Huobi Research: Will RWA tokenization be the next crypto wealth code?

TechFlow Selected TechFlow Selected

Huobi Research: Will RWA tokenization be the next crypto wealth code?

This research report provides a detailed analysis of 19 representative RWA projects from multiple dimensions, including RWA tokenization mechanisms, protocol status, token functions and performance, as well as protocol advantages and risks.

TechFlow has released "RWA: The Next Crypto Wealth Code", a research report providing a comprehensive overview of the RWA sector's development. This report analyzes 19 representative RWA projects across multiple dimensions including tokenization mechanisms, protocol status, token functionality and performance, as well as protocol advantages and risks. By analyzing and summarizing these projects, we gain insight into the overall development, existing challenges, and future potential of the RWA space.

Introduction

Blockchain brings trust, liquidity, transparency, security, efficiency, and innovation. However, during the crypto bear market, it has been difficult to find new growth drivers, and the industry urgently needs a new narrative. RWA tokenization can bridge traditional finance and crypto finance, accessing an asset market worth tens of trillions of dollars—making it a potential lifeblood for the crypto industry beyond bull and bear cycles. While RWA tokenization has long been attempted since blockchain's inception, it has faced obstacles from technology, regulation, and market factors. Now, the RWA sector is gaining renewed attention, with multiple institutions beginning to position themselves in this space. RWA projects have become increasingly diverse, predominantly DeFi-focused, offering high yields but also high risk, gradually entering public awareness. However, most projects still face issues such as poor liquidity, early-stage development, and lack of price discovery. Whether the RWA sector will explode in the coming years depends on infrastructure development and regulatory maturity. This report emphasizes that token standardization and compliance are essential pathways for RWA development. Despite facing multiple challenges, the industry continues to progress forward. We are already witnessing innovative projects emerge, particularly those based on U.S. Treasuries and equities, SME financing, and physical assets. These projects share three main characteristics:

1. Collaboration with traditional financial institutions;

2. Maximizing project and token yields;

3. Introducing more legitimate third-party participants.

These features help address some of the problems in RWA tokenization—including regulation, centralization, on-chain/off-chain identity, and asset valuation—and we look forward to seeing more projects enriching the RWA ecosystem.

1. An Emerging Narrative

After over a year-long bear market, the total market cap of the crypto industry has significantly shrunk, capital continues to flow out, on-chain activity remains depressed, and DeFi yields no longer attract interest, resulting in severe internal trading. It's hard to imagine what could spark the next bull market. There remains a substantial gap between the crypto and traditional financial markets. Yet, from the collapses seen during the bear market, we can glimpse enormous business opportunities.

The primary cause behind the bankruptcies of several major institutions in 2022 was their reliance on altcoins for fundraising and borrowing. When these altcoins crashed during the bear market, it intensified loan liquidations, triggering a death spiral. We saw that institutions and credit fueled the 2021 bull run—and they also drove the 2022 bear market. In reality, credit underpins trillions of dollars in business and much of global economic development. Its potential is immense. Currently, in the DeFi market, more protocols are entering traditional credit markets like equity and debt financing. While this introduces certain risks, it is the only way to bring over $80 trillion in traditional financial markets on-chain. To bridge the gap between crypto and traditional finance, we must tokenize real-world assets (RWA).

In the first half of this year, both traditional and crypto industries began paying attention to the RWA sector.

First, Goldman Sachs announced its digital asset platform GS DAP officially launched, which had already helped the European Investment Bank (EIB) issue a €100 million two-year digital bond. Shortly after, Hamilton Lane, a private equity firm managing over $100 billion, tokenized part of its $2.1 billion flagship equity fund on Polygon and offered it to investors. Siemens, the engineering giant, issued a €60 million digital bond on the blockchain for the first time. Additionally, government agencies have begun exploring RWA, including the Monetary Authority of Singapore (MAS), partnering with JPMorgan Chase and DBS Bank.

