Why are we bullish on the NFT-AMM sector in the long term?

TechFlow Selected TechFlow Selected

Why are we bullish on the NFT-AMM sector in the long term?

Heimdall's wheel has begun to tremble; I look forward to the NFT AMM building a new rainbow bridge.

Author: Jeff, Foresight Ventures

I. The walls surrounding Asgard are impenetrable—enhancing on-chain asset liquidity remains an eternal topic.

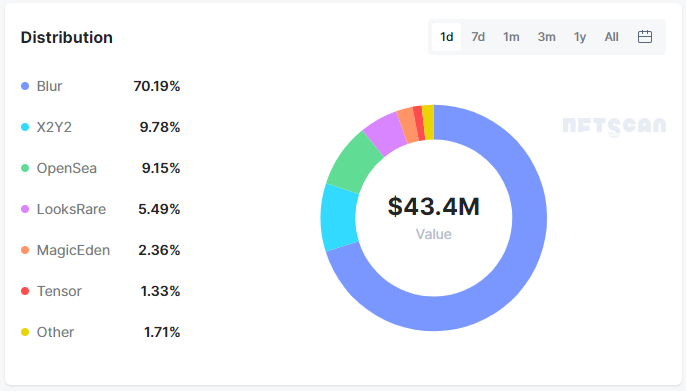

The emergence of DeFi opened a rainbow bridge straight to Asgard, where liquidity was fully unleashed. Designing innovative trading models to enhance NFT liquidity has become the shared goal across all NFT marketplaces. Although the current NFT market lacks a mature and unified pricing model, transaction volume data from blue-chip NFTs shows that order book-based marketplaces account for over 95% of total trading volume; in contrast, AMM-based marketplaces collectively represent less than 5% of trading volume.

Marketplace trading volume share

II. Drawing parallels from the CEX-to-DEX trading volume ratio in fungible tokens (FT), we see significant growth potential for AMM-based NFT trading volumes.

However, unlike FTs, NFTs come in diverse types. Their pricing mechanisms and trading behaviors mean only certain categories are suitable for AMM-driven liquidity solutions. Functionally, NFTs can be categorized into four groups: Profile Picture Projects (PFP), Virtual Assets (e.g., land, game items), On-chain Real World Assets (RWA), and On-chain Identities (domains, tickets, etc.). Considering issuance volume and holder trading demand, PFP and virtual asset NFTs are currently best suited for AMM trading models.

