Cryptocurrency Market Making Report: How Founders Can Choose the Right Market Maker?

TechFlow Selected TechFlow Selected

Cryptocurrency Market Making Report: How Founders Can Choose the Right Market Maker?

This report reveals the current state of cryptocurrency market making and provides founders with practical insights for working with market makers (MMs).

Author: Paperclip Partners

Translation: Block unicorn

The opacity and complexity of market making in the cryptocurrency market can be daunting. Nevertheless, ensuring liquidity is crucial for the growth and stability of token economies.

This report reveals the current state of crypto market making and offers founders practical insights into working with market makers (MMs). Key considerations include assessing whether your project needs a market maker, criteria for selecting one, and contract negotiations.

Our research findings are supported by real project agreements and experts in quantitative finance and market making.

Market Making 101

Market making involves an institution or trader simultaneously quoting bid (buy) and ask (sell) prices for a security or asset to provide market liquidity. The bid price represents the highest amount a buyer is willing to pay for a security, while the ask price represents the lowest amount a seller is willing to accept for the same security. The difference between the bid and ask prices is known as the spread, which represents the profit margin for the market maker.

Market makers generally have an incentive to maintain tight spreads and supply liquidity because doing so attracts more buyers and sellers, leading to increased trading volume. In turn, higher trading volume increases the market maker’s profits.

Liquidity refers to how easily an asset can be bought or sold without affecting its price. Highly liquid markets have many buyers and sellers, so there is always someone willing to trade an asset. Conversely, illiquid markets have fewer participants, potentially causing significant price swings when large trades occur.

Great—now that we understand what market makers are, what's the issue?

The problem lies in the misalignment between the market maker’s goal of short-term profit and the project team’s objective of long-term value creation. Our aim is to help founders build synergistic relationships with market makers and avoid structuring deals that allow market makers to benefit at the expense of the project’s long-term goals.

Do You Need a Market Maker?

Founders should first consider two questions:

1. Does my project need a market maker at this stage?

Market makers are typically needed during early listing phases—for example, during an initial exchange offering (IEO)—when initial trading volume is near zero. Established digital assets usually have sufficient organic liquidity, reducing the added value of a market maker.

2. What benefits does partnering with a market maker bring to my project?

In other words: does my protocol require liquidity? For a high-volume decentralized finance (DeFi) protocol, liquidity may be critical. In contrast, for a low-turnover governance token designed for holding, liquidity is less essential.

In the latter case, a simple 50/50 Uniswap pool or another decentralized liquidity pool might suffice. Setting up a liquidity pool can be a straightforward self-service solution and requires significantly less capital than hiring a market maker charging recurring fees. Once the protocol reaches a certain scale (e.g., hundreds of thousands or millions of daily active users), the project can list on centralized exchanges such as Binance, Huobi, or Crypto.com.

Weighing Pros and Cons

When conducting a cost-benefit analysis, founders should consider their specific circumstances, including financial status, project timeline, and token utility:

Benefits

1. Tighter Spreads: Narrow bid-ask spreads make trading more attractive by lowering transaction costs for both buyers and sellers. Tight spreads ensure minimal fees and slippage, improving the trading experience.

2. Liquidity Begets Liquidity: Initial liquidity encourages further liquidity, attracting more buyers and sellers (“liquidity breeds liquidity”), creating a virtuous cycle that amplifies trading volume and depth.

3. Price Discovery: Liquid markets support accurate price discovery, reflecting the true value of an asset based on decisions from numerous market participants.

4. Price Stability: High liquidity reduces sharp price movements caused by large orders, enhancing investor confidence. Ideally, users should price tokens based on intrinsic utility and value rather than purely speculative behavior (which often occurs during periods of high volatility).

Costs

1. Engagement Fees: Market makers may charge setup fees, recurring fees, or token loans. For instance, GSR, a leading crypto market maker, charges $100,000 as a setup fee, $20,000 monthly, plus a $1 million loan in Bitcoin and Ethereum.

(Block unicorn note: Setup fees are typically one-time payments made to the market maker before services begin. These may cover strategy configuration, system setup, and preparatory work required to initiate market making.)