In April, Binance announced it would become a node operator for Layer-1 blockchain Polymesh. Meanwhile, DeFi protocols such as MakerDAO, Aave, and Maple Finance have been active in the RWA space, and more crypto investment firms are seeking RWA-related projects. Currently, there are over 50 RWA projects, primarily focused on financial assets including fixed income and TradFi, with fewer in real estate and carbon credits. Recently, RWA concept tokens have seen price increases, with some rising over tenfold. Will the momentum built in the first half of 2023 signal that RWA will lead the next wave of crypto narratives in the coming years?

2. The Past and Present of RWA

The concept of RWA is not new in the blockchain industry. The earliest RWA project was Bytom, focusing on "asset-on-chain." Today, the most successful RWA examples are digital dollar stablecoins USDT and USDC—essentially tokenized representations of fiat dollars. Stablecoins have quietly influenced the entire crypto industry and have now become foundational pillars.

RWA stands for Real World Assets tokenization—the process of converting ownership value (and associated rights) of tangible or intangible assets into digital tokens. This enables digital ownership, transfer, and storage of assets without centralized intermediaries, mapping value onto blockchains for trading. RWAs can be either tangible or intangible.

Tangible assets include: real estate, art, precious metals, vehicles, sports clubs, racehorses, etc.

Intangible assets include: stocks and bonds, intellectual property, investment funds, synthetic assets, revenue-sharing agreements, cash, accounts receivable, etc.

2.1 Current State of the RWA Sector

RWA projects come in various forms, mostly DeFi-based, falling into three main categories: 1) Fixed-income projects based on off-chain assets such as U.S. Treasuries, equities, real estate, and art; 2) Public credit projects involving publicly issued or traded instruments; 3) Trading market projects based on virtual assets like carbon credits. In addition, there are vertical public chains serving as infrastructure.

Fixed-income projects leverage U.S. Treasuries and equities to offer loans to individuals and institutions. Their key distinction from other DeFi lending projects lies in accepting real-world assets as collateral.

Public credit projects allow crypto users to invest via funds tracking U.S. Treasuries or other bonds.

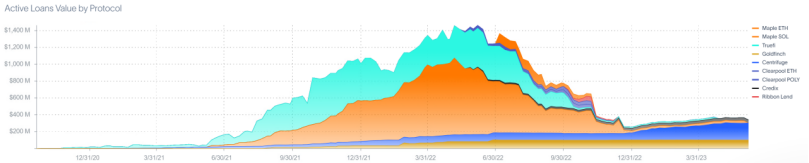

According to data from RWA.xyz, eight RWA lending protocols—including Centrifuge, Maple, GoldFinch, Credix, Clearpool, TrueFi, and Homecoin—have collectively disbursed $4.38 billion in loans, with users earning an average APR of 10.52%, primarily serving countries with lower to middle development levels. These credit protocols offer higher yields than most DeFi lending platforms, though Maple Finance suffered a $69.3 million default during the 2022 institutional collapse.

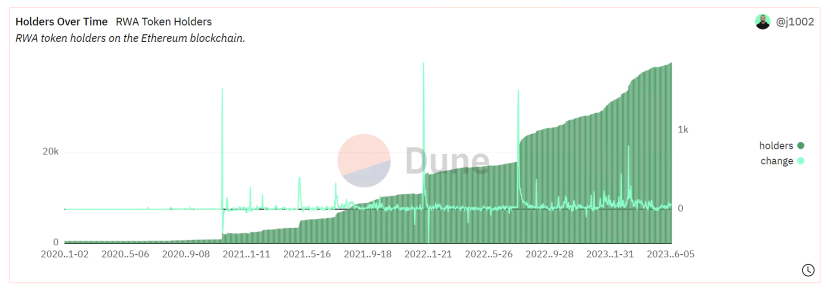

According to Dune Analytics dashboards, the number of holders for RWA tokens such as $wCFG, $MPL, $GFI, $FACTR, $ONDO, $RIO, $TRADE, $TRU, and $BST on Ethereum continues to grow, currently reaching 3.9k addresses.

2.2 Advantages of Asset Tokenization

Ideally, any valuable asset could be tokenized. The benefits stem from decentralized blockchain technology, creating applications that solve inefficiencies in traditional finance:

(1) Unlocking massive markets, attracting both investors and retail users

As leading financial institutions seek to benefit from blockchain efficiency and economic possibilities, RWA tokenization is gaining institutional attention, with several tokenized products already developed. RWA projects will also boost DeFi investment returns.

