Deep Dive into MakerDAO's Past and Future: Long-Term Value Undervalued, More Catalysts Ahead

TechFlow Selected TechFlow Selected

Deep Dive into MakerDAO's Past and Future: Long-Term Value Undervalued, More Catalysts Ahead

MakerDAO is by far the largest decentralized stablecoin, and new products on V3 will only strengthen its leading position.

Author: PEARY

Translation: TechFlow

This article will first explore the entire stablecoin industry, then introduce MakerDAO in three stages: past (V1), present (V2), and future (V3).

1 Stablecoins

Due to the early stage, illiquidity, and speculative nature of cryptocurrencies, they are highly volatile. The first stablecoin launched in 2014 aimed to mitigate this volatility, and since then, fiat-backed stablecoins have become a crucial part of the ecosystem. They create a more efficient, stable, and accessible experience for everyone. Common use cases include:

-

Store of value: Reducing overall volatility of digital portfolios. Without stablecoins, all crypto wallets would suffer extreme fluctuations.

-

Remittances: Sending money becomes simple, faster, more efficient, and free of fees or cumbersome procedures for everyone.

-

Trading: Enables trading on exchanges without traditional bank accounts. Exchanges can settle trading pairs using stablecoins like USDT instead of settling everything in USD.

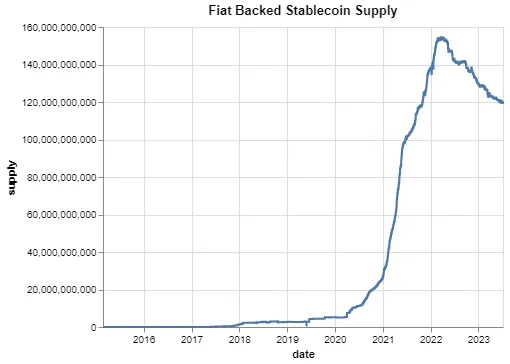

Below is a chart showing the total market cap of the six largest fiat-backed stablecoins. At the peak of the last bull run, stablecoin market cap reached about $160 billion and now stands slightly above $120 billion, accounting for over 10% of the entire cryptocurrency market. Approximately 70% of supply is in USDT, with another 25% in USDC.

1.1 Profitability

Stablecoins are one of the few profitable areas within the cryptocurrency ecosystem because they deploy dollars into yield-generating assets. From Tether's publicly disclosed balance sheet, we see it holds approximately $81.8 billion in assets and $79.4 billion in liabilities (USDT market cap), generating $1.48 billion in profit in just the first quarter. They achieve this by re-pledging consumer-held assets into safe investments like short-term Treasuries, which currently yield over 5%. For example, investing $80 billion into short-term Treasuries allows Tether to earn around $4.5 billion in profit annually.

As an unusual profitability benchmark, Coinbase—the second-largest spot exchange by volume—earned only $736 million in total revenue and actually incurred losses after expenses. Many crypto companies are private with limited public information, but we can speculate that Tether (and Circle, the parent company behind USDC) likely earns more than all other crypto companies combined (excluding Binance). Unfortunately, the general public currently cannot invest in Tether (USDT) or Circle (USDC), as they are private companies with no current plans for listing.

1.2 Other Types of Stablecoins

This isn't to say fiat-backed stablecoins are risk-free. Just months ago, due to Silicon Valley Bank (SVB) freezing $3.3 billion in funds, USDC’s peg dropped to about $0.87. For better or worse, fiat-backed stablecoins heavily rely on external factors such as the banking system. To date, the U.S. Federal Deposit Insurance Corporation (FDIC) has not fully paid out all depositors, leaving roughly $1.9 billion still outstanding.

Two other notable types of stablecoins are algorithmic stablecoins and crypto-collateralized stablecoins. A famous example of an algorithmic stablecoin is UST, which collapsed in a single day, wiping out $20 billion in value. Crypto-collateralized stablecoins theoretically avoid the death spiral pressure seen in algorithmic versions and are less dependent on the banking system. This article focuses on the history of MakerDAO—the most popular issuer of crypto-collateralized stablecoins—and its current role in the ecosystem, why we believe it is a solid investment today, and its future roadmap.