Recurring fees refer to periodic payments (e.g., monthly or annually) made during the service period. These cover ongoing operational costs such as monitoring, managing strategies, and maintaining liquidity. These fees are typically fixed and unrelated to the actual trading volume executed by the market maker.)

2. Imbalanced Negotiations: Founders or token issuers often hold weaker bargaining power due to low trading activity (less profitable for market makers). In such cases, market makers may exploit this imbalance to impose unfavorable terms.

3. Bad Actors: The lack of regulation in the crypto industry may attract fraudulent market makers engaging in wash trading or misusing token loans. Risks associated with misconduct or default by a market maker must be considered.

Criteria for Selecting a Market Maker

Currently, there are over 50 major market makers in the crypto/Web3 space. When choosing a market maker, we recommend evaluating the following five key criteria:

1. Fees: Total sum of setup fees, recurring fees, performance-based fees, and options.

2. Capacity (Volume and Spread): Initial quote size or spread offered by the market maker. Some may only guarantee quotes during certain hours, while others operate 24/7.

3. Reputation: Established firms with strong balance sheets, proven track records (e.g., partnerships with reputable projects, traditional finance experience), and expertise in delta-neutral market making.

4. Accessibility: Criteria set by the market maker when selecting markets (e.g., minimum trading volume thresholds).

5. Relationships: Reliable connections with major exchanges (Binance, Huobi, Crypto.com), which could aid in exchange listings—though these should be approached cautiously and conservatively.

Market Maker Contract Terms

The final step is negotiating and finalizing the contract outlining the terms of the market making agreement, also known as a Liquidity Consulting Agreement (LCA).

By analyzing public and private market making agreements, we identified key contractual elements every founder should focus on.

Compensation

We define compensation as any form of financial incentive designed to reward positive behavior by the market maker. From multiple market making deals, we identify three primary forms of compensation: 1) service fees, 2) options, and 3) KPI-based fees.

Service Fees

Fixed fees paid to the market maker can represent a substantial fiat outlay for early-stage projects. Several pricing structures exist:

1. Setup Fee: A one-time lump-sum payment made to the market maker at the start of the service contract.

2. Retainer Fee: Periodic payments (e.g., monthly, biweekly, quarterly) made to the market maker—usually a fixed rate.

3. Combination of setup and retainer fees (retained market making services).

4. No Fees: In bull markets, market makers may choose not to charge any fees, especially for popular tokens. Supply and demand dynamics determine overall market making costs; heavily hyped tokens generate enough profit through trading alone, eliminating the need for additional fees.

Founders should be cautious, as market makers typically hold stronger negotiation leverage due to:

Broad Market Access: Market makers can operate across numerous markets, so losing a single project has limited impact on their business.

Limited Profit Potential in Early Projects: For early-stage projects with little existing trading volume or liquidity in their native token, market makers see limited profit opportunities and risks. Since they rely on high-frequency algorithmic trading for profits, low-volume environments (due to illiquidity) are unattractive.

Options

Options are common in market maker agreements, providing financial returns tied to token price appreciation. Typically, this grants the market maker the right to purchase tokens at a pre-agreed strike price after the loan period ends.

Thus, the market maker has an incentive to keep the price above a certain threshold (the option strike price), enabling them to exercise the option, buy tokens at the predetermined strike price, and immediately sell them at the higher market price for substantial profit.

Market makers use options to convince founders to sign agreements, arguing that options align their interests with the token’s success (i.e., price increase). This is especially common in bull markets, where early project tokens could grow 100x, making market makers eager—and often successful—in securing option deals.

However, these options become worthless upon expiration, meaning alignment is always short-term.

Using options as compensation for market makers is complex and risky for several reasons:

