Exploring the Underlying Business Model of RWA: Reflecting on Sustainability

TechFlow Selected TechFlow Selected

Exploring the Underlying Business Model of RWA: Reflecting on Sustainability

This article will examine and analyze existing RWA business models in the crypto market, starting from the underlying assets most suitable for RWA in the medium to short term.

Author: PSE Trading Analyst, @Yuki

Under the macro environment of Federal Reserve rate hikes, the U.S. has entered a "high-interest-rate era." In the face of continuously rising U.S. Treasury yields, low-risk returns in the DeFi world appear clearly insufficient. The crypto market is陷入 a predicament of capital steadily flowing out into traditional financial markets.

“Bringing real-world asset (RWA) yields into DeFi” will become a crucial move to retain on-chain capital and attract external funds. Based on this, the crypto market is refocusing attention on the RWA (Real World Assets) concept first introduced back in 2020, attempting to explore optimal methods for mutual capital circulation between traditional finance and the crypto ecosystem through various business models.

This article analyzes and organizes existing RWA business models in the crypto market, starting from the most suitable underlying assets for RWA in the medium- to short-term.

1. Exploring RWA Underlying Assets

1.1 Sector Background & Current State

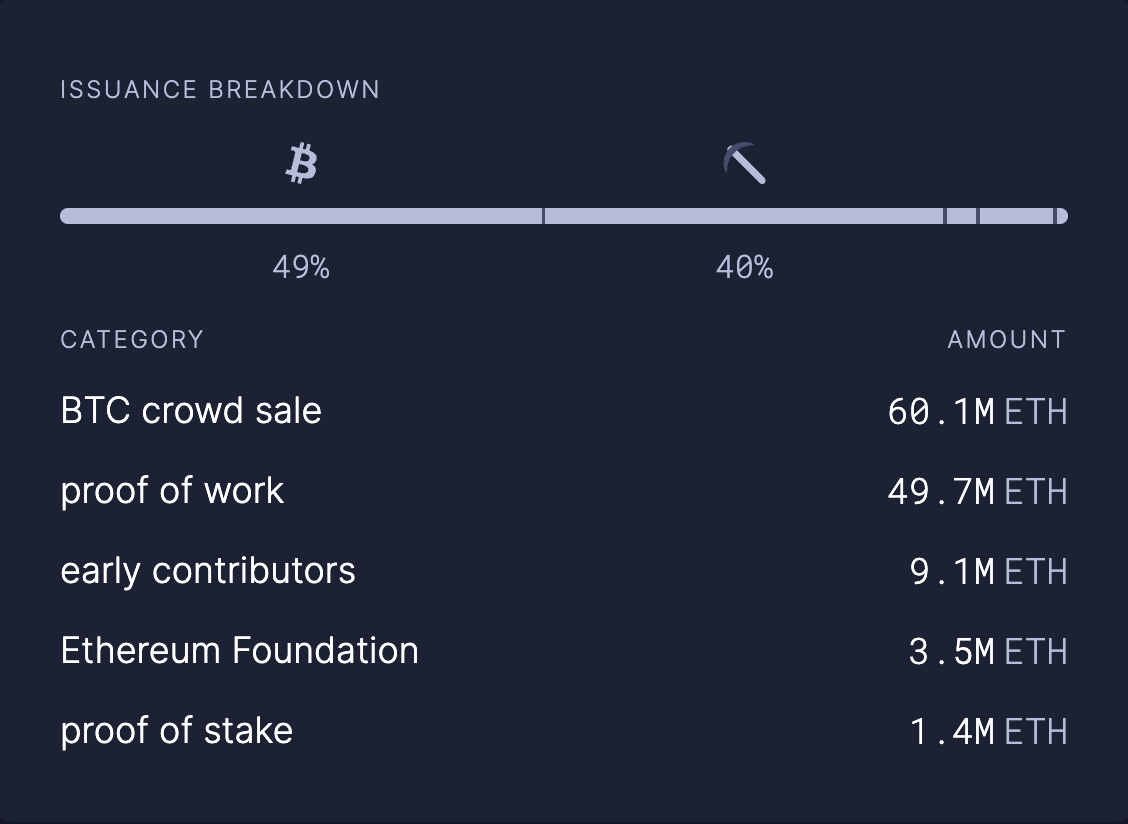

Currently, although the total market cap of the crypto market remains around one trillion USD, there is a lack of stable low-risk yield sources within the ecosystem. Only ETH-denominated liquid staking based on the PoS mechanism has gained recognition and support from market capital. This indirectly highlights the inevitability of LSDFi's rise.

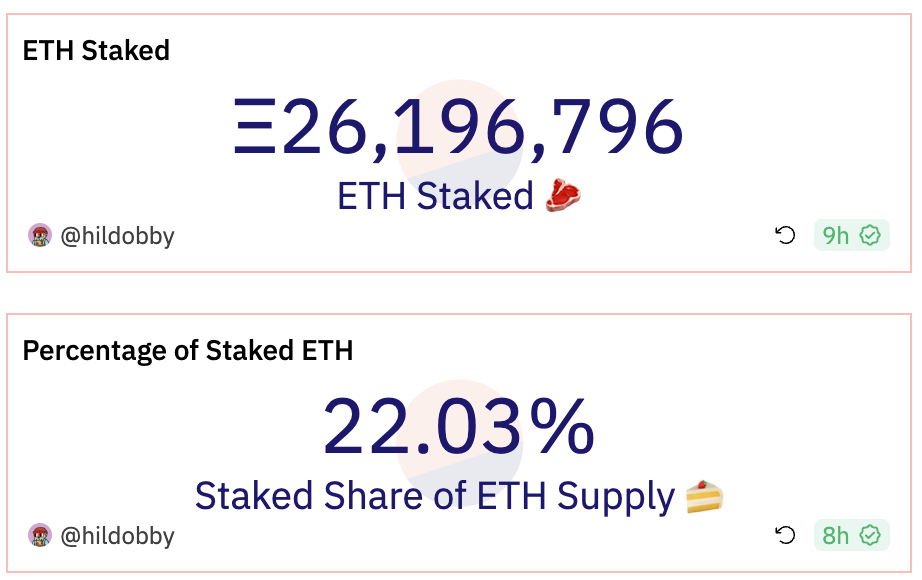

According to ultrasound.money, since Ethereum’s transition to PoS, over 1.4 million ETH in staking rewards have been generated, despite a current staking rate of only 22.03% of total supply. This means Ethereum has become an interest-bearing asset yielding approximately 5.3% (Staking Rewards / ETH staked), generating a foundational $2.4 billion in annual yield (with ETH priced at $1,720 per token at the time of writing).

Following the same logic, RWA tokenization maps the “equity value” of real-world assets directly onto blockchains in digital form, granting tradable liquidity to these “equity values.” In other words, RWA brings real-world asset yields into the crypto industry, serving as genuine yield-bearing USD-denominated (U-denominated) assets that can inject greater liquidity and vitality across the entire market.

