MKR Price Rebounds: Can MakerDAO Realize Its Grand Vision of a "Fair Global Stablecoin"?

TechFlow Selected TechFlow Selected

MKR Price Rebounds: Can MakerDAO Realize Its Grand Vision of a "Fair Global Stablecoin"?

MakerDAO's core business has never changed, which is to promote its own stablecoin and generate "seigniorage revenue" from the issuance and operation of the stablecoin.

Author: Alex Xu

This issue of Clips focuses on MakerDAO, a leading RWA project and blue-chip DeFi protocol that has recently attracted significant attention. The author attempts to analyze the internal and external drivers behind MKR's price increase and evaluates Maker’s strengths, challenges, and long-term risks from a business perspective.

The views expressed below represent the author's opinions at the time of publication and may contain factual inaccuracies or biases. They are intended solely for discussion purposes, and corrections or feedback from other researchers and investors are welcome.

1. MKR Price Rebound: A Confluence of Factors

Recently, secondary market prices for legacy DeFi projects have warmed up noticeably, with Compound and MakerDAO showing particularly strong gains. While Compound’s surge was partly fueled by founder Robert Leshner’s new venture in the RWA space, this event had limited impact on its fundamentals—Comp’s rally appears more speculative (“dry pull”) and offers little analytical value.

In contrast, MKR’s rise is driven by a combination of internal and external factors, including fundamental business improvements and the gradual realization of Endgame’s long-term vision.

Specifically, key catalysts behind MKR’s recent price movement include:

1. A decline in the protocol’s monthly expenses—from routinely exceeding $5–6 million to around $2 million in June.

Maker token transfer payment statistics

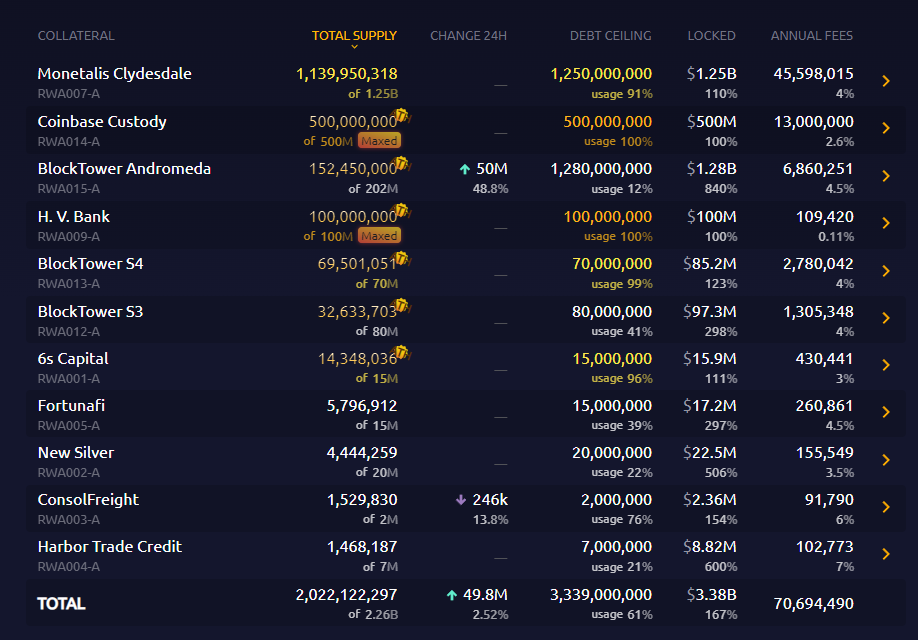

2. Shifting collateral from non-yielding stablecoins to U.S. Treasuries or stablecoin yield products, significantly improving financial income expectations, reflected in lower PE ratios. According to makerburn data, MakerDAO’s projected annual revenue from RWA alone reaches nearly $71 million.

Maker’s RWA asset list

3. Founder Rune’s consistent repurchase of MKR on the secondary market over several months while selling off other tokens like LDO, sending strong confidence signals to the market.

4. Governance-approved reduction of the surplus buffer threshold required to trigger buybacks—from $250 million down to $50 million. Currently, the system surplus stands at $70.25 million, enabling approximately $20 million in buyback funds. However, Maker’s current mechanism has shifted from “buyback and burn” to “buyback and market making.” As such, only half ($10 million) will be used to repurchase MKR, while the remaining $10 million Dai will be paired with MKR to provide liquidity on Uniswap v2, held as LP assets in the treasury.

Maker system surplus data

Additionally, since Maker founder Rune Christensen introduced the Endgame transformation plan last year, its grand narrative has inspired belief and investment following MKR’s performance and price recovery.

