Deep Dive into Coinbase's Investment Logic and Growth Potential

TechFlow Selected TechFlow Selected

Deep Dive into Coinbase's Investment Logic and Growth Potential

Coinbase's profitability will remain suppressed over the next 12 months, but its revenue and profit growth potential will be unlocked within 24 months.

I. Investment Thesis

1. Asset Class - Compliant U.S. Equity Exposure to the Crypto Market

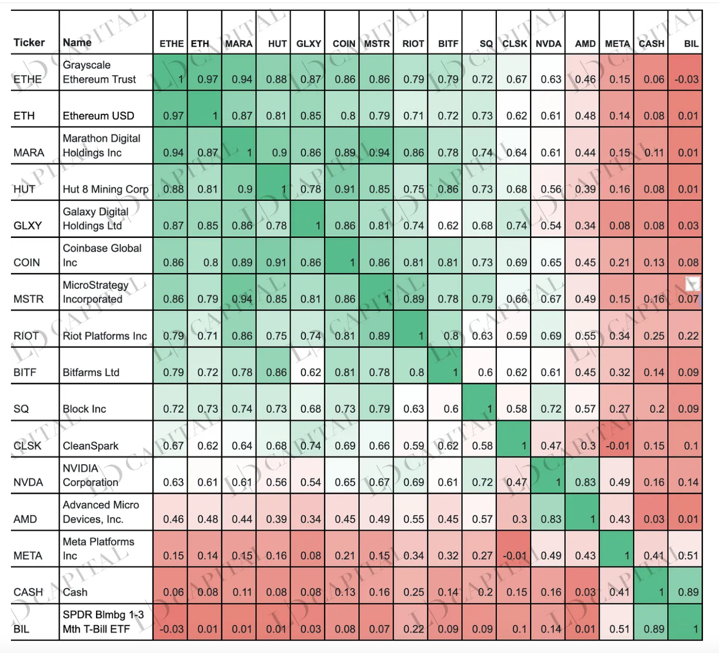

Coinbase stock has risen over 120% this year, driven by Bitcoin's 65% gain since the beginning of the year and a 35% boost from broader tech stocks. Its dual correlation with both the U.S. equity market and the crypto market enables it to outperform both during upward trends.

The chart below shows the correlation between COIN and ETH, along with other related assets (MARA, HUT, GLXT, COIN, MSTR), all of which closely track ETH’s movements.

Source: LD Capital

2. Core Business Growth Potential Not Yet Realized

Coinbase’s primary revenue source is transaction fees, which are cyclical and sensitive to macroeconomic and industry conditions. The halving event may drive speculative activity and increase trading volume. However, for the next 8–12 months, the continuation of a macro environment characterized by high inflation and high interest rates—unfavorable for crypto growth—will likely continue to negatively impact Coinbase’s core business.

For Coinbase, which went public in May 2021 just before entering a bear market, growth remains the key driver of its stock price. Coinbase International and its derivatives trading platform were only officially launched in May this year. The international platform will generate additional spot trading volume, while the derivatives business will significantly boost transaction revenues. On August 14, Coinbase announced its official entry into Canada, launching services with Interac payment rails, partner integrations, fund transfers, and Coinbase One. This highlights Coinbase’s strong focus on growth through geographic and product expansion. While external constraints may limit business growth over the next 12 months, multiple unpriced catalysts suggest substantial revenue growth potential within the next 24 months.

3. First-Half EBITDA Significantly Exceeded Expectations, Potentially Priced In Future Profitability

Coinbase achieved $194 million in adjusted EBITDA in Q2 2023, significantly exceeding expectations. This was primarily due to cost-cutting measures initiated a year earlier, resulting in nearly a 50% year-over-year reduction in operating expenses. Given ongoing macro headwinds, a deep crypto winter, and increasing regulatory pressures, this non-organic cost reduction may have front-loaded profitability, leaving limited room for earnings growth in the next two quarters. Profitability expectations for the second half of the year and into next year remain weak.

4. Expansion of Ancillary Businesses Creates New Growth Engines

• International and Derivatives Trading – Coinbase’s derivatives exchange is still in early stages, currently serving around 50 institutions with $5.5 billion in contract value. Q2 mainly involved launching an API test version with only a small number of clients. Next steps include integrating derivatives into the retail app. The official launch of international and derivatives products will drive material revenue growth.