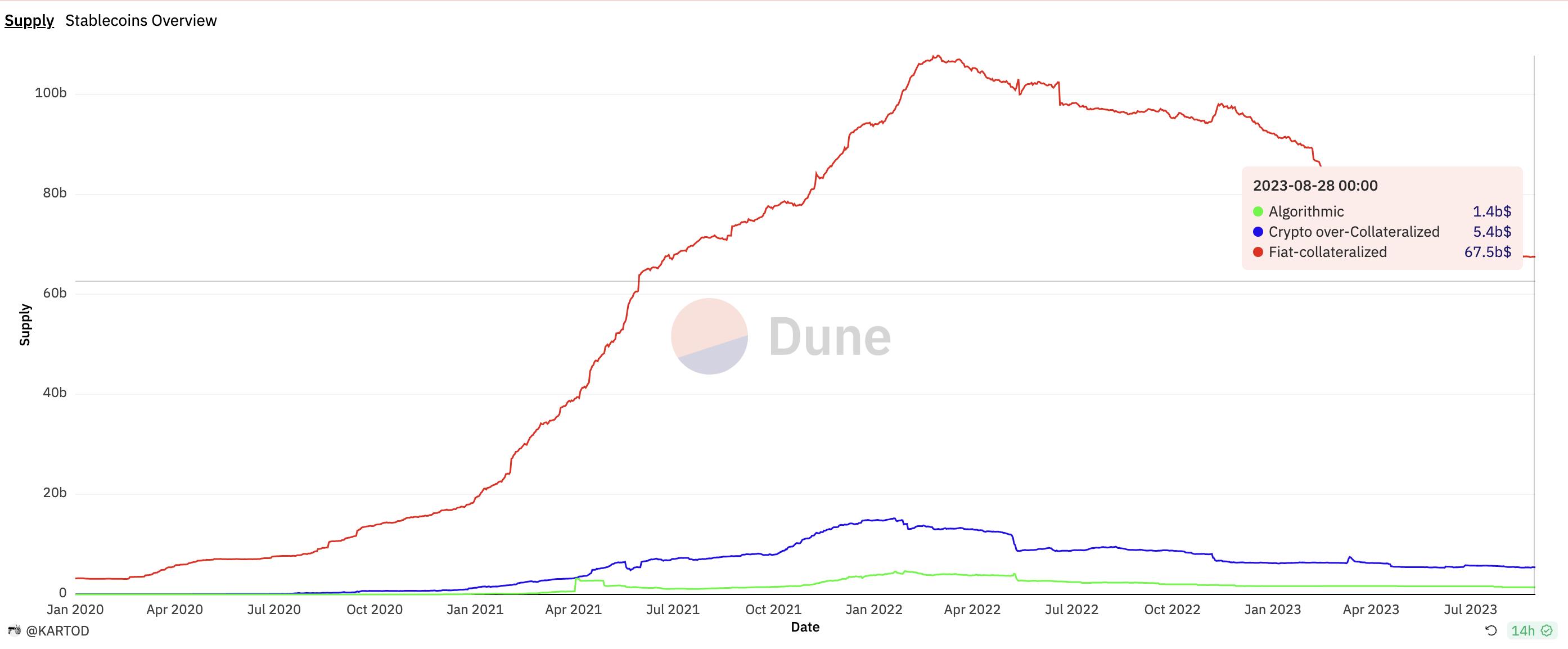

Currently, the total stablecoin supply in the crypto industry stands at approximately $74.3 billion, but most dollar-pegged stablecoins (U-denominated assets) do not offer stable real yields (unlike ETH’s 5% staking yield). If RWA could provide similar real yields (~5% APY) to U-denominated assets, it could generate an additional $3.7 billion in foundational annual yield while further stimulating growth in stablecoin adoption.

