The Only Right Path for Mid- to Short-Term RWA: A Discussion on Web3 Treasury Bond Business

TechFlow Selected TechFlow Selected

The Only Right Path for Mid- to Short-Term RWA: A Discussion on Web3 Treasury Bond Business

In the medium to long term, competition might be influenced by increasingly deep regulatory involvement, potentially creating greater opportunities for certain lightweight KYC projects.

Author: Colin Lee

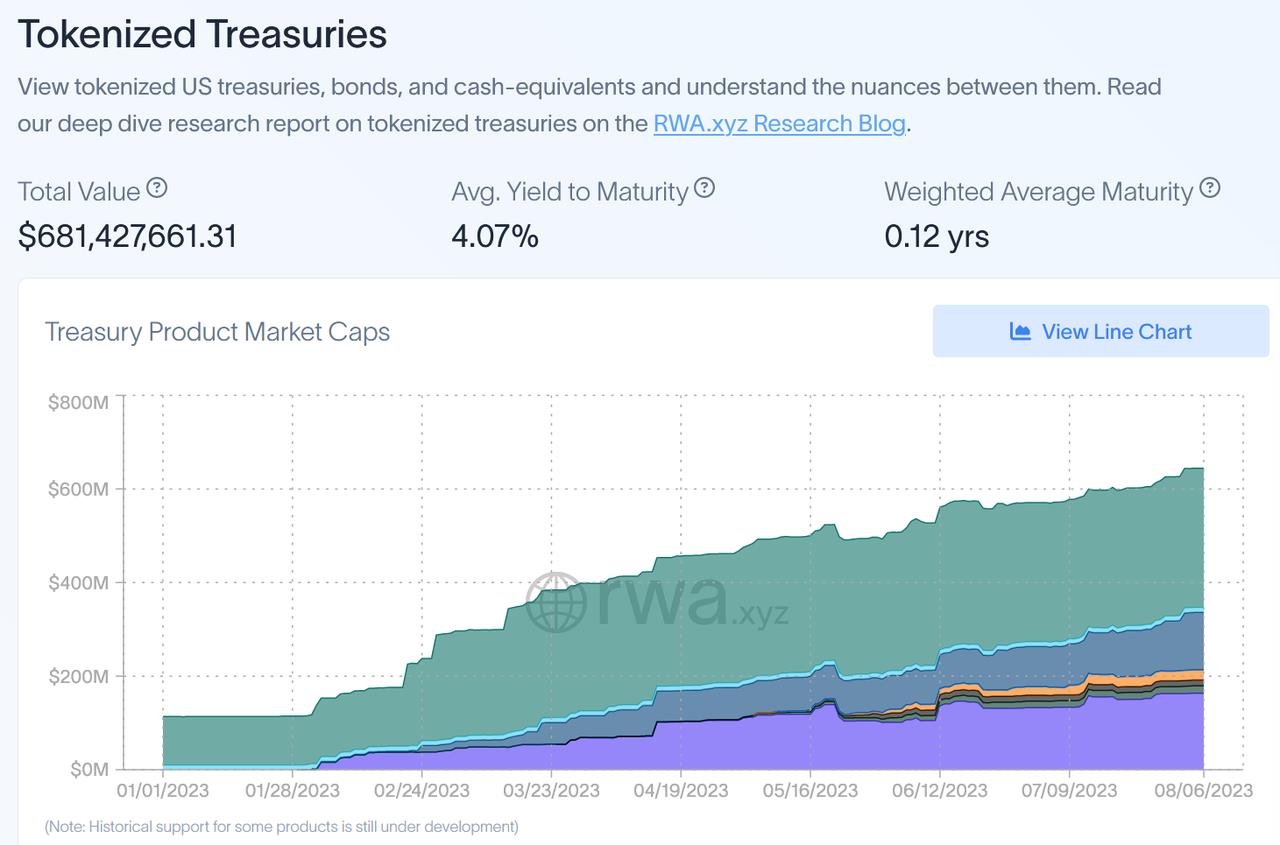

In our previous article, we mentioned that in the short to medium term, government bond-based RWAs are most likely to achieve explosive growth in scale and user adoption among all RWA subcategories. According to data from rwa.xyz, tokenized U.S. Treasury assets (excluding those held by MakerDAO) have already approached $700 million—representing approximately a 240% increase since the beginning of the year. Additionally, MakerDAO’s holdings of U.S. Treasury-related RWAs have rapidly grown into the billions of dollars. Overall, government bond RWAs are expanding at a fast pace.

Given this industry backdrop, we now analyze the major government bond RWA projects currently active in the market.

1. The Significance of Government Bond RWAs

In prior articles such as "How Should the Native Risk-Free Rate Be Defined in Crypto?" and "Outlook for an On-Chain Bond Market in Crypto," we discussed the concept of a native risk-free rate and potential bond markets within the crypto ecosystem. We can roughly consider Proof-of-Stake (PoS) yields on public blockchains as the native risk-free rate, around which an on-chain bond market could gradually develop.