• USDC Business – Coinbase is acquiring a minority stake in Circle, though specific investment details were not disclosed. This strategic alignment strengthens the partnership between Coinbase and Circle in shaping the future financial system. It signals a broader development path for USDC, potentially expanding beyond crypto trading into foreign exchange and cross-border payments. Coinbase executives downplayed competition from PayPal’s stablecoin (PYUSD, with only $44 million supply and minimal market share). Coinbase and Circle will continue to earn interest income from USDC reserves, which will be shared based on the amount of USDC held on each platform. They will also equally share interest income generated from broader USDC distribution and usage.

• On-chain Revenue Streams – Base’s launch generates direct MEV (Maximal Extractable Value) revenue for Coinbase as the sole sequencer. Beyond direct profits, Coinbase CFO Alesia noted during the earnings call that Base adoption could drive usage of other Coinbase products such as payment channels and wallets, creating ancillary revenue. Additionally, ETH staking contributes at least $100 million in annual revenue.

5. Coinbase Likely to Capture More of Binance’s Market Share, Becoming the Leading Exchange

SEC allegations against Binance are more severe than those against Coinbase. In addition to charges of operating an unregistered securities exchange, broker, and clearing agency, Binance is also accused of activities similar to FTX: fraud, commingling of funds across entities, and acting as a counterparty to customer trades. The SEC has not brought similar accusations against Coinbase. Binance’s global crackdown presents a significant opportunity for Coinbase, positioning it to potentially replace Binance as the most influential cryptocurrency exchange.

6. Regulatory Compliance Positions Coinbase as a Major Beneficiary of Spot ETF Approvals

If traditional asset managers receive approval for spot Bitcoin ETFs, Coinbase stands to benefit significantly as a potential custodian. It would earn primary revenue from AUCC (average annual custody costs) associated with holding newly launched spot ETFs. Additional income could come from settlement, clearing, and other services. However, many regulatory and operational hurdles remain, indicating a long timeline ahead.

7. Regulatory Pressure Increases Compliance Costs

Despite Coinbase’s strong performance during the ongoing crypto winter, persistent regulatory uncertainty remains a foundational risk. Coinbase is seeking to dismiss the SEC lawsuit filed in June, accusing the company of operating an unregistered exchange, broker, and clearing agency. The SEC is unlikely to win outright; a settlement is more probable, but any penalty (e.g., Kraken’s $30 million fine) would significantly impact profitability. Such an outcome could hurt fundamentals but might be interpreted positively by markets.

Expanding into banking-like services such as deposit or wealth management products may require licenses from U.S. regulators like the Federal Reserve, FDIC, OCC, or state banking authorities, as well as equivalent bodies abroad. This increases operating expenses (compliance costs) and exposes the company to fines or shutdowns if licenses are not obtained. Divergent global regulations further constrain international expansion.

In summary, we believe Coinbase’s profitability will remain suppressed over the next 12 months, but its revenue and earnings growth potential will materialize within 24 months. Key upside not yet priced in includes: 1) Substantial revenue growth following the official rollout of international and derivatives products; 2) Continued growth in staking revenue, including sequencing income from Base (and other chains), staking fees, and increased use of Coinbase’s other products (wallets, etc.) by on-chain users; 3) Recovery in USDC scale driving higher reserve interest income and fee revenue from wider distribution. However, due to its strong correlation with crypto markets, core transaction revenue is unlikely to see significant growth in the next 8–12 months under continued macro headwinds. In the next bull cycle, however, growth could surpass the 515% surge seen in 2021.

Valuation suggests a fair value of $89 in the base case, implying the current price of $74 is undervalued by 16%. However, given the DCF model’s high sensitivity to projected business growth and terminal EV/EBITDA multiples, the short-term stock price faces downward pressure due to the dual bearish environment in both U.S. equities and crypto markets. A practical strategy is to sell over the next 12 months and buy into the 24-month cycle, with a fair value of $89 at 7x EV/EBITDA and $170 at 14x.

II. Company Background and Business Overview

Founded in 2012, Coinbase operates a diversified cryptocurrency business and is the largest digital asset exchange in the United States, serving over 108 million customers. Users can buy, sell, and trade cryptocurrencies on its platform. On April 14, 2021, Coinbase successfully listed on Nasdaq, becoming the “first crypto stock.”