By tokenizing real-world assets, businesses can access capital through the DeFi ecosystem at lower costs, benefiting from reduced entry barriers and new funding methods—especially relevant for emerging markets. Simultaneously, the DeFi ecosystem gains investment returns, access to diversified off-chain markets, and opportunities to expand into traditional finance customer bases.

(2) Improving capital efficiency and enabling positive feedback loops for asset tokenization

Traditional financial markets are labor-intensive, while blockchain technology offers instant settlement and 24/7 trading, lowering operational costs and market entry barriers. Moreover, asset tokenization turns illiquid assets into fractional portfolios, eliminating the need for extensive paperwork, large sums of money, or prolonged time commitments. This creates a fairer market and fosters new business and social models, such as shared property ownership or rights sharing.

In securities, tokenization serves as a useful tool to securitize assets or refinance low-liquidity assets into more liquid instruments.

Bringing real-world assets on-chain into the DeFi ecosystem unlocks unique collateral or investment opportunities, improves market efficiency, and provides liquidity unattainable in traditional markets. Enhanced capital efficiency further fuels RWA sector growth, creating a virtuous cycle.

(3) Lowering retail entry barriers and increasing physical asset liquidity

Tokenization removes current barriers preventing real-world asset fragmentation, allowing retail investors access to asset classes typically reserved for high-net-worth individuals or institutional investors—particularly in physical assets. Retail users can invest in cross-regional products or jointly purchase real estate or artwork—activities requiring prohibitively high thresholds in traditional finance. Illiquid physical assets gain access to global investors once tokenized. Issuers can reach broader investor pools and create new asset classes. Retail investors enter previously inaccessible markets and make smarter decisions using transparent data.

(4) Leveraging blockchain’s strengths for more efficient and secure RWA transactions

Blockchain ensures transparency in on-chain payments and data flows, immutability and traceability of transaction records, higher efficiency, lower operating costs, robust risk management, clear ownership, greater composability, and a fairer market environment. As blockchain evolves, higher-performance L1s or L2 solutions, stricter smart contract audits, and privacy-preserving zk-based projects will provide fertile ground for RWA development.

3. Prerequisites for RWA Sector Growth

Asset-on-chain is the sole critical point for the RWA sector. Addressing this requires two foundations: mature blockchain infrastructure and legal regulation. Blockchain involves interoperability, security, and privacy across protocols and tokens. Legal regulation concerns whether off-chain assets and on-chain identities have corresponding legal frameworks. Many issues are actively debated, but here we focus on two: token standards and auditing systems.

3.1 Diversified Token Standards

On-chain token standards include ERC-721 and ERC-20 on Ethereum, representing non-fungible and fungible tokens respectively. Traditional financial assets vary widely—tangible and intangible. On blockchains, we need corresponding token standards based on asset attributes. Fungible and non-fungible tokens have distinct features:

Fungible Tokens: Interchangeable, each unit having identical market value and validity, meaning token holders can swap assets confidently. Divisible—assets can be split into smaller units, each retaining proportional value and validity.

Non-fungible assets are non-interchangeable and irreplaceable because each unit represents unique value with distinct information and attributes. NFTs are generally indivisible, though partial ownership via cost-splitting exists (e.g., commercial real estate).

Most assets can use fungible token standards, but some—like bonds and derivatives—may benefit more from NFT-based tokenization. As RWA projects grow, more formats may emerge, making simple ERC-20 and ERC-721 standards insufficient. Vertical RWA public chains anticipate this and begin developing dedicated tokenization standards, such as Polymesh. Given most RWA projects currently operate on Ethereum, expanding ERC standards offers broader applicability. ERC-3525 is widely discussed, and more standards may emerge—especially post-BRC-20. Ideal RWA-enabling token standards should possess two traits:

(1) High operability and flexibility for RWA issuers, combining features of both ERC-721 and ERC-20;

(2) Some privacy to protect transaction and user data.