Even if a fully developed native bond market akin to traditional financial systems does not emerge quickly on-chain, the emergence of LSDs ("Liquid Staking Derivatives") still holds great significance for investors: holders of native chain tokens (e.g., ETH) can earn low-risk yield denominated in their base asset even during bear markets. From this perspective, certain investment strategies common in traditional finance—such as equity-bond allocation—can be more smoothly adapted to the crypto-native space.

Similarly, government bond RWAs introduce traditional finance’s risk-free rate onto the blockchain, enabling USD-pegged (U-denominated) investors to apply conventional portfolio strategies. This brings several advantages:

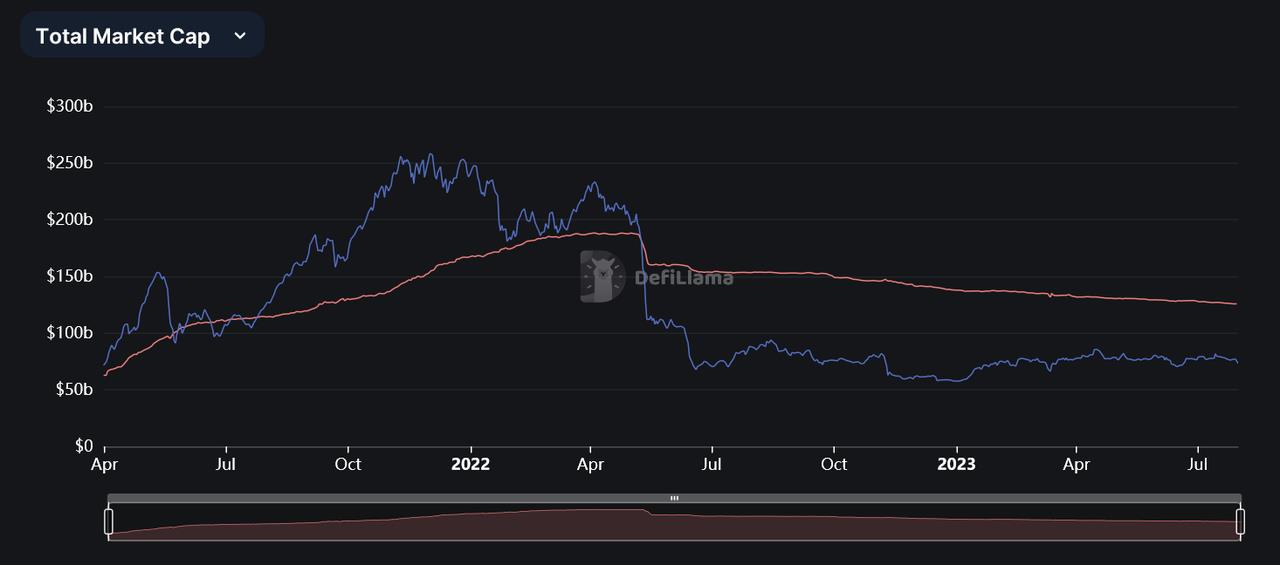

(1) U-denominated investors gain access to a relatively safe and stable yield-generating venue even during bear markets. For example, after the market began turning bearish in mid-2021, the total stablecoin market cap declined from $188 billion to under $130 billion today. This reduction has also impacted overall market liquidity;

(2) Hybrid equity-bond financial products become easier to launch and gain market acceptance. Such blended products are already familiar to most investors in traditional finance, and their introduction will further drive innovation in DeFi asset management.

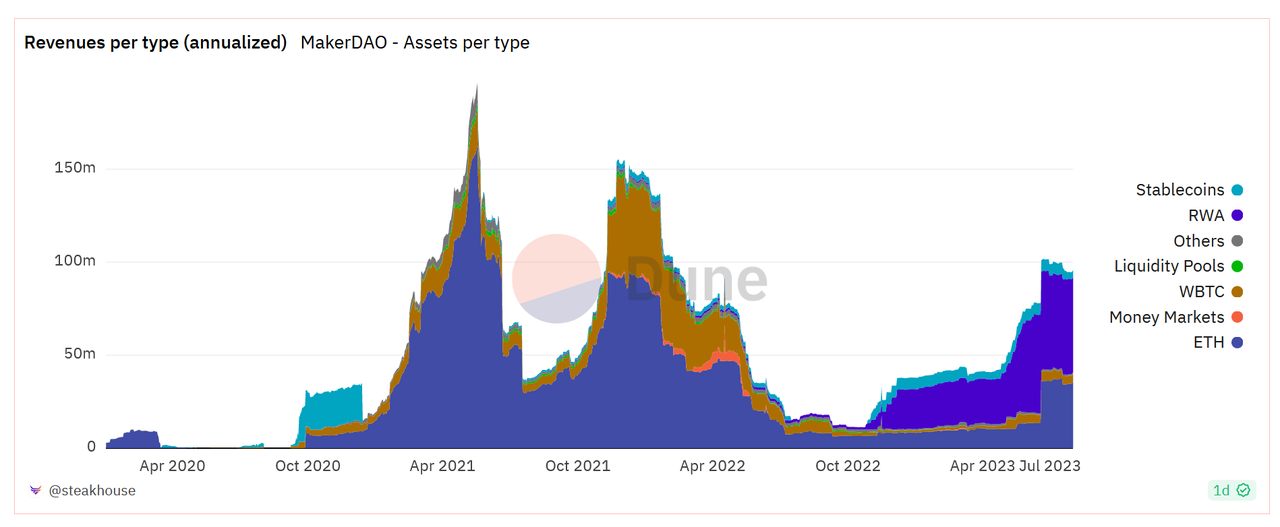

A prominent current example is MakerDAO. After shifting its investment focus to U.S. Treasuries amid rising yields during the bear market, MakerDAO's profitability significantly improved starting in 2023.