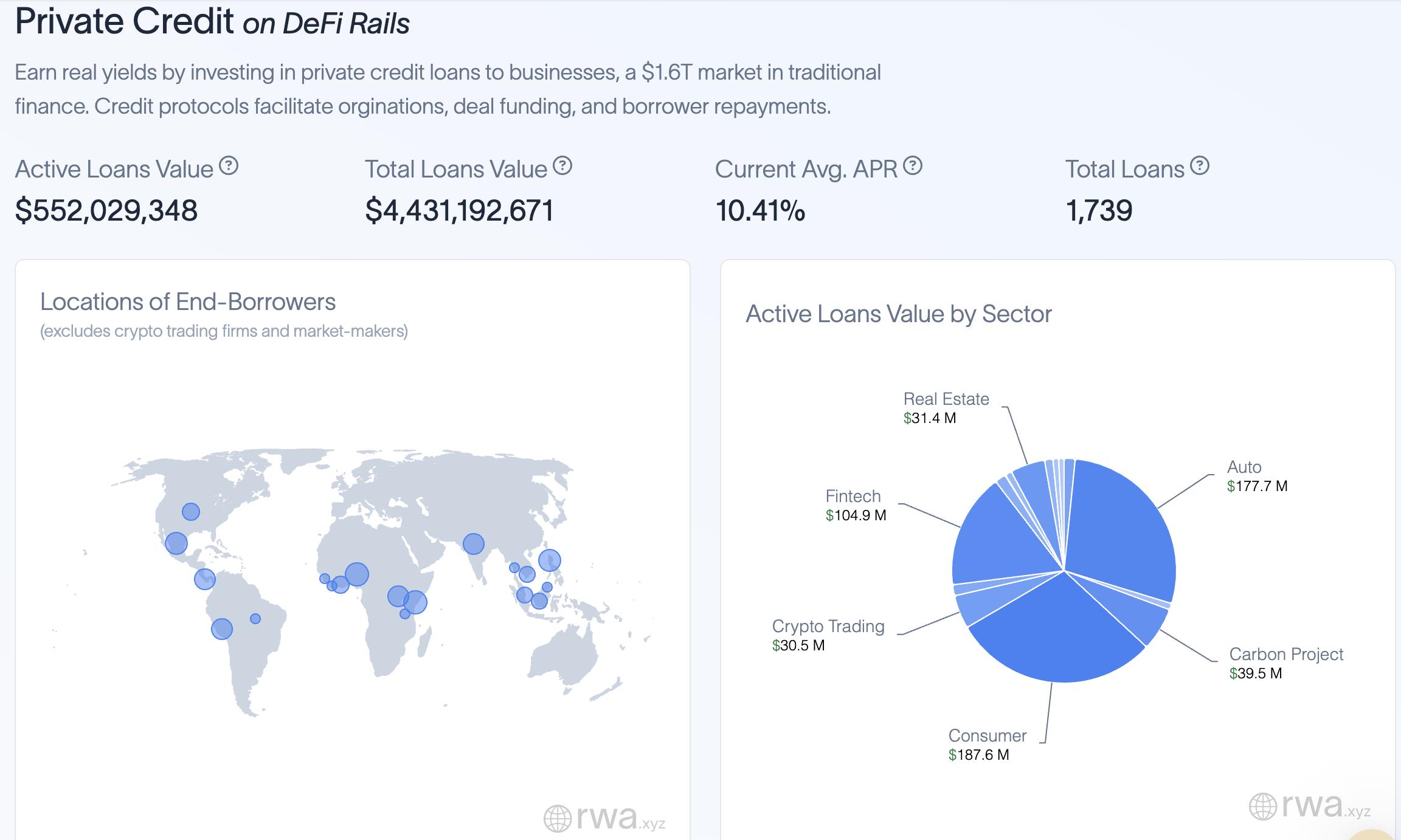

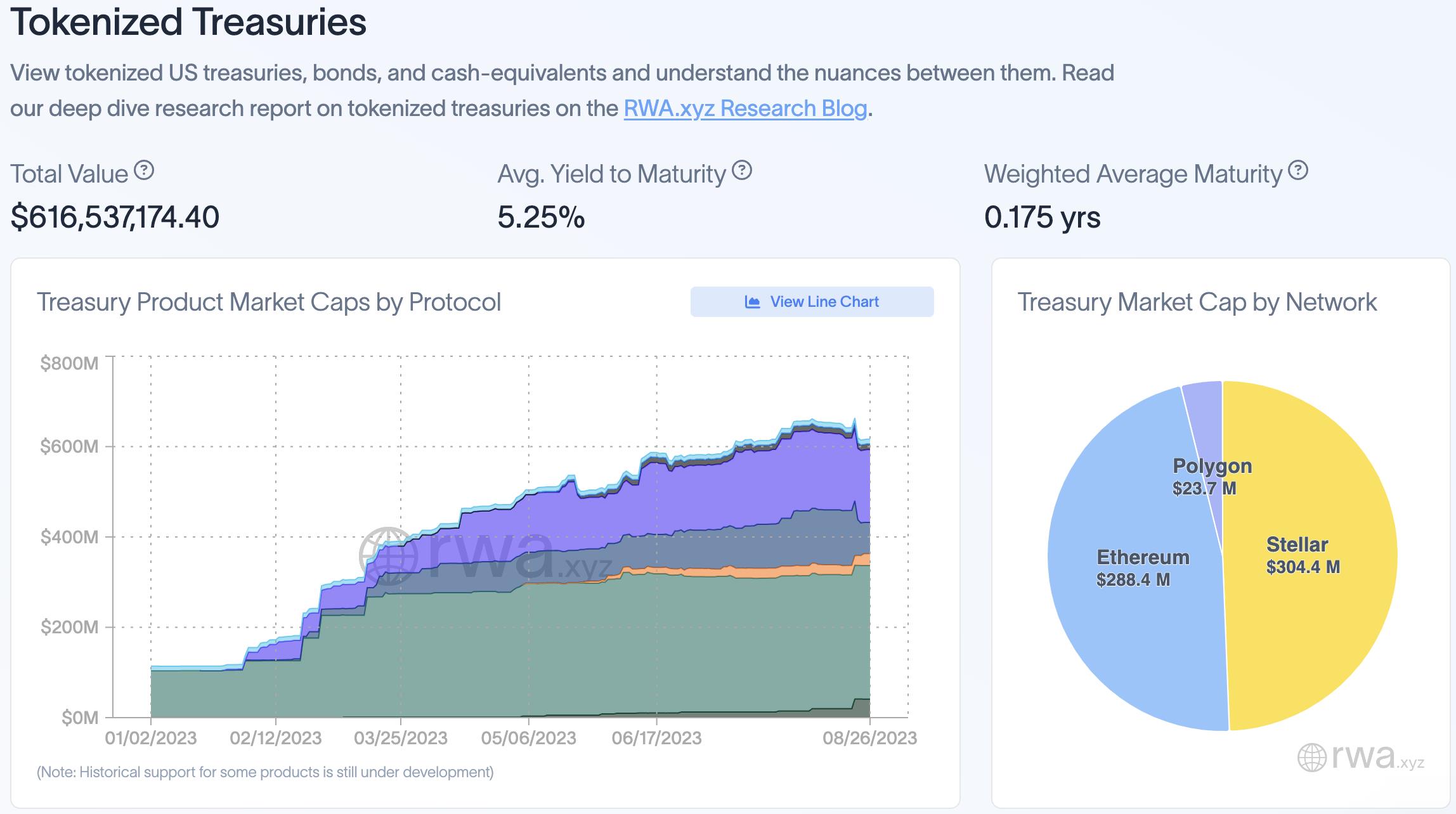

According to rwa.xyz, cumulative borrowing volume across existing private credit RWA protocols amounts to just over $500 million (excluding MakerDAO), while tokenized U.S. Treasury securities amount to only $640 million (excluding indirect integration models), totaling less than $1.2 billion.

Taking short-term U.S. Treasury Bills as an example, the U.S. Department of the Treasury reported an average interest rate of 5.219% as of July 31, with an outstanding scale of $4.769 trillion. If RWA successfully channels these yields into the crypto market, it could theoretically generate $248.89 billion in annual yield—flood-like liquidity that would revitalize the entire industry, which currently has a total market cap of only about $1 trillion.

A report jointly released by BCG and ADDX also projects that global tokenized assets—including real estate, stocks, bonds, and investment funds—will grow to $16.1 trillion by 2030, bringing significantly more attention and capital into the crypto market.

In summary, RWA is still in its early development stages but holds immense potential. Just as ETH-denominated real yield triggered the explosive growth of LSDFi, RWA could similarly serve as genuine yield for U-denominated assets and drive incremental expansion across the crypto market.

The crypto market has already keenly sensed this massive potential behind RWA, with established DeFi OGs such as MakerDAO and Compound actively entering the space.

1.2 Best Mid-Term Underlying Asset: Bonds

Since RWA requires off-chain traditional assets to be tokenized, the selection of underlying assets becomes the most critical issue. The reason is that the choice of underlying assets profoundly impacts the complexity and flexibility of subsequent tokenization, as well as the difficulty of asset and risk management.

