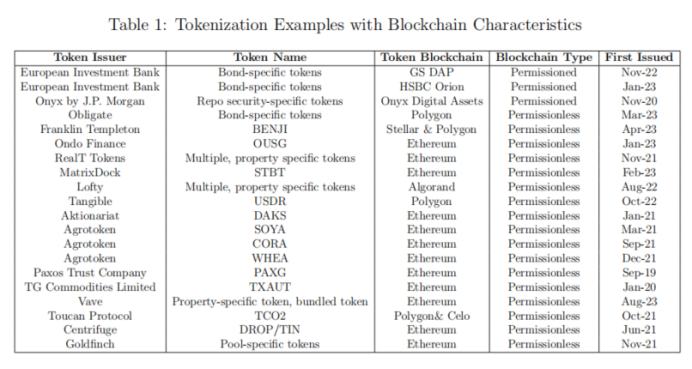

The first consideration in designing a tokenization scheme is the underlying blockchain used for issuing, storing, and trading tokens. Some projects issue tokens on permissioned private blockchains, while others use permissionless public blockchains. Permissioned blockchains are usually controlled by a centralized entity that approves selected participants into a private ecosystem. In contrast, tokens issued on permissionless blockchains (such as Bitcoin, Ethereum, Solana, etc.) allow broader public participation with fewer restrictions—but issuers have less control over the tokens. Tokens on permissionless blockchains can also integrate with decentralized finance (DeFi) protocols such as decentralized exchanges. Examples of projects issuing tokens on both types of blockchains are shown in Figure 1.

Another key factor is the nature of the underlying assets backing the tokens. Underlying assets can be categorized in multiple ways—for example, on-chain vs. off-chain, intangible vs. tangible. Off-chain underlying assets exist independently of the crypto market and can be tangible (such as real estate and commodities) or intangible (intellectual property and traditional financial securities). Tokenizing off-chain/underlying assets typically involves an off-chain intermediary, such as a bank, responsible for valuing the asset and providing custody services. On-chain/crypto asset tokenization requires smart contracts to manage custody and valuation of the crypto assets.

The final important consideration is the redemption mechanism. Similar to some stablecoins, issuers may allow token holders to redeem their tokens for the underlying assets. Such mechanisms connect the crypto market with markets for underlying assets. Additionally, tokenized assets can be traded on secondary markets such as centralized crypto exchanges and DeFi exchanges. While some security tokens representing other on-chain debts or equity stakes may not include redemption mechanisms, they still grant token holders certain rights—such as entitlement to cash flows associated with the underlying assets.