2 SAI: V1

While fiat-backed stablecoins were emerging, people began experimenting with alternative backing mechanisms. MakerDAO was one such project—one of the largest and oldest decentralized applications focused on supporting stablecoins using cryptocurrencies (rather than fiat). Initially, the goal was to build an over-collateralized decentralized stablecoin backed solely by ETH, launching this prototype in 2017. Decentralized stablecoins offer many of the same advantages as centralized fiat-backed ones, while also providing trustlessness and reduced counterparty risk. The first version worked as follows:

Jill deposits ETH into a MakerDAO smart contract and can then mint SAI (a stablecoin) at a 150% collateral ratio: meaning $150 worth of ETH can mint up to 100 SAI. The smart contract sends the SAI to Jill, records the amount issued as debt, and locks her collateral until the debt is repaid.

Jill can then use her newly minted SAI while maintaining exposure to the ETH she deposited in the smart contract. A typical use case is exchanging SAI for more ETH, effectively creating a leveraged position. In the example above, if Jill swaps all her SAI for ETH, she gains exposure to $250 worth of ETH despite starting with only $150 worth, achieving 1.6x leverage.

To protect the collateral, ensure MakerDAO doesn’t take on bad debt, and accumulate protocol revenue, Jill must monitor her collateralization ratio and pay the stability fee (an interest rate paid by minter). If the value of her ETH falls below the 150% threshold, part of her collateral may be liquidated to bring her back to 150% (set by governance).

This early version of MakerDAO significantly improved capital efficiency for ETH holders. To redeem her collateral, Jill simply needs to “burn” the SAI she minted (plus any accrued interest) by returning it to the smart contract, which then unlocks her ETH. It’s important to note that parameters governing the MakerDAO dApp—such as collateral ratios and stability fees—are determined via MKR token-based governance.

2.1 Product-Market Fit

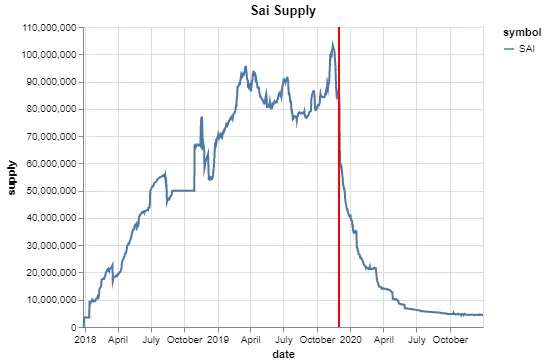

From the SAI supply chart, strong traction and product-market fit are evident from day one, similar to fiat-backed stablecoins. Supply grew beyond $100 million by November 2019, after which MakerDAO upgraded to its second version, marked by the red vertical line. Perhaps even more telling of SAI’s appeal is the emergence of other crypto-collateralized stablecoins such as Frax, Fei, Liquity, RAI, and Alchemix.

3 DAI: V2

In 2019, MakerDAO upgraded to version V2, allowing multiple collateral types to mint DAI—a new stablecoin replacing SAI across the ecosystem. Thus, in addition to ETH, other assets (approved via MKR governance votes) could now mint DAI. Essentially, this update increased the circulating supply of DAI and reduced volatility in DAI supply tied to ETH price swings. Today, various assets serve as collateral, including liquid staking derivatives (stETH and rETH), wBTC, ERC-20 LPs, and real-world assets (RWAs) such as Treasuries.

The next section describes the protocol’s current state and details MakerDAO’s various revenue streams.

3.1 V2 Overview

3.1.1 Dai Savings Rate (DSR)

Beyond multi-collateral support, V2 introduced several notable improvements, such as the Dai Savings Rate (DSR), incentivizing users to hold Dai. DSR is a benchmark interest rate available to any Dai holder who deposits their Dai into a dedicated DSR contract. The current DSR is 3.49%, serving as a baseline "risk-free" rate in crypto. There are no minimum deposits or withdrawal fees, and the Maker protocol allocates a portion of its income to all DSR depositors.

