a16z: How Did Revolut Become Europe’s Most Profitable Neobank—Without Relying on Net Interest Margins or Burning Cash?

TechFlow Selected TechFlow Selected

a16z: How Did Revolut Become Europe’s Most Profitable Neobank—Without Relying on Net Interest Margins or Burning Cash?

Revolut’s revenue reached £4.6 billion, with a profit margin of 38%; it accounts for 1 out of every 3 new accounts opened in Europe.

Authors: Alex Immerman & Santiago Rodriguez

Translation & Editing: TechFlow

TechFlow Intro: a16z dissects Revolut’s 2025 Annual Report to reveal how a company achieved a staggering 76% CAGR within a mature financial market. The numbers alone are astonishing—but what’s even more compelling is the underlying growth logic: profitability not driven by net interest margin, ROE three to four times that of traditional banks, and NPS more than double the industry average. Taken together, this is no longer just the story of a challenger bank.

Full Text Below:

As growth-stage investors, we often say great companies speak first through their numbers. As a UK-based company, Revolut is required to publicly disclose its annual financial statements—and its numbers are outliers. That’s an understatement.

Revenue grew 46% to £4.5 billion

Pre-tax profit rose 57% to £1.7 billion, with a 38% margin

Retail customers grew 30%, adding 16 million in 2025

Revolut operates across all of Europe, with no single country contributing more than 25% of fee income

Revenue is distributed across six business segments, with no single category exceeding 22%

Eleven product lines each generated over £100 million in revenue

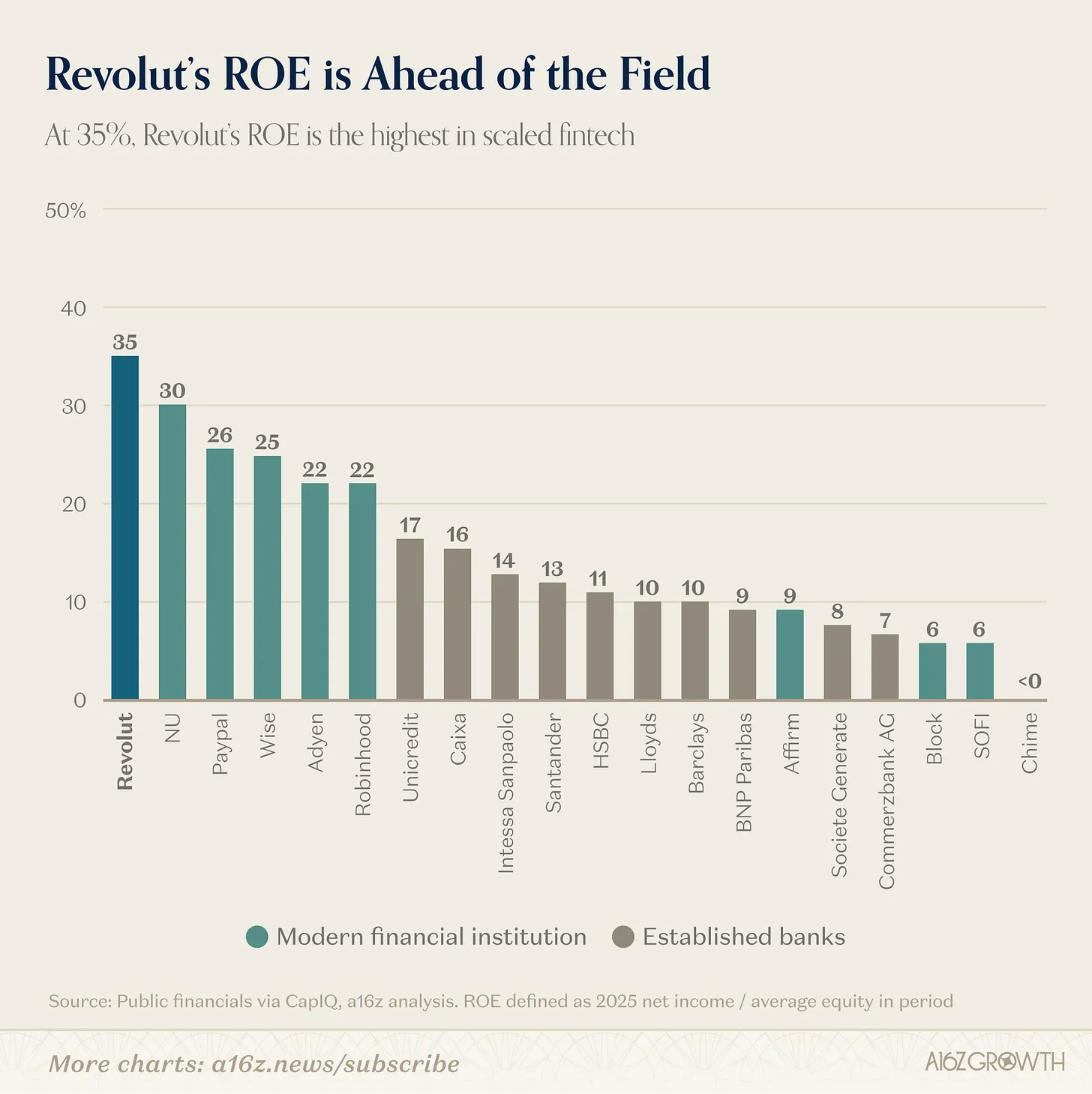

Return on equity (ROE) reached 35%—a record level among peers (despite being capital-rich)

