Analyzing the Lending Protocol Inverse Finance: Can It Make a Comeback?

TechFlow Selected TechFlow Selected

Analyzing the Lending Protocol Inverse Finance: Can It Make a Comeback?

The gradual market recognition of the Inverse protocol is a positive development signal.

Author: LD Capital

1. Project Overview

Inverse Finance is an Ethereum-based CDP lending product that allows users to borrow the stablecoin DOLA by collateralizing cryptocurrencies. Launched in 2020, the project gained market attention after being endorsed by YFI founder Andre Cronje (AC). At the time, its product offered lossless yield generation around the stablecoin Dai—users deposited Dai into the protocol’s treasury and received an equivalent amount of deposit tokens called inDai, while the treasury deployed Dai into yield-aggregating protocols like Yearn to earn rewards in assets such as ETH and YFI.

Unfortunately, the project suffered two malicious attacks in 2022, leading to the suspension of its products. In October 2022, Inverse transitioned into a fixed-rate lending market.

2. Team

The only publicly known team member is Nour Haridy, the project's founder from Egypt, who has been working as a Web3 developer since 2018. In an interview with Cointelegraph, Haridy mentioned several years of experience developing in the Ethereum ecosystem, primarily designing gasless Dai smart wallets such as Metacash and Mosendo. Nour now works full-time on Inverse Finance, with 28k Twitter followers and moderate social influence.

Figure: Founder's Twitter

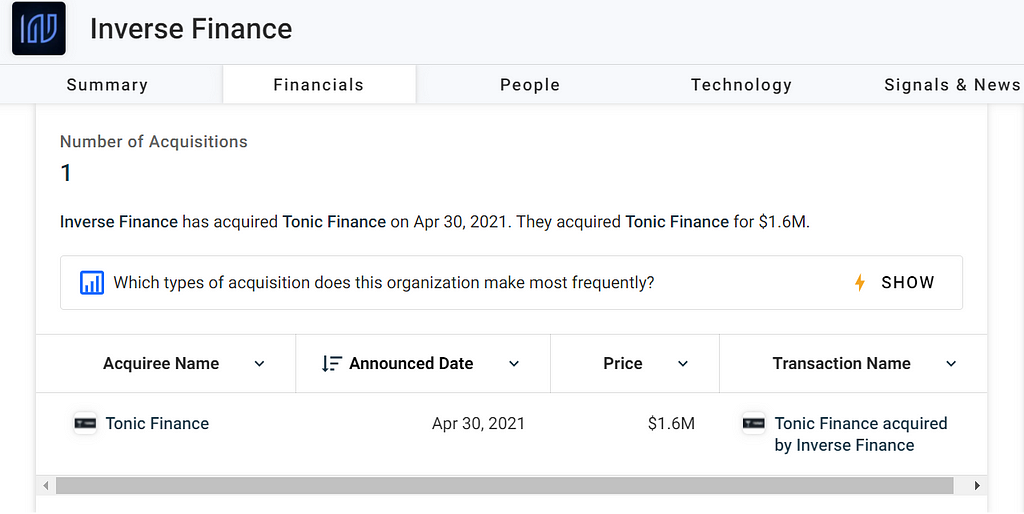

According to Crunchbase, Inverse acquired Tonic Finance on April 30, 2021, for $1.6 million.

Figure: Inverse Finance Public Profile

3. Products

Inverse’s current main products are the fixed-rate lending market FiRM and the stablecoin DOLA.

3.1 DOLA

DOLA is a decentralized stablecoin issued by Inverse Finance, pegged 1:1 to the US dollar and managed by the Feds smart contracts, which control DOLA’s supply and redemption.

Note: Due to oracle manipulation attacks on Frontier (the frontend), DOLA currently carries some bad debt. The DAO is actively repaying this debt, and the frontend product has been deprecated.

