How to use friend.tech to create a Ponzi?

TechFlow Selected TechFlow Selected

How to use friend.tech to create a Ponzi?

For a social product to sustain long-term existence, it must give users a reason to remain trapped within its system.

Before getting into specific operations, let's first review how the (3,3) and ve(3,3) flywheels used in large-scale Ponzi schemes actually take off:

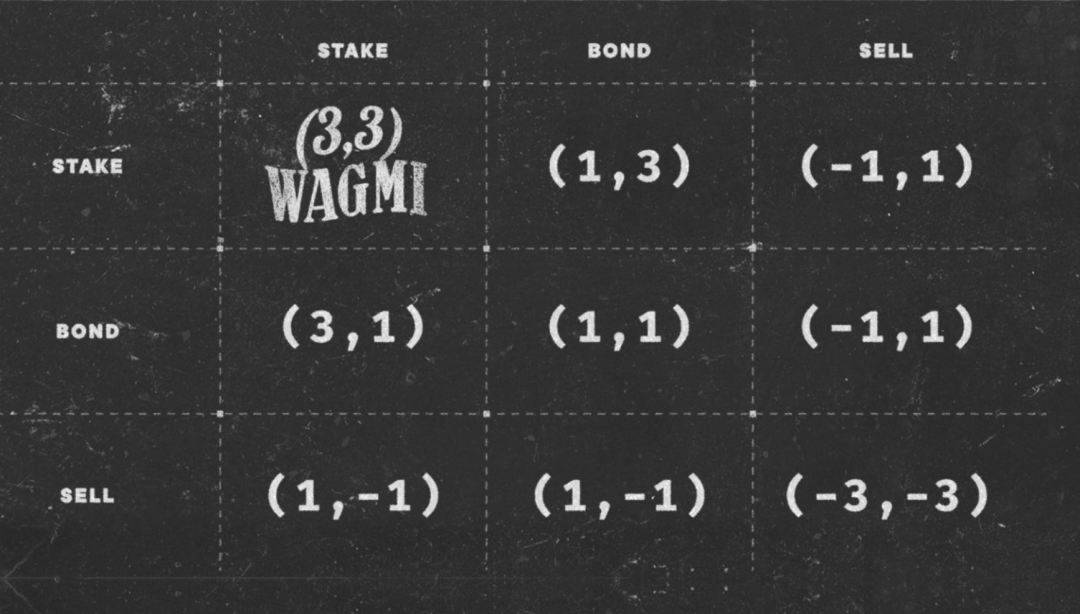

First, (3,3): OHM employs a classic case from game theory—The Prisoner’s Dilemma—a type of non-zero-sum game. Simply put, when users all choose (stake, stake) or (bond, bond), the bubble grows larger and larger.