2. Current Scale of the Tokenization Market and Categories of Tokenized Assets

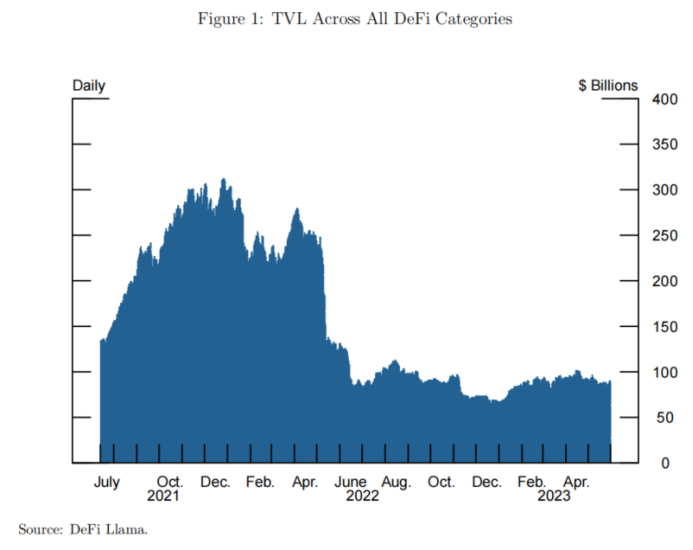

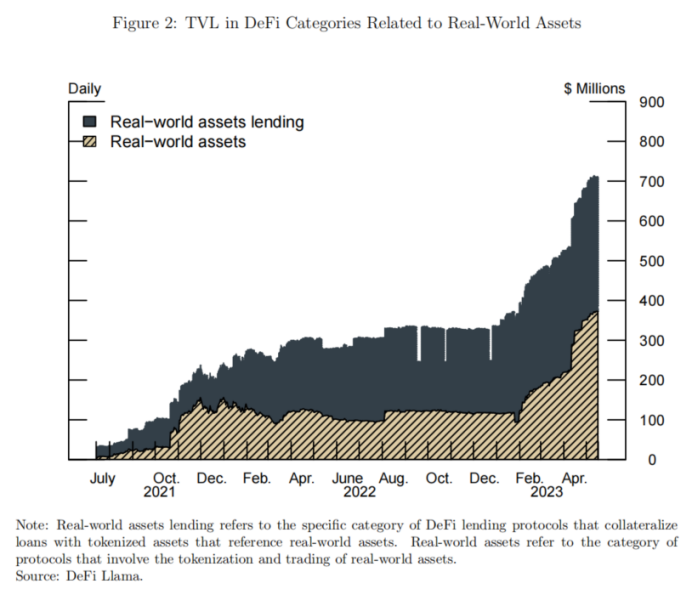

Based on publicly available information, we estimate that as of May 2023, the size of the tokenization market on permissionless blockchains was $2.15 billion. These assets are typically issued by DeFi protocols like Centrifuge and traditional finance companies like Paxos. Due to differences in tokenization designs and lack of standardized reporting, comprehensive data is difficult to obtain. Therefore, we use public data from DeFiLlama to illustrate the rapid growth of tokenization within DeFi. As shown in Table 1, the total value locked (TVL) in the overall DeFi market has remained relatively stable since June 2022. Meanwhile, Table 2 shows that since July 2021, the TVL of real-world assets (RWA) has consistently grown faster than other asset categories or the broader DeFi market. Many new tokenization projects have recently been announced, involving diverse underlying assets such as agricultural products, gold, precious metals, real estate, and other financial instruments.

A recent notable example involves agricultural commodities SOYA, CORA, and WHEA, which reference soybeans, corn, and wheat respectively. This project was launched in March 2022 by Santander Bank and crypto firm Agrotoken as a pilot program in Argentina. By embedding claims to the underlying assets into the tokens and building infrastructure to verify transactions and handle redemptions, Santander Bank can now accept these tokens as collateral for loans. Santander and Agrotoken stated their intention to expand this commodity tokenization model to larger markets such as Brazil and the United States.

Other common underlying assets for tokenization include gold and real estate. As of May 2023, the tokenized gold market was valued at approximately $1 billion. Two major players dominate 99% of this market: Pax Gold (PAXG), issued by Paxos Trust Company, and Tether Gold (XAUt), issued by TG Commodities Limited. Both issuers peg one token unit to one troy ounce of gold stored according to standards set by the London Bullion Market Association (LBMA). PAXG can be redeemed for its USD equivalent, while XAUt is redeemed through the issuer selling gold on the Swiss market. Overall, both models are functionally similar, with values tracking gold futures.

Compared to agricultural goods and gold, real estate poses greater challenges due to difficulties in standardization, low liquidity, complex valuation, and complicated legal and tax implications. Real Token Inc. (RealT) is a project that tokenizes ownership rights of residential properties. Each property is held by a separate limited liability company (LLC), and it's the shares of the LLC—not the physical property—that are tokenized, enabling fractional ownership among different investors. The project primarily targets international investors seeking exposure to U.S. real estate, offering rental income as returns. As of September 2022, RealT had tokenized 970 properties with a total value of $52 million.