In Q2 2023, transaction revenue reached $327 million, accounting for about half of net revenue and representing its core business. Coinbase also earned over $200 million from interest income via its partnership with USDC, the second-largest stablecoin. While still a smaller segment, this is viewed as a key driver for expanding ancillary revenue. Other offerings include cloud infrastructure and high-yield “staking” products.

By business line:

1) Coinbase App – For Retail Traders

Users can trade tokens on the platform. Revenue comes from two main models: First, transparent pricing plans where users pay transaction fees added to trades when buying, selling, or converting crypto using fiat-to-crypto or crypto-to-crypto pairs. Fees are based on a percentage of trading volume (except small transactions, which have flat fees); advanced traders face tiered pricing. Second, through the subscription product Coinbase One, users pay a monthly fee instead of per-trade fees up to a certain threshold. However, spreads still apply to simple trades.

The Coinbase app offers expanded proprietary experiences, enabling peer-to-peer payments, remittances, direct deposits, and spending via the Coinbase Card (a branded debit card). Users can also earn yield on crypto through staking rewards, DeFi yields, and other asset-specific methods.

Staking crypto independently poses technical challenges, requiring users to run their own hardware and software with near-100% uptime. Coinbase provides true on-chain proof-of-stake services, simplifying the process so users can earn staking rewards while retaining full ownership of their assets. In return, Coinbase collects a commission on all staking rewards. Recently, its Cloud product integrated Kiln, enabling Ethereum staking with less than the standard 32 ETH requirement.

2) Two Wallet Products

Web3 Wallet

Consumers access third-party products by adding a “web3 wallet” within the Coinbase app. This allows interaction with certain dApps, such as trading on decentralized exchanges or accessing art and entertainment platforms. The product enhances convenience and enables shared responsibility for securing private keys, making wallet recovery possible. Coinbase monetizes by charging fees on certain dApp transactions, such as trades on decentralized exchanges.

Coinbase Wallet

Coinbase offers a standalone software product called Coinbase Wallet to consumers in over 100 markets, enabling direct interaction with dApps and crypto use cases without central intermediaries. While similar to Web3 Wallet, key differences include full user control over private keys and seed phrases, and broader support for web3 assets and use cases. Revenue is generated from select dApp transactions, such as fiat-to-crypto trades or trades on decentralized exchanges.

3) Institutional Services

Coinbase offers two institutional-facing products serving various clients, including market makers, asset managers, hedge funds, banks, wealth platforms, RIAs, payment providers, and public/private companies.

Coinbase Prime is a comprehensive platform fulfilling all institutional spot crypto needs on an agency basis. It provides trading, storage, transfers, staking, and financing services. Through Coinbase Prime, institutions access deep liquidity pools and optimal execution prices enabled by connections across multiple venues, including Coinbase Spot Market. Pricing is volume-based, with fees charged on each matched trade.

It also provides market infrastructure via Coinbase Spot Market and Coinbase Derivatives Exchange.

Coinbase launched the first regulated derivative products—Nano Bitcoin Futures and Nano Ethereum Futures contracts—on its Derivatives Exchange. It became the first crypto-native platform recognized in a regulated derivatives market. It enables other derivatives intermediaries to trade on its exchange. Once regulatory approval is granted, Coinbase plans to offer these derivative products directly to retail customers (currently available only to institutions).

4) Developer Suite

The developer suite includes recent products such as Coinbase Cloud and Coinbase Pay.

Coinbase Cloud offers APIs for crypto payments/trading, data access, and staking infrastructure. These tools enable faster development of crypto products and simplify blockchain interactions. Coinbase Pay and Coinbase Commerce allow developers and merchants to easily integrate crypto transactions into their products and businesses.