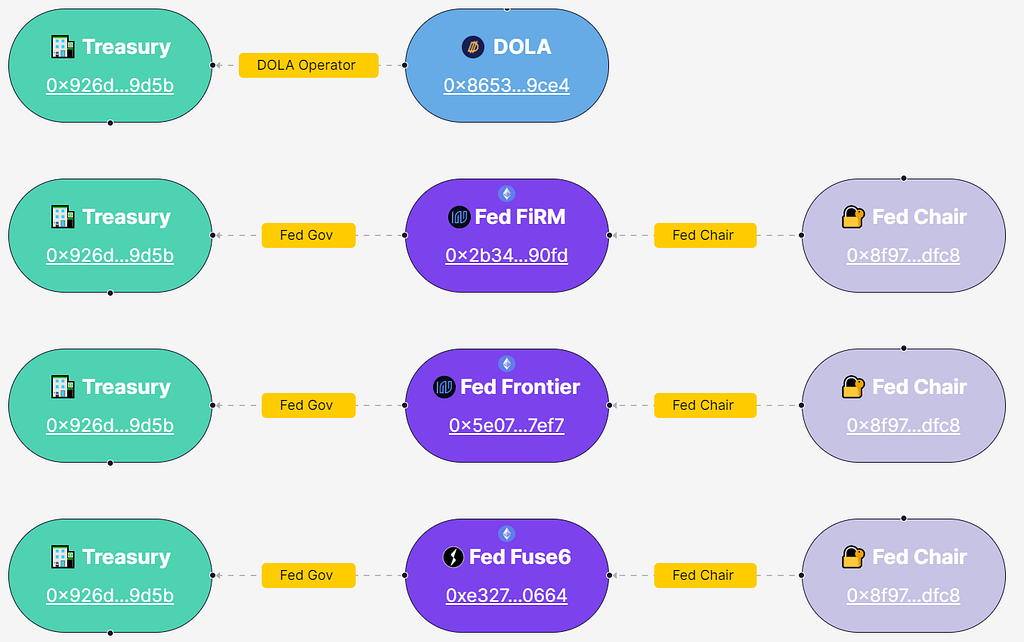

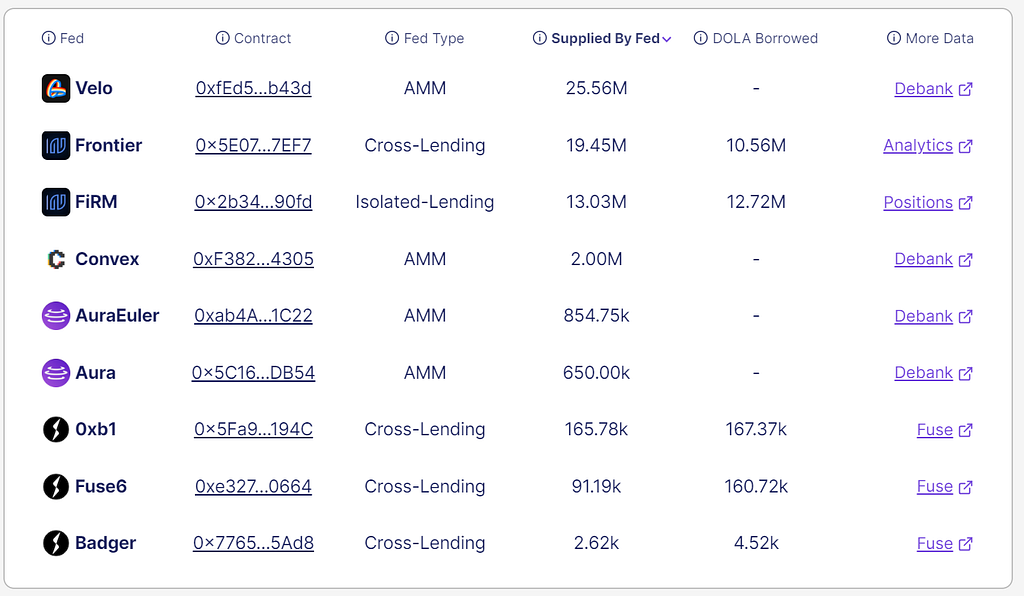

The Fed smart contracts are governed by Inverse DAO and come in three types. All can mint DOLA and directly supply it to liquidity pools or lending markets, or withdraw and burn DOLA to stabilize its price.

Figure: Types of Feds

Cross-Lending Feds: Refers to Frontier & Fuse; frontend now deprecated.

Isolated Mode Lending Feds: Refers to the FiRM lending market. FiRM sets global DOLA borrowing limits as well as daily borrowing caps per asset market. We will detail FiRM below.

AMM Feds: Provide liquidity to protocols such as Velo, Convex, and Aura.

3.2 FiRM

In February 2021, Inverse partnered with Anchor to launch the stablecoin DOLA. However, following the collapse of the Terra ecosystem and two successive attacks on Inverse, the existing frontend was suspended. In October 2022, Inverse launched its fixed-rate lending product, FiRM.

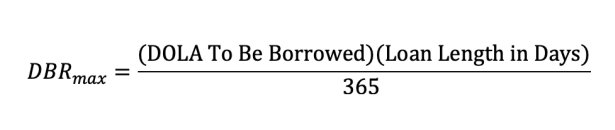

FiRM operates on over-collateralized lending, similar to other lending platforms. It is called “fixed-rate” because it implements fixed-cost borrowing based on DBR (DOLA Borrowing Rights). To borrow DOLA on FiRM, users must hold DBR—one DBR represents the cost of borrowing one DOLA for one year. The number of DBRs required per day can be calculated based on the amount of DOLA borrowed and the loan duration, allowing borrowers to estimate their total DBR usage and borrowing cost upfront. Loan durations can be extended at any time by adding more DBRs to the wallet.