MakerDAO’s Endgame aims to optimize governance structures, fund sub-projects, and ultimately realize its vision of a “fair global stablecoin.”

Moreover, the RWA narrative has recently gained traction in the market. Although few projects tied to actual RWA operations have launched tokens yet, discussions are heating up, drawing positive sentiment from major investment firms.

In summary, MKR’s recent rally stems from a mix of internal and external drivers—with internal improvements playing the dominant role. Rather than RWA hype driving Maker, it is Maker’s practical execution and early success in RWA that have helped shape and advance the broader crypto RWA narrative. The causality here is often reversed.

2. The Nature of MakerDAO’s Business

How should we assess the long-term implications of these developments? Can these positive trends propel Maker to the next level and fulfill its ambitious goal of creating a “fair global stablecoin”?

The author believes this is unlikely—and understanding why requires examining the core nature of MakerDAO’s business.

MakerDAO’s core business has never changed—it is fundamentally the same as USDT, USDC, BUSD, and others: promoting its own stablecoin to earn seigniorage revenue from issuance and operation.

Seigniorage can broadly refer to income earned by currency issuers through minting. Different stablecoin projects generate seigniorage differently. For example, Liquity charges users a 0.5% fee when minting its stablecoin LUSD. Tether charges users 0.1% or $1,000 for depositing/withdrawing USD.

Tether also actively deploys deposited USD into liquid assets such as government bonds, reverse repos, or money market funds to earn financial returns on the asset side.

Dai previously relied heavily on borrowing interest (stability fees) paid by users who minted Dai using collateral. Later, Maker adopted an approach similar to Tether—replacing low-yield stablecoin collateral in its PSM module (e.g., USDC) with income-generating assets such as Treasury bonds or USDC held in Coinbase’s yield-bearing accounts.

However, the crux of any stablecoin business lies in expanding demand-side adoption. Only with sustained high issuance volume can sufficient collateral be accumulated to deploy capital and generate financial income.

Furthermore, Dai differs from USDT and USDC primarily due to its decentralized positioning—the claim that “Dai offers stronger censorship resistance and lower regulatory exposure compared to USDT and USDC” represents Dai’s most important differentiator. Yet replacing Dai’s collateral with real-world assets (RWA) that can be seized by centralized authorities fundamentally erodes this distinction between Dai and centralized stablecoins like USDC and USDT.

That said, Dai remains the largest decentralized stablecoin today, with a $4.3 billion market cap—significantly ahead of Frax (~$1 billion nominal market cap) and LUSD ($290 million).

3. Sources of Dai’s Competitive Advantage

Beyond its active pivot toward RWA on the asset side, Maker’s overall management of Dai has felt stagnant in recent years. Its continued dominance in the decentralized stablecoin category rests on two pillars:

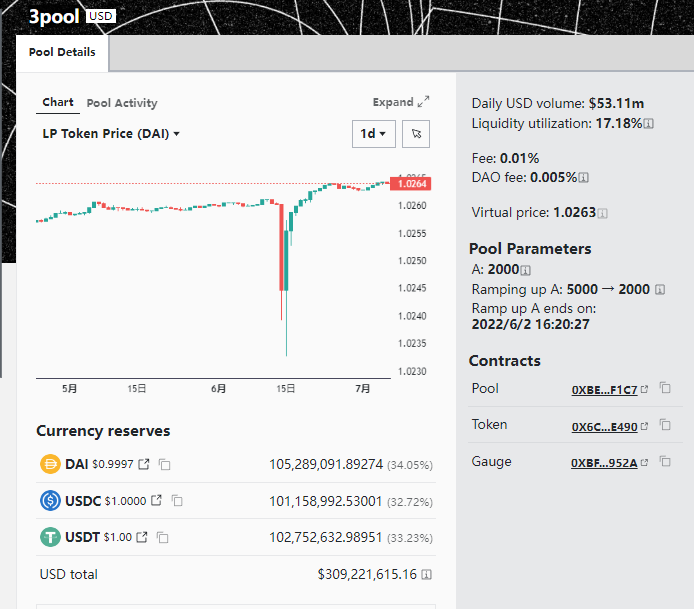

1. The legitimacy and brand recognition of being the “first decentralized stablecoin”: This allowed Dai to be integrated earlier into top-tier DeFi platforms and centralized exchanges (CEX), drastically reducing liquidity acquisition and business development costs. Take Curve, for instance—Dai is one of the original components of Curve’s longest-standing stablecoin liquidity pool, the 3pool, which makes Dai a default base stablecoin. As a result, Maker pays nothing for Dai’s liquidity on Curve. Moreover, Dai benefits indirectly from liquidity bribes provided by other projects (when they purchase their own tokens to pair with 3pool liquidity).