III. Financial Analysis

1. Business Model and Revenue Growth

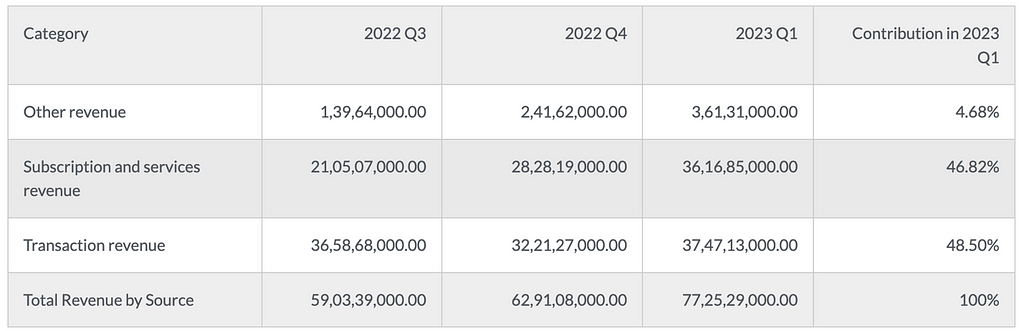

Breaking down revenue streams, transaction revenue remains the dominant source. Ancillary businesses grow alongside transaction volume. Transaction revenue accounted for 61% and 52% of total revenue in Q3 and Q4 2022, respectively, and 48% in Q1 2023. Subscription and service revenues have become increasingly meaningful and show a rising trend.

Transaction revenue surges explosively during bull markets and declines in bear markets, while subscription and service revenues remain stable or grow during downturns and expand further during bull cycles.

Revenue by Segment

Source: https://businessquant.com/coinbase-revenue-by-segment

Transaction Revenue is Coinbase’s primary income stream, including trading fees: Coinbase earns money from buying and selling crypto, typically a percentage of transaction value or fixed amounts. Spreads: the difference between buy and sell prices. Conversion fees: charged when converting one cryptocurrency to another. OTC services: cater to institutional buyers, large trades, or high-volume traders. Leveraged trading: allows borrowing funds; revenue comes from interest and loan fees. Payment processing fees: charged when users make payments via crypto on the platform.

Total transaction revenue was $375 million in Q1 2023, compared to $322 million in Q4 2022 and $366 million in Q3 2022, accounting for 48.5% of total revenue.

Subscription and Service Revenue

Coinbase offers subscription services including Coinbase Pro, Coinbase Prime, and Coinbase Custody.

Coinbase Pro is an advanced trading platform for professional and institutional investors, offering free features and premium subscriptions. Coinbase Prime is tailored for institutions, providing enhanced trading capabilities, dedicated account management, and liquidity solutions. Coinbase Securities typically offers secure custody for institutions, including insurance coverage for digital assets.

Subscription and service revenue reached $210 million in Q3 2023, up from $283 million in Q3 2022 and $240 million in Q4 2022, hitting a record $362 million in Q1 2023, representing 46.82% of total revenue.

Other Revenue

Other revenue sources include Coinbase Commerce, Coinbase Cards, interest income, institutional services, and other products.

Other revenue accounts for approximately 4.5% of total revenue—$14 million in Q3 2022, rising to $24 million in Q4 2022. In Q1 2023, it tripled compared to Q3 2022.