DBRs were initially distributed via airdrops: ① INV stakers with balances remaining in the frontend application before October 30, 2022, each received 2,000 DBRs; ② Users could earn up to 1,000 DBRs through a raffle event.

DBRs are tradable on secondary markets, so increased or decreased borrower demand may cause DBR prices to rise or fall. High demand raises DBR prices—beneficial for investors but increases borrowing costs, reducing FiRM’s attractiveness and hindering Inverse’s growth. To address this, Inverse introduced DBR Streaming, issuing DBR rewards to INV stakers. By staking INV in FiRM, users earn DBR tokens. The community can adjust DBR emission rates to influence DBR prices and borrowing costs.

4. Fundamental Metrics

4.1 TVL

Current total TVL stands at $51.81 million. After the attacks, TVL remained stagnant until June 12, when Curve’s founder began depositing CRV and cvxCRV into Inverse and borrowing DOLA, significantly boosting Inverse’s TVL and drawing broader market attention.

Figure: TVL Trend

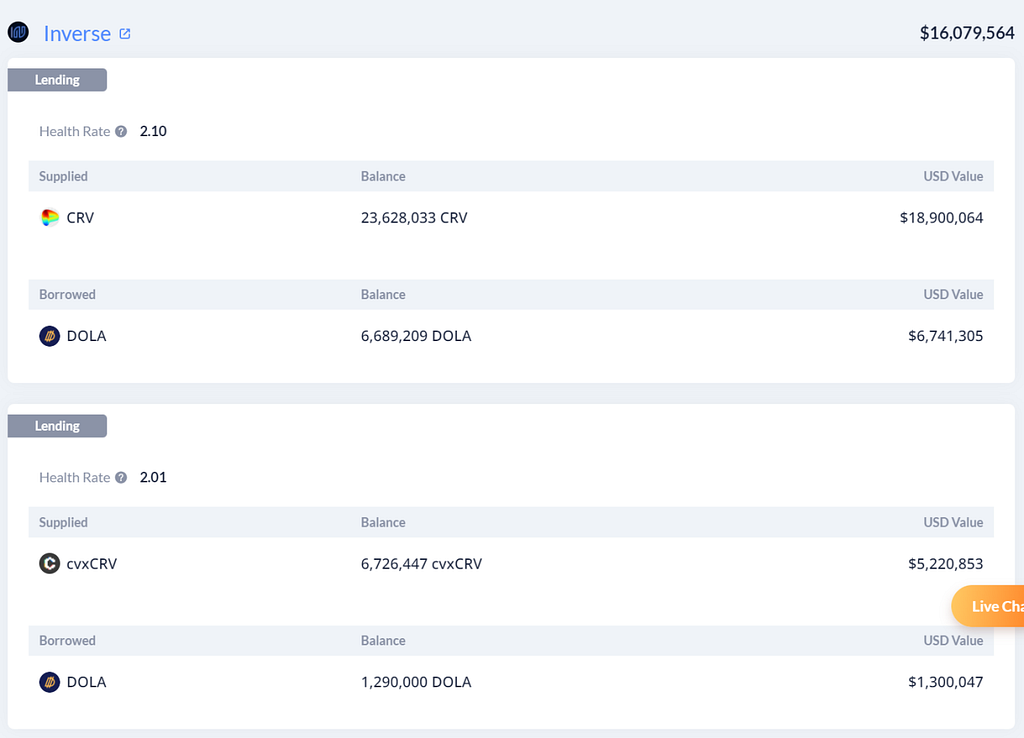