Therefore, it is reasonable to expect that other DeFi protocols, seeing MakerDAO’s success as a model, will seek to enhance their own profitability through diversified strategies including RWA investments. Especially during bear markets, RWAs can provide stable and sufficient revenue streams critical for project sustainability.

2. Business Models of Government Bond RWAs

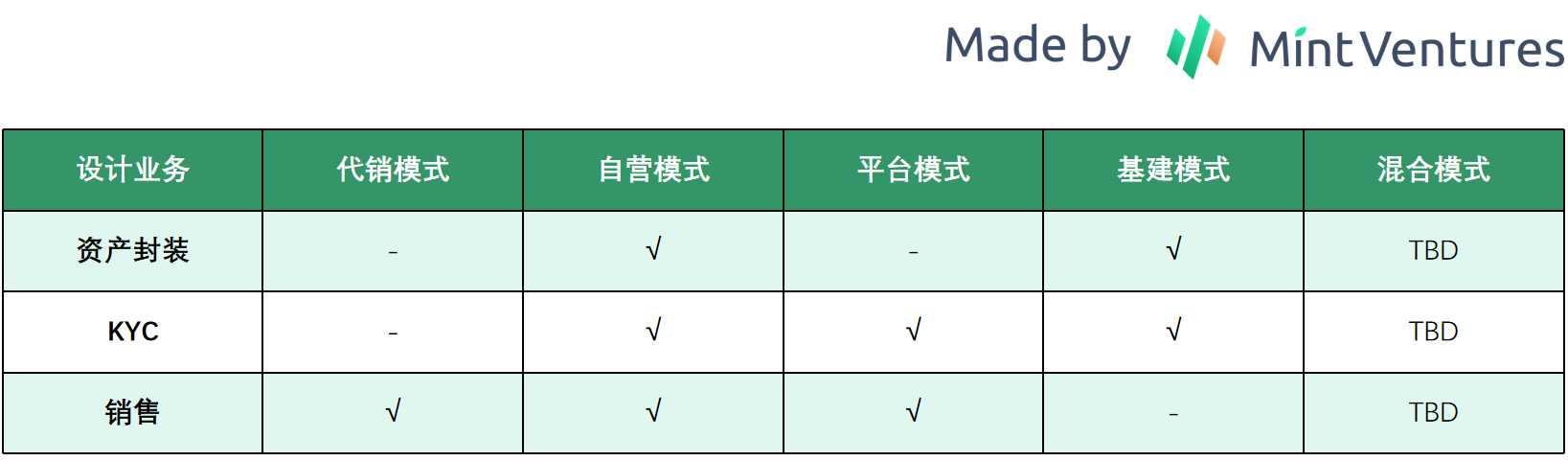

Currently, five primary business models have emerged in the government bond RWA space: Distribution Model, Platform Model, Infrastructure Model, Proprietary Model, and Hybrid Model.

Distribution Model: These projects do not directly participate in underlying asset tokenization nor offer KYC services. Instead, they focus on crypto-native user acquisition, emphasizing marketing, capital raising, ecosystem development, and use-case expansion. Representative examples include TProtocol. These projects operate similarly to foundational DeFi protocols like Aave or Compound—typically pooling user funds via liquidity pools and lending them out to a single borrower who purchases U.S. Treasuries or similar assets.

Platform Model: The project provides services such as onboarding assets onto the blockchain, sales infrastructure, and KYC solutions, but does not directly engage in asset tokenization itself. Examples include Desmo Labs. These platforms generally offer three core services:

(1) Asset/equity tokenization;

(2) On-chain verifiable information services;

(3) User KYC services. In theory, such platforms can support tokenization of any traditional financial asset—not limited to government bonds—and resemble internet platform businesses. To succeed, these projects must deliver user-friendly end-to-end solutions and demonstrate strong customer acquisition capabilities.

Infrastructure Model: These projects provide services related to RWA tokenization, asset purchasing, and asset management, but do not directly interact with retail (C-end) or institutional (B-end) investors buying treasury products. Notable examples include Centrifuge and Monetalis Group.

Proprietary Model: Projects using this model source assets independently, collaborate with external partners to build operational frameworks, ensure proper risk isolation, and tokenize the resulting assets or rights. Many current projects follow this model, including MakerDAO, Franklin OnChain U.S. Government Money Fund, and Frax Finance. This approach involves greater off-chain complexity compared to the first two models, requiring significant effort in legal structuring, corporate organization, partner selection, and asset management. However, a key advantage lies precisely here: greater control over underlying assets enables proactive risk management.