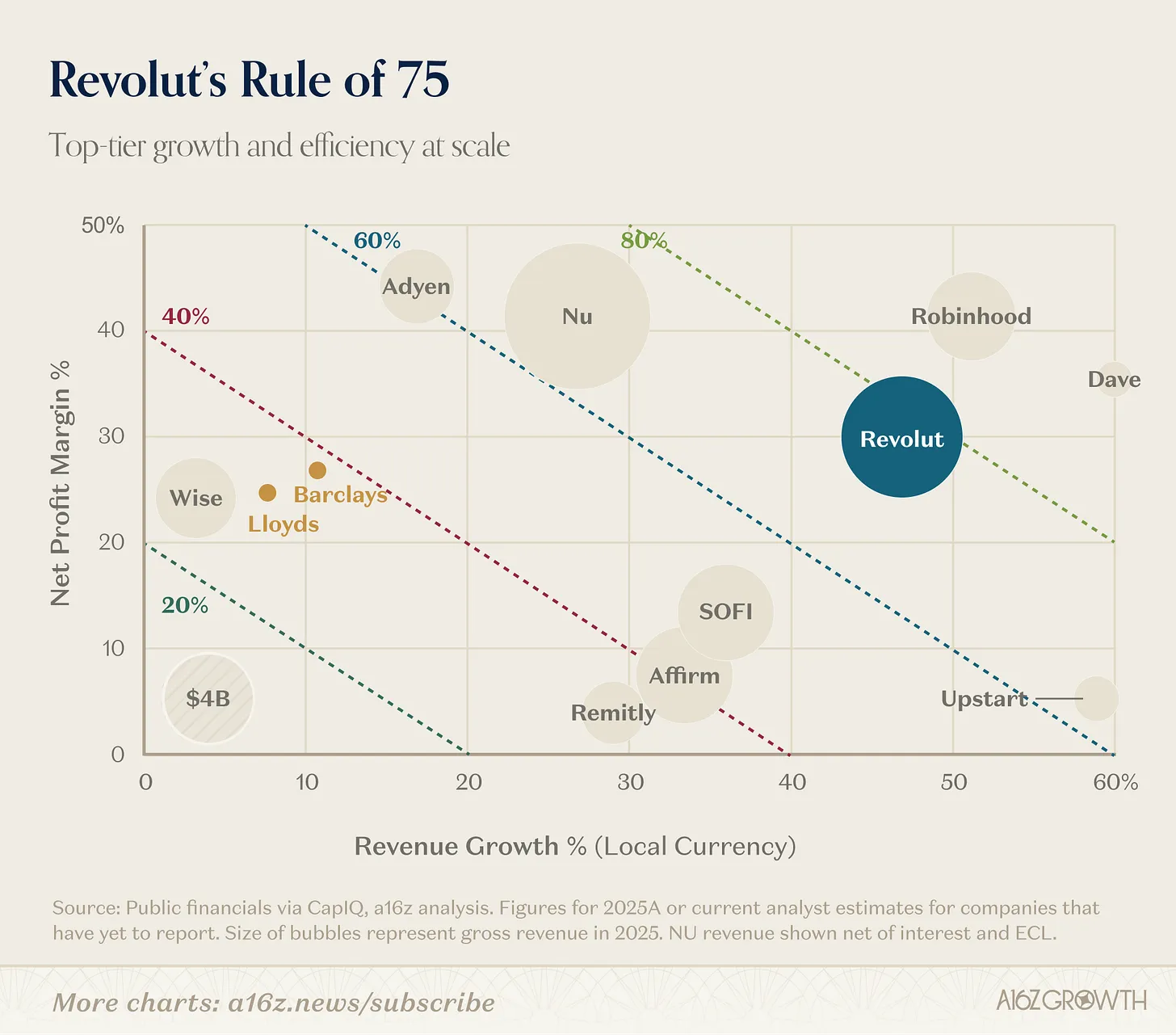

Revolut continues to grow rapidly and efficiently—its “Rule of 75%” (revenue growth + net profit margin) places it at the top tier among both modern and mature financial institutions.

More importantly, we believe Revolut still has substantial room to grow both its customer base and monetization in existing markets—not to mention untapped potential in new ones. Revolut has just applied for a U.S. banking charter and harbors genuine global ambitions.

This is not your grandmother’s new bank. Revolut has the potential to become one of the world’s largest banks. There remains much ground to cover—but we believe the foundation is already solid.

No more preamble. Let’s dive in.

I. One of the Fastest-Growing Financial Institutions Globally

Let’s begin with revenue. Revolut’s revenue growth is extraordinary.

Alongside NU (Nubank), Revolut stands in a league of its own relative to other consumer fintech companies (see chart below). Since crossing the $1 billion revenue threshold in 2022, Revolut has delivered remarkable compound growth—76% CAGR (70% in GBP terms)—over the past four years, making it one of the fastest-growing companies post-$1B revenue. This is especially notable given the extreme maturity of European consumer banking (unlike NU’s emerging-market context).

Chart: Revenue converted to USD using year-end exchange rates; NU revenue shown net of interest and expected credit losses (ECL)

Source: Revolut 2025 Annual Report

For perspective: In 2022, Revolut’s revenue was either lower than or roughly equivalent to any of Robinhood, Affirm, SoFi, Adyen, Wise, or Chime. Today, its revenue exceeds that of any of these well-known consumer fintech firms by 33% to nearly 3x.