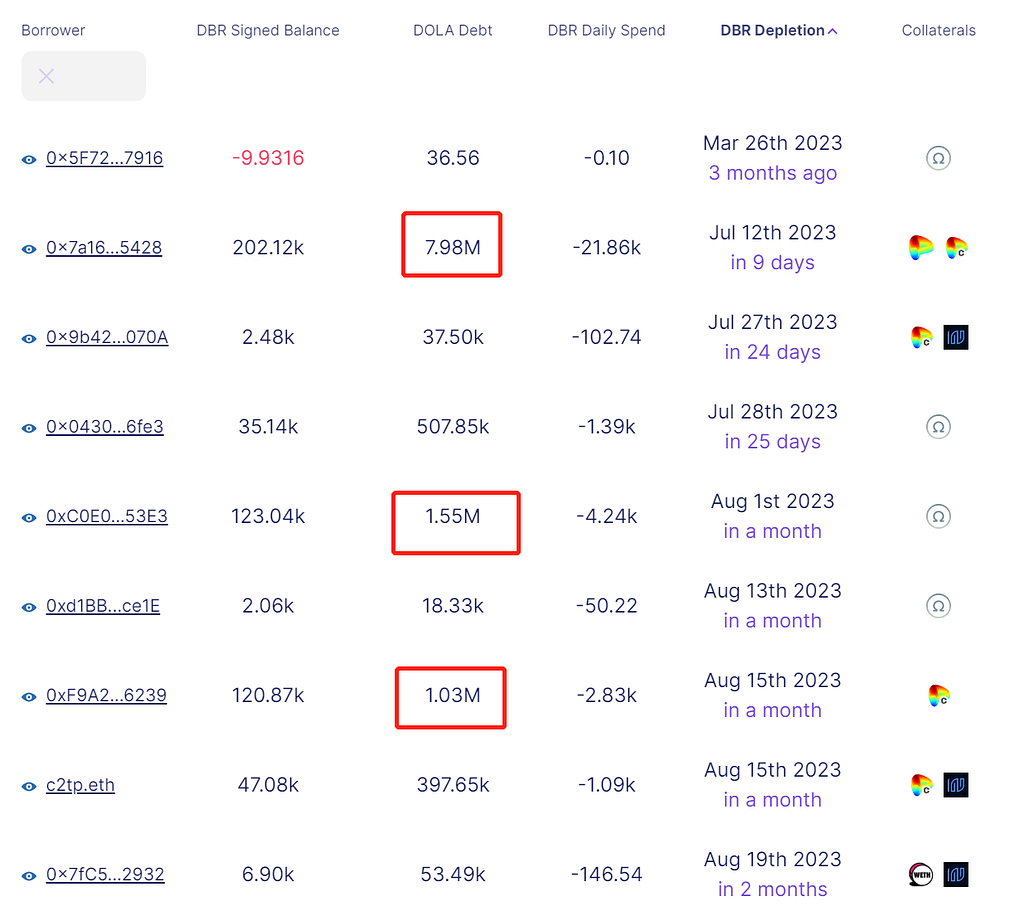

Currently, Curve’s founder has deposited approximately 23.63 million CRV and 6.73 million cvxCRV—worth about $24 million—and borrowed roughly 7.98 million DOLA. His individual position ($16.08 million) accounts for 31% of Inverse’s TVL, indicating significant dependency on Curve for protocol growth.

Figure: Curve Founder’s Account

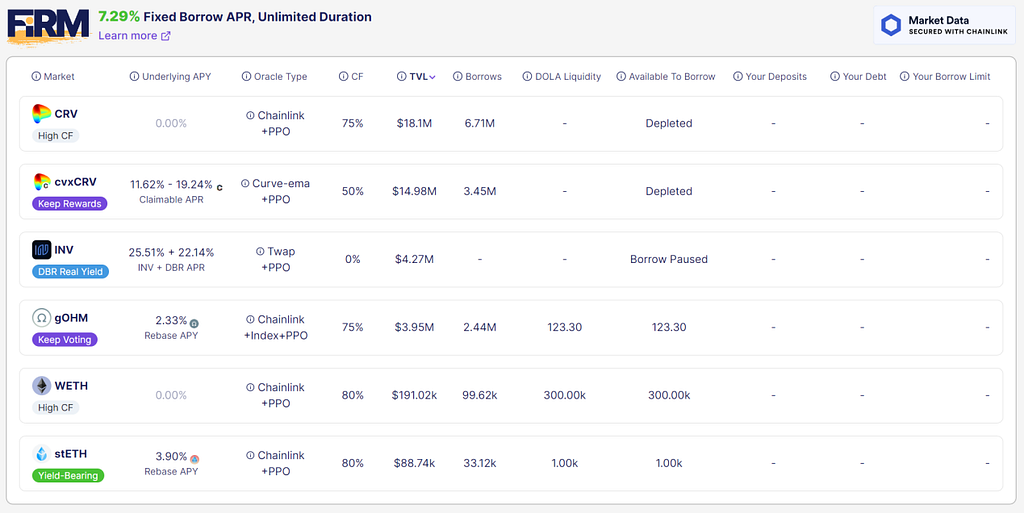

FiRM has been operating in "protected mode," imposing daily borrowing limits and total supply caps per asset. Supported assets include CRV, cvxCRV, gOHM, WETH, and stETH. CRV and cvxCRV dominate, accounting for the largest share. According to a May 2023 proposal, the CRV market has a daily borrowing cap of 1 million DOLA and a total supply cap of 10 million DOLA, while cvxCRV has a daily cap of 500,000 DOLA and a supply cap of 6 million DOLA. Combined borrowing in these two markets totals 10.16 million DOLA, reaching 63.5% of capacity. Due to rapid liquidity inflows, new deposits into these markets have been paused two weeks ago for security reasons.