Curve’s 3pool stablecoin pool

2. Network effects of stablecoins: Users tend to adopt the stablecoin with the largest network, highest user count, most use cases, and greatest familiarity. Within the niche category of decentralized stablecoins, Dai still leads its competitors.

Yet Dai’s main rivals aren’t Frax or LUSD (which face their own struggles). When users or protocols choose a stablecoin to integrate or transact with, they typically compare Dai directly against USDT and USDC—against which Dai clearly lags in network scale.

4. MakerDAO’s Real Challenges

Despite the concentration of short-term positive indicators, the author remains pessimistic about MakerDAO’s future. Having clarified Maker’s fundamental business model and Dai’s current competitive advantages, let us now confront the real issues it faces.

Problem 1: Dai’s Scale Is Shrinking, Use Case Expansion Has Stalled

Dai’s current market cap has declined nearly 56% from its peak and shows no signs of bottoming out. In contrast, even during bear markets, USDT has reached new all-time highs in market cap.

Dai’s last major growth phase came during the DeFi Summer yield farming boom. But what will drive its next cycle of expansion? No compelling new use cases appear on the horizon.

Maker hasn’t been idle in thinking about how to broaden Dai’s adoption. According to the Endgame blueprint, the first strategy is to back Dai with renewable energy projects, transforming it into “clean money.” The idea is that this would give Dai a mainstream-friendly branding element and raise the political cost for authorities attempting to seize or penalize Dai’s clean energy assets. To the author, however, increasing the “green” content of collateral will boost Dai’s acceptance is overly naive. People may support environmental causes rhetorically, but in practice, they’ll still opt for the more widely accepted USDT or USDC. Promoting a decentralized stablecoin within the highly idealistic Web3 world is already difficult enough—how can we expect real-world users to adopt Dai simply because of “environmental friendliness”?

The second approach—also a centerpiece of Endgame—is for Maker to incubate subDAOs developed by the community around Dai. These subDAOs would not only decentralize governance currently concentrated in MakerDAO, distributing coordination across multiple domains, but could also launch standalone commercial ventures to explore new revenue streams and create fresh demand for Dai. However, this brings us to the second major challenge Maker must overcome.

Problem 2: How Can SubDAO Projects Succeed While Also Subsidizing MKR and Dai?