III. Why do we maintain long-term optimism about the NFT-AMM sector?

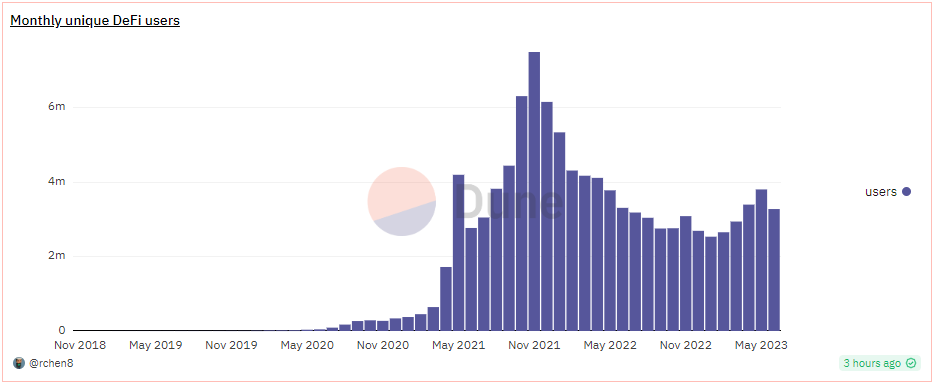

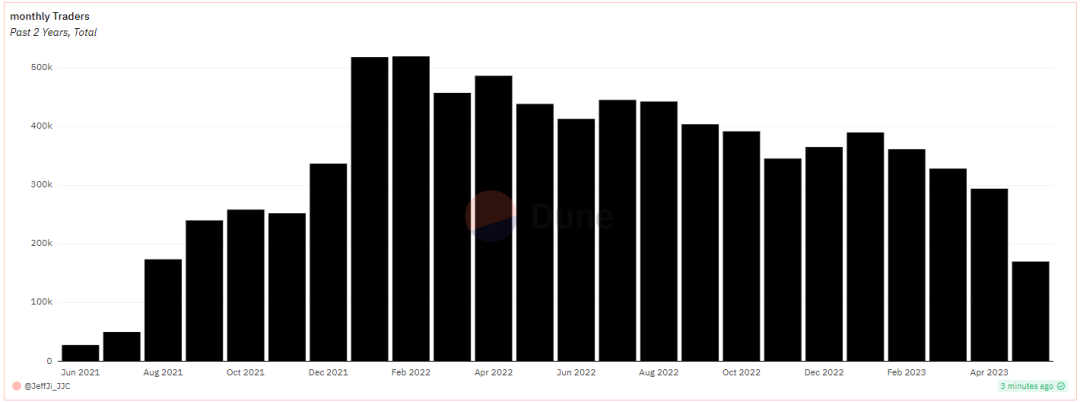

a) Vast potential user base. From a cross-chain ecosystem perspective, DeFi users represent the latent user pool for NFT-AMM platforms. Currently, DeFi ecosystems have around 1 million monthly active users, while independent NFT traders number only about 200,000. The NFT-AMM model can expand liquidity providers beyond NFT holders and traders to include all participants in the broader DeFi ecosystem.

Figure: Monthly Active Users in DeFi

Figure: Monthly Active NFT Traders

b) Significant room for growth in NFT types and quantities. Continuous innovation in functionality and composability means user adoption still has considerable upside. In May 2023, nearly all transactions on OpenSea originated from the top 100 NFT collections—a sharp increase from just 65% in February 2022 (https://dune.com/mizmatcat/OpenSea). This indicates that during bear markets, the ecosystem urgently needs stimulation through new NFT categories. Additionally, AAA gaming NFT assets are expected to peak in launches between 2023–2024, creating abundant opportunities for active NFT trading pairs.

c) The NFT-AMM sector can serve as a bridge between NFT and FT assets. Like DeFi tools, its composability unlocks vast innovation potential and thus higher growth ceilings. Before the rise of DeFi, FT liquidity was confined to centralized exchanges using order books. AMM protocols like Curve and Uniswap liberated on-chain assets and established new value recognition paradigms. Similarly, NFTs need AMM tools to achieve novel valuation frameworks and create new pricing models. We envision several directions for innovation in NFT-AMM models:

-

Integration with derivatives: NFT derivatives are an innovation hotspot. As Sally outlined in “IOSG Weekly Brief|From Commodity Speculation to Financial Speculation: The Semiotic Game of NFT Derivatives #174,” trading demands fall into several categories: speculation (profiting from NFT price swings with small capital), leveraged yield (increasing capital efficiency via leverage), risk hedging, and portfolio diversification with standardization. Driven by these diverse market needs, creating leveraged speculative markets allows NFT-AMM models to foster dynamic in-pool博弈 (strategic interactions), generating real-time on-chain data and expanding market depth. We anticipate such integration could lead to entirely new NFT pricing rules.

-

Integration with lending platforms: Leading NFT-backed lending platforms like BendDAO and Paraspace still rely on traditional models—users pledge NFTs and borrow amounts based on floor prices. Even after Blur entered this space, the competitive landscape hasn't shifted significantly. We expect that once NFT-AMM gains traction and funding, LP tokens could emerge as a new class of income-generating, collateralizable, and liquid asset receipts. By unlocking LP token liquidity, the existing lending market structure could transform, attracting non-NFT holders to participate via liquidity provision.

-

Helping projects reduce liquidity management costs via NFT-AMM. For game-related NFTs, relying solely on order book models forces project teams to constantly monitor floor prices without achieving automated liquidity management. We envision that under the NFT-AMM model, projects could inject assets into pools to dynamically and batch-adjust their NFT liquidity strategies.