3.1.2 Dai Collateral

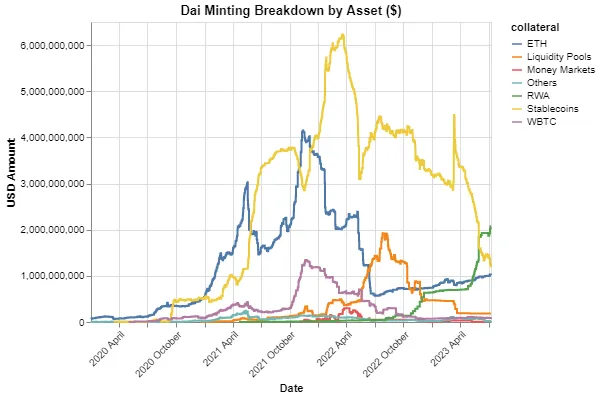

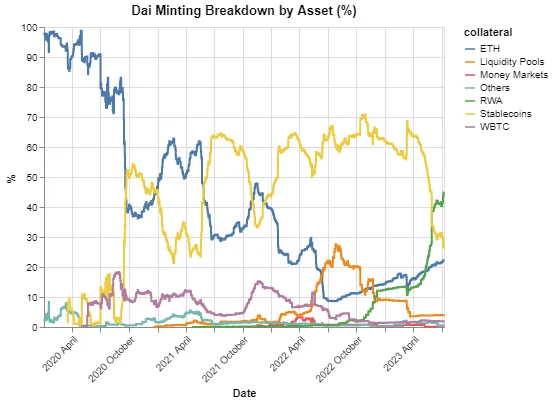

MakerDAO generates revenue primarily by charging stability fees to borrowers minting Dai. Currently, there is approximately $9.1 billion in total value locked (TVL) in the Maker protocol, with about $4.6 billion worth of Dai issued. Initially, Ethereum was the primary method for issuing Dai, likely carried over from the SAI era due to user familiarity. Early on, DAI consistently traded above its peg as users sought to deploy DAI into liquidity mining opportunities. MIP-21 created the Peg Stability Module (PSM)—a programmatic vault allowing stablecoins like USDC to mint Dai at a 1:1 ratio without paying a stability fee, which triggered explosive growth in DAI supply.

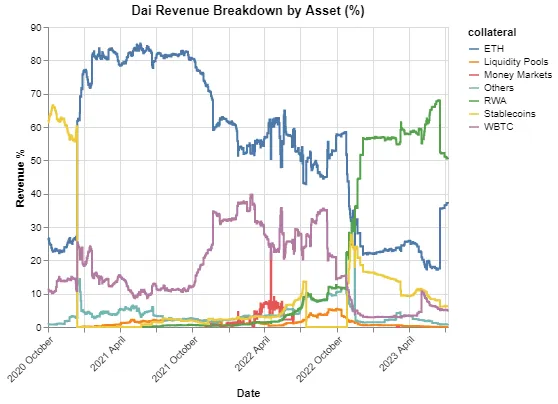

More recently, MIP-65 allowed real-world assets (RWAs) into the Maker protocol, and this segment’s share has steadily grown. In just over a year, RWAs’ share of DAI collateral has risen from zero to nearly 50%.