II. Deconstructing Revolut’s Growth Algorithm: Six Engines Running in Tandem

A key differentiator for Revolut is that it is no longer a one-trick pony. It now drives revenue from multiple, simultaneous engines.

Revolut launched by solving a real pain point for Europeans: foreign exchange fees. With Revolut, Europeans traveling within or beyond the Eurozone—or sending money overseas—no longer face payment delays or banks’ typical 5% FX fees.

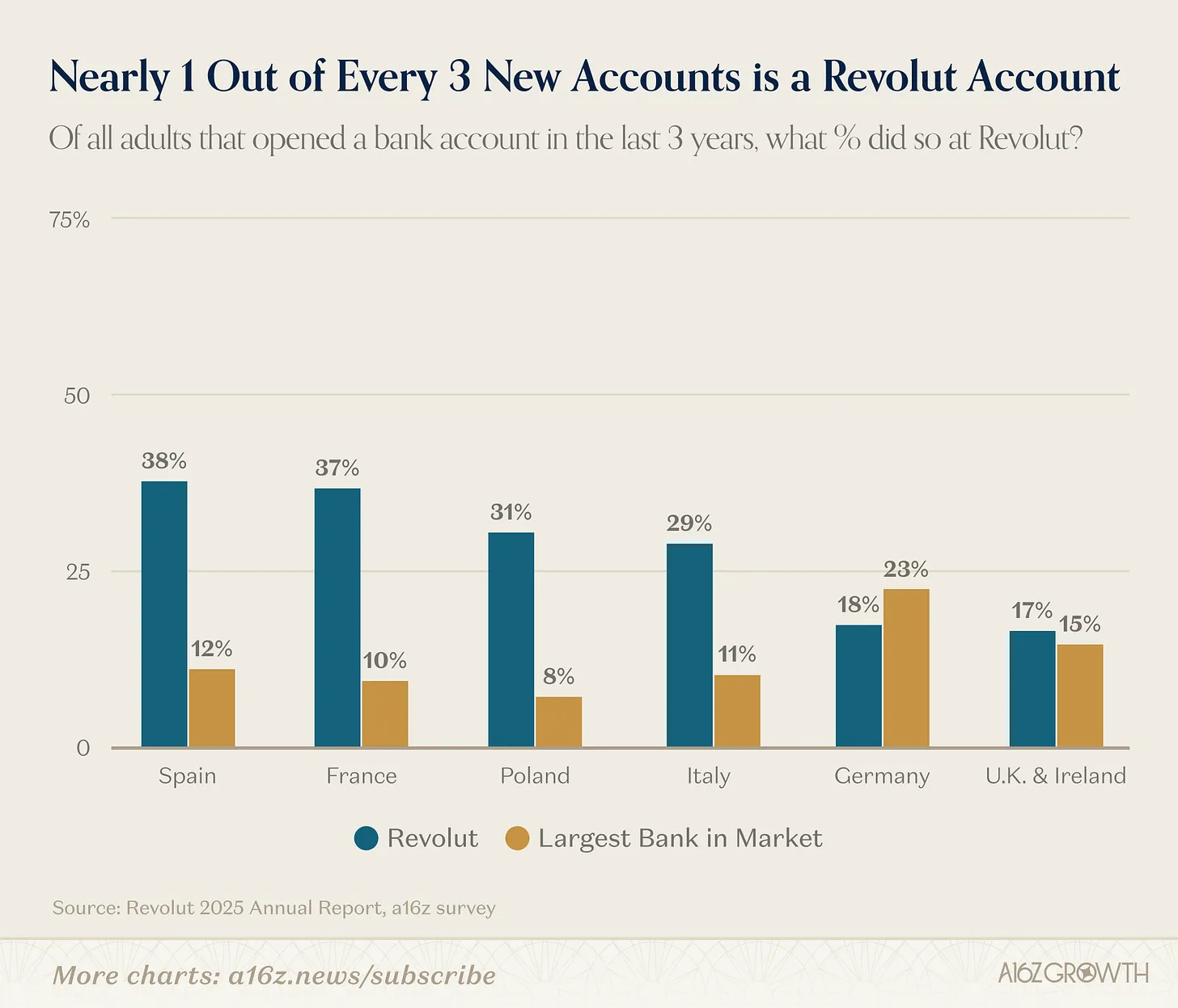

From a single-product, geographically concentrated solution, Revolut has evolved into a fully featured personal and business bank. Today, approximately one in three new accounts opened in Europe (Revolut’s primary operating region) is with Revolut:

Chart: Survey conducted across key markets using a representative sample of general adult populations; respondents indicated where and when they opened each account

Source: a16z European Banking Survey, July 2025 (N = 3,500)

One in five working-age adults across Europe uses Revolut. Its broad appeal across the Eurozone reflects exceptional product iteration speed and execution discipline.

Revolut offers a complete suite of personal and business banking features—and drives growth across diverse European markets. Critically, Revolut’s product suite increasingly attracts users who do not care about its original FX value proposition at all. Calling Revolut’s platform “feature-complete” may actually understate reality—because Revolut keeps launching new features.

It’s not just about quantity of features and products—it’s also about quality of execution. Users love it. In 2024, the company reported that 65% of new users came via organic acquisition or referrals from existing users. Our survey further shows Revolut’s user NPS exceeds the industry average by more than double.