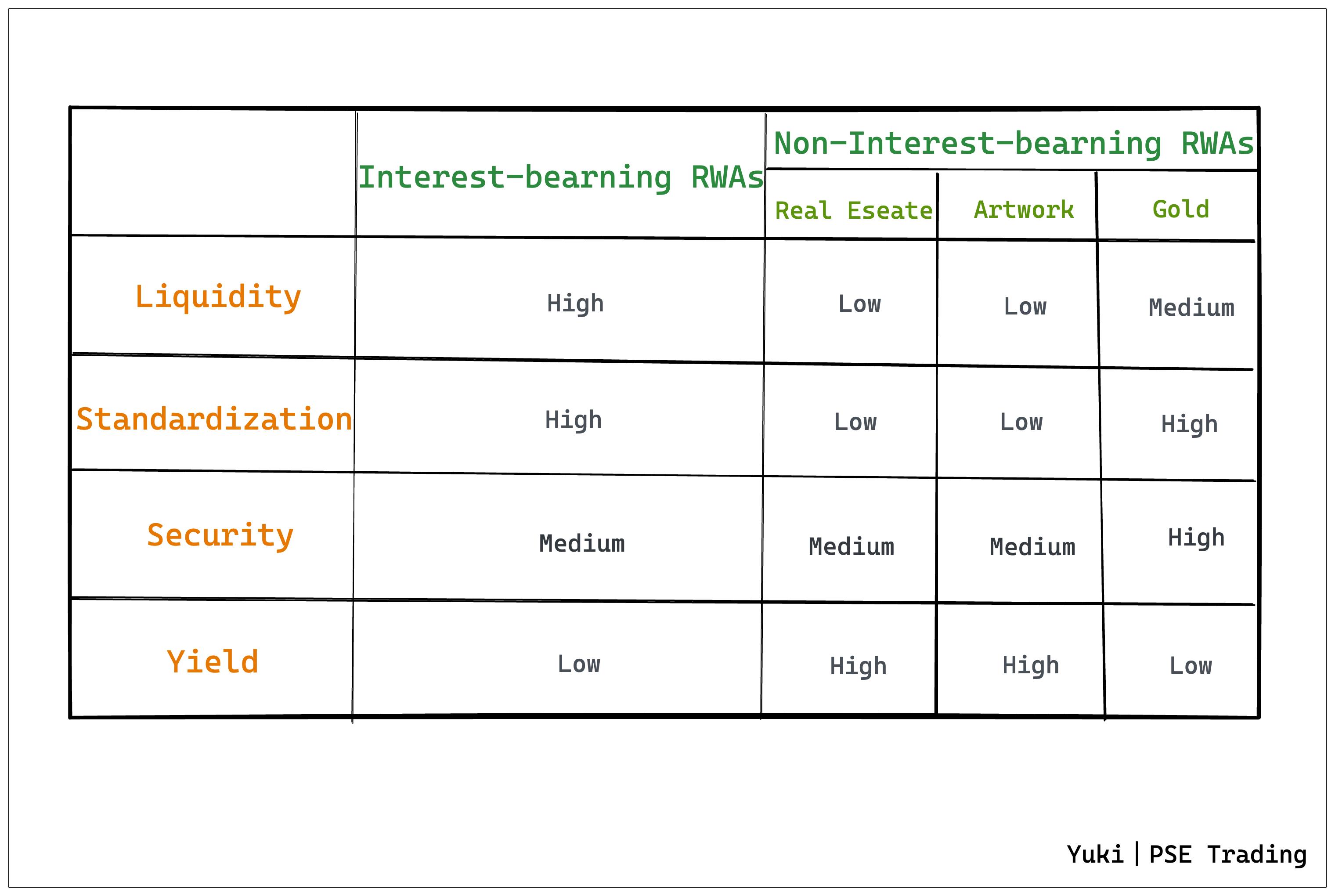

Based on the above rationale—RWA as genuine yield for crypto-native U-denominated assets—I categorize RWA underlying assets into two main types:

-

Yield-Bearing RWA (analogous to post-PoS ETH): Bond-type assets, primarily short-term U.S. Treasuries or bond ETFs

-

Non-Yield-Bearing RWA (analogous to PoW ETH): Real estate, art, gold, etc.

Further considering the underlying assets’ liquidity, standardization, security, and yield, we find that while yield-bearing RWAs (primarily bonds) may lag behind non-yield-bearing RWAs (such as real estate and art, which have higher yield ceilings) in terms of return rates, they hold clear advantages in the more important aspects of liquidity and standardization. Only highly liquid and standardized underlying assets can support large-scale application and expansion of RWA.

Additionally, yield-bearing RWA resembles ETH-denominated yield-bearing assets—despite potentially modest yields, the stability of “yield generation” enables greater protocol composability, thus driving further DeFi innovation.

Therefore, I believe the best mid-term RWA underlying assets are debt-based instruments centered on short-term U.S. Treasuries or bond ETFs. Their yield-bearing nature perfectly satisfies the crypto market’s demand for low-risk yield sources, while their high liquidity and standardization facilitate broad RWA adoption.

Hence, the following sections will conduct an in-depth exploration of representative RWA projects using U.S. Treasuries or bond ETFs as underlying assets, focusing on their business models.

2. RWA Business Models Based on U.S. Treasuries / Bond ETFs

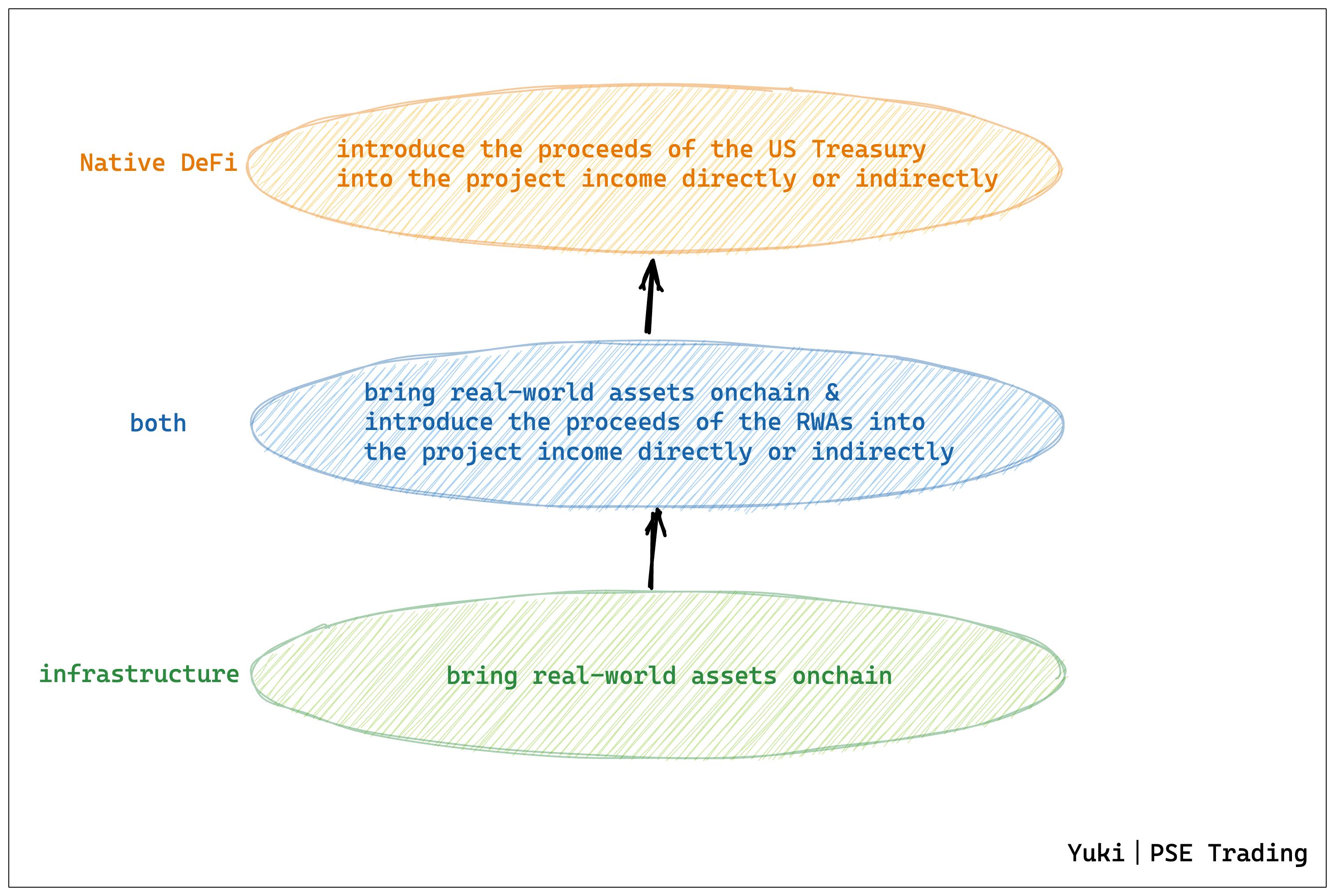

Starting from U.S. Treasury-backed RWA, we observe three prevailing business model layers:

-

Infrastructure Layer: Responsible for bringing U.S. Treasury RWA on-chain

-

Middle Hybrid Layer: Handles both on-chain RWA and integrating Treasury yields into DeFi

-

Upper DeFi Layer: Directly uses or indirectly integrates Treasury yields as project revenue

These three layers differ significantly in terms of RWA tokenization difficulty, flexibility, and target customer segments.

Specifically, infrastructure-layer RWA tokenization businesses typically do not directly engage retail users but instead focus on B2B clients. The step of “creating an on-chain representation of off-chain real-world assets” must resolve identity alignment between on-chain and off-chain systems while addressing asset security, regulatory risks, and implementation costs. These operations are often the most difficult and complex, yet indispensable for RWA development.

In contrast, native DeFi applications at the upper layer do not need to concern themselves with the tokenization process itself. Instead, they can directly or indirectly integrate RWA yields atop existing tokenized assets—either through partnerships with infrastructure projects or by building DeFi products on top of RWA tokens—thus primarily targeting retail (C-end) users.

The middle layer combines both approaches: it performs RWA tokenization while simultaneously developing suitable on-chain products for its own RWA tokens, directly incorporating RWA yields and integrating them into the DeFi ecosystem.