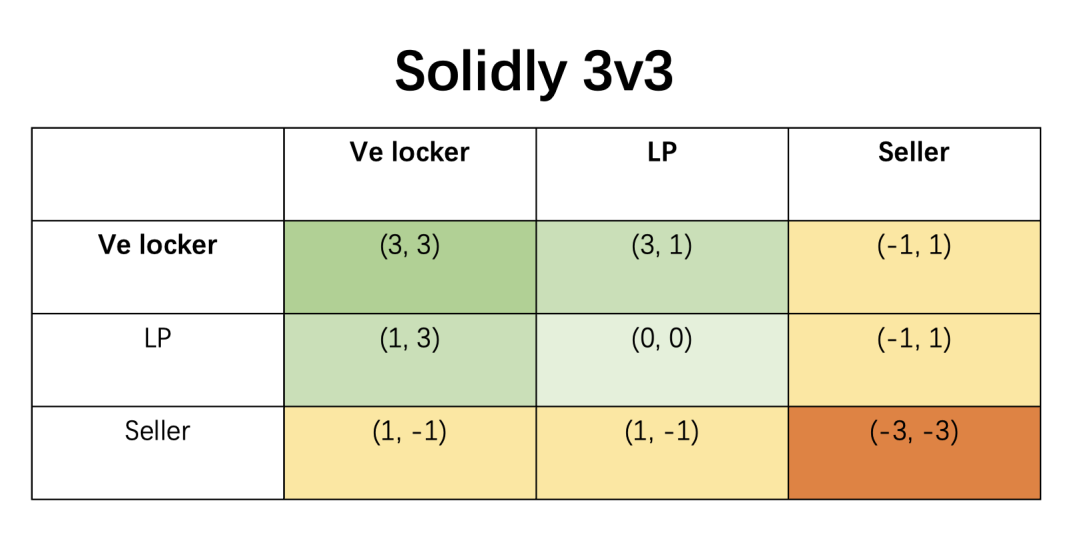

Next is ve(3,3), which combines Curve’s ve (vote escrow) model with OlympusDAO’s (3,3) model. "ve" means that after users lock up their CRV tokens, they can receive benefits such as a share of Curve’s trading fees, boosted LP yields, voting rights for projects, and airdrops from partner protocols. ve(3,3) adjusts token issuance based on the amount of tokens locked, encouraging collective locking to prevent token value dilution (note: founder AC has already exited).

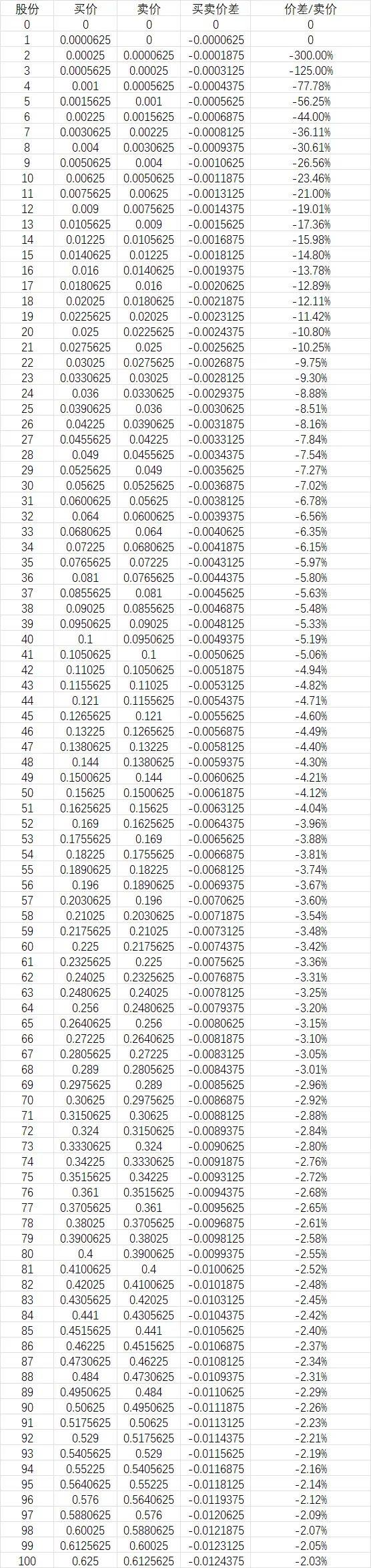

Now let’s turn to Friend Tech’s economic model. The stock pricing formula is: price per share (in ETH) = (supply²) / 16000.

To briefly explain this formula: the square of the total supply represents the KOL’s market cap. For example, if you have 10 holders, your market cap is 100. Divided by 16000, the price of one Key becomes 0.00625 ETH.

We can see this is a classic prisoner’s dilemma problem.

As the number of buyers increases exponentially, when the 10th person buys in, the first buyer profits 100x. When the 100th person buys in, the 10th buyer also profits 100x.

There is always a spread between buy and sell prices, given by (2n + 1)/16000. This equation shows that as n increases, the spread increases linearly—by 2/16000 (i.e., 0.000125) for each unit increase in n.

Therefore, selling is a typical weak equilibrium behavior (-3,-3).

With these two models as our starting point, let’s discuss how a Friend Tech influencer can transform themselves into a Ponzi-like model?

In fact, the core of a Ponzi scheme revolves around just a few key elements:

1. Use game theory to convince holders not to sell, incentivize users while discouraging them from cashing out rewards. Find ways to lock up holdings or delay selling, keeping users trapped within the system and reducing sell pressure.

2. Aggressively build hype and expand influence through word-of-mouth CX models to achieve early network effects, continuously attracting new members and external capital.

3. Generate income and cash flows to provide user incentives, creating positive externalities.

I’ve always said not to look down on Ponzis—ideally, they can result in win-win outcomes, i.e., Nash Equilibrium—provided the rate of gaining positive externalities keeps pace with slowing user acquisition.