Figure: FiRM Lending Market

4.2 DOLA

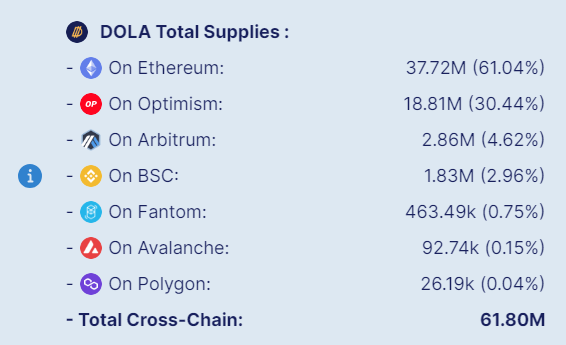

According to official data, DOLA’s current total supply is 61.8 million. Of this, 37.72 million (61.04%) are on Ethereum, followed by Optimism with 30.44%. Primary use cases are on Optimism’s DEX Velo and Inverse’s own product FiRM. The DOLA team places strong emphasis on Layer 2 adoption.

Figure: DOLA Issuance Scale

Figure: DOLA Distribution

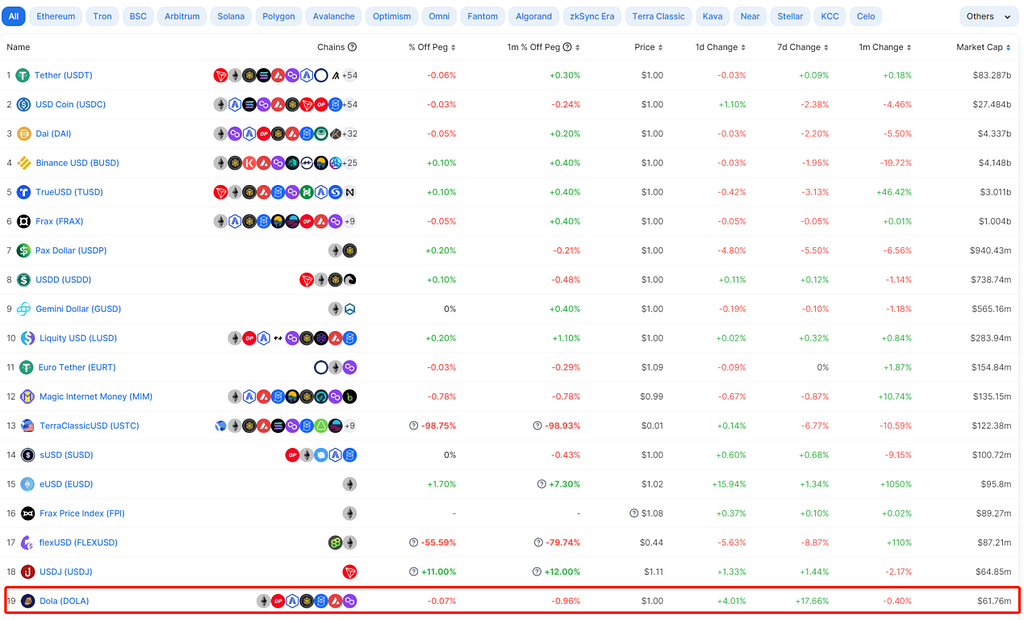

According to defillama.com, DOLA ranks 19th in stablecoin market capitalization, amounting to just 1.4% of DAI’s market cap ($4.337 billion), the leading decentralized stablecoin.

Figure: Stablecoin Market Cap Ranking

After the "hacking incident," DOLA’s price has remained relatively stable since October 2022. Two notable price fluctuations occurred recently: one on March 8 due to USDC depegging, and another on April 9 for unknown reasons.

Figure: DOLA Price Chart

5. Tokenomics

Inverse has three token types: DOLA, INV, and DBR. DOLA, the stablecoin, has already been covered. This section focuses on INV and DBR.

5.1 INV

INV is Inverse’s governance token, currently used only for staking and governance.

The full economic model of INV remains undisclosed. Token supply is determined by governance proposals; previously, a minting proposal was approved quarterly, with emissions aligned to liquidity strategies. A new proposal on June 30 set a mint of 60,000 INV for H2 2023 to fund DAO operations over the next 3–6 months.