3.2 V2 Profitability

3.2.1 Dai Revenue

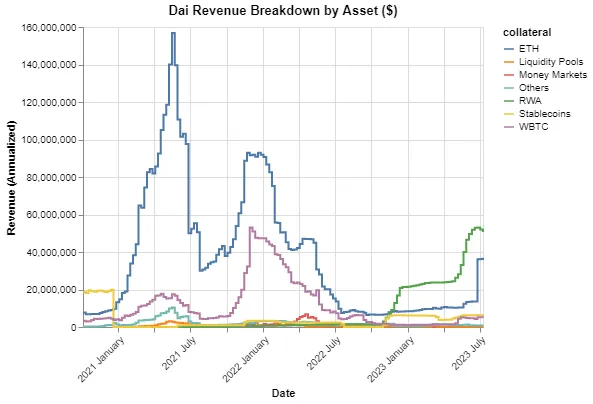

In this new multi-collateral environment, stability fee percentages vary by asset class, while real-world assets do not charge stability fees. Instead, yields flow into the surplus buffer—an insurance fund designed to absorb potential losses. Below is a breakdown of revenue by asset class. We can see that initially, most revenue came from ETH stability fees (and to a lesser extent WBTC). However, starting early this year, MakerDAO followed its fiat-backed peers USDT and USDC by allocating most of its capital into real-world assets. Now, over 50% of revenue comes from these short-term Treasuries and similar instruments. Note that this breakdown reflects unrealized P&L; future figures will be higher as both stability fees and real-world yields increase.

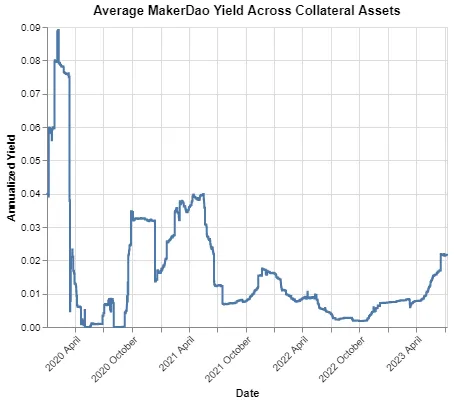

3.2.2 MakerDAO Yield

How much yield does MakerDAO generate on its assets? Below we see annualized returns are highly volatile. MakerDAO is gradually increasing its total yield, primarily by converting non-yielding stablecoins into productive assets.

3.2.3 Expected Revenue

Specifically, the protocol earns about 3.79% yield from ERC-20 stability fees, equating to roughly $3.57 million monthly and $42.8 million annually. Real-world asset yields are also relatively stable due to lower interest rate volatility and slower adjustments.

3.2.4 Other Income

In addition to stability fees and real-world asset yields, MakerDAO earns revenue from liquidations. These revenues are irregular and occur mainly during market volatility (typically downward moves). As a reference, the monthly average liquidation P&L over the past year was $1.37 million, though some months (like January) saw zero, while others (like October 2022) reached $3.92 million.

Additionally, there are PSM issuance fees and flash loan fees, but these are negligible in overall profitability. Including liquidation income, we arrive at expected annual revenue of $138.24 million and monthly revenue of $11.57 million. Notably, these figures are extremely high compared to other decentralized protocols aside from fiat-backed stablecoins.

3.2.5 Expenses

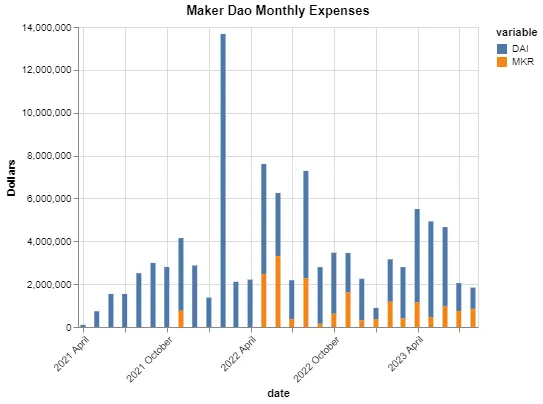

To infer overall profitability, we must consider expenses—including core development teams, managers, risk officers, lawyers, and various other costs required to operate a large decentralized organization. These figures constantly evolve as new programs are introduced, making future predictions difficult.

Expenses over the past 12 months totaled approximately $38 million: $29 million in DAI and $9 million in MKR. Importantly, while many new spending initiatives have been approved, most legacy core units are exiting, so past expenses are not reliable indicators of future costs, and some approved plans may never materialize. Expenses could rise or fall.