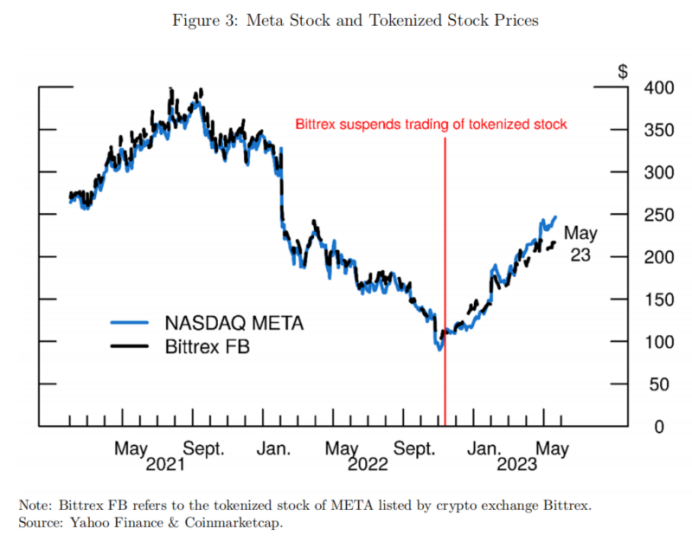

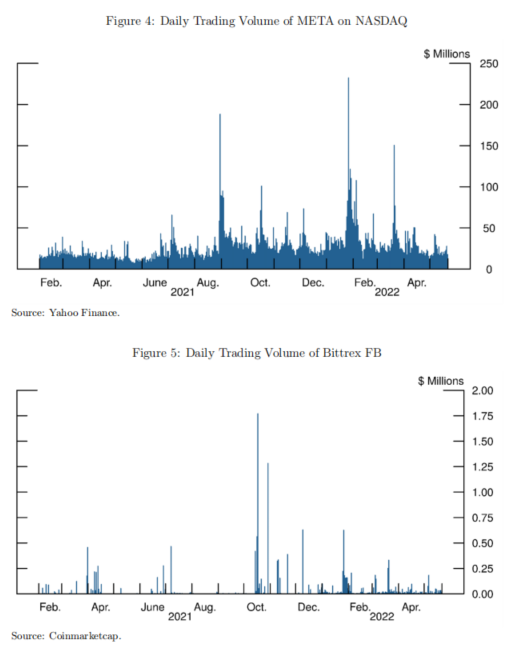

Tokenization of financial assets includes securities, bonds, and ETFs as underlying assets. Unlike direct ownership of securities, the prices of tokenized securities may differ from those of the original securities—partly because tokens trade 24/7, and partly due to programmability and composability with DeFi, which can create unique liquidity dynamics. Tables 3, 4, and 5 illustrate price and trading volume differences between the stock META and its corresponding token MEAT (based on Bittrex FB).

Traditional compliant exchange-listed securities can be tokenized, or tokens can be directly issued on blockchains. Akoinariat, based in Switzerland, provides tokenization services for Swiss companies. U.S.-listed stocks such as Amazon (AMZN), Tesla (TSLA), and Apple (AAPL) have been or currently are available as tokenized securities on platforms like Bittrex and FTX.

Earlier in 2023, Ondo Finance issued tokenized funds whose underlying assets are ETFs of U.S. Treasuries and corporate bonds. Shares of these tokenized funds represent proportional ownership in the respective ETFs. Ondo Finance also holds a small amount of stablecoins as liquidity reserves. Ondo Finance manages the fund, Clear Street acts as broker and custodian, and Coinbase serves as stablecoin custodian.

3. Potential Benefits of Tokenization

Tokenization offers numerous benefits, including enabling investor access to previously high-barrier or inaccessible markets. For instance, tokenized real estate allows investors to purchase fractional shares in specific commercial buildings or homes—offering more granularity than real estate investment trusts (REITs), which bundle multiple properties.

The programmability of tokens and use of smart contracts allow additional functionalities to be embedded, potentially benefiting the underlying asset markets. For example, liquidity-saving mechanisms can be applied during token settlement—features that are difficult to implement in traditional systems. These blockchain-native characteristics may lower entry barriers for retail investors, enhancing market competitiveness, liquidity, and price discovery.

Tokenization may also facilitate lending by allowing tokens to serve as collateral—as discussed earlier with tokenized agricultural commodities, where using physical crops as collateral would otherwise be costly or impractical. Moreover, settlement of tokenized assets is more efficient compared to real-world underlying or financial assets. Traditional securities settlement systems like Fedwire Securities Services and the Depository Trust and Clearing Corporation (DTCC) typically settle trades in gross or net amounts, usually one business day after the transaction.

ETFs are the closest existing analog to tokenized assets, and empirical evidence suggests tokenization could similarly improve liquidity in underlying asset markets. Academic literature on ETFs demonstrates a strong positive correlation between ETF trading activity and liquidity of underlying assets, showing that increased ETF trading enhances information flow about the underlying holdings. For tokenized assets, similar mechanisms imply that higher liquidity in crypto markets could benefit price discovery for underlying assets.