Hybrid Model: Combines aspects of the above four models. These projects may offer their own onboarding, KYC, and other services while also sourcing assets directly and offering investment opportunities to users. Fortunafi is a representative example. It offers four main services:

(1) Access Capital – providing funding channels for borrowers;

(2) Earn Yield – allowing users who complete KYC to directly invest in pre-packaged assets;

(3) Protocol Services – offering governance and treasury management tools for other protocols;

(4) Whitelabeled Products – delivering full-cycle RWA tokenization services. Naturally, these projects are not limited to treasury bonds and can support tokenization of various other asset classes.

Beyond these five models, there are also pure-play trading infrastructures such as DEXs serving the RWA ecosystem—for instance, DigiFT. However, since such projects do not participate in asset selection, tokenization, or distribution processes, we will not elaborate on them here.

3. Asset Side: Underlying Assets and Structural Architecture

3.1 Underlying Assets

The market currently features several types of underlying assets:

(1) U.S. Treasury ETFs. Projects adopting this type include Backed Finance, Swarm, MakerDAO, and ARKS Labs. The main advantage is simplicity—the ETF issuer handles asset management, including liquidity and roll-over operations—relieving project teams of direct responsibility. Given that U.S. Treasury ETFs have historically avoided major risks, operational risk for these projects remains low. They simply need to select the largest and most liquid ETFs available.

(2) Direct U.S. Treasury Bonds. Projects in this category include OpenEden, TrueFi, and Matrixdock. These typically invest in short-term Treasuries, offering near-cash liquidity. However, because the project directly selects custodial partners, it assumes responsibility for asset management risk—making partner selection crucial.

(3) Composite portfolios combining U.S. Treasury Debt, U.S. Government Agency Debt, and Cash / Repurchase Agreements (Repos). Projects using this structure include Franklin OnChain U.S. Government Money Fund, Superstate Trust, TProtocol, Arca Labs, and Maple Finance. Similar to ETF-based models, these delegate asset management to professional managers. However, issues related to rollover and liquidity remain tied to the project’s oversight. Operationally, failure to select high-quality managers could lead to problems.

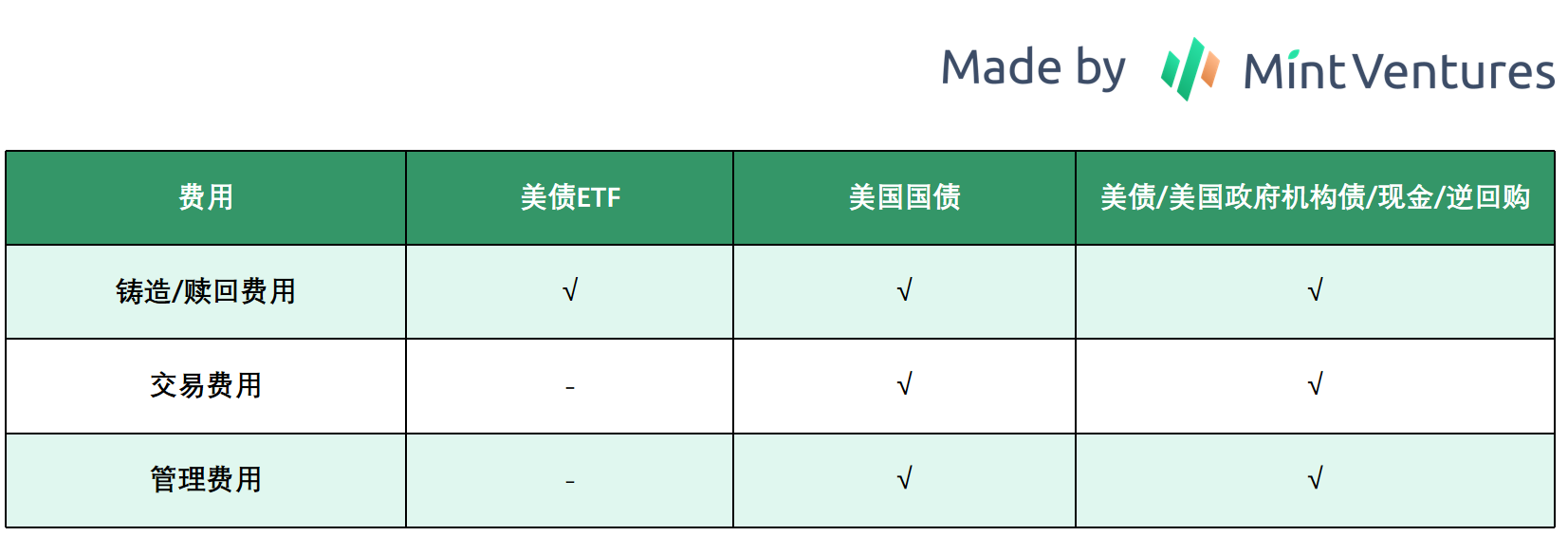

3.2 Fee Structure

The three types of underlying assets discussed above result in different fee structures. Excluding gas fees associated with on-chain transactions, the main cost components are illustrated below:

For ETF-based products, management is outsourced to the ETF provider. Therefore, the main costs occur during minting and redemption, typically ranging from 0.05% to 0.5%. For the latter two models involving direct asset management, additional management and transaction fees apply. Management fees range from 0.3% to 0.5%, while transaction fees—covering bank wire charges and similar costs—are around 0.2%.