3.2.6 Profitability

Subtracting expenses from revenue, we get approximately $100 million in annualized profit. Aside from the aforementioned stablecoins and a few exchanges, almost no other decentralized application is more profitable. MKR has a market cap of about $820 million. While we (and many in crypto) dislike applying traditional financial metrics to assess crypto protocols—preferring internal KPIs—this implies a P/E ratio of 8.2. The market prices MakerDAO like a mature bank stock, valuing its revenue based on yield generation, while stripping away all future growth potential.

3.3 MKR Token (Immediate Catalyst)

In crypto, there is often friction between protocol value accrual and token value accrual. It is well known that dYdX does not return profits/revenue to token holders. But MKR is different. Once the surplus buffer reaches a certain level, the protocol buys back and burns MKR. Weeks ago, the Smart Burn feature was introduced: instead of pure buybacks, half the surplus funds are used to buy MKR, while the rest provide liquidity to the MKR/DAI Uniswap V2 pool. Unlike burning, purchasing and providing liquidity reduces MKR volatility during both up and down markets while capturing trading fees.

3.3.1 SmartBurn

The surplus buffer ceiling was recently adjusted from $250 million down to $50 million. Any excess DAI will trigger the Smart Burn mechanism. Given our current surplus of ~$80 million, the protocol will swap and pool $5,000 worth of DAI every half hour until the surplus buffer returns to $50 million—equivalent to a 125-day TWAP buy order.

Note that the Smart Burn mechanism has not yet been activated. Its activation will mark the beginning of MakerDAO’s third version—Endgame. This protocol-owned 50/50 MKR/DAI UniV2 pool, called Maker Elixir, will enhance MKR liquidity, provide consistent buying pressure, and capture trading fees.

3.3.2 Additional Revenue

There is $500 million in USDC sitting idle in the PSM, generating no yield. PSM outflows have finally slowed, and a contract with Blocktower has been signed to gradually deploy these dollars, potentially generating over 4.5% yield and adding $22.5 million in annual revenue for MakerDAO. If rates remain stable, we expect MakerDAO to easily surpass $150 million in annual revenue by year-end, bringing its P/E ratio down to 6 (assuming price remains unchanged).

3.4 Problems

V2 has several significant issues, some interrelated:

-

MakerDAO is overly complex and disorganized, leading to numerous divisions and fractures. This leads to inefficiencies.

-

DAI supply is trending downward and needs to be reversed.

-

MKR token lacks real utility beyond governance and offers insufficient incentives for voting on most proposals.

3.4.1 Governance Issues

A major issue with V2 is governance apathy, resulting in a sluggish environment—often opposite to its competitors. On average, each MIP takes over two months from proposal to approval, and actual participation is minimal. Fewer than 40 independent individuals vote on each action, and votes typically pass with only 5–10% of total supply. In a recent vote, one individual contributed 88% of the voting MKR.

To be fair to voters, MakerDAO is extremely comprehensive; making informed decisions is essentially a full-time job requiring deep understanding—from RWAs to optimal liquidation parameters. However, this slow pace makes MakerDAO inefficient and suboptimal in value capture. Especially regarding stability fees, governance has historically been too slow to adjust rates during market ups and downs.

3.4.2 Inefficiency in Yield Optimization

Proper yield optimization requires continuous review, precise monitoring, and accurate reporting. These characteristics do not currently apply to many RWA vaults.

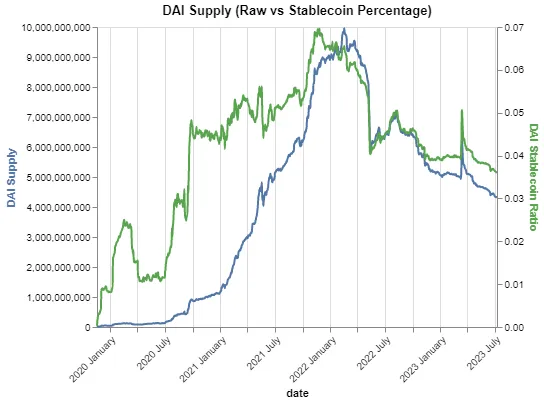

3.4.3 Declining DAI Supply

Below is a time series chart of original DAI supply and DAI’s percentage share of the total stablecoin market cap. Throughout the bull run, stability fees were too low, causing DAI’s market share to rapidly grow from 1% to nearly 7% near the peak, but failing to capture sufficient revenue. Since November 2021, the trend has reversed due to excessively high stability fees—especially compared to other protocols. DAI’s market share has declined from a peak of 7% to about 3.5%, and supply has dropped from $10 billion to just over $4 billion, largely due to higher fees relative to other DeFi lending markets.