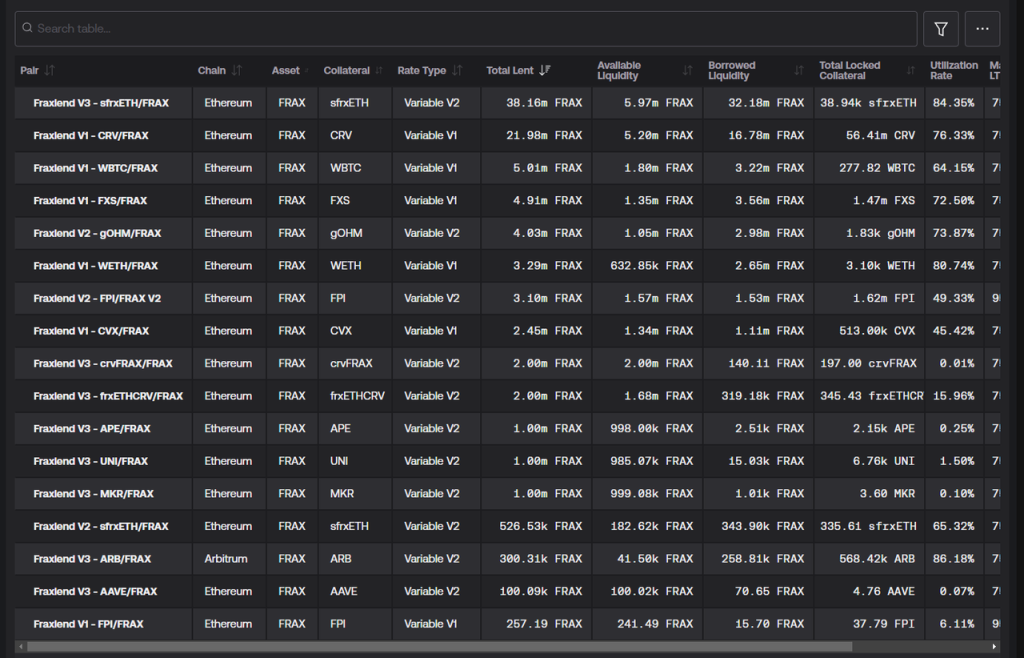

Future subDAOs incubated by Maker will use their own newly issued tokens to incentivize liquidity mining for Dai, boosting its usage. Additionally, MakerDAO will offer subDAO projects low-interest or zero-interest loans in Dai to help them launch. Beyond cheap capital, subDAOs inherit MakerDAO’s brand credibility and community—a crucial advantage for seeding early users and bootstrapping DeFi projects. Compared to relying on green initiatives to boost adoption, the subDAO strategy sounds more executable and has precedents in DeFi. For example, Frax launched Fraxlend, allowing users to borrow Frax using various collaterals, thereby creating utility for Frax.

Fraxlend asset lending list

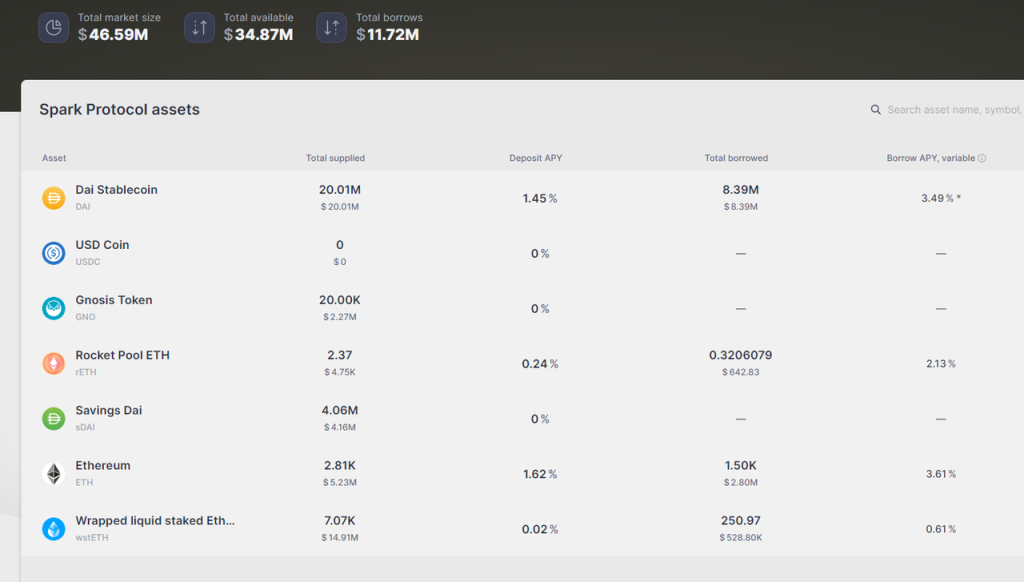

But the problem is, in a DeFi landscape where “low-hanging fruit” have already been picked, launching a successful subDAO tailored to real market needs is extremely challenging. More importantly, these subDAOs must simultaneously contribute value to Dai and MKR by allocating additional project tokens as incentives for Dai, ETHD (a rewrapped version of an LST token proposed in Endgame, intended as Dai collateral), and MKR. Under such “tribute obligations,” delivering products that meet user needs and outcompete existing solutions becomes exponentially harder. Spark, a lending product launched by MakerDAO, currently has only around $20 million in organic TVL after excluding the $20 million in Dai directly minted by MakerDAO.

5. Other Hidden Risks Facing MakerDAO

Beyond the two challenges above, MakerDAO faces several other concerns.

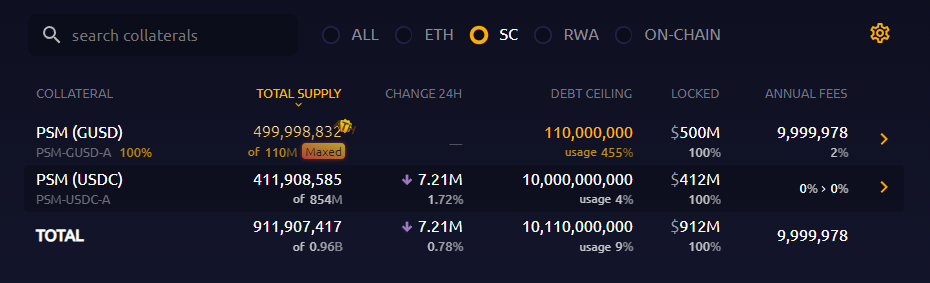

First, MakerDAO’s reserves available for further RWA purchases are dwindling, limiting its ability to increase exposure to U.S. Treasuries.

