Those unable to purchase Anthropic shares have driven its “shadow stocks” up 16-fold.

TechFlow Selected TechFlow Selected

Those unable to purchase Anthropic shares have driven its “shadow stocks” up 16-fold.

It’s not the shadow that’s valuable—it’s the feeling of being locked outside that’s too costly.

Author: David, TechFlow

Last Thursday, a new stock debuted on the New York Stock Exchange (NYSE) under the ticker VCX.

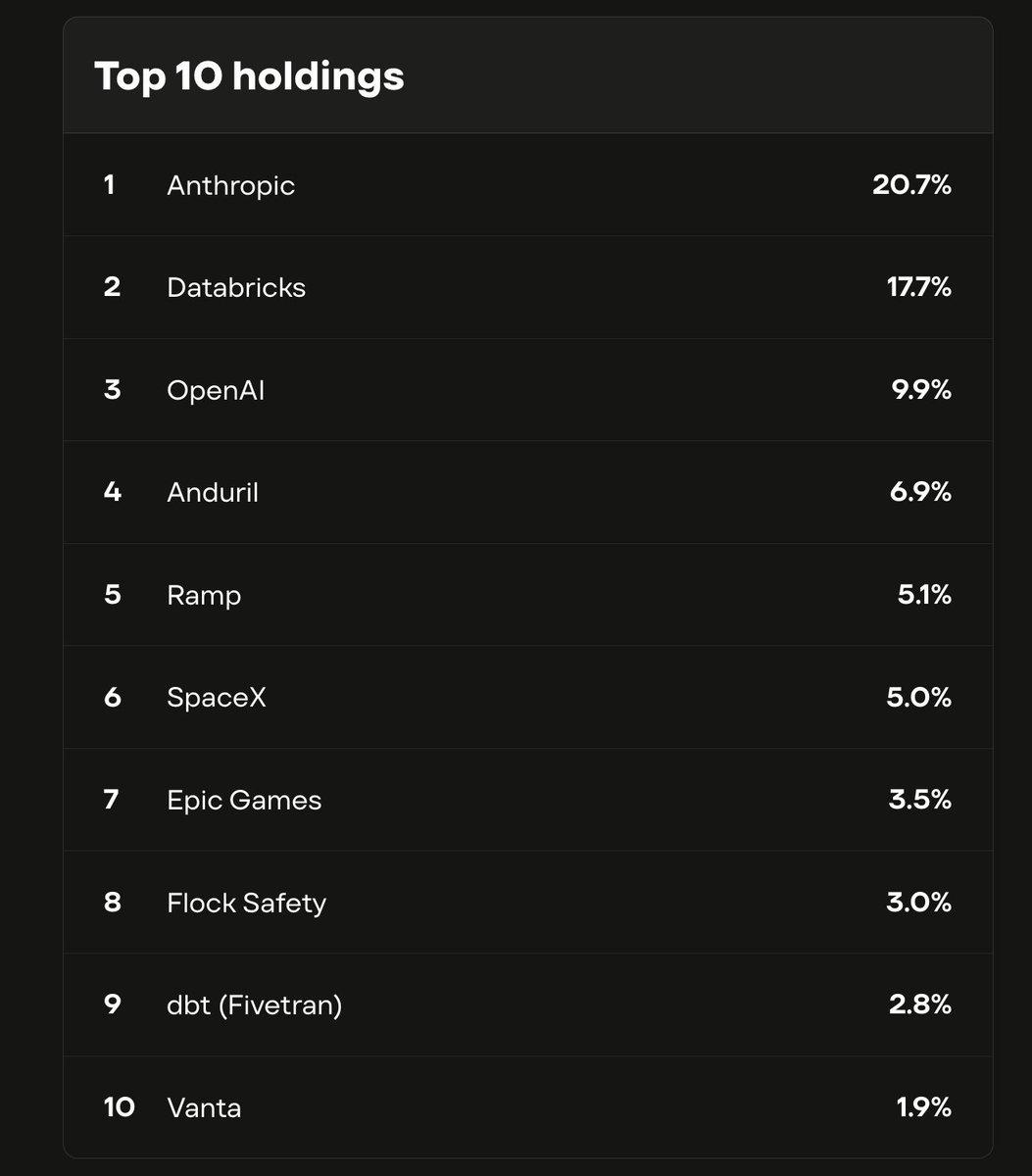

It is, in fact, a fund—holding shares of private companies including Anthropic, OpenAI, and SpaceX. Anthropic accounts for 21% of the fund’s holdings; OpenAI, 10%.