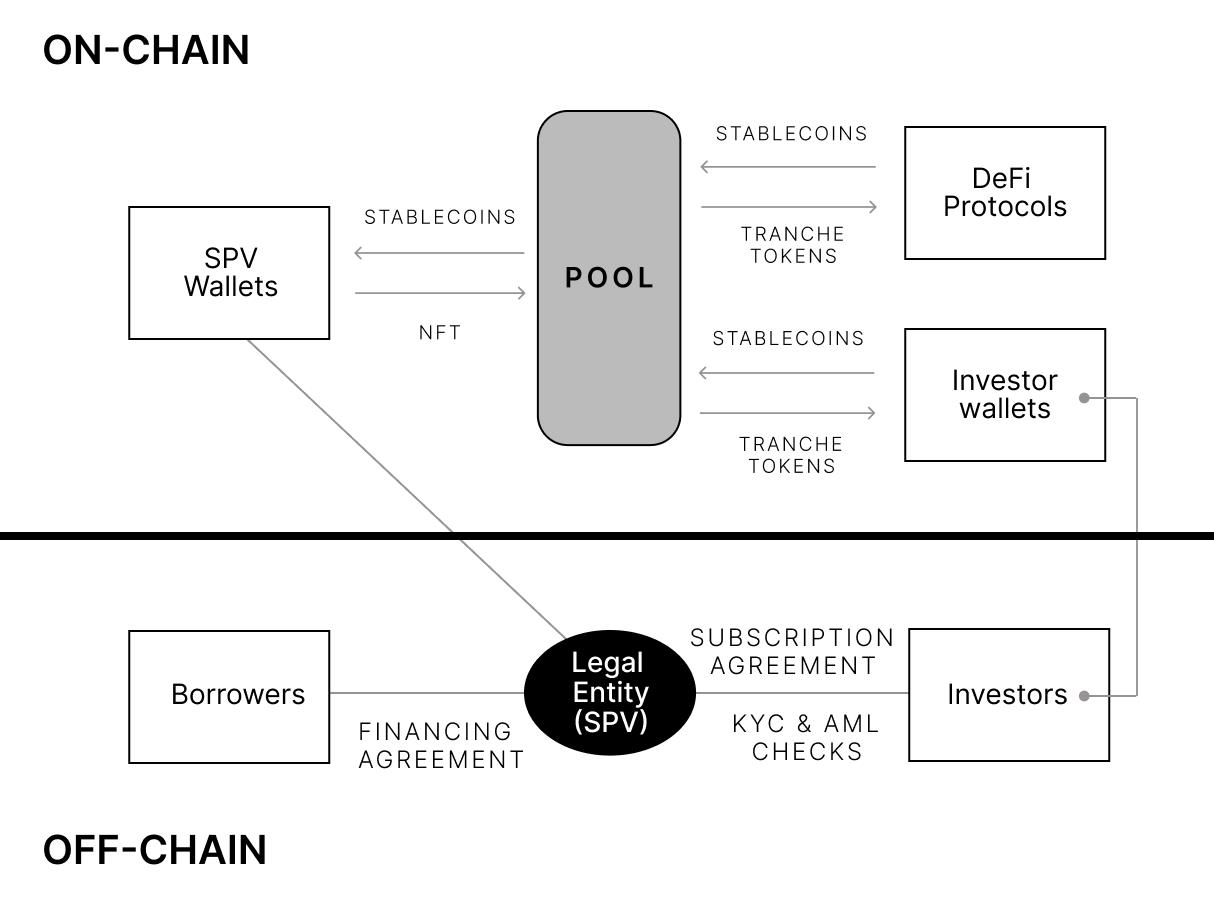

Generally speaking, any project involving RWA tokenization imposes strict KYC requirements. While this stems from security and regulatory demands, it inherently contradicts DeFi’s core ethos of openness and permissionlessness, thereby raising entry barriers for RWA participation.

2.1 Infrastructure Layer: RWA Tokenization

An essential step in bringing real-world assets on-chain is encapsulating those assets into a compliant, digitized form while preserving key information such as value, ownership, and maturity. This layer plays a foundational role akin to laying a solid base for a skyscraper.

Business Model 1: SPV-Based Tokenization

The most common approach to RWA tokenization today follows the framework of asset securitization—establishing a Special Purpose Vehicle (SPV) to hold the underlying assets, enabling control, management, and risk isolation.

Representative Project: Centrifuge

Although Centrifuge operates as an RWA lending protocol, its SPV-based tokenization path offers significant insights for many DeFi protocols pursuing RWA integration. Its Centrifuge Prime offering provides technical and legal frameworks specifically designed to enable DAOs to invest in RWAs.

MakerDAO partnered with New Silver via Centrifuge as early as February 2021 to issue its first RWA002Vault. Subsequent large-scale RWA integrations have largely followed the SPV tokenization route.

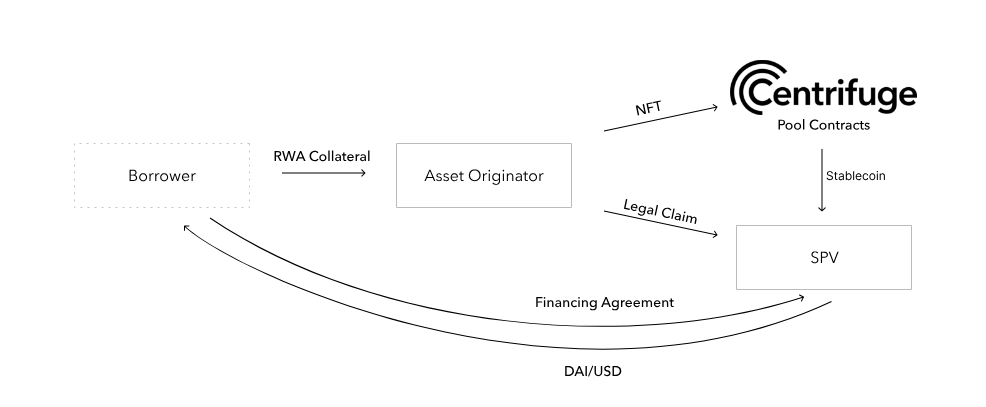

Centrifuge’s RWA implementation pathway:

-

An Asset Originator (AO) establishes a legal entity (an SPV) for each pool to isolate financial risk and fund specific RWA assets backing a given Centrifuge pool;

-

Borrowers tokenize off-chain assets into NFTs via the AO, which serve as on-chain collateral;

-

Borrowers sign financing agreements with the SPV and request the AO to lock their NFTs into the Centrifuge pool associated with the SPV;

-

Once locked, DAI is drawn from the Centrifuge reserve and transferred to the SPV’s wallet, which then converts DAI to USD and wires it to the borrower’s bank account;

-

At maturity, borrowers repay the principal plus fees, either directly in DAI on-chain or in USD off-chain. The SPV converts received USD into DAI and pays it to the Centrifuge pool. Upon full repayment, the locked NFT is returned to the AO and destroyed.

Despite Centrifuge’s use of SPVs for risk isolation and collaboration with Securitize for KYC/AML compliance, its RWA pools still face some bad debt issues. According to rwa.xyz, Centrifuge has \(13,210,882 in defaulted loans, representing 3.01% of total loan volume (\)438,341,921).

Business Model 2: Fund Share Tokenization

Another common method involves launching a regulated fund based on short-term U.S. Treasuries and recording fund transaction data on-chain, thereby tokenizing fund shares.