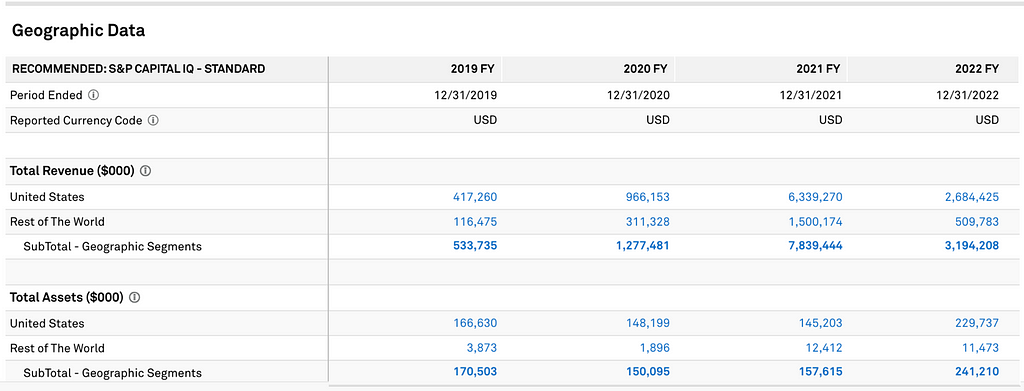

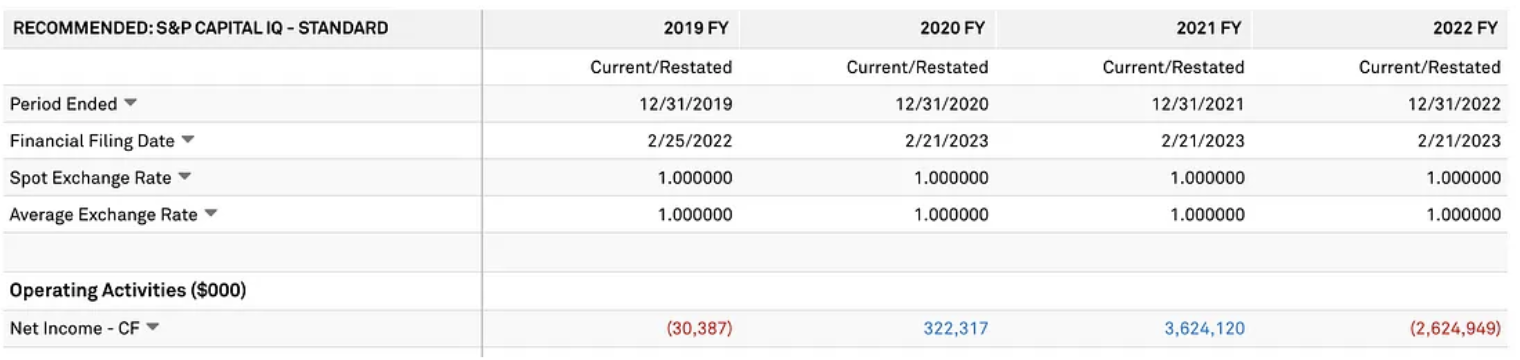

Geographic Revenue: Although Coinbase serves over 100 countries, the U.S. accounts for about 40%, followed by the UK/Europe at 25%. However, U.S. revenue represented 78%, 76%, 81%, and 84% of total revenue from FY2019 to FY2022, far exceeding other regions. In August, Coinbase announced its entry into Canada, but growth elsewhere is constrained by local regulations and competition from domestic exchanges.

Source: Capital IQ

2. Profit Breakdown

Coinbase has very high overall margins—a hallmark of SaaS companies—with a 46% margin in 2021.

Profits primarily stem from transaction and subscription revenues. MEV income from staking and USDC-related income are reflected in “other revenue,” with staking generating $100 million and USDC $200 million. Debt repurchases reduced interest expenses ($5.4 million), slightly boosting net margins, though the impact is minor.

Source: Capital IQ

Staking and Base MEV Revenue

As the sole sequencer on Base, Coinbase captures all MEV profits from transaction ordering.

Using L2 Revenue = L2 Fees – L1 Data Storage Costs – L1 Validation Costs

Estimating sequencing revenue from Base’s cumulative fees, roughly half of $546k minus $354k could go to Coinbase (~$100k), though actual income comes from 25%-35% commissions on staked ETH.

Source: Dune

Base contributes ~$100k to Coinbase (even lower in absolute terms). Coinbase leads all CEXs in staked ETH (8.6% market share), ranking second behind Lido. With $300 million in realized ETH staking revenue, Coinbase takes a 25%-35% cut—approximately $100 million in staking revenue.

Source: Dune

Coinbase maintains EBITDA at around 40% of revenue. This ratio may decline when core revenue stagnates due to cycles and regulation, or when external costs rise. It should expand as bull markets resume.

USDC Business

Coinbase holds 232 million USDC, second only to Binance. Despite USDC redemptions due to SVB’s collapse and Binance swapping USDC for other stablecoins, CEO Brian Armstrong noted on the earnings call that USDC has seen net market cap growth over the past 6–7 weeks—an important signal. He acknowledged heightened U.S. regulatory risks, with USDC perceived as more U.S.-linked than Tether, potentially posing near-term challenges.

Source: Dune Analytics

Circle generated $779 million in revenue in H1 2023, already surpassing its full-year 2022 revenue of $772 million. It posted $219 million in EBITDA, exceeding last year’s full-year $150 million. However, USDC’s market cap declined, now holding only 21% of the stablecoin market—likely why Circle brought in Coinbase as an investor and plans to launch USDC on six new blockchains between September and October to halt further share loss. Clearly, Coinbase values the stablecoin business and aims to capture maximum revenue from it.

3. Cost Structure

In January 2023, the company completed a restructuring affecting approximately 21% of its workforce as of December 31, 2022 (“2023 Restructuring”). Aimed at managing operating expenses amid adverse crypto market conditions and shifting priorities, the move led to the termination of about 950 employees across departments and locations, who received severance and other benefits.