These companies share one key trait: none are publicly listed, meaning ordinary investors cannot buy their shares directly.

VCX is currently one of the very few vehicles enabling retail investors to gain indirect exposure to Anthropic’s equity.

Its net asset value (NAV) stands at $19 per share. On its first trading day, it opened at $42, surged intraday to $125, and closed at $76. By its fourth trading day, it hit an intraday high of $315—triggering two volatility circuit-breakers.

In four days, its price soared from $19 to $315.

Investors were effectively bidding 16 times the fund’s actual asset value—not because of any extraordinary skill by the fund manager, but solely due to Anthropic’s inclusion.

Just one month ago, Anthropic raised $30 billion at a $380 billion valuation—the second-largest private funding round globally this year—and reported annualized revenue of $14 billion. Yet it remains unlisted: no stock ticker, no presence in any brokerage’s search bar.

Unable to buy the real thing, investors scramble for its shadow. VCX is currently Anthropic’s shadow—or more precisely, the shadow of AI-related FOMO.

Why So Expensive?

VCX is not a conventional fund.

In typical funds, if you deem the price too high, you can wait for it to fall—because fund managers can issue additional shares, making supply elastic. VCX, however, is a closed-end fund: its share count was fixed at listing and will not increase.

More critically, the vast majority of shares are simply non-transferable. Investors who bought before February 20 face a six-month lock-up period, meaning they cannot trade until September. With over 100,000 VCX investors, only a tiny fraction of shares are actually available for trading today.

What does that mean? Demand is massive—but available supply is minuscule. A small number of buyers can drive the price wildly out of alignment with fundamentals.

That 16x premium, therefore, essentially prices two things: “How many people want exposure to Anthropic—and how narrow is the doorway?” Crucially, this scarcity-driven frenzy wasn’t engineered by VCX itself.

Chart: Top 10 Holdings of Fundrise’s VCX Fund

Over the past decade, a structural shift has taken place across the tech industry: the best companies are going public later—or never at all.

When Facebook went public in 2012, its $104 billion valuation was considered astronomical. Today, Anthropic’s private valuation is over three times Facebook’s IPO valuation—and yet Anthropic had no concrete IPO plan until recently.

OpenAI’s $500 billion valuation? Also unlisted. Rumors about SpaceX’s IPO have circulated for over a year—but no definitive date has been announced.

Ten years ago, companies reaching such scale would already be ringing the NYSE bell. Now, they don’t need to. Private markets offer nearly limitless capital—without quarterly reporting pressures or scrutiny from retail investors and short-sellers.

For founders, it’s a rational choice. For ordinary investors, it means watching history’s fastest-growing companies through glass—unable to step inside.

VCX was originally scheduled to list on March 9—but its debut was delayed by ten days due to the Iran conflict. During those ten days, nothing changed: Anthropic’s valuation held steady, and the fund’s portfolio remained untouched. Yet the delay itself amplified anticipation for another ten days.

When VCX finally launched, all that pent-up demand flooded into an extremely narrow channel.

Not All Shadows Are Valuable

Accessing shares of private companies isn’t limited to VCX.

But before exploring alternative routes, a more fundamental question arises: How did a publicly traded fund acquire shares in a private company like Anthropic in the first place?

The answer: the back door.

Major private companies raise new funding rounds every few months—from Series A to Series G—each admitting new investors. Anthropic recently closed a $30 billion Series G round, with participants ranging from Singapore’s GIC to Sequoia Capital and Goldman Sachs. Such rounds are typically open only to institutional investors, with minimum commitments often starting in the tens of millions of dollars.

Yet there’s a second path.

A company’s private status doesn’t prevent its shares from trading privately. Early employees and angel investors hold equity—and some wish to cash out early. This gives rise to private secondary markets: opaque, non-public, yet very real.