3.2 Strict Auditing Systems

Security is crucial for tokenized real-world assets, especially when used as collateral. For RWA issuers and investors, due diligence on DeFi protocols is vital—prioritizing secured loans, strict regulatory compliance, and technology/services built with high-quality open-source code. Project teams may need to offer two key solutions:

-

Avoid KYC/AML risks—conduct Know Your Customer (KYC) or Anti-Money Laundering (AML) checks on platform users and/or transactions. Prevent direct or indirect interactions or transactions with counterparties listed on OFAC or other sanctions lists, or politically exposed persons.

-

Provide effective monitoring tools—products and services to monitor and detect suspicious activities by DeFi users.

Thus, projects require dedicated compliance teams to review and approve or reject user access based on identity verification, risk assessment, and due diligence. Additionally, continuous monitoring of user activity helps identify potentially fraudulent or money-laundering behavior.

4. Representative Project Analysis

The RWA sector encompasses multiple subcategories. This report analyzes 19 representative RWA projects across dimensions including tokenization mechanisms, protocol status, token functions and performance, and protocol advantages and risks. Through analysis and summary, we gain insights into the overall development, challenges, and future potential of RWA projects.

4.1 U.S. Treasury Concepts

(1) MakerDAO

In 2020, MakerDAO formally incorporated RWA into its strategic priorities, releasing guidelines and plans for RWA integration. Beyond issuing its stablecoin DAI, Maker expanded accepted collateral types beyond ETH to include tokenized real estate, invoices, and accounts receivable. Maker's primary revenue sources are DAI lending interest and liquidation penalties.

Protocol Status: By TVL, Maker ranks among the top three DeFi protocols, behind Lido and Aave, and leads Collateralized Debt Position (CDP) protocols.

Currently operating solely on Ethereum, as of June 2, 2023, DefiLlama reports a TVL of $6.29 billion, 30-day protocol revenue of $23.53 million, treasury holdings of $68.4 million. The governance token $MKR is listed on major exchanges including Coinbase, Binance, KuCoin, Kraken, OKX, Huobi, Bybit, and Gate, with a 24-hour trading volume of $13.58 million and a 30-day average volume nearing $20 million.

-

Token Functionality: $MKR serves as MakerDAO's governance token. Its price performance has been weak, mainly due to limited value capture by the protocol, though it plays a significant role in governance. $MKR utility includes four aspects:

-

Governance Rights: MKR holders govern the MakerDAO system, voting on critical matters such as system parameters, risk management measures, and protocol changes. Their votes significantly influence MakerDAO’s development and operations.

-

Collateral Stabilization: MKR tokens can serve as collateral within the MakerDAO system. Users generate stablecoins (e.g., DAI) by locking crypto assets (e.g., Ethereum), requiring payment of MKR as additional collateral. This mechanism aims to ensure system stability and security.

-

System Stability Buyback: MKR collateral is used in a buyback mechanism. If DAI’s value drops below its USD peg, the system automatically buys back and burns MKR tokens to stabilize itself.

-

Risk Sharing: MKR holders assume risks within the MakerDAO system. If debts cannot be repaid or other issues arise, MKR token value may suffer. This incentivizes MKR holders to actively participate in and oversee system operations to ensure safety and stability.

-

Protocol Advantages:

-

1. Built on EVM and L2 ecosystems, enjoying a loyal user base and stable, secure network support compared to other public chain RWA protocols;

-

2. Institutional advantages tested through bull and bear cycles, featuring strict collateral admission criteria, over-collateralization, and a robust auction system ensuring DAI maintains its 1:1 USD peg in most cases, with emergency shutdown mechanisms available in extreme scenarios.

-

-

Protocol Risks:

-

1. Governance attacks: Short-term concentration of MKR ownership could lead to governance centralization, risking malicious actions such as adding junk collateral, initiating emergency shutdowns, or tampering with risk parameters. However, as MKR value rises and internal risk controls strengthen, such risks are largely mitigated;

-

2. Market price risk: During periods of increased volatility in major tokens, cascading protocol auctions increase token supply, worsening liquidity—a recurring issue during past broad crypto downturns—though the protocol itself hasn't incurred major losses.