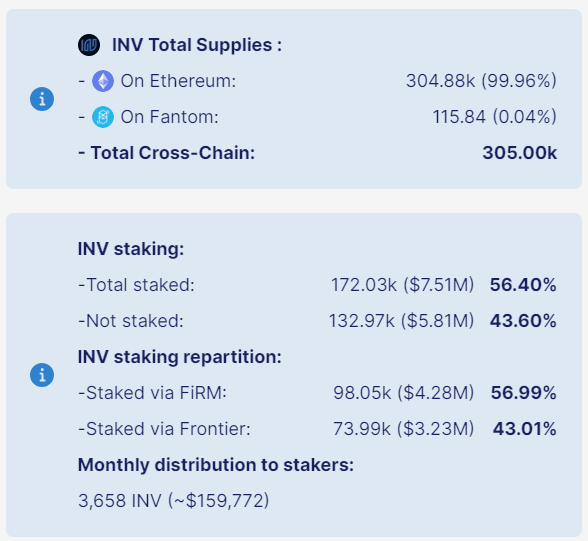

Total current supply is 305,000 INV, with a 56.4% staking rate. 98,000 are staked via FiRM, and 74,000 remain from legacy frontend staking. The frontend was deprecated in June 2022 following the attacks.

Figure: INV Token Supply

5.2 DBR

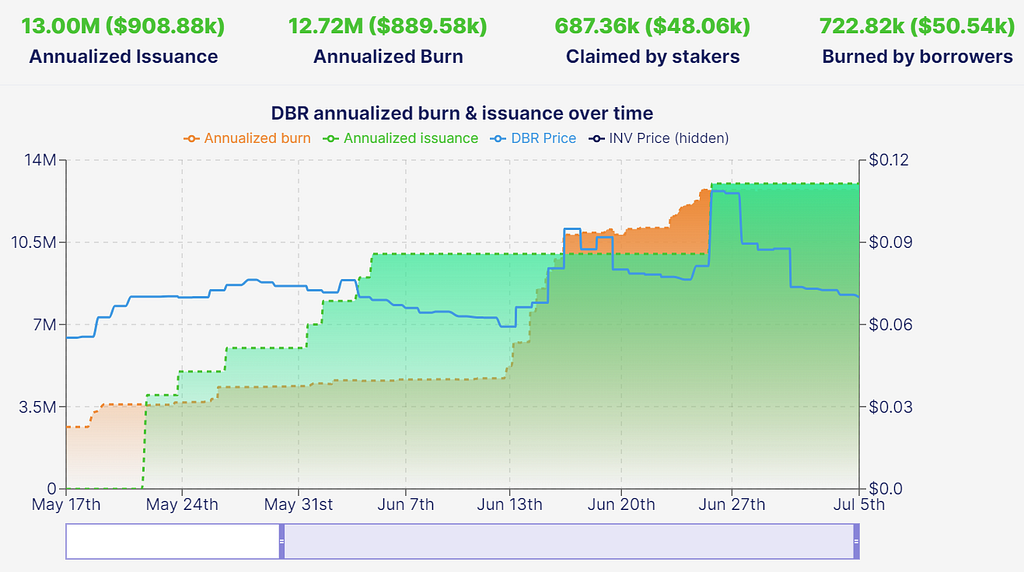

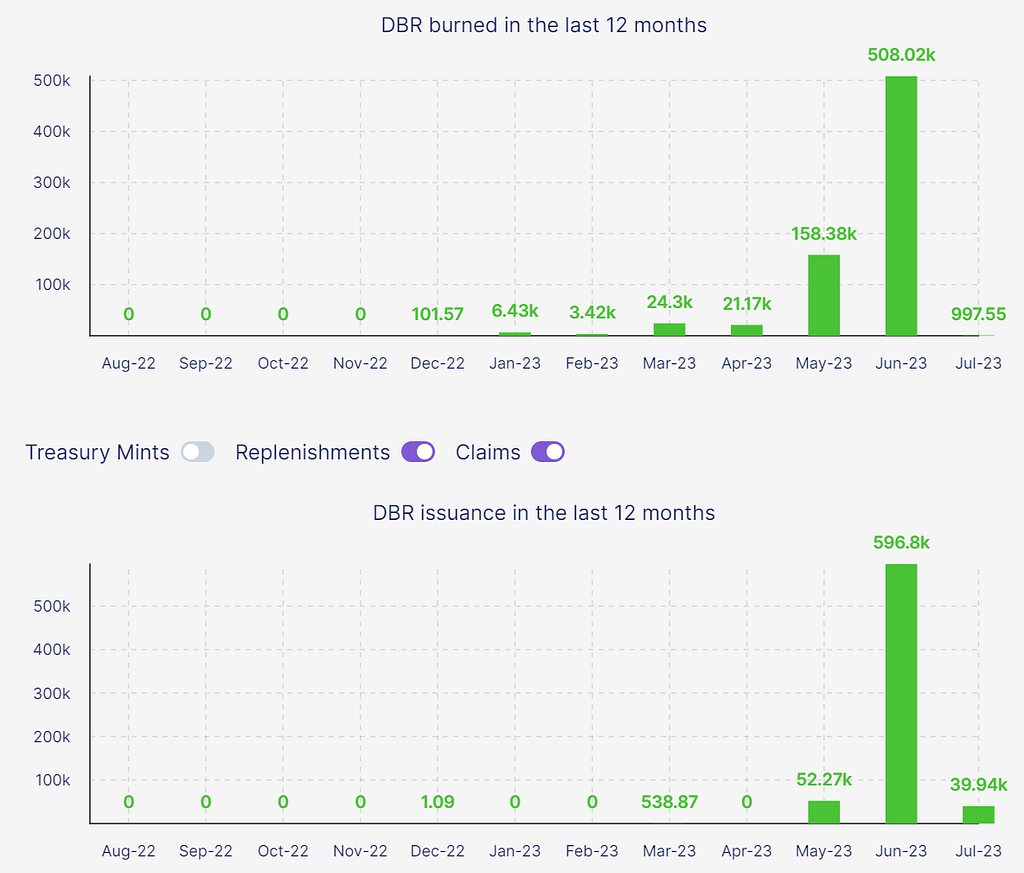

DBR has no supply cap and is controlled by Inverse DAO. Over the past year, 13 million DBR were issued and 12.72 million burned, leaving approximately 280,000 in circulation. According to Coingecko, total DBR supply is currently 4.646 million.

Figure: Annual DBR Supply and Burn

Since March, DBR burn volume has increased noticeably. In June, due to heightened activity in the CRV and cvxCRV markets, burns tripled compared to May, and annualized burns exceeded issuance—putting DBR into deflationary mode.

With rising borrowing activity on FiRM and increasing demand for DOLA loans, the community proposed raising DBR issuance from 10 million to 20 million annually.

Figure: Monthly DBR Supply and Burn