Fundrise began acquiring stakes via both channels back in 2022, when valuations for private tech firms had just plunged—making them cheap. Over four years, it assembled a portfolio featuring Anthropic, OpenAI, and SpaceX—then packaged it into VCX and listed it on the NYSE, allowing retail investors to buy in as easily as purchasing a stock.

In the same month, at least three other similar funds also began trading on the NYSE—all selling the same core idea:

Buying through the back door—and selling through the front.

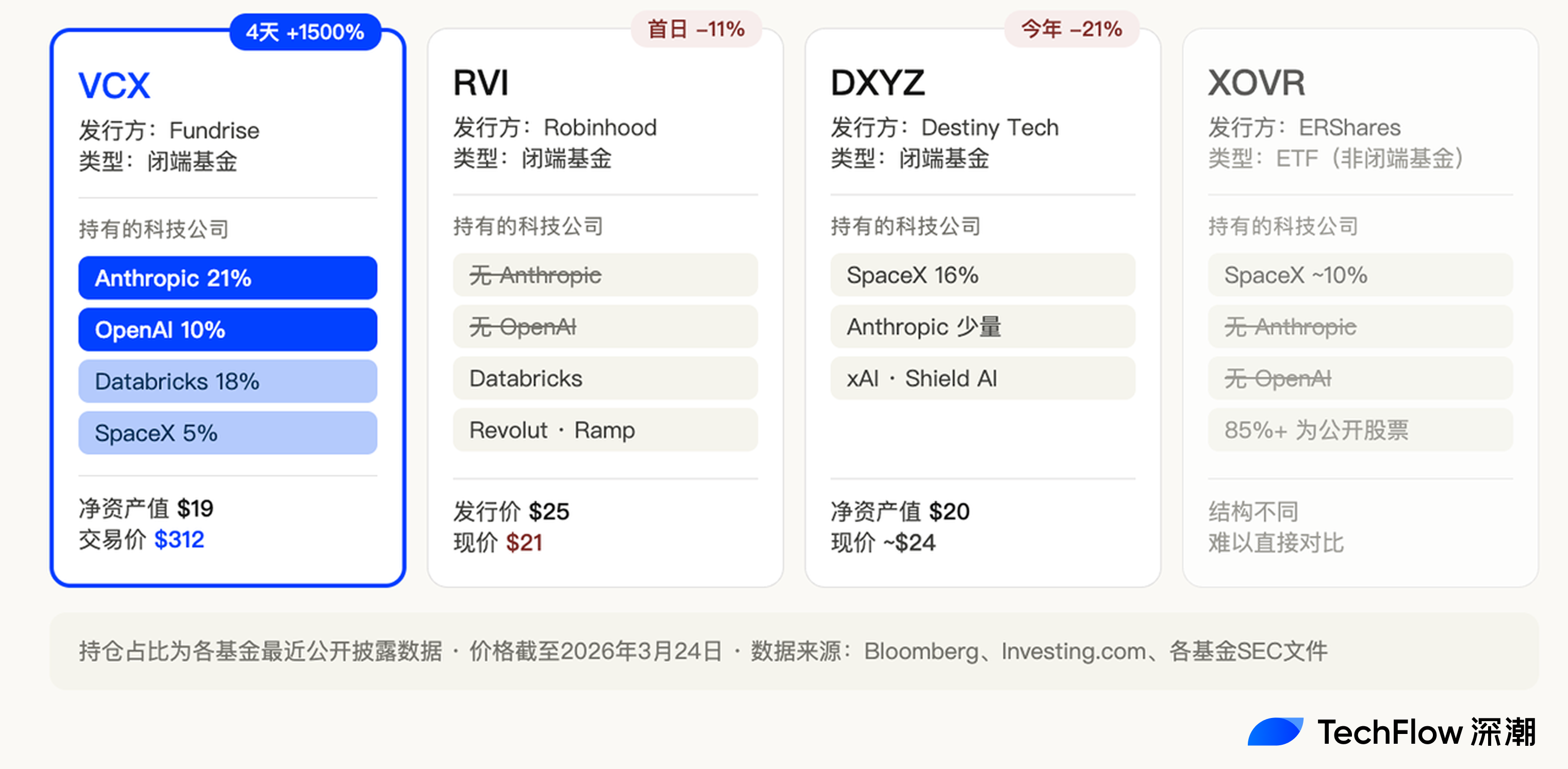

Robinhood launched a fund called RVI, which listed on March 6 at $25 per share. Its holdings include promising private firms Databricks, Revolut, and Ramp. Yet on its first trading day, RVI fell 11%, closing at $21.