3.3 Asset Business Architecture

Differences in underlying assets also affect the overall business logic and architecture. Current market approaches include the following:

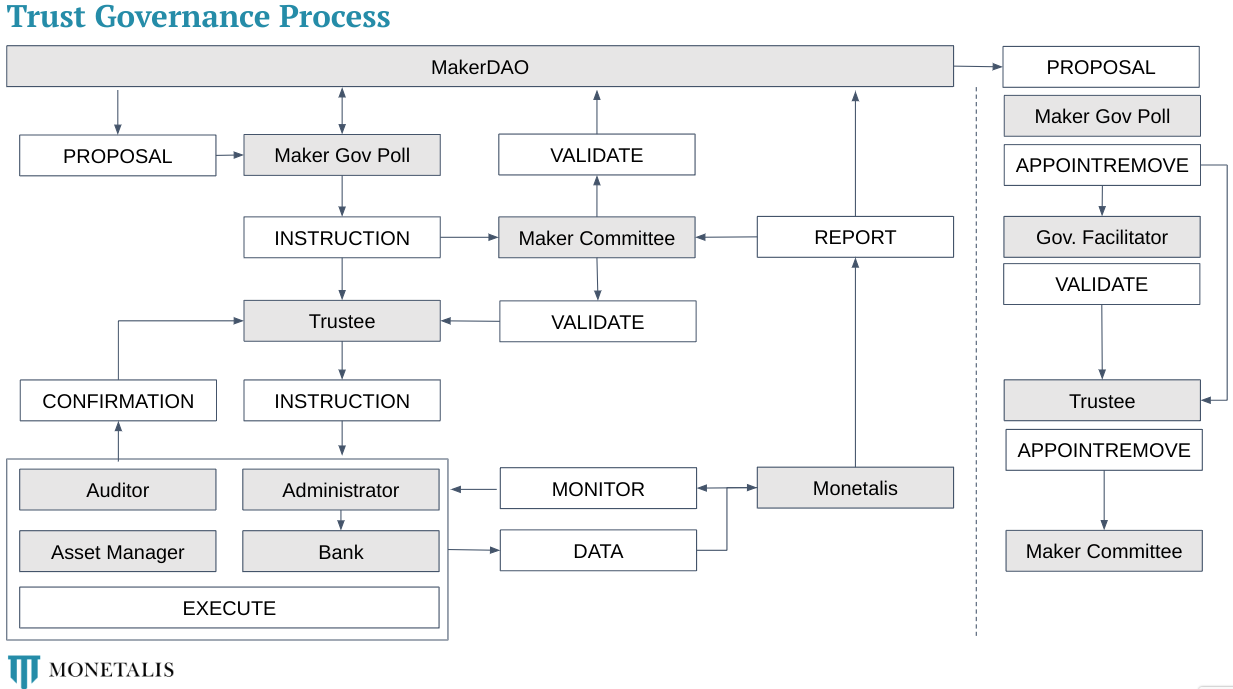

(1) Trust Structure: Used by projects such as MakerDAO.

In a trust setup, the sponsor transfers assets to a Special Purpose Vehicle (SPV), establishing a trust relationship. The sponsor receives beneficial interest, which is then transferred to retail investors. Using MakerDAO’s U.S. Treasury RWA as an example, roles such as manager and auditor are involved, with part of the off-chain structure built by Monetalis Group. Monetalis handles asset purchases, periodic reporting, and on-chain updates. Within this framework, MakerDAO influences decisions such as scale and asset purchases through governance mechanisms.

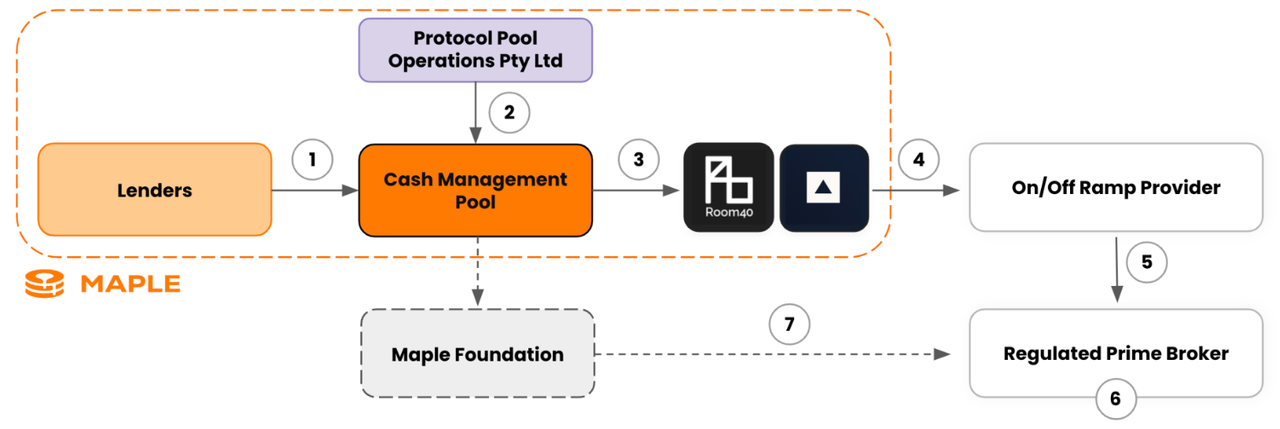

(2) Limited Partnership SPV Structure: Adopted by projects like Maple Finance and Matrixdock. The project team actively participates in sourcing assets and securing liquidity.