4. Implications of Tokenization for Financial Stability

Given its current size—under $1 billion—the tokenization market remains small relative to both the broader crypto market and traditional financial systems, posing no systemic financial stability concerns at present. However, if the tokenization market continues to grow in scale and volume, it could introduce financial stability risks to both crypto and traditional financial systems.

In the long term, the redemption mechanisms linking the crypto asset ecosystem with traditional financial systems—central to many tokenization models—could pose potential financial stability implications. For example, at sufficient scale, a sudden sell-off of tokenized assets could impact traditional financial markets, especially if price discrepancies in crypto markets create arbitrage opportunities for redeeming underlying assets. Thus, mechanisms may be needed to manage value transmission across these two markets.

Additionally, illiquidity of underlying assets may pose challenges for tokenized assets—particularly those backed by real estate or other less liquid assets. This issue is well-documented in ETF literature, which shows strong relationships between the liquidity of underlying assets and the liquidity, price discovery, and volatility of ETFs.

Another financial stability risk lies with the issuers of tokenized assets themselves. Tokenized assets with redemption options may face issues similar to asset-backed stablecoins like Tether. Any uncertainty regarding the underlying assets—especially due to insufficient disclosure or information asymmetry—could incentivize investors to redeem en masse, triggering fire sales of tokenized assets.

Such liquidity shocks could be exacerbated by structural features of crypto markets. Crypto exchanges enable 24/7 trading, whereas most underlying asset markets operate only during business hours. This mismatch in trading times could create unpredictable pressures during critical events.

For example, issuers of redeemable tokenized assets might face sell-offs over weekends when underlying assets are held off-chain and traditional markets are closed, preventing timely redemptions. This situation could worsen if declining token values threaten the solvency of institutions holding large positions on their balance sheets. Even if institutions can access liquidity from traditional markets, they cannot inject it during market closure periods.

Consequently, large-scale sell-offs of tokenized assets could rapidly erode the market value of holding institutions and issuers, impairing their borrowing capacity and ultimately threatening their ability to meet obligations. Another risk arises from automated margin-top-up mechanisms on DeFi exchanges, which may trigger forced liquidations or token swaps, creating unpredictable spillovers into underlying asset markets.

As tokenization technology and markets evolve, tokenized assets themselves could become underlying assets. Given that crypto asset prices tend to be more volatile than their real-world counterparts, price swings in such tokenized assets could spill over into traditional financial markets.

As the tokenized asset market grows, traditional financial institutions may participate directly—either by holding tokenized assets or accepting them as collateral. Examples include Santander Bank accepting tokenized agricultural commodities as loan collateral for farmers. Similarly, we see cases like Ondo Finance tokenizing U.S. government money market funds.

Although conceptually similar to JPMorgan’s initial use of money market fund (MMF) shares as collateral for repo and securities lending transactions, Ondo Finance’s approach could have broader implications. Ondo Finance deploys its tokens on the public Ethereum blockchain rather than a private, permissioned chain operated by a single institution, meaning it cannot control how users or DeFi protocols interact with its tokens. As of May 2023, Ondo Finance’s tokenized funds accounted for 32% of the entire tokenized asset market. According to DeFiLlama, Ondo Finance is the largest player in this category, and its token OUSG is accepted as collateral on the nineteenth-largest lending protocol, Flux Finance.

Finally, similar to the role of securitization, tokenization may package risky or illiquid underlying assets as safe and tradable instruments, potentially increasing leverage and risk-taking. Once risks materialize, such assets could trigger systemic events.

5. Conclusion

This paper aims to provide background on asset tokenization and discuss its potential benefits and financial stability risks. Currently, the scale of asset tokenization is very small. However, numerous projects involving diverse types of underlying assets are under development, suggesting tokenization may play a larger role in the crypto ecosystem in the future. Among its benefits, the most significant are lowering barriers to previously inaccessible markets and improving market liquidity. The primary financial stability risks stem from the interconnections created between the crypto ecosystem and traditional financial systems, which may transmit risks from one financial system to another.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News