Destiny Tech100 (ticker: DXYZ), launched in 2024, was an early entrant in this space. It holds 16% in SpaceX and only added a small, indirect position in Anthropic this February. Its current share price hovers near $24.

Another fund, XOVR, is the first ETF approved to hold direct equity stakes in private companies—SpaceX comprises roughly 21% of its portfolio.

Four funds—similar structures, similar concepts, same exchange—yet vastly different fates.

VCX surged 1,500% in four days. RVI broke below its offering price on day one. DXYZ has been lackluster.

VCX holds 21% in Anthropic and 10% in OpenAI. RVI holds neither. DXYZ’s Anthropic exposure is recent—and minimal.

This suggests that, at least for now, the market isn’t bidding up “private-company shares” in general—it’s bidding up Anthropic specifically.

Proximity matters. Value accrues to whoever is closest.

Robinhood’s RVI lost here. Databricks and Revolut are strong companies—but right now, they’re not the names investors are willing to pay a 16x premium for.

Shadows Have Expiration Dates

What are investors betting on when they buy VCX at $312?

They’re betting that, before the door opens, someone else will pay even more to gain exposure to Anthropic.

But that door won’t stay shut forever.

VCX has over 100,000 investors—most of whom face a six-month lock-up. That period ends on September 19. At that point, a flood of shares will hit the market, transforming supply overnight from extreme scarcity to abundance.

VCX’s 16x premium stems partly from Anthropic’s inclusion—and partly from the acute scarcity of tradable shares. Once the lock-up expires, the latter factor vanishes.

There’s an even larger variable at play.

Anthropic, OpenAI, and SpaceX are all rumored to pursue IPOs between late 2026 and 2027. Anthropic’s recent $30 billion raise at a $380 billion valuation included hiring Wilson Sonsini—a top Silicon Valley law firm—to prepare for its public listing. SpaceX’s CFO has been discussing IPO plans with investors since last year, targeting mid-2025.

Once the real thing goes public, the shadow loses value.

If you can type “Anthropic” into your brokerage’s search bar and buy shares directly, why pay a 16x premium for a fund holding them indirectly?

Take DXYZ, for example: it spiked shortly after launching in 2024—but as SpaceX’s IPO kept getting delayed, interest waned, and its share price dropped more than half from its peak.

Thus, VCX investors are living through a classic countdown.

What they’ve purchased for 16x NAV isn’t Anthropic’s equity—it’s a time-limited ticket. When the door opens depends entirely on when Anthropic decides to go public.

Until then, the premium is sustained by scarcity. Afterward, it evaporates.

Yet the phenomenon of “shadow stocks” isn’t accidental.

Every major technology wave spawns the same anxiety: the most important companies are inaccessible to you. In the 2000s, it was Google pre-IPO—Goldman Sachs employees fought internally for allocation. In 2020, it was SpaceX—secondary-market intermediaries in Silicon Valley suddenly became the hottest contacts.

Now, it’s AI’s turn.

And this time, the anxiety runs deeper. Anthropic and OpenAI may not yet be profitable—but they’re rewriting the rules. Because of AI, SaaS stocks crashed, cybersecurity stocks crashed, and IBM shed $31 billion in market cap in a single day.

Investors aren’t just seeing “a profitable company”—they’re seeing “if I’m not on its side, I risk being crushed by it.”

VCX’s 16x premium doesn’t price just a fund—it prices that anxiety itself.

The ticket expires. The premium fades. But as long as AI keeps accelerating—and as long as the most valuable companies remain behind closed doors—investors will keep paying irrational prices for shadows.

Not because the shadow is worth that much—but because the feeling of being locked out is far more expensive.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News