An SPV (“Special Purpose Vehicle”) primarily functions to raise capital from investors during asset securitization or purchase. Originally designed for bankruptcy remoteness, SPVs have evolved beyond this initial purpose. Modern SPVs offer several advantages:

(1) Simplified financial management, avoiding the complex departmental dependencies and unclear workflows typical of traditional corporate structures;

(2) Enhanced transparency and traceability. Typically, one SPV corresponds to one project or asset, simplifying oversight. For example, individual mortgage details are rarely disclosed in a commercial bank’s public reports—such information may only exist internally for managerial accounting. But when packaged into an SPV, detailed disclosures become standard practice, including loan duration, interest rates, collateral, and sometimes even per-loan specifics—greatly enriching available data;

(3) Tax efficiency. For certain assets, SPVs benefit from lower tax rates.

This architecture consists of two layers:

Layer 1: Users and SPV – Users hold claims against the SPV; their returns depend on the SPV fulfilling its obligations;

Layer 2: SPV and Commercial Banks – The SPV participates in the Treasury market and engages in repo transactions within the interbank market. If counterparty defaults occur in these repos, the risk exposure may exceed that of holding direct U.S. Treasuries.

Additionally, users face an extra layer of risk: the SPV itself may encounter operational or solvency issues.

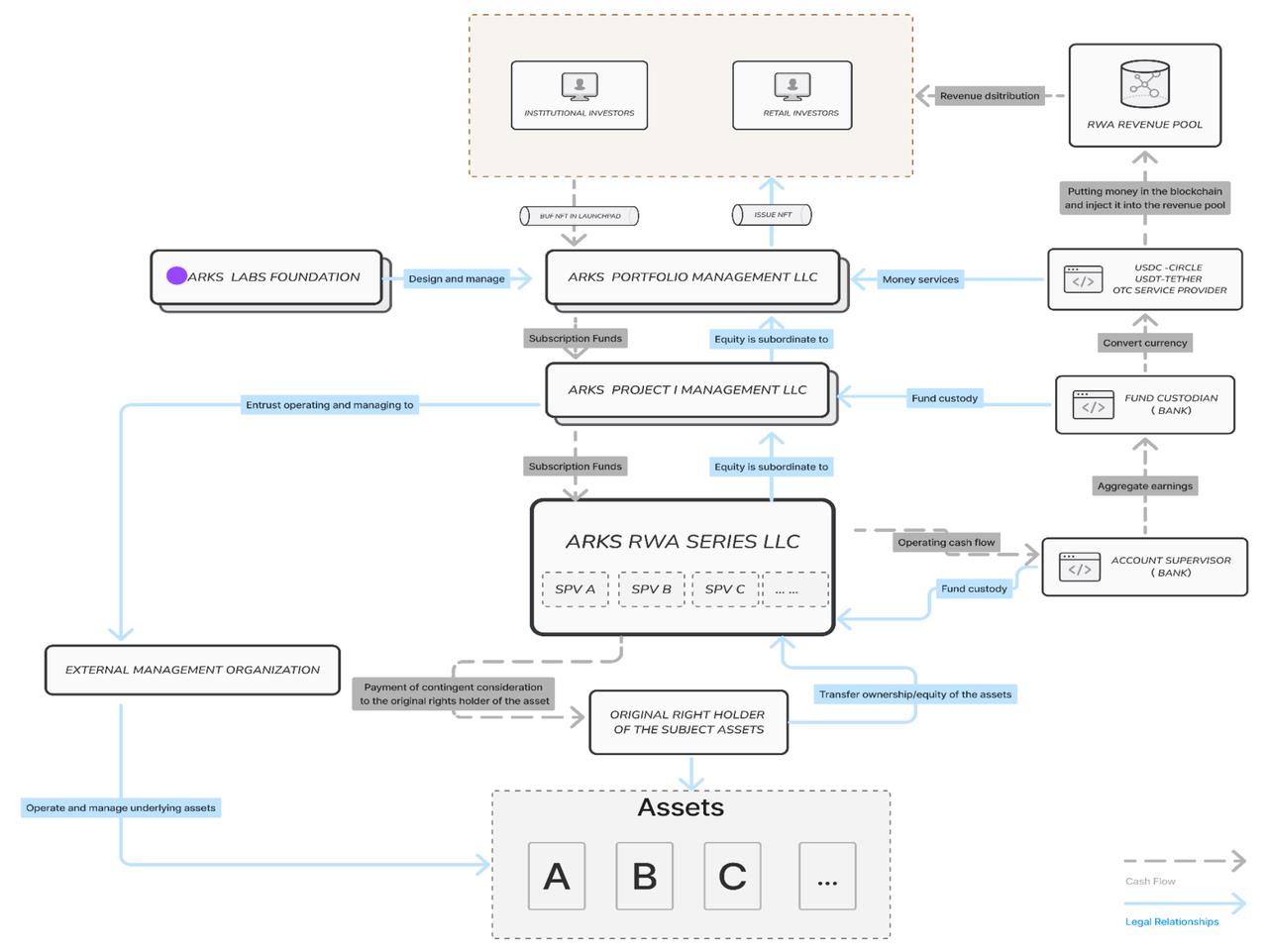

ARKS Labs extends this model by nesting smaller SPVs within a larger framework, enabling scalability and ease of adding new underlying assets—similar to the architecture described earlier in our article “Ramblings on RWAs: Underlying Assets, Business Structures, and Their Evolution.”