Recent DBR consumption shows CRV market as the primary driver, followed by OHM. The address 0x7a16 corresponds to the Curve founder’s position.

Figure: DBR Consumption

5.3 INV and DBR

DBR is a necessary consumable within the Inverse protocol, with real utility. Demand for DOLA borrowing directly drives DBR price appreciation. Rising DBR prices increase borrowing costs. To ensure sustainable growth and suppress borrowing costs, Inverse DAO can increase DBR emissions to expand supply and lower DBR prices.

DBR is primarily earned by staking INV. Increased DBR demand incentivizes INV holders to stake, enhancing INV’s utility. The two tokens reinforce each other.

6. Assets and Liabilities

6.1 Assets

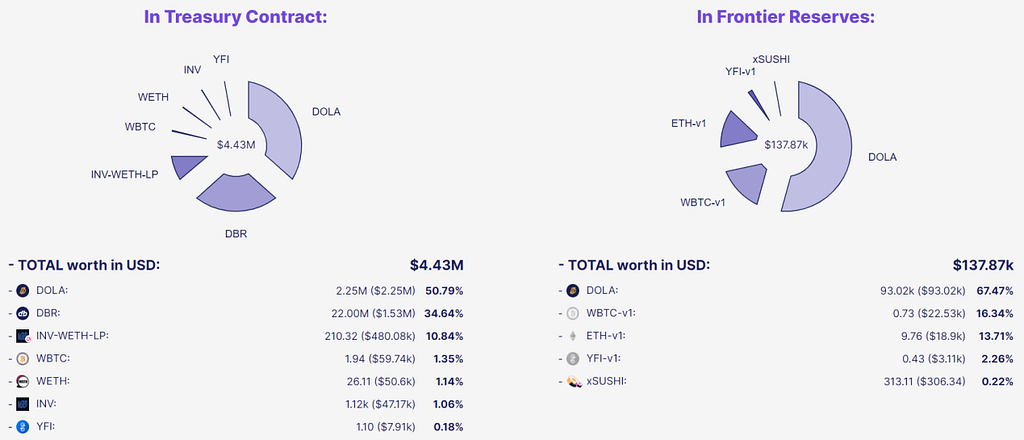

Treasury assets total $4.57 million, including $4.43 million held in Treasury contracts and $137,800 in Frontier reserves. Most treasury assets are DOLA ($2.25 million), followed by DBR ($1.53 million).

Figure: Treasury Asset Distribution

6.2 Liabilities

On April 2, 2022, Inverse Finance was exploited due to a vulnerability, losing 4,300 ETH (~$14.96 million). On June 16, 2022, it suffered a flash loan attack, losing ~$1.2 million.