Cash payments related to the restructuring were largely completed in Q2 2023, with the remainder expected by December 31, 2023. The 50% reduction in operating expenses due to lower labor costs explains why Coinbase posted positive and significantly above-consensus EBITDA in both Q1 and Q2 2023.

On March 3, 2023, the company acquired One River Digital Asset Management, LLC (ORDAM), purchasing all issued and outstanding membership interests. ORDAM is an institutional digital asset manager registered with the SEC. The acquisition aligns with Coinbase’s long-term strategy, enhancing institutional access to the crypto economy. Total consideration paid was $96.8 million.

Source: Capital IQ

4. Debt and Financing Costs

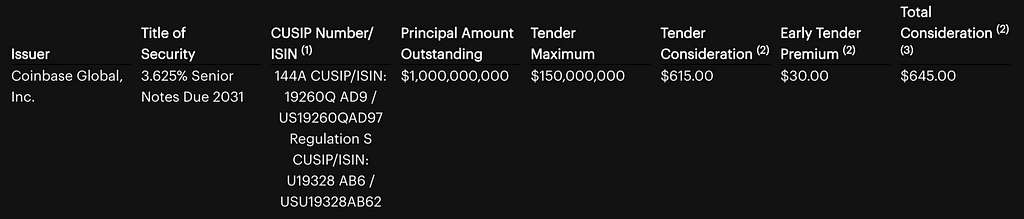

On August 7, 2023, Coinbase announced a cash tender offer to purchase up to $150 million of its senior unsecured notes maturing in 2031—at a price of 64.5 cents per dollar (before August 18) or 61.5 cents (after August 18 but before the September 1 expiration). Funding will come from operating cash flow. This follows a June 2023 repurchase of $645 million in 0.5% convertible senior notes due in 2026 at a 29% discount, costing ~$45.5 million in cash. Given Coinbase’s strong liquidity and no near-term refinancing risk, the transaction is favorable and poses no cash crisis. It will further increase excess cash reserves against debt and reduce annual interest expenses by ~$5.4 million.

Theoretically, proactive tender offers to retire future debt reduce interest burdens and improve financial stability. Stronger debt repayment capacity and financial health can boost market confidence, potentially lifting stock prices and credit ratings while lowering future borrowing costs.

IV. Valuation

DCF Analysis

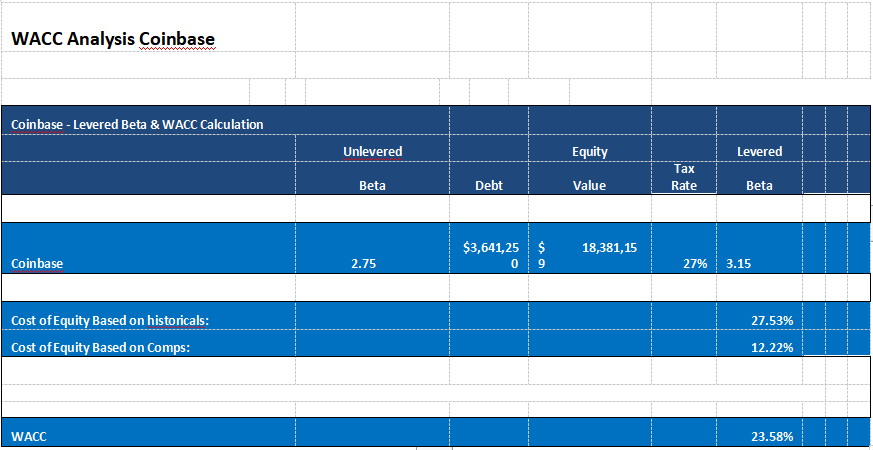

For the discounted cash flow analysis, we used the current D/V (67%) and E/V (33%) ratios based on Coinbase’s capital structure. Levered equity beta was calculated at 3.15. Using CAPM, assuming a 7% market risk premium and 5.5% risk-free rate, we derived the cost of equity. The pre-tax cost of debt was based on Coinbase’s senior notes, adjusted for a 27% effective tax rate to obtain after-tax cost. The resulting WACC is 23.58%.