Representative Projects: Superstate, Franklin Templeton

In June, Robert Leshner, founder of Compound, announced the launch of Superstate, officially entering the RWA space. Superstate plans to launch a fund based on short-term government bonds and has already filed relevant applications with the SEC awaiting approval. Notably, Leshner has prior experience in U.S. Treasury-related roles, giving him a strategic advantage.

Superstate’s RWA implementation pathway:

-

Superstate launches a fund based on U.S. Treasuries and government agency securities for U.S. residents;

-

Users subscribe to the fund and become shareholders;

-

Shareholders can convert their fund shares into corresponding tokens recorded on Ethereum;

-

Fund share token holders must register their addresses on a whitelist; non-whitelisted addresses cannot execute transactions;

-

Official fund transfer agent records are still maintained in book-entry form. In case of discrepancies between on-chain and off-chain records, the fund manager updates the on-chain record based on the off-chain ledger.

Franklin Templeton, a publicly traded asset manager overseeing over a trillion dollars in assets, employs a business model similar to Superstate. In 2021, it launched the Franklin OnChain U.S. Government Money Fund (FOBXX) on the Stellar blockchain via fund share tokenization, with BENJI tokens representing fund units.

2.2 Middle Hybrid Layer: RWA Tokenization + DeFi Integration

Compared to the infrastructure layer, middle-layer RWA projects add direct connectivity and interoperability with DeFi—akin to a “vertically integrated” model. This allows greater control over design from bottom to top, facilitating risk management and scalability. However, due to strict legal requirements for U.S. Treasury tokenization, KYC remains unavoidable.

Business Model 3: Fund Share Tokenization + DeFi Protocol

Representative Project: Ondo Finance

Ondo Finance serves institutional-grade users through exempt offerings, which impose stringent eligibility criteria requiring investors to meet SEC definitions of “accredited investors” and “qualified purchasers.”

Ondo’s RWA implementation pathway:

-

Users deposit USDC (or other stablecoins) into Ondo’s fund products and receive corresponding fund tokens;

-

Ondo converts stablecoins into USD (held in custody by Coinbase) and deposits them into a bank account;

-

Then purchases U.S. Treasury ETFs via Clear Street, a licensed broker and custodian;

-

As underlying assets generate yield, earnings are reinvested automatically, compounding returns;

-

At any time, users wishing to redeem their USDC burn the fund tokens and receive USD.

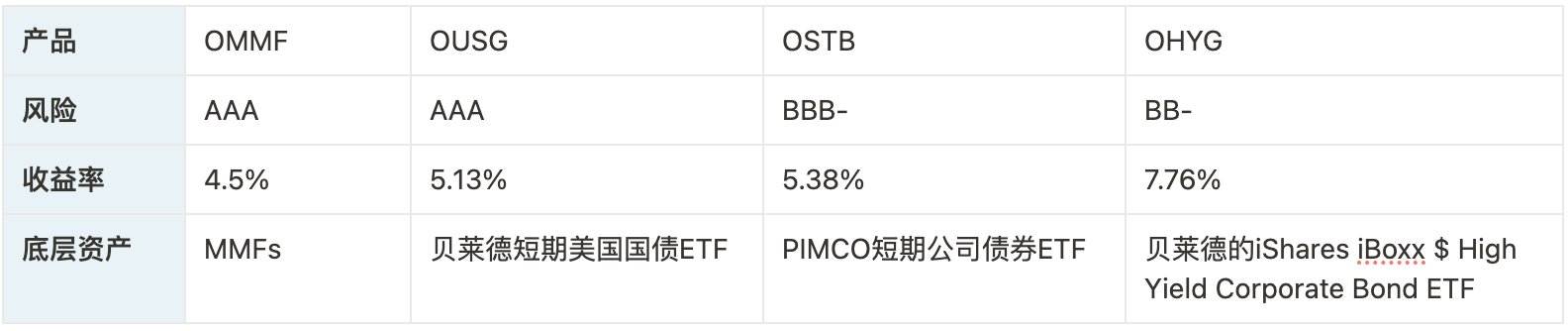

Ondo currently offers four RWA products tailored to U.S. users, backed by different underlying assets and catering to diverse risk preferences.

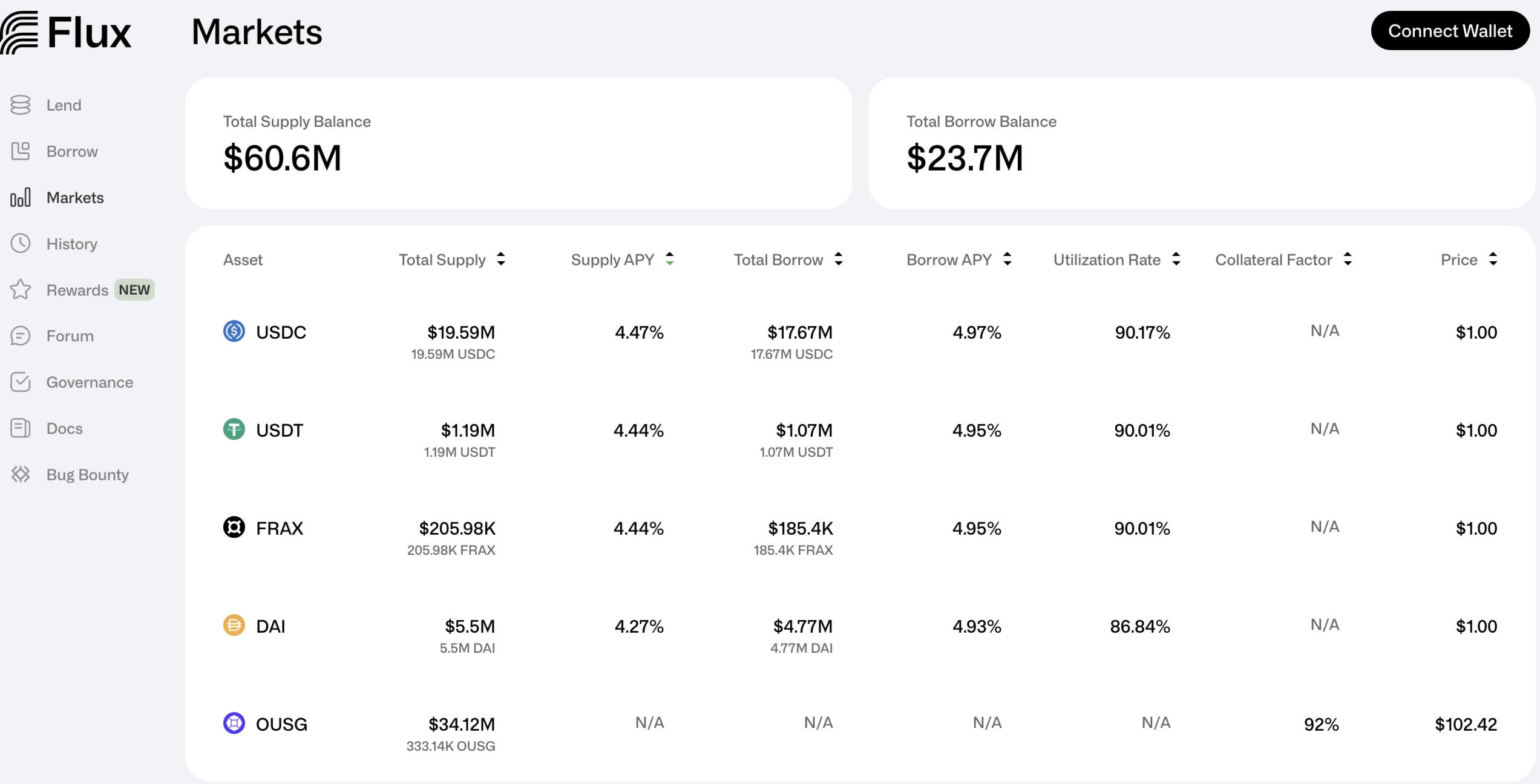

OUSG, its largest fund, has expanded usage scenarios through Flux Finance—a decentralized lending protocol developed by Ondo. OUSG holders can pledge OUSG on Flux to borrow stablecoins like USDC, DAI, and Frax.