-

(2) Ondo Finance

Ondo Finance is one of the most watched RWA projects in the first half of this year, raising $20 million in a Series A round led by Founders Fund and Pantera Capital in April. Ondo Finance operates as a decentralized investment bank, investing off-chain in U.S.-listed money market funds, and on-chain offering stablecoin lending services via Flux Finance with USDC, FRAX, DAI, and USDT, averaging around 5% interest. Protocol revenue comes from a 0.15% annual management fee.

Users must complete KYC/AML procedures before trading fund tokens or using them in permissioned DeFi protocols. Ondo Finance has launched four tokenized bond products for investor selection:

-

U.S. Money Market Fund (OMMF): Invests in high-credit-rated U.S. government bonds and short-term debt instruments, prioritizing capital preservation, currently yielding ~4.5% annually.

-

U.S. Treasury Bonds (OUSG): Invests in short-term U.S. Treasury ETFs, currently yielding ~4.85% annually, with $100.87 million TVL.

-

Short-Term Bonds (OSTB): An actively managed ETF aiming for maximum current income while preserving capital and ensuring daily liquidity. Primarily invests in short-term investment-grade debt securities with an average portfolio duration under one year, currently yielding ~5.77% annually.

-

High-Yield Bonds (OHYG): Primarily invests in high-yield corporate debt, currently yielding ~7.9% annually.

Protocol Status: $100.5 million TVL on Ethereum, ranking first among DefiLlama’s RWA category. OUSG has the largest usage scale. OUSG holders can deposit into Flux Finance, Ondo’s own decentralized lending protocol, to earn yield. According to Tzedonn of Tioga Capital, the current market cap of bond tokens is $168 million, with Ondo (OUSG) holding 61% market share, 28% of which is deposited into Flux Finance. Flux Finance’s total supply exceeds $40 million, and OUSG’s market cap has surpassed $100 million. The lending protocol FLUX has been sold to Neptune Foundation.

Token Functionality: The governance token $ONDO offers four functions:

Platform Fee Payment: Users may pay transaction, lending, or other financial service fees on Ondo Finance using $ONDO tokens.

Voting Rights and Governance: $ONDO holders can participate in platform governance, voting on upgrades, parameter adjustments, proposals, and influencing platform direction.

Rewards and Incentives: Ondo Finance may distribute $ONDO token rewards to encourage user participation and ecosystem contributions.

Lending and Collateral: Users can use $ONDO tokens as collateral to obtain loans on Ondo Finance, unlocking higher borrowing limits or lower interest rates.

Protocol Advantages: Compliance-first approach—products are either low-risk U.S. government-related debt instruments or high-risk ETFs—all being compliant, third-party audited financial products. Users must pass KYC/AML processes.

Protocol Risks:

1. Off-chain risks: Core products are off-chain ETFs and U.S. government debt instruments—compliant but exposed to external market and credit risks, especially OHYG's high-yield corporate bonds;

2. Centralization drift: The project appears to be shedding decentralization, shifting toward a centralized + compliant operational model. The governance token may be marginalized, with blockchain used merely for profit distribution, accounting, and share sales—not progressing toward full decentralization, contradicting core crypto principles.

(3) Maple Finance

Maple Finance has evolved over three years, primarily offering institutional credit loans. On-chain, it provides USDC and wETH lending services, but individual centralized pool managers oversee lending operations—including borrower selection, amounts, interest rates, and strategies. Though Maple Finance may not seem like a pure RWA project, in April it announced plans to launch a lending pool investing in U.S. Treasuries, allowing non-U.S. DAOs and offshore companies to contribute capital into Maple-managed pools.

Protocol Revenue: Maple Finance generates income through several streams:

-

Borrowing Fees: Charged based on loan amount and term, calculated according to pool-set interest rates.

-

Loan Processing Fees: Platform charges for loan applications, disbursements, and settlements.

-

Token Mining Rewards: May distribute rewards to participants providing liquidity or joining lending pools.

-

Platform Governance Fees: A percentage charged to support platform operations, including feature development, security audits, and community governance.