Notably, the remaining supply of over $4 billion in DAI is quite stable, as many of the top 50 wallets are smart contracts, hackers, or scammers.

3.4.4 No Real Value Accrual

Crypto Twitter is, at its best, a place where ideas stand on their own merit because everyone is anonymous. At its worst, it’s a broken record of noise with little independent thought. A well-known account named DegenSpartan has criticized MKR for the past four years. He raised some valid questions, but more importantly, the charts align with his arguments.

We’ve recently seen one of the worst-performing charts, especially when observing the red MKR/ETH ratio. The chart resembles constant selling pressure with no buying support—first due to negative spillover from the UST collapse affecting the broader stablecoin sector, then because MakerDAO increased its surplus buffer to $90 million, then $250 million, before pausing buyback and burn programs over the past year and a half. However, Smart Burn has now passed to address this issue.

3.5 V2 Conclusion

The current version of Maker is one of the most profitable protocols in crypto. Earning $100 million annually (and growing), the market values the token like a mature bank stock with no upside or future plans priced in. If we break down MakerDAO’s cash flows and assume the Maker token has no further utility, it would be the cheapest cryptocurrency from a price-to-earnings perspective.

This isn’t to say MakerDAO V2 is without flaws—inefficient revenue capture due to core governance weaknesses, a non-value-accruing token, declining demand for DAI, and poor sentiment and price performance within the broader crypto community.

All these issues contribute to a massive disconnect between fundamentals and price. MakerDAO’s new version V3 aims to inject strong momentum into the protocol, increasing TVL, stability fees, and introducing a suite of new value-capture mechanisms for the MKR token, hoping to reverse sentiment and price trends.

4 Endgame: V3

MakerDAO founder Rune has been working on V3 development for over a year. The new version will bring sweeping changes to governance operations, tokenomics, and numerous decentralized applications, aiming to make MakerDAO the largest and most widely used stablecoin project in the coming years. Aptly named “Endgame,” this upgrade seeks to establish a powerful and enduring end state where MakerDAO’s core remains unchanged.

The document highlights the following goals, among others:

-

Achieve global mass accessibility of DAI;

-

Create steps toward decentralizing and expanding the Maker ecosystem;

-

Reduce MKR centralization through new tokenomics and distribution methods;

-

Reduce governance burden on MKR holders.

Perhaps more importantly, it attempts to solve all major pain points of V2.

4.1 Overview

4.1.1 subDAO (Efficient Revenue Extraction)

To achieve the above goals, tasks will be reorganized into smaller, more agile subDAOs. For example, a subDAO could focus exclusively on RWAs to extract maximum yield. Voters within subDAOs will receive smaller mandates, enabling faster iteration and deeper discussion.

Each subDAO will operate independently, generate its own profits, and have its own subDAO token (SDT). These new tokens will serve as rewards to promote specific protocol segments—such as DAI adoption—and create synergies between MakerDAO and individual subDAOs.

subDAOs allow members to focus on specific tasks and develop specialized expertise, creating a more efficient and value-capturing protocol. Returning to the RWA optimization example: currently, RWA vaults earn an annualized yield of about 2.6% on $500 million. Note that U.S. Treasury yields are 5.5%, and USDC is essentially backed by Treasuries—so why pay Coinbase a 3% fee? Yes, there are benefits in custody and slight risk diversification, plus settlement delays in traditional finance (all trades take three business days). Last month, Coinbase launched Coinbase Earn, offering anyone 4% yield. That extra 1.4% might seem small, but for a $500 million deposit, it’s an additional $7 million. Each subDAO can implement many such low-cost optimizations to boost protocol revenue.