Flux itself imposes no KYC restrictions but implements a whitelisted liquidation mechanism. Its purpose is to help Ondo better integrate RWA into native DeFi ecosystems, striving to build an “ecological closed loop.”

For non-U.S. users, Ondo plans to launch a new product called USDY—a tokenized note secured by short-term U.S. Treasury holdings and bank demand deposits. After 40–50 days, users can transfer USDY on-chain.

Business Model 4: SPV Tokenization + DeFi Protocol

Representative Projects: Matrixdock, Maple Finance, Kuma Protocol

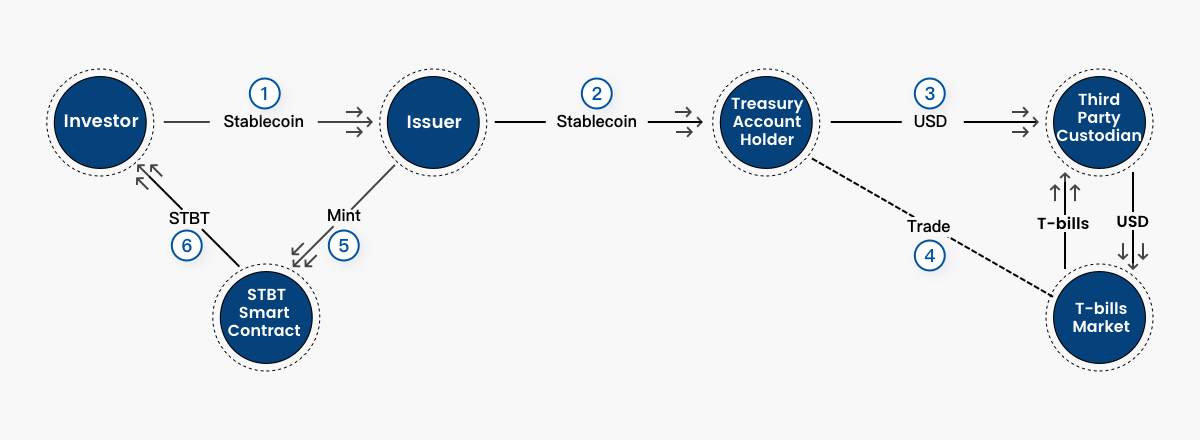

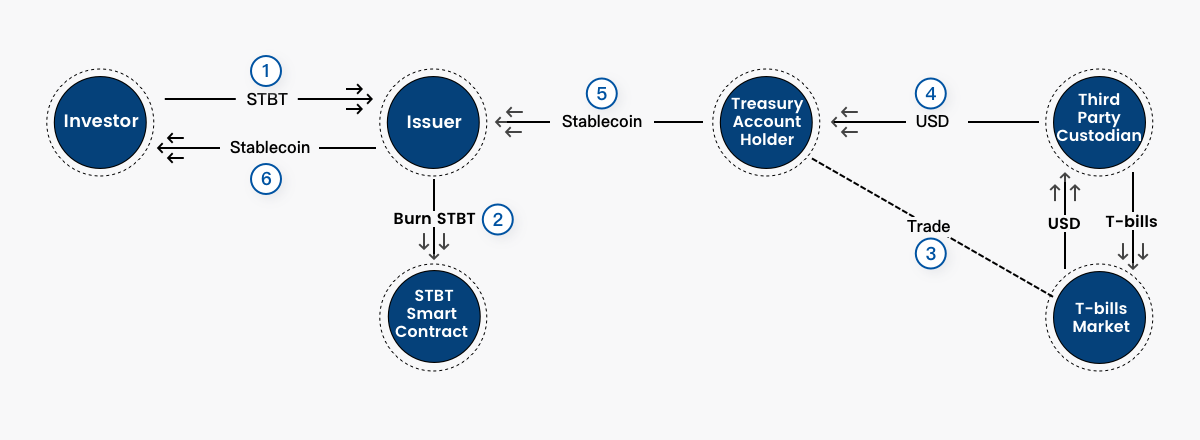

Matrixdock, a Matrixport-launched on-chain bond platform, offers STBT (Short-term Treasury Bill Token), based on short-term U.S. Treasuries. STBT is an ERC-1400 standard token that recalibrates interest accrual daily, backed by U.S. Treasuries maturing within six months and reverse repurchase agreements.

Matrixdock’s RWA implementation pathway:

-

A dedicated SPV established by Matrixport acts as the STBT issuer;

-

Investors deposit stablecoins into the SPV, triggering smart contract minting of equivalent STBT;

-

The SPV converts stablecoins to fiat via Circle and pledges U.S. Treasury and cash assets to STBT holders;

-

Fiat is held by qualified third-party custodians who purchase short-dated Treasuries (maturing within six months) or invest in the Fed’s overnight reverse repo market via traditional financial accounts;

-

STBT holders enjoy first-priority claim rights over the physical asset pool.

Note: Only KYC-verified investors may participate in Matrixdock products. STBT transfers are restricted to whitelisted users, including within Curve pools. The permissionless RWA lending protocol T Protocol has built an open-access U.S. Treasury investment pool using STBT.

Maple Finance was formerly an uncollateralized lending protocol based on RWAs, but excessive risk led to over $50 million in bad debt. In April, Maple pivoted to launch a new cash management pool (similar to Matrixdock), allowing non-U.S. accredited investors and entities to participate in U.S. Treasury investments via USDC. Its RWA implementation closely mirrors Matrixdock’s and won’t be detailed again here.

Notably, Maple recently raised $5 million to expand its lending arm, Maple Direct, aiming to provide DAOs and Web3 companies simplified on-chain access to Treasury yields.

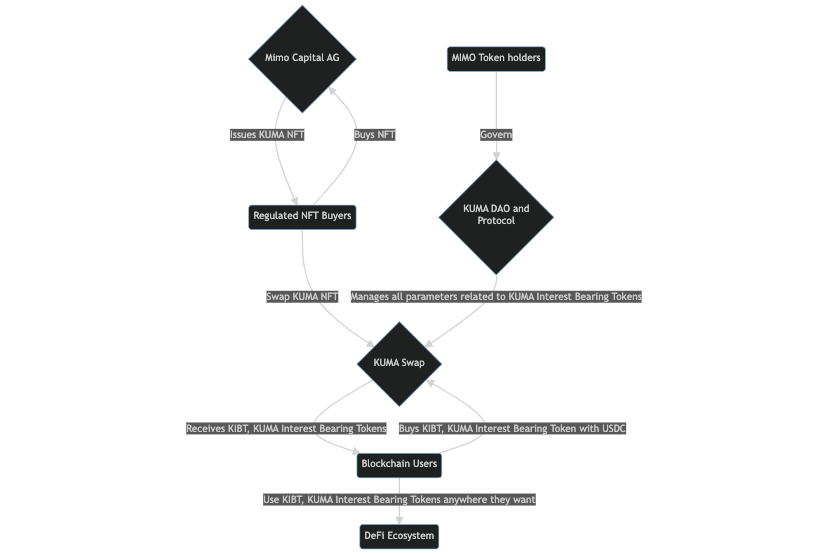

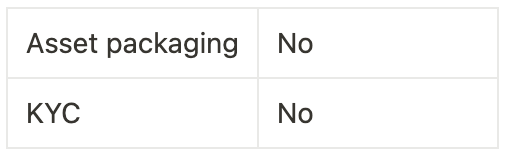

Kuma Protocol, launched by Mimo Labs, introduces RWA yields into DeFi by issuing regulated NFT-backed interest-bearing tokens (KIBT). Currently, Kuma only accepts NFTs backed by sovereign bonds (U.S. Treasuries).