Protocol Status: On DefiLlama, Maple Finance ranks #145 by TVL but leads unsecured lending protocols with $48.56 million TVL, $32.22 million outstanding debt, cumulative earnings of $45.6 million, 18 active loans (few due to centralized credit-backed nature), and 8 cash pools (7 USDC + 1 ETH, averaging 7% APY over 30 days). Maple also has minor TVL on Solana, but with declining on-chain activity, it holds only ~$16.4k TVL, with 99% originating from the Ethereum mainnet.

Token Functionality: MPL is Maple Finance’s native token, serving several roles:

-

Fee Payments: MPL can be used to pay transaction fees on the platform, often with discounts to incentivize token usage and holding.

-

Community Governance: MPL holders participate in platform governance, proposing and voting on key decisions affecting platform direction.

-

Voting Rights: MPL holders have voting power on protocol parameters, upgrades, and other important matters.

-

Profit Sharing: MPL holders qualify for profit distributions from Maple Finance’s lending pools, sourced from borrower interest or other income, allocated proportionally.

Incentive Mechanisms: Maple Finance may offer incentives to MPL holders to promote ecosystem growth, including airdrops, rewards, or other benefits encouraging user engagement and platform expansion.

Protocol Advantages: Enhanced security—lending risk is managed by pool operators who receive management fees. Liquidity providers enjoy lending yields while bearing reduced default risk.

Protocol Risks:

1. Credit risk: Pool managers and borrowers are vetted by centralized entities, and loans rely on credit rather than asset collateral (collateral comes from pool managers). Widespread institutional defaults could lead to insolvency;

2. High barriers: To ensure debt safety, lending thresholds remain high, excluding most users, limiting community engagement.

4.2 TradFi

(1) Polytrade

Polytrade is a decentralized trade finance platform aiming to provide seamless loans to enterprises across industries. Since January 2022, it has reported zero defaults and zero LP losses. V3 plans to add NFT capabilities for real assets, potentially launching an NFT secondary market.

Protocol Status: Governance token TRADE is listed on KuCoin, Gate, MEXC, Bitfinex, with primary trading on MEXC. DefiLlama shows minimal TVL of $10,984—far below the fully diluted $17.27 million market cap, indicating possible overvaluation. Raised $3.8 million in seed funding on March 30, 2023, from Polygon Studios, Matrix, CoinSwitch, Alpha Wave Global, and others.

Token Functionality: TRADE is the governance token, primarily used for voting on protocol revenues and updates. More detailed token utility may be disclosed upon V3 launch.

Protocol Advantages:

1. Lower transaction costs on Polygon, leveraging EVM-native advantages like gas fees and speed;

2. Strategic advantage—backed by Polygon, likely securing competitive positioning within the Polygon EVM ecosystem.

Protocol Risks:

1. Credit risk: Although lending occurs on-chain, borrower selection, business evaluation, and approval happen off-chain. The project claims protection from institutions like AIG and Mercury, but cannot eliminate counterparty default risks;

2. Technical risk: Transitioning from V2 to V3, with no third-party audit reports yet released, leaving potential undiscovered bugs.

(2) Defactor

Defactor connects traditional finance with DeFi, aiming to provide businesses with financing and liquidity. Still unlaunched and in early stages. According to its roadmap, H2 2023 remains focused on recruitment, developer hiring, and development. According to the official website, $FACTR is the native token of the Defactor ecosystem, designed to lower application and infrastructure usage barriers, align incentives, and drive ecosystem growth.

4.3 Lending

(1) Goldfinch

Goldfinch is a decentralized credit protocol targeting off-chain entities, fintech companies, and debt funds—similar to Maple Finance. Goldfinch offers uncollateralized USDC credit lines. Its model resembles traditional banking but uses decentralized auditors, lenders, and credit analysts. Borrowers convert USDC to fiat and deploy it to end-borrowers locally. Before loan approval, borrowers must be verified by a protocol auditor—an independent entity required to stake the governance token GFI to validate borrowers in exchange for rewards.