Endgame will include many groundbreaking changes, many of which are layered, making the upgrade sequence critical. Below is a rough timeline:

4.2 New Tokens

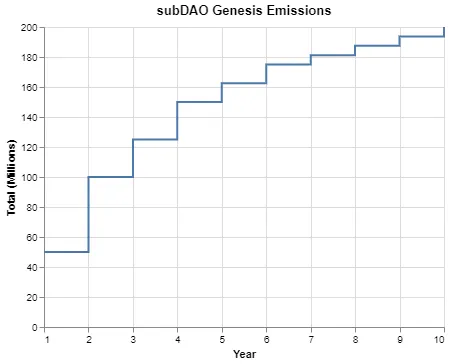

A token split will occur, with each MKR token converting into 1,200 new governance tokens (NGT). Additionally, a new stablecoin (NSC) will launch as a wrapped version of DAI. To drive initial NSC adoption, several liquidity mining programs will launch: one for NGT (10 million NGT annually, ~1.2% of total supply) and six farms for each independent subDAO (35 million SDT annually, ~1.75% of total supply), all accepting only NSC.

Note that each subDAO’s first-year token allocation is 230 million SDT, so 35 million represents over 15% of the first-year supply. These liquidity mines will act as powerful marketing tools to bootstrap NSC and direct attention to each subDAO. They will reverse the declining trend in DAI supply.

4.3 subDAO

Six subDAOs will launch first: two FacilitatorDAOs focused on DAO governance operations, and four AllocatorDAOs focused on generating NSC use cases and allocating various collateral assets.

Of the 230 million SDT, 200 million will go to mining, allocated as follows:

Similar to how MKR currently uses surplus income to buy and pool MKR, subDAOs will do the same. Maker Elixir is a 50/50 MKR/DAI pool, while each SDT will have its own Elixir with a 50/50 SDT/MKR composition. Essentially, any profit within the ecosystem will be used to buy and pool MKR, creating permanent buying pressure and deep liquidity. It’s easy to envision MKR becoming the third most liquid asset on-chain after ETH and BTC.

4.4 Sagittarius Lock-up Engine

The final piece of tokenomics is the Sagittarius Engine (SE), a MKR voter incentive and governance lock-up mechanism. A major issue with the current MakerDAO version is extremely low voting and delegation participation (typically 5–10%). SE will require long-term locking of MKR (or NGT), active governance participation, and grant exclusive access to private liquidity mining for DAI and other subDAO tokens.

If depositors wish to withdraw MKR from SE, they face a steep 15% penalty, which is burned. Additionally, when subDAO tokens launch, 30% of all token mining rewards will go to SE participants.

4.5 MKR Value Accrual

Unlike worthless governance meme tokens, MKR in V3 will have multiple utilities beyond governance:

-

Optimal mining of various SDTs via SE;

-

Maker Elixir surplus buybacks;

-

subDAO Elixir surplus buybacks;

-

Staking to validate the new MKR chain.

5 Investment Summary and Conclusion

In this article, we provided a broad overview of the entire stablecoin industry and highlighted it as one of the few profitable sectors in crypto. Maker is the oldest and largest investable stablecoin, and by traditional valuation metrics, it appears very cheap—discounting all future growth.

At the protocol level, we reviewed V1 and V2 and analyzed some shortcomings. Then we explored how V3 fixes and reverses many of V2’s problems and explained the intricate new tokenomics governing V3. MakerDAO is by far the largest decentralized stablecoin, and new products under V3 will only strengthen its leadership. It is also the most profitable decentralized stablecoin protocol, and efficiencies created by subDAOs will accelerate this profitability. In my view, these fundamental changes—combined with the token rebranding (a $900 MKR becoming 1,200 NGTs valued at $0.75 each)—are positive catalysts for the token.

Some short-term liquidity to note: A16Z has uncollateralized MKR from governance and sent it to Coinbase for sale. They’ve already sent about 15,000, with 34,000 remaining (19,000 in wallet, 14,000 in governance), and we can safely assume these will be sold.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News