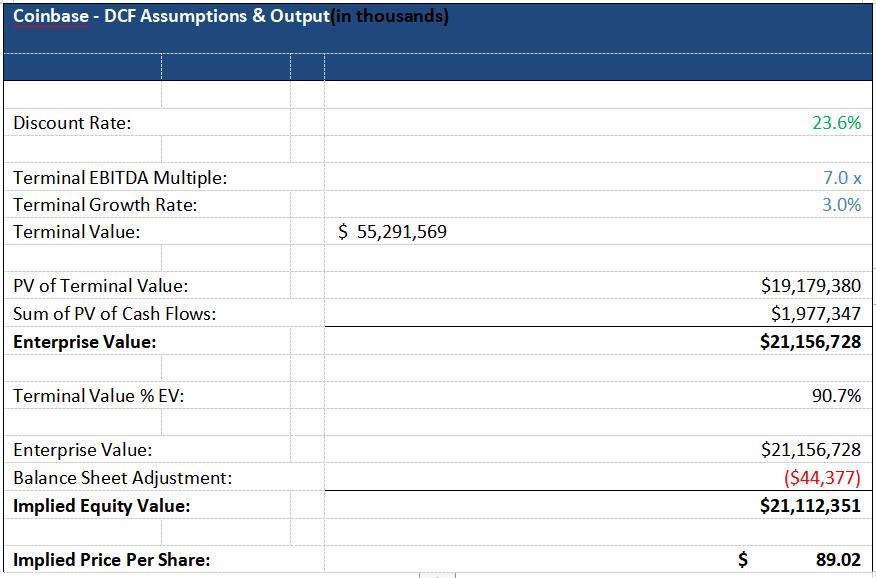

Given the current high-interest-rate environment, which may persist until mid-next year, terminal value assumptions in the DCF model are conservatively set. Revenue growth projections for FY2023–2025 are -5%, 10%, and 500%, respectively.

Valuation Rationale and Recommendation

Valuation indicates a fair value of $89 in the base case, suggesting the current $74 price is undervalued by 16%. However, due to the DCF model’s high sensitivity to forecasted growth and terminal EV/EBITDA multiples, the short-term stock price faces downward pressure from the dual bearish environment in U.S. equities and crypto markets. A practical strategy is to sell over the next 12 months and buy into the 24-month cycle: fair value is $89 at 7x EV/EBITDA and $170 at 14x.

Recommendation: Investment Horizon – Sell over the next 12 months

Buy into the 24-month cycle, with target prices of $89 at 7x EV/EBITDA and $170 at 14x.

V. Risk – Regulatory Uncertainty

Coinbase is seeking to dismiss a lawsuit filed by the SEC in June in a New York federal court against Coinbase, Inc. and its parent Coinbase Global, Inc., accusing them of operating unregistered exchanges, brokers, and clearing agencies.

Key Allegations: Under the 1934 Securities Exchange Act, broker-dealers, exchanges, and clearing agencies traditionally operate separately. Coinbase allegedly combines all three functions without SEC registration or applicable exemptions. For years, Coinbase has disregarded regulatory frameworks and evaded disclosure requirements mandated by Congress and the SEC.

During the same period, Coinbase allegedly operated as an unregistered broker by offering two additional services: Coinbase Prime (Prime), routing crypto orders to its own or third-party platforms; and Coinbase Wallet, routing orders via third-party platforms to access off-platform liquidity.

Coinbase has earned transaction revenue by listing crypto assets without acknowledging their potential classification as securities. Since 2016, Coinbase understood these assets should fall under securities regulation, yet consistently marketed itself as compliant while allowing trading of assets meeting the Howey Test criteria.

Since 2019, Coinbase has offered staking services, allowing investors to earn returns while taking 25–35% in commissions. However, it never registered or filed staking offerings with the SEC, depriving investors of critical information, harming investor interests, and violating registration requirements under the 1933 Securities Act.

All Coinbase revenue flows to its parent CGI, which is effectively the true controller. Thus, CGI also violates the same securities laws as Coinbase.

The SEC seeks:

(a) Permanent injunction against violations of securities laws;

(b) Disgorgement of ill-gotten gains with prejudgment interest;

(c) Civil penalties and equitable relief for investors’ benefit.

(Note: The SEC sought a permanent ban on financial activities for Binance.)