Revenue Sources: 10% of all interest payments are retained in the protocol treasury. Additionally, a 0.5% fee applies when users redeem from the Senior Pool, also directed to the treasury.

Protocol Status: Total outstanding principal across all loans is $101.34 million, with a 0% loss rate. Repaid principal and interest total $25.1 million. Generated $100,100 in revenue over the past 30 days. No bad debt reported so far.

Token Functionality: Goldfinch currently has two ERC-20 native tokens, GFI and FIDU.

GFI is Goldfinch’s core native token, used for governance voting, auditor staking, auditor voting rewards, community grants, supporter staking, protocol rewards, and deposits into the membership vault to earn member rewards, supporting protocol development.

FIDU represents LP deposits in the Senior Pool. When LPs provide funds to the Senior Pool, they receive an equivalent amount of FIDU. FIDU can be redeemed for USDC within the Goldfinch dApp at a rate based on the Senior Pool’s net asset value, minus a 0.5% withdrawal fee. Over time, the FIDU exchange rate increases as the Senior Pool earns interest.

Protocol Advantages: Mechanism lowers borrowing thresholds, helping users with lower credit ratings access loans. Compared to traditional platforms, Goldfinch offers superior usability, with most processes handled by smart contracts.

Protocol Risks: DeFi adoption is global, but differing national laws may increase operational costs and complications for Goldfinch. Additionally, due to the lack of collateral, the Senior Pool faces default risk.

(2) Centrifuge

Launched in 2017, Centrifuge is one of the earliest RWA-focused DeFi projects and a technology provider behind top protocols like MakerDAO and Aave. Like other lending protocols, Centrifuge is an on-chain credit ecosystem enabling SME owners to pledge assets on-chain and gain liquidity.

Centrifuge allows anyone to launch on-chain credit funds and create secured loan pools. It created Tinlake, an open asset pool based on smart contracts. Borrowers tokenize physical assets via Tinlake. Physical collateral is divided into two token types—DROP and TIN—representing senior fixed-rate and junior floating-rate tranches. Investors choose DROP or TIN based on risk tolerance and return expectations. Currently, Centrifuge charges no fees.

Project Status: On May 23, Centrifuge announced a new Centrifuge App replacing Tinlake. The new app enhances KYC and investment participation speed, automates KYB (Know Your Business) processes, and lays groundwork for multi-chain support. Existing Tinlake pools migrate automatically. Official data shows Centrifuge’s current TVL at $201 million and total financed assets at $397 million.

Token Functionality: CFG is the native token of Centrifuge Chain, used for on-chain governance. CFG holders manage protocol development. CFG also pays transaction fees on Centrifuge Chain.

Project Advantages: 1. Low financing threshold, enabling investors to earn income from real assets. Centrifuge closely mimics traditional enterprise credit processes; 2. Committed to compliance—built on U.S. asset securitization legal frameworks.

Project Risks: Loan delinquency/default risk. According to rwa.xyz, $10,194,481 worth of Centrifuge loans are overdue by more than 90 days.

(3) Clearpool

Clearpool is a DeFi lending protocol offering unsecured loans to institutions. It offers two products: Prime and Permissionless. Clearpool Prime is restricted to whitelisted institutions and requires no collateral. Borrowers create pools with specific terms in core smart contracts. Once created, borrowers can invite other whitelisted institutions to fund the pool. Loan assets transfer directly to the borrower’s wallet without custody by Clearpool. Clearpool Permissionless requires borrowers to be whitelisted, but lenders face no restrictions.

Protocol Revenue: Clearpool takes 5% of all interest payments as protocol fees.

Protocol Status: Cumulative loans issued: $398 million. Current outstanding balance: $16.58 million. Permissionless TVL: $20.78 million.

Token Functionality: CPOOL is Clearpool’s utility and governance token. CPOOL holders vote on new borrower whitelist additions.

Protocol Advantages: Fully uncollateralized lending executed purely through the protocol, greatly improving efficiency.

Join TechFlow official community to stay tuned Telegram:https://t.me/TechFlowDaily X (Twitter):https://x.com/TechFlowPost X (Twitter) EN:https://x.com/BlockFlow_News