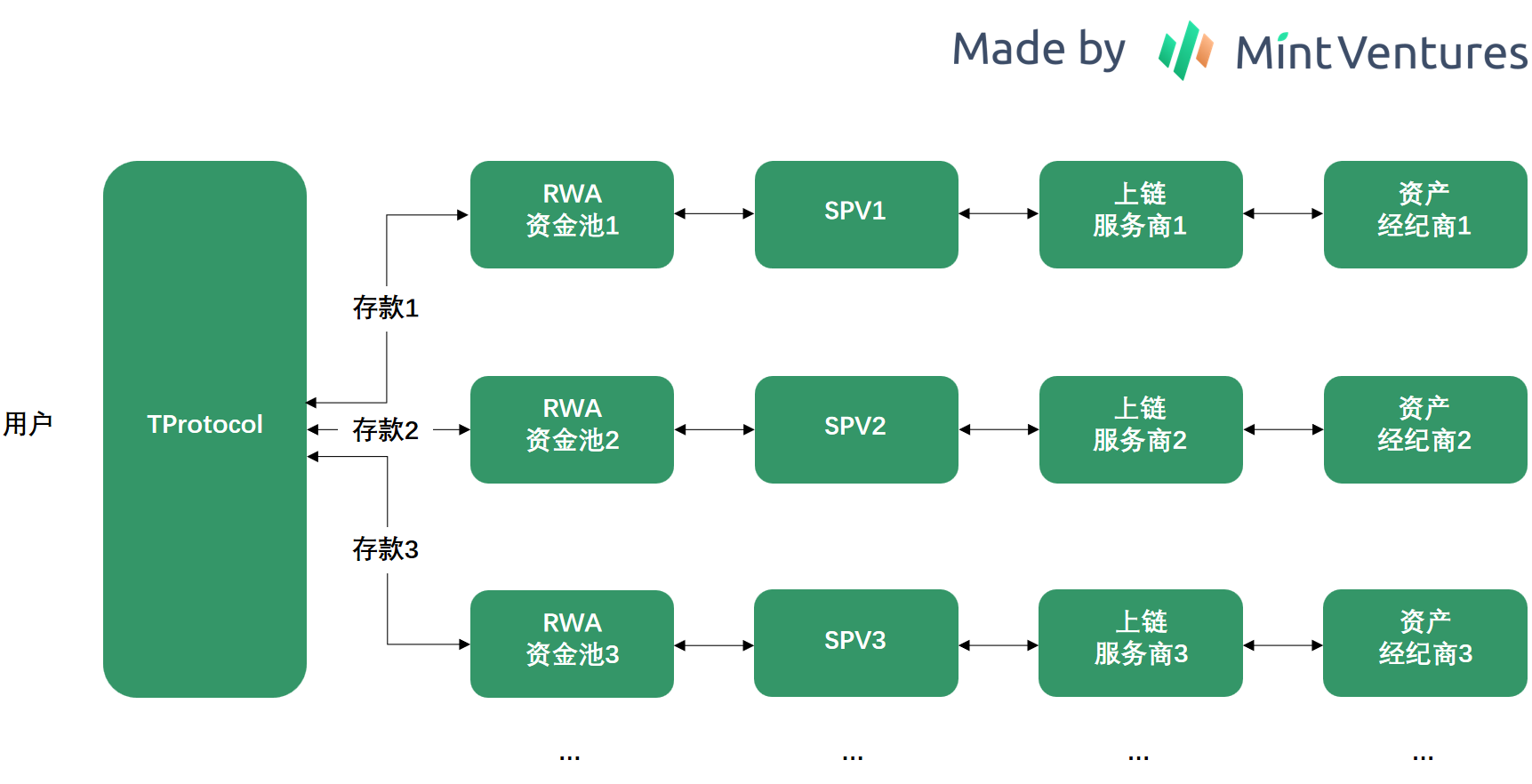

(3) Lending Platform + SPV Structure: Used by TProtocol. Unlike the previous SPV model where the project team is directly involved in asset sourcing and packaging, in TProtocol’s case, the SPV is independent of the protocol and instead belongs to the RWA originator.

As shown in the diagram, SPVs can be initiated by various institutions, with different service providers handling on-chain integration and brokerage. This makes TProtocol’s structure more flexible—but not without trade-offs: as the number of partners increases, oversight and management capabilities over downstream SPVs may weaken.