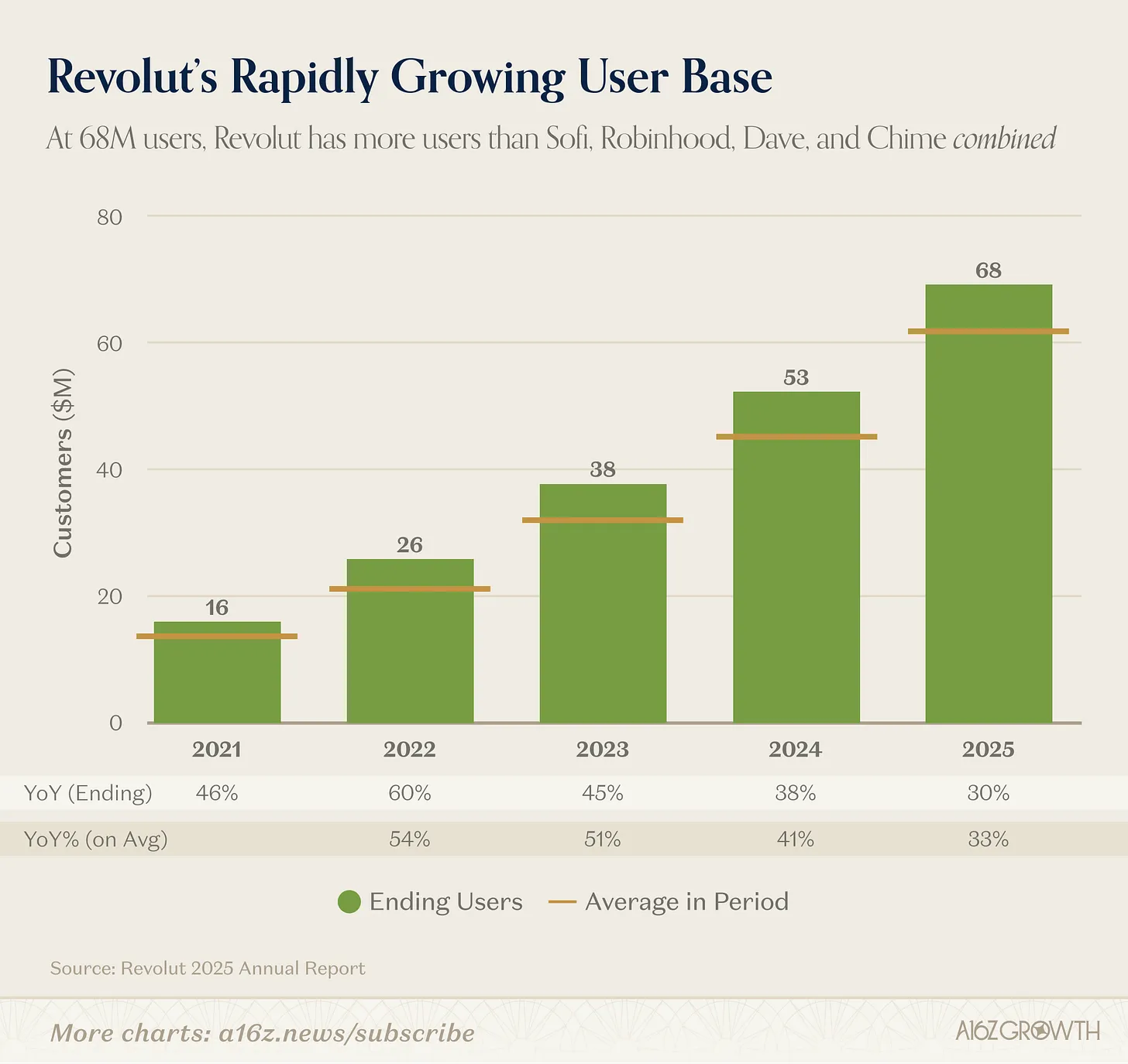

In aggregate, user count continues growing at a 30% CAGR, reaching 68 million by end-2025.

Source: Revolut Annual Report

To put 68 million users in perspective: JPMorgan Chase—the world’s largest bank outside China—has roughly 85 million consumer customers (of which over 70 million are considered “digitally active”).

True, JPMorgan’s total AUM dwarfs Revolut’s—but purely in terms of user reach, Revolut is no longer just a “challenger.” It is a real competitor. Revolut’s user count already exceeds the combined total of SoFi, Robinhood, Dave, and Chime.