Conclusion

In summary, we believe Coinbase’s profitability will remain suppressed over the next 12 months, but its revenue and earnings growth potential will be unlocked within 24 months. Key upside not yet fully priced in:

1) Substantial revenue growth following the official launch of international and derivatives products;

2) Continued growth in staking revenue, including sequencing income from Base (and other chains), staking fees, and increased usage of Coinbase’s other products (wallets, etc.) by on-chain users;

3) USDC scale recovery driving higher reserve interest income and fee revenue from broader distribution; however, due to its strong correlation with crypto markets, core transaction revenue is unlikely to grow significantly over the next 8–12 months under continued macro headwinds. In the next bull market, growth could exceed the 515% surge seen in 2021.

Appendix

Regulatory Status

Coinbase’s CEO believes MiCA has passed in Europe, but every major financial center—UK, Singapore, Brazil—is actively advancing legislation, with others leading the U.S. in regulatory clarity.

Coinbase is actively working to bring regulatory clarity to the entire industry. One of the biggest barriers to technology adoption is the lack of clear rules and enforcement-driven regulation in the U.S. While much of the world has made significant progress embracing crypto and Web3 with clear legislation, the U.S. has lagged. Coinbase plays a vital role here. When the SEC refuses to create rules and instead uses enforcement actions, Coinbase turns to the courts to help establish regulatory clarity and build case law. It is also actively engaged in Congress, where bipartisan support for crypto legislation is evident.

In recent weeks, the House Financial Services Committee and the House Agriculture Committee passed landmark bills—the FIT21 crypto market structure bill and the stablecoin bill—with bipartisan support. These will go to a full House vote later this year and then to the Senate. Coinbase is committed to ensuring the U.S. passes crypto legislation and does not fall behind. It has begun mobilizing crypto users nationwide to ensure their voices are heard in American democracy. Today, one in five Americans uses crypto—more than those holding union cards. So far, the “Support Crypto” campaign has rallied around 60,000 advocates across all 435 congressional districts. For example, in a recent event in New York City, Coinbase hosted a live gathering with representatives from Senator Gillibrand’s office, Mayor Adams’ office, Governor Hochul’s office, and hundreds of crypto enthusiasts.

Coinbase is subject to various anti-money laundering (AML) and counter-terrorism financing laws, including the U.S. Bank Secrecy Act (BSA) and similar foreign regulations. In the U.S., as a money services business registered with FinCEN, the BSA requires Coinbase to develop, implement, and maintain a risk-based AML program, provide AML training, report suspicious activities, comply with reporting and recordkeeping obligations, and collect and maintain customer information. Additionally, it must adhere to customer due diligence requirements, including risk-based policies, procedures, and internal controls designed to verify customer identity.

Coinbase has implemented a compliance program designed to prevent its platform from being used for money laundering, terrorist financing, or other illegal activities, whether domestically or involving OFAC-designated countries, individuals, or entities abroad.

In the U.S., Coinbase has obtained money transmitter licenses or equivalents in all states where it operates, including D.C. and Puerto Rico. It also holds a BitLicense from the New York State Department of Financial Services (NYDFS).

Outside the U.S., Coinbase has obtained licenses from Germany’s Federal Financial Supervisory Authority (BaFin) to provide crypto custody and trading services. It is registered in Japan as a crypto asset exchange provider under the Kanto Local Finance Bureau, covering crypto and first-party payment services. In Singapore, it operates under the Payment Services Act and is supervised by the Monetary Authority of Singapore (MAS). It is currently in preliminary approval status and requires final MAS approval to become a Major Payment Institution. Under these licenses, it is subject to extensive rules, including AML, asset and fund safeguarding, capital requirements, fit-and-proper management, operational controls, corporate governance, disclosures, reporting, and recordkeeping.

Coinbase Custody Trust Company, LLC, a subsidiary, is a limited-purpose trust company chartered by New York and regulated, examined, and supervised by NYDFS. NYDFS regulations impose numerous compliance obligations, including operational limits on eligible crypto assets, capital requirements, BSA and AML program mandates, restrictions on affiliated transactions, and notification and reporting duties.

Coinbase serves customers through e-money institutions authorized by the UK Financial Conduct Authority and the Central Bank of Ireland. It complies with European e-money regulations, including those related to fund custody, corporate governance, AML, disclosures, reporting, and audits.

Coinbase has established policies and practices to evaluate each crypto asset considered for listing or custody and is a founding member of the Cryptocurrency Rating Council. Its brokerage operations are conducted by Coinbase Capital Markets and Coinbase Securities, both registered as broker-dealers with the SEC under the Securities Exchange Act of 1934.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News