According to Makerburn data, Maker’s PSM currently holds about $912 million in stablecoins (USDC + GUSD). Of this, $500 million in GUSD already earns a 2% annual yield subsidy from Gemini. Despite lower yields than other RWA investments, complex factors—including the fact that MakerDAO’s PSM holds 89% of total GUSD supply—make large-scale liquidation impractical due to potential price slippage.

Thus, Maker’s truly flexible cash for purchasing income-generating assets is limited to ~$412 million in USDC within PSM. At best, it could convert another $500 million in USDC currently earning 2.6% annually on Coinbase into Treasuries. Altogether, maximum possible reinvestment into Treasuries is around $900 million. However, considering redemption pressures via PSM, the actual amount deployable into Treasuries must remain conservative—otherwise, large redemptions of Dai for USDC would force Maker to sell Treasuries at a loss due to transaction frictions and bond price volatility. Furthermore, if Dai’s market cap continues to shrink, Maker’s investable asset base will contract accordingly.

Second, the author doubts whether MakerDAO can sustain its cost discipline. While Endgame proposes decentralizing governance from a central “Maker core” to individual subDAOs, each subDAO introduces complex roles, organizations, and arbitration bodies—making the entire coordination framework the most complicated among known projects, a true “governance maze.” Interested readers can experience cognitive strain firsthand by reading the Endgame V3 full overview. Additionally, integrating RWA introduces intersections between DeFi and traditional finance, spawning numerous high-cost outsourced roles. Combined with severe governance centralization (in October 2022, 70% of votes approving the Endgame proposal came from voting blocs linked to founder Rune), MakerDAO’s rent-seeking risks are now undeniable. For example, Monetalis Clydesdale, a small firm managing Maker’s largest RWA vault, oversees $1.25 billion in funds allocated to Treasury assets and interfacing with traditional financial institutions. It charges nearly $1.9 million annually in fees and was, at the time, Maker’s sole client—while Rune Christensen himself is a major shareholder of Monetalis.

Rune is a primary investor in Monetalis

Another case involves Block Analitica, Maker’s risk management service provider, which receives nearly $5 million annually (paid in Dai and MKR). Strangely, Block Analitica serves both as the service provider and evaluator of its own risk assessments—an athlete-judge conflict that turns Maker’s risk management into a lucrative monopoly. The only remaining question is how Block Analitica and the MKR governance cartel will split the spoils drawn from Maker’s treasury. With such precedents and Endgame’s grandiose plans—so convoluted that even a16z reportedly shook their heads—future treasury leakage seems inevitable. As operations decentralize, mechanisms for draining and redistributing treasury funds may become even more opaque and indirect.

Source: CoinDesk

Additionally, Dai’s stability fee recently increased from over 1% to above 3%, further dampening borrowing demand via MakerDAO and undermining efforts to maintain Dai’s scale.

Finally, the coordinated moves—from Endgame announcements and large-scale Treasury/RWA acquisitions to the founder’s high-profile secondary market buybacks and governance votes lowering the treasury withdrawal threshold for buybacks—have delivered short-term market success for MKR, but left behind serious隐患:

1. Insufficient treasury surplus reserves weaken bad debt risk resilience.

2. Aggressively increasing RWA exposure raises counterparty seizure risks, amplifying Dai’s fragility.

3. The ever-expanding, frequently revised Endgame roadmap has deeply divided the community. In Rune Christensen’s May-published Endgame Phase One roadmap, new ideas such as “AI governance,” launching a “new brand” stablecoin and governance token (while retaining existing Dai and MKR), and MakerDAO launching its own blockchain were introduced—raising eyebrows across the ecosystem.

6. Endgame Is Not the Endgame

In the comment section of Rune Christensen’s May forum post detailing the Endgame roadmap (The 5 Phases of Endgame), amid typical praise and confused queries from other governors, two user comments stand out:

“(We) wasted precious money and energy funding useless people and garbage instead of focusing on creating value for MKR and growing Dai’s scale. All resources and research should go toward making Dai and MKR self-sustaining! Cut bloated staffing, simplify governance—that’s the right path.”

“Why do we assume a pre-designed ‘endgame plan’ is better than solving current problems incrementally? Except for blockchain components, the plan details ‘what we’ll do’ very specifically, but says almost nothing about ‘why we’re doing it.’”

No one replied.

For blockchain-based Web3 projects, transparency and low trust costs should be leveraged for efficiency—not used to erect new walls and fog up operations behind rent-seeking agendas.

Endgame is not the rightful endgame for DeFi. It is merely MakerDAO’s wall and fog.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News