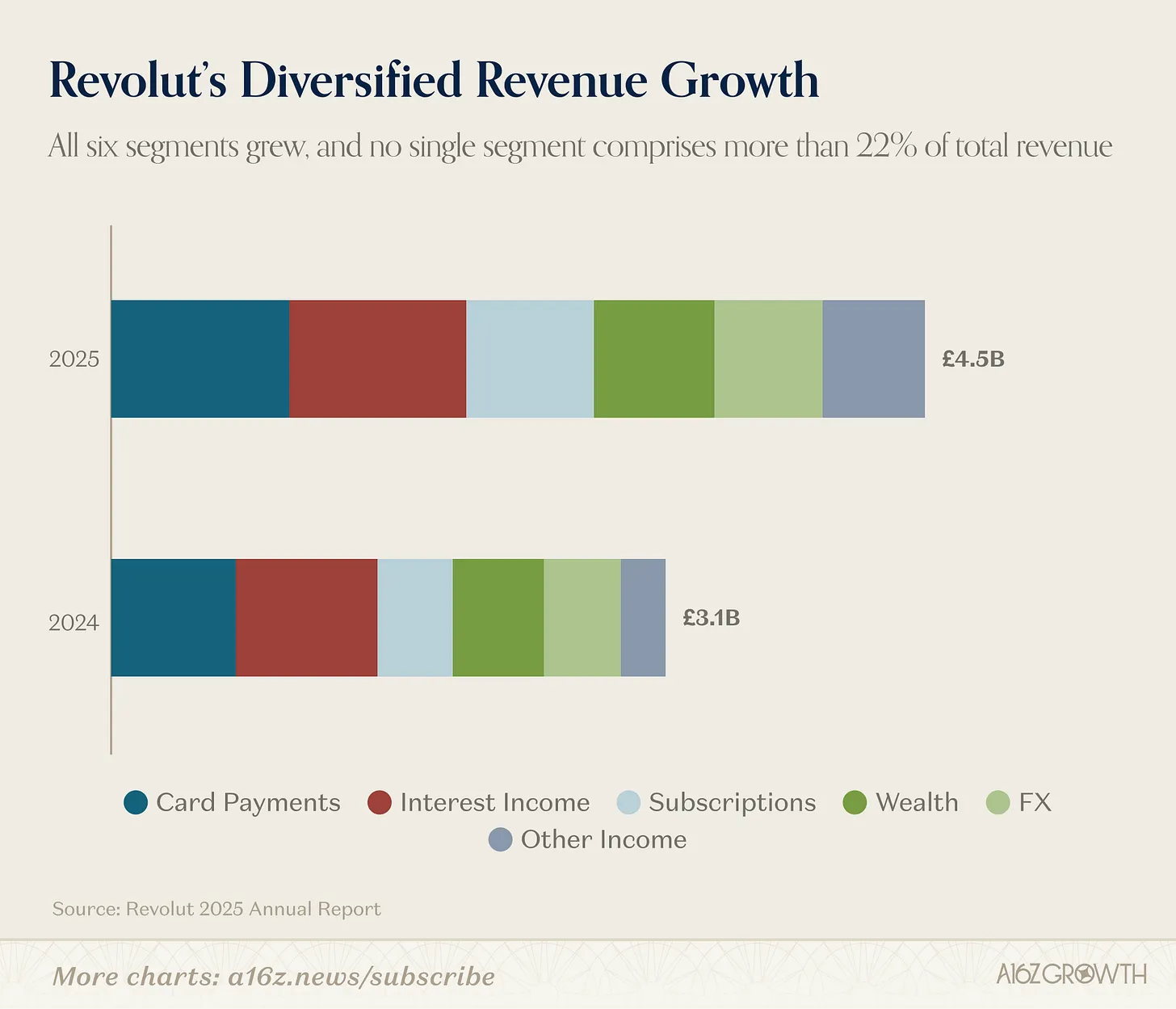

A full product suite doesn’t just attract more customers—it also creates an increasingly diversified revenue structure:

Source: Revolut Annual Report

The company publicly discloses six primary revenue streams:

Interest income

Card payments

Subscriptions

Other income

All six segments grew year-on-year, with no single segment accounting for more than 22% of total revenue.

Diversification runs deeper than this disclosure suggests—each revenue stream comprises multiple sub-products (e.g., wealth includes both public equities and crypto assets). In 2025, eleven individual product lines each generated over £100 million in revenue.

Importantly, 76% of revenue now comes from fees—up over 4 percentage points from 2024—while interest income accounts for just under 22%. This contrasts sharply with mature banks, which typically derive over 70% of revenue from interest income—and is one key reason Revolut achieves such high ROE (discussed further below).