This is how the FT group is designed:

1. Establish rules, incentive mechanisms, and a tiered system:

a. Users must purchase the KOL’s Key to join the group. Upon entry, they leave their Twitter handle, self-introduction, what value they bring to the community, and pledge never to sell—committing to stay and become “family.” The KOL then replies to the user, making their message visible to all, prompting other “family” members to follow their Twitter or buy their Key.

b. Design incentive mechanisms so users gain more benefits as long as they don’t leave, such as: 1) gaining attention from other group members, enabling self-promotion and social value; 2) access to high-quality alpha information within the group; 3) leveling up within the group, collaborating with the community to secure whitelist spots, airdrops, ads, and other perks.

c. Implement a tiered system to build community identity.

Regularly elect community managers, appointing 10% of members as admins responsible for enlivening discussions, organizing events, and recruiting new members.

The group owner shares part of the transaction fees with a select few to create competition.

Ensure everyone feels valued—for example, highlight top daily contributions from members, publish them externally, attract new members, and distribute profits collectively.

d. Inviting others unlocks new privileges.

2. Establish penalty mechanisms beyond the 0.000125 fee:

a. Sellers will be publicly shamed—everyone unfollows them and tweets “shame on you” on Twitter.

b. Every time someone exits, the group owner uses fees to buy back Keys, urging members to collectively purchase and push the price higher via (3,3), making it costlier for sellers to re-enter.

3. Build a ve-model for the community to generate external revenue and distribute dividends

a. Once the community scales, host AMAs with project teams.

b. Vote to decide the future direction of community profits.

c. Moral locking: each user commits not to sell before a certain date.

d. Use transaction fees for buybacks.

Mechanistically, I’d love to tweak that denominator 16000—if more members choose to lock up, the divisor 16000 could shrink. (Just a small idea—I’m not sure what would happen.)

Based on this model, we arrive at a payoff matrix for a Friend Tech version:

In this matrix, if all users choose not to sell, the community thrives and each gains exponential returns—that is, (+3,+3). Selling incurs a penalty equal to the 0.000125 price spread.

I’ve seen many criticize FT for lacking a social graph or content, being nothing but a Ponzi. Yet the short-lived rise of Facebook’s Threads and Nostr/Damus proves one thing: short-term traffic surges alone cannot sustain a social product.

What is the fundamental reason a social product can survive long-term?

It’s giving users a reason to be trapped within your system.

The core method of trapping users is increasing the efficiency of building valuable relationships.

For example, Taobao—the social app—connects merchants and users.

What are users seeking inside Friend Tech? Beyond airdrop expectations, I believe it’s the opportunity to interact with top-tier users. This mirrors the essence of premium communities, MBA programs, or paid groups: “I have the people you want to meet. Pay me, and you can talk directly with top KOLs—and the later you come, the more expensive it gets.”

Put yourself in their shoes—wouldn’t you FOMO in? After all, attending Token2049 in Singapore costs thousands of dollars in travel. A fraction of an ETH? Definitely worth it.

How do you achieve early traction for a social product? Who says using a Ponzi mechanism isn’t a valid approach?

Of course, I also believe Friend Tech has clear design flaws:

1. Selling out is too easy. Once prices rise and buying demand drops, subsequent sell pressure becomes uncontrollable.

2. Others cannot see a user’s messages unless the KOL replies. This diminishes individual presence, reduces stickiness, and makes user tiering nearly impossible. It turns the KOL into a single super-node facing hundreds of users. Beyond 100 members, the KOL becomes overwhelmed. Without decentralized user management, the group collapses. Proven social platforms rely on top users driving traffic and mid-tier users engaging socially—yet Friend Tech operates as one-to-many, silencing ordinary users and hindering sustained growth.

3. Functionality is too limited—no way to preserve valuable content, nor extend to features like红包(red packets), voting, or greetings.

4. Due to functional and product shortcomings compared to traditional social media, it struggles to attract non-crypto degens, leading to weak subsequent growth and difficulty sustaining narratives.

So currently, it's only sustained by token launch expectations. I don’t think there’s any strong incentive mechanism post-token launch unless it evolves into something like Curve.

Urgent issues needing resolution now:

1. Add a locking feature: users who lock their Keys can speak freely in the group without requiring a reply from the KOL.

2. Grant corresponding privileges based on lock-up duration, unlocking additional features.

3. Expand to multi-chain ecosystems—not relying solely on ETH payments, but supporting other cryptocurrencies, or even adopting traditional knowledge-platform models, running ads, and drawing in external funding. Of course, from Base chain and ETH interests’ perspective, this may not be a high priority.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News