IV. In the current AMM landscape, numerous platforms are exploring different directions.

Here, we examine several examples to illustrate existing product strengths and corresponding challenges.

a) NFTX pioneered introducing AMM models to NFT trading by using NFT fractionalization as its foundation.

NFTX aimed to use fractionalized NFT tokens as one side of a liquidity pool, paired with assets like ETH. This was a bold innovation that quickly gained attention. However, as NFT diversity increased, users realized this model expanded price volatility at the cost of eroding NFTs’ core scarcity trait—trading collectible value for tradability—leading to diminishing market acceptance over time.

b) Building on Uniswap V1, platforms like Sudoswap brought Uni-V3 mechanics into the NFT-AMM space.

Sudoswap adapted Uni-V3’s mechanism to NFT liquidity markets and innovatively introduced diversified product curves tailored for NFT trading. Users can create liquidity pools within tightly defined price ranges—typically near floor prices—to improve capital efficiency. However, initial liquidity is set solely by the creator, who also holds exclusive rights to add further liquidity. As a result, Sudoswap features multiple sub-pools arranged along optimal execution prices, each with varying depth and coverage. These pools operate in isolation, with no cross-pool liquidity sharing.

c) Midaswap improved upon prior AMM designs by adopting Trader Joe V2’s Liquidity Book model.

On Midaswap, users select price ranges to provide liquidity. Since each price "bin" maintains a fixed rate, all LP positions are aggregated into a single pooled liquidity source, enhancing overall depth. LPs can deposit single-sided liquidity and receive ERC721 LP tokens as proof. The clever use of ERC721 token IDs to track individual NFT liquidity contributions enables two key innovations: aggregating NFT liquidity into one pool while preserving original scarcity attributes—effectively combining the strengths of both NFTX and Sudoswap. Moreover, Midaswap is exploring cross-platform integrations between LP tokens and NFT lending protocols, enabling collateralized borrowing across platforms or customized liquidity mining per project needs.

V. Among these innovations, users express market feedback through on-chain activity. While unresolved issues remain, the progress compared to the stagnant landscape a year ago is substantial.

Below are some areas requiring further improvement.

a) Liquidity fragmentation is pronounced due to isolated pools. In current AMM designs, even NFTs from the same collection are split across multiple pools, mostly clustered near floor prices. This results in disconnected liquidity—when prices fluctuate or oracles are compromised, individual pools may collapse. With liquidity and depth only locally enhanced, users trade within small siloed pools, making large-scale buy/sell orders impractical.

b) Floor price still directly dictates AMM price ranges, preventing emergence of new pricing models. Fragmented liquidity forces LPs to anchor their pools to prevailing floor prices, making them passive followers of order book platforms. This eliminates any chance of becoming an independent pricing source.

c) Similar to above, excessive reliance on floor prices makes pools vulnerable to manipulation. Given the lack of interconnectivity, large buy/sell orders can easily distort prices, disrupting trading bot strategies within the platform.

d) Limited pool diversity hampers composability. A primary goal of AMM integration is to bring more on-chain assets into NFT trading pools, stimulating greater demand. Yet current AMM models still restrict pairing to ETH or a single native ecosystem token, excluding other assets from participating as LPs in NFT markets.

VI. After reviewing these challenges and pain points, we predict future breakout NFT-AMM projects will exhibit—or effectively solve—the following characteristics:

a) Support broader asset and user inclusivity, allowing non-NFT holders to contribute their assets to liquidity pools.

b) Achieve deep composability with other DeFi tools, using LP tokens to bridge diverse DeFi platforms and attract DeFi-native capital through varied yield mechanisms.

c) Enable composability with NFTFi assets—interoperability with lending, options, futures platforms—for expanded collateral types and improved capital efficiency.

d) Establish new pricing models—using AMMs to boost user acquisition efficiency, reducing dependence on oracle feeds and asserting autonomous price discovery.

VII. Despite imperfections in current offerings, we remain optimistic—perfect solutions for NFT liquidity and composability will eventually emerge.

Heimdall’s wheel has begun to tremble. We look forward to seeing NFT AMM build a new rainbow bridge.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News