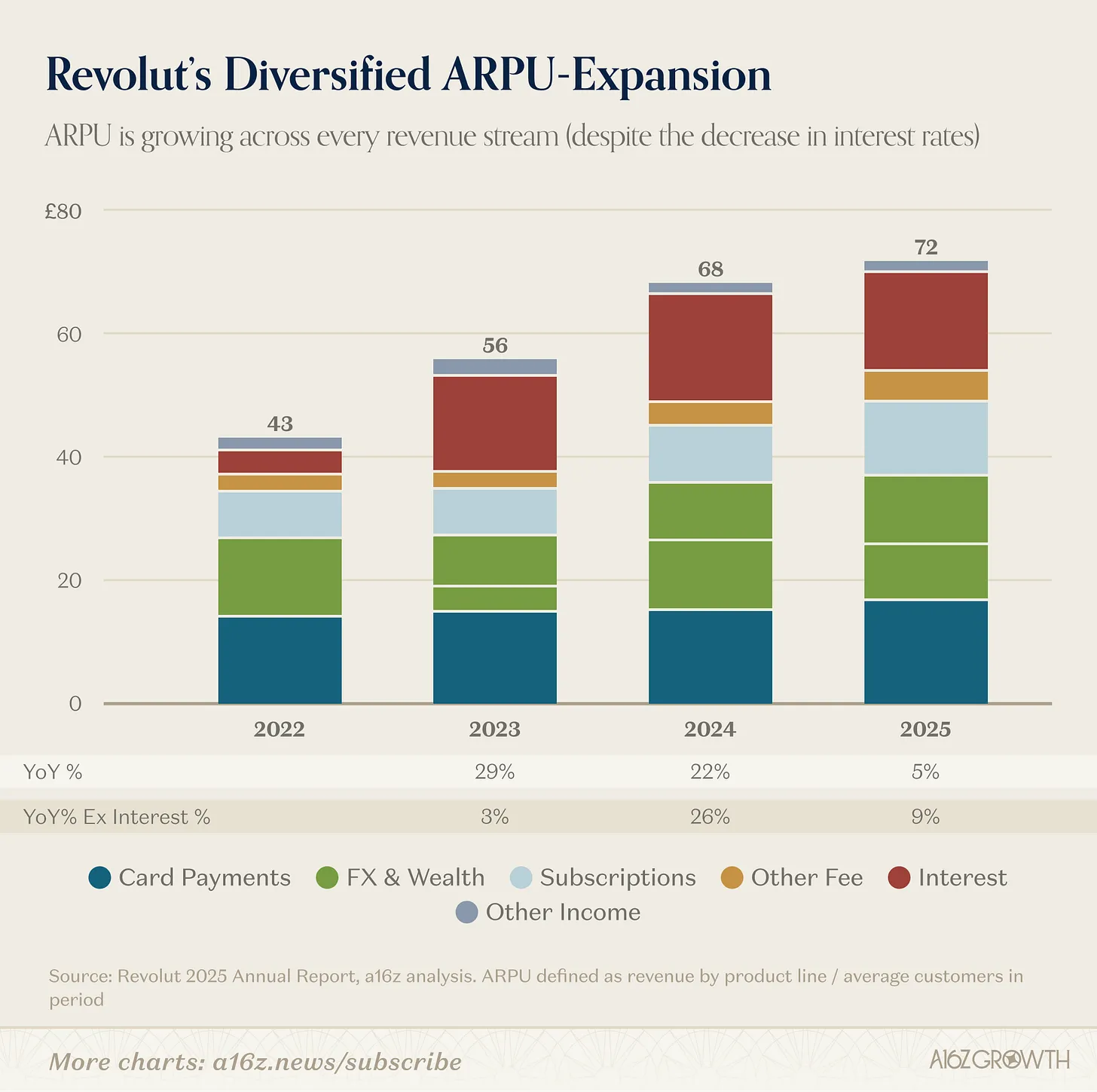

Unsurprisingly, this diversified revenue structure also supports diversified ARPU growth.

Chart: ARPU defined as product-line revenue / average number of customers during the period

Source: Revolut Annual Report

Since 2022, every disclosed revenue stream has grown, driving overall ARPU up ~65%—an 18% CAGR.

Diversification matters because it sustains compounding and builds resilience. In any given year, some product lines may boom while others face headwinds (e.g., last year’s rate decline). But cumulatively, new product add-ons and steady core wallet-share gains continue powering strong ARPU growth.

III. World-Class Efficiency

Revolut delivers rapid user growth, exceptional product iteration velocity, and diversified revenue—and fulfills its promise of efficiency too.

In 2025, Revolut achieved 46% revenue growth and a 29% net profit margin—its “Rule of X” (growth + margin) hit 75%. The “Rule of 40” is obsolete!

Chart: 2025A data or current analyst consensus forecasts for companies yet to report earnings; bubble size represents 2025 total revenue; NU revenue shown net of interest and expected credit losses (ECL)

Source: Public financial data via CapIQ; a16z analysis

This combination of growth and efficiency places Revolut in an exceptionally rare position—historically, very few companies have achieved a Rule of 75% at over $1B revenue scale.

In fact, given Robinhood and Dave’s consensus 2026 growth forecasts both sit below 30%, Revolut may soon stand alone atop the podium.

Efficiency is baked into Revolut’s DNA. Building its own banking infrastructure, achieving highly organic growth, and maintaining strict cost control collectively deliver a 29% net profit margin. Coupled with minimal physical branch presence, Revolut already holds meaningful cost advantages versus traditional banks—and those advantages compound as scale expands.

AI is further enhancing operational leverage. Take customer service:

In 2024, Revolut’s AI-powered chatbot cut issue resolution time by 80%. In 2025, improvements continued—retail resolution time fell another 40%+, enterprise resolution time dropped over 50%+, and user NPS rose nearly 12 points year-on-year. Revolut’s AI assistant now resolves over 75% of customer inquiries.

This efficiency enables Revolut to achieve the highest ROE we’ve seen among scaled fintechs—and it’s still improving. We’ve previously written about ROE’s critical role in bank valuation. Revolut is a textbook case of scale-driven efficiency.

Chart: ROE defined as 2025 net income / average equity during the period

Source: Public financial data via CapIQ

Revolut’s 35% ROE far exceeds other leading consumer fintechs—and is roughly 3–4x that of mature banks. Note: Revolut is “capital-rich” (i.e., reported equity exceeds regulatory capital requirements), meaning its “true” ROE could be even higher.

Few companies achieve growth this capital-efficiently.

IV. Ample Growth Runway: ARPU × User Count

Though Revolut’s 2025 performance is impressive, we believe enormous runway remains ahead. Returning to Revolut’s core revenue growth algorithm (user count × ARPU), both variables still offer significant upside.

More Users to Acquire

The company reports 68 million users at end-2025. As noted, that’s sizable—but still less than 15% of Europe’s (ex-Russia) ~450–500 million adult population. That excludes Australia and Singapore (existing markets), Mexico and Brazil (newly entered), the U.S. (just applied for a banking charter), and many more untapped regions.

Revolut still has vast pools of potential users to acquire.