As disclosed on Discord on June 28, outstanding DOLA bad debt remains at approximately $9.42 million. Since June 2022, the team has repaid $1.372 million, including funds raised through OTC sales to DWF and other entities.

The team continues to sell INV and DBR assets to repay bad debt. Latest updates:

1. A newly passed proposal mints 26 million DBR to be sold at a 15% discount (based on 30-day TWAP price on Coingecko) to whitelisted buyers, with a minimum transaction size of $100,000 to qualify for discount. The proposal took effect on July 3.

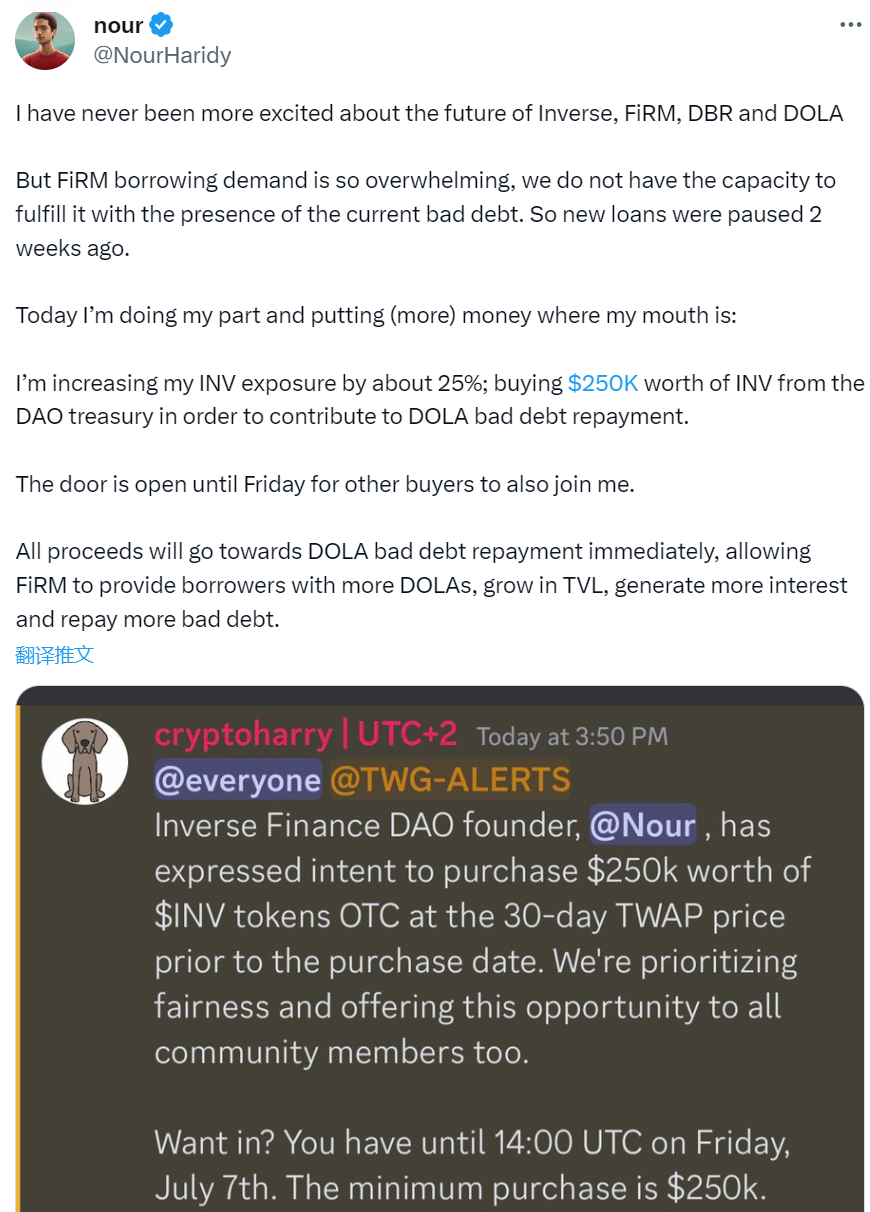

2. The founder announced on Twitter purchasing $250,000 worth of INV from Treasury at the 30-day TWAP price, with proceeds dedicated to bad debt repayment, and invited other buyers to participate. OTC sales will continue until July 7.

Figure: Founder Nour’s Twitter Post

Conclusion

Inverse’s main challenge today is the large amount of legacy bad debt. Currently, all protocol revenue and token sales are directed toward debt repayment, constraining product expansion. However, with Aave reducing exposure to CRV, the Curve founder has shifted part of his borrowing activity to Inverse, bringing renewed market attention. Although liquidity caps for CRV assets have been reached, Inverse’s TVL continues to grow steadily—a positive signal indicating gradual market recognition and healthy development momentum.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News