At its core, KIBT functions as an interest-bearing stablecoin whose balance grows with accrued interest. The significance of KIBT lies in enabling users to earn RWA yields while simultaneously deploying KIBT within DeFi applications.

Kuma Protocol’s RWA implementation pathway:

-

Mimo Labs establishes an SPV—Mimo Capital AG—and issues KUMA NFTs backed by sovereign bonds;

-

Users purchase KUMA NFTs with stablecoins and mint interest-bearing KIBT tokens via KUMA Swap;

-

KIBT is a rebase-enabled ERC-20 token. Two variants exist:

-

EGK: KIBT linked to KUMA NFTs backed by 740-day Eurozone sovereign bonds

-

USK: KIBT linked to KUMA NFTs backed by 1-year U.S. sovereign bonds

Kuma Protocol’s key challenge is expanding the utility and liquidity of its interest-bearing KIBT tokens. Still in early stages, its KYC-free model stands out as its biggest current advantage.

2.3 Upper Layer: DeFi Integrating RWA Yields

Native DeFi applications at the upper layer don’t need to handle the tokenization process or KYC risks directly. Instead, they can integrate RWA yields—directly or indirectly—on top of already tokenized assets. Implementation paths typically involve partnering with infrastructure projects or building DeFi products atop RWA tokens.

Business Model 5: Indirect Integration of RWA Yields

When native DeFi apps pursue RWA strategies, they generally take one of two approaches: either build directly atop RWA yields or indirectly incorporate them as protocol revenue. The most successful example of the latter is MakerDAO.

Representative Projects: MakerDAO, Frax Finance

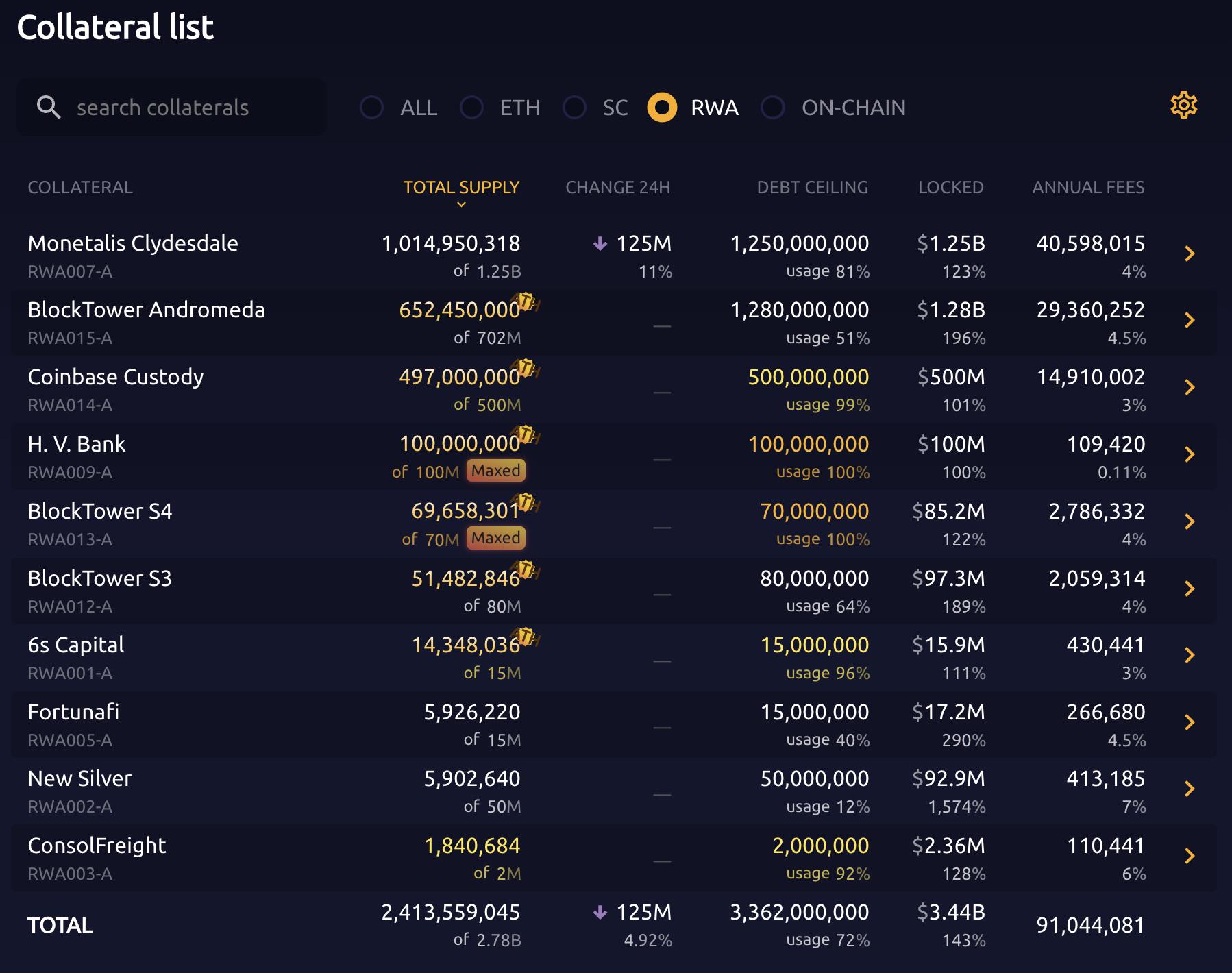

Despite Dai’s multi-billion-dollar scale, it has struggled to grow further. To address this, MakerDAO co-founder Rune proposed integrating RWA as a transitional strategy. According to MakerBurn, MakerDAO has now onboarded 10 RWA projects totaling $2.413 billion in collateral. These RWA assets contribute over 50% of MakerDAO’s revenue. The increase in DSR (Dai Savings Rate) is closely tied to RWA-generated yields.

Among MakerDAO’s RWA holdings, Monetalis Clydesdale is the largest. It originated from MIP65, a proposal introduced in January 2022 by Monetalis founder Allan Pedersen.

MIP65 aims to generate stable returns from part of MakerDAO’s stablecoin reserves by investing in high-liquidity, low-risk bond ETFs.

Monetalis Clydesdale’s RWA implementation pathway:

-

After MakerDAO governance approval, Monetalis is appointed as executor and required to report regularly;

-

Monetalis, as planner and operator, designs a full trust structure based in the British Virgin Islands (BVI) to bridge on-chain and off-chain coordination;

-

All MKR holders are beneficiaries and govern purchasing/disposal decisions for trust assets;

-

Coinbase provides USDC-to-USD conversion services;

-

Funds are invested in two ETFs: BlackRock’s iShares US$ Treasury Bond 0-1 yr UCITS ETF and iShares US$ Treasury Bond 1-3 yr UCITS ETF;

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News

Add to FavoritesShare to Social Media