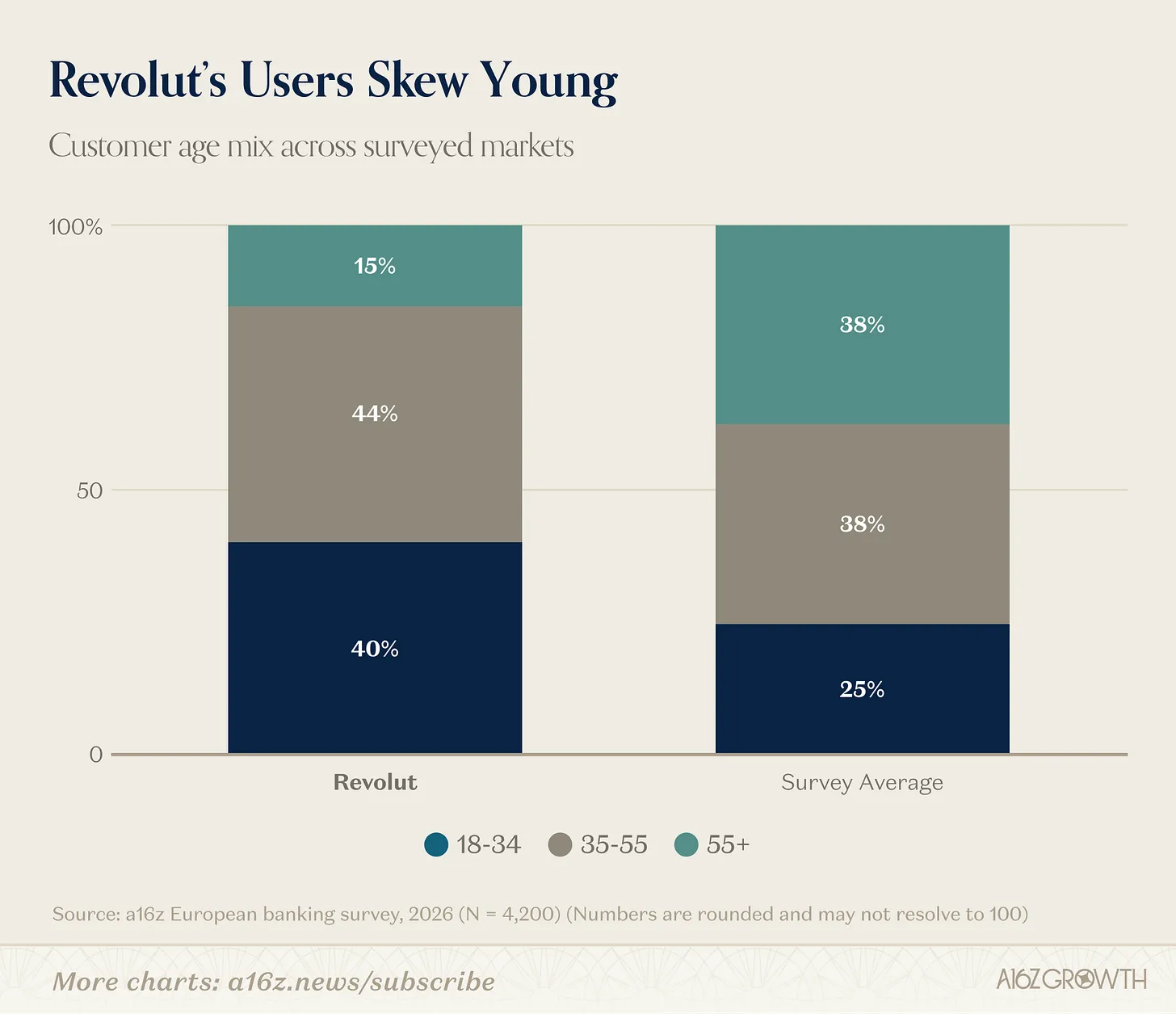

Moreover, its current user composition signals that tomorrow won’t look like today. Unsurprisingly, Revolut’s users skew younger and more digitally native—a cohort we believe reflects the trajectory of the broader population.

Chart: Survey markets include UK, Ireland, France, Spain, Italy, Germany, and Poland

Source: a16z European Banking Survey, February 2026 (N = 4,200)

As Revolut continues capturing large shares of new-account openings—and convinces older demographics that banking can be delightful—market share should keep rising.

Critically, our survey shows ~25% of Revolut users under age 35 use it as their primary account. On its own, this implies profound implications for European banking market share as this cohort ages.

ARPU Still Has Significant Upside

The second growth lever—ARPU—offers even greater expansion potential.

Wallet-share migration in financial services typically unfolds over decades—not years. Revolut continues winning user trust: its primary-account users (per company definition) grew 45%, outpacing overall user growth of over 30%.