(4) Tokenized Mutual Fund Shares: Similar to traditional fund investing, requiring precise mapping between investor identities and wallet addresses. Franklin OnChain U.S. Government Money Fund uses this structure. These projects resemble what was previously termed “blockchain transformation”—where off-chain assets and investor data are brought on-chain, with future transfers recorded both off-chain and mirrored on-chain via bookkeeping.

Although the RWA sector is still in its early stages—with modest user and capital scales placing limited demands on architectural design—the scalability of these architectures becomes increasingly important as government bond RWAs gain investor recognition. The ability to rapidly tokenize new assets and integrate additional off-chain service providers may determine competitive advantage during periods of rapid growth.

4. User Side: KYC and Other Requirements

Due to differences in underlying assets and business structures, projects impose varying requirements on users. Currently, distinctions mainly fall into three categories:

(1) Minimum Investment Threshold: Projects such as MakerDAO, ARKS Labs, and TProtocol do not set minimum investment amounts. Others—including Maple Finance, TrueFi, Arca Labs, and Backed Finance—impose clear thresholds. No-minimum models better align with current DeFi user expectations, while those requiring $100,000+ typically target high-net-worth individuals.

(2) KYC Requirements: Based on KYC intensity, projects fall into three groups: no KYC required (e.g., Flux Finance, ARKS Labs, TProtocol); lightweight KYC (e.g., Desmo Labs, requiring passport uploads); and full KYC (e.g., OpenEden, Ondo Finance, Maple Finance, Matrixdock), demanding documentation comparable to traditional finance. High KYC barriers are not only perceived as restrictive in traditional finance but are also poorly received by many current DeFi users.

(3) Other Restrictions: Some projects limit eligibility based on geography—for example, serving only non-U.S. residents, or excluding users from the U.S., Singapore, and Hong Kong. Such restrictions are often enforced via IP blocking.

Many projects rely on third-party KYC providers to verify user compliance, without directly participating in the review process themselves.

5. Yield Distribution Strategies and Composability

5.1 Yield Distribution Strategy

Two primary yield distribution models currently dominate the market:

The first and most common model distributes yield directly via debt claims. Regardless of whether users hold SPV debt or exposure to Treasury ETFs/bonds through other structures, they receive nearly all of the underlying Treasury yield. After deducting minting/redeeming and intermediary fees, net yields are approximately 4 percentage points.

This mirrors the LSD model: most staking rewards are passed back to users, with only small fees retained.

The second model is currently unique to MakerDAO: yield is distributed via a deposit rate mechanism. Since user funds are not directly linked to specific assets, MakerDAO operates similarly to a commercial bank using interest rate spreads: on the asset side, deploying capital into higher-yielding instruments like RWAs; on the liability side, adjusting user returns via the DSR (Dai Savings Rate). To date, DSR has been adjusted four times: (1) from 1% to 3.49%; (2) from 3.49% to 3.19%; (3) from 3.19% to 8%; (4) from 8% down to 5%.

This approach gives the team greater flexibility, but comes with obvious drawbacks: users lack a clear analytical framework for predicting future yields. With Treasury RWAs, investors naturally expect returns close to actual Treasury yields. Yet monetary policy adjustments—such as MakerDAO recently allocating excess profits to depositors, pushing rates up to 8%—can cause volatility. As more depositors join, yields may drop back toward prevailing Treasury levels. Such fluctuations are unattractive to investors seeking stable returns.

For Treasury RWAs, clear and predictable yield expectations are essential. Thus, the first distribution model is likely superior. However, if a project using the second model clearly anchors its yield to Treasury benchmarks, the practical difference between the two models diminishes.

5.2 Composability

KYC requirements also impact the composability of Treasury RWA tokens:

Strict-KYC projects such as Ondo Finance, Matrixdock, and Franklin OnChain U.S. Government Money Fund enforce address whitelisting. Even if corresponding token pools exist on-chain, unrestricted trading is not possible. Unless these projects grow large enough in asset scale, gaining broad DeFi protocol integration and rich composability will remain challenging.

Conversely, no-KYC projects face no inherent composability barriers. The only limitations to their integration stem from their own business development resources, partnership strength, and overall scale.

6. Conclusion

By analyzing existing government bond RWA projects, we can begin to identify potentially winning business models in the near to medium term:

Underlying Assets: Utilizing Treasury ETFs may be a clever shortcut, outsourcing liquidity and rollover management to established players in traditional finance. Direct Treasury or composite asset purchases place greater emphasis on the project’s ability to select reliable partners.

Business Architecture: Proven structural models already exist and should be adopted with strong scalability to allow rapid expansion and future inclusion of new asset classes;

User Experience: In the short to medium term, projects without KYC and minimum investment thresholds will attract broader user bases. If regulation eventually mandates KYC, lightweight-KYC models may become dominant;

Yield Distribution: To give Treasury RWA investors stable and reliable yield expectations, the optimal approach is to maintain a consistent ratio between user returns and actual Treasury yields;

Composability: Before regulators restrict access to on-chain RWA assets, maximizing the utility and integration scenarios of RWA tokens will be crucial for long-term growth.

In the longer term, increasing regulatory scrutiny may favor lightweight-KYC projects, giving them greater competitive opportunity.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News