Primary-account growth is pivotal—because “primary-account” users drive the real ARPU upside:

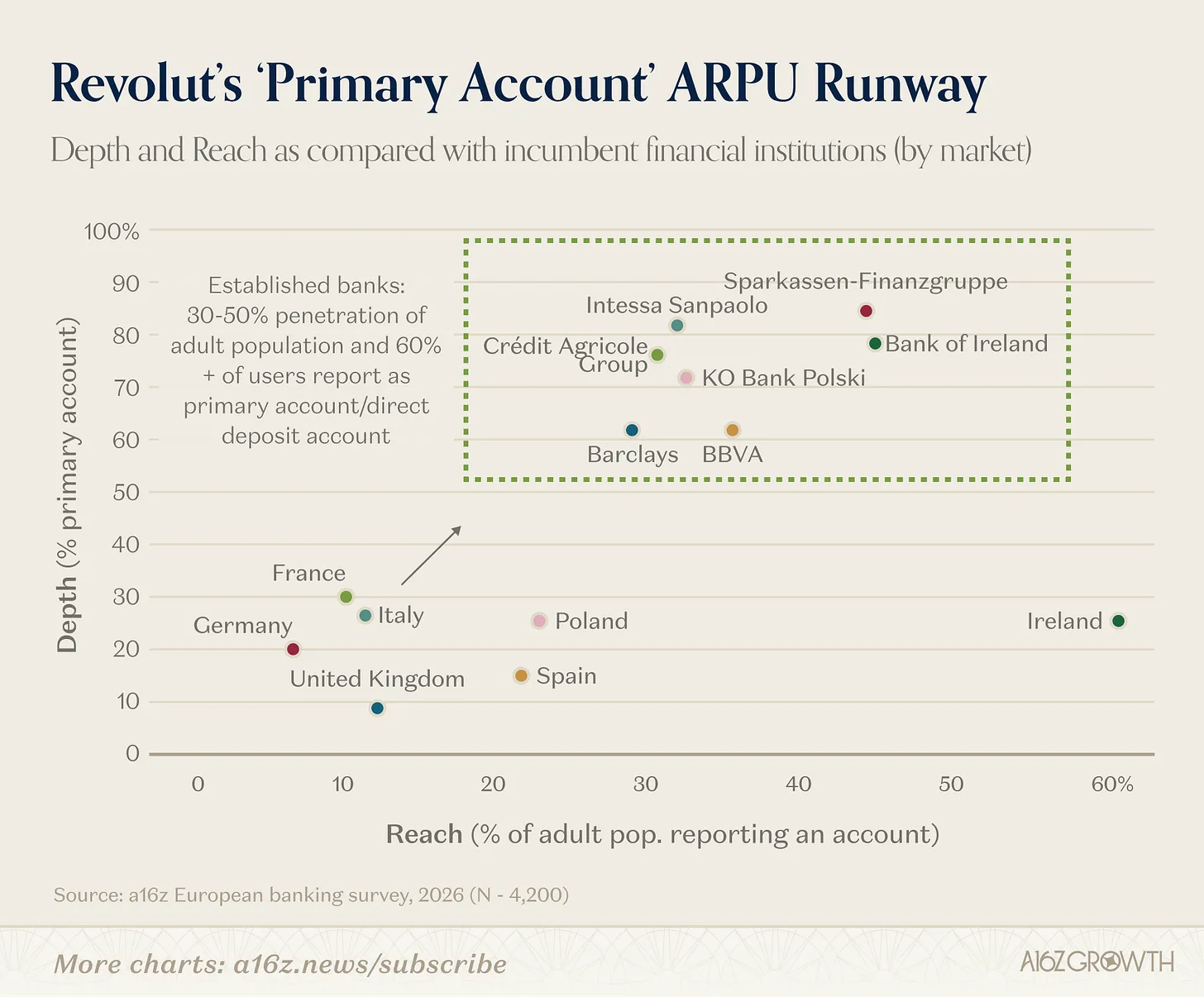

Our research shows mature customer relationships at traditional banks push primary-account share above 60%.

Revolut reports its primary-account users spend and save roughly twice as much on Revolut as on any other active account—and spending increases with age.

In short, more (and increasingly mature) primary-account users translate directly into higher ARPU—and if traditional banks serve as a benchmark, Revolut’s ceiling for primary-account share is very high.

Another dimension of primary-account growth is Revolut’s underexploited lending revenue opportunity:

As noted, Revolut currently derives 76% of revenue from fees—versus ~30% for mature banks;

At end-2025, Revolut’s loan-to-deposit ratio (LDR) stood at only ~6%, compared to 70–90%+ for mature banks (or ~4% if calculated against total customer balances). Loan balances grew ~2x in 2025—and can compound for many years to come.

Of course, prudent lending growth takes time. But if traditional banks’ ceilings provide a reference, Revolut has ample room to significantly expand ARPU by deploying its balance sheet and offering better lending products. For context, a rough estimate puts Barclays’ UK consumer and business banking ARPU at ~£435—about six times Revolut’s current level.

Here’s where Revolut currently sits on breadth (penetration) and depth (primary-account share):

Source: a16z European Banking Survey, February 2026 (N = 4,200)

Revolut has ample runway to move steadily up and right (Ireland’s case is primarily upward)—both by expanding its user base and deepening more relationships into “primary accounts.” The latter should occur organically as its young user cohort matures.

V. Conclusion: More Than Just a Challenger

Revolut’s 2025 numbers matter—not only because they’re impressive, but because they paint a full portrait of a financial institution, not merely a “challenger bank.”

User growth remains exceptional, monetization continues broadening, primary-account adoption is rising, and profitability strengthens—even as the company invests aggressively and scales rapidly. This combination is extraordinarily rare in financial services—or any industry.

Execution challenges remain ahead—especially in lending, regulation, and entering new markets—but after reading this annual report, the question has shifted: not “Can Revolut become a scaled banking platform?” but rather “How big can this platform become?”

The company’s stated long-term goal is “100 million daily active users across 100 countries.” That journey is already underway.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News