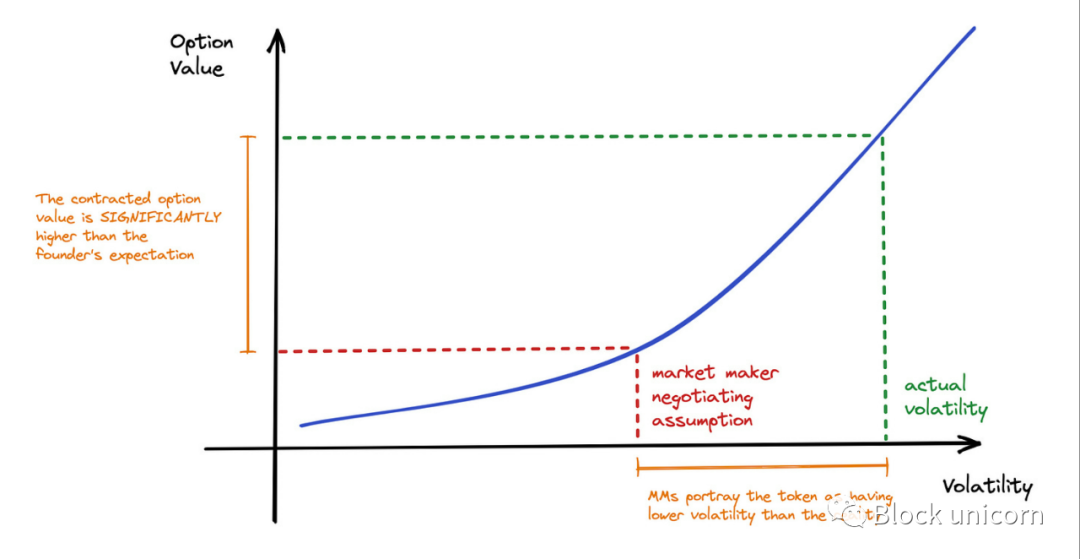

1. Pricing Challenges: Determining a fair strike price, term, or volatility for a new asset is extremely difficult and prone to significant inaccuracies. In bull markets, market makers aim to negotiate large option packages at low prices, effectively gaining equity-like upside similar to venture capital.

2. Manipulation Risk: Founders with limited financial/statistical knowledge may fall victim to manipulation of key option valuation parameters. They might not even realize the options they’re granting carry embedded value—similar to the difficulty of valuing startup equity.

——Unethical market makers can underestimate the true value of options by using unrealistic assumptions in calculations, causing founders to unknowingly give away more value. This can be done by applying unreasonable assumptions (e.g., assuming the token’s volatility equals Bitcoin’s), making the stated option value in the contract significantly lower than reality.

Important Note: While token founders don’t need to master advanced statistics or option pricing theory, tools exist to roughly estimate the value of token options in contracts. It’s hard to precisely determine your option deal’s worth, but founders should understand the implied value to engage in more transparent and informed discussions with market makers.

Various tools and methods can estimate option value, such as calculators or simulators based on option pricing models. Founders can use these to generate approximate valuation ranges and better understand the value at stake. However, these estimates are illustrative—actual option values depend on multiple factors including market conditions, project development, and the market maker’s incentives.

Founders should strive to understand the value of their option deals and approach discussions with greater transparency and awareness. This helps protect long-term project interests and ensures agreements with market makers are relatively fair and beneficial.

We’ve created a basic tool to assist in estimating and valuing option contracts: Paperclip Option Pricing Tool

Potential for Price Manipulation:

1. If the option strike price is too high, it incentivizes the market maker to push the price upward.

2. If the option strike price is too low, the market maker (if the loan repayment is denominated in token quantity) could maximize profits by shorting the token and ultimately repaying only a fraction of the principal.

One variation of option pricing uses “tranches,” where the token issuer provides several option tranches with different strike prices or expiration dates. For example, GenesysGo, under contract with Alameda, offered three tranches priced at $1.88, $1.95, and $2.05 per option.

Interestingly, tranches have little real impact on actual service delivery. Yet they exist for two reasons: a) market makers want to make deals appear more complex and thus “legitimate”; b) they may offer slightly better terms compared to competitors.

Performance-Based Fees

Key Performance Indicators (KPIs) can be used to create performance-based fees that reward market makers for achieving project-defined goals. Below are some metrics (along with our assessment):

1. Trading Volume

Volume is highly risky as a metric because it may incentivize wash trading. This practice is illegal in most jurisdictions and distorts market data by artificially inflating volume figures.

2. Price

Not ideal as a metric, as it may encourage market makers to inflate the token price, risking ecosystem collapse when prices eventually correct.

3. Spread

a. The spread, or bid-ask spread, is the difference between the quoted immediate sell and buy prices. In other words, it’s the gap between the highest price a buyer is willing to pay and the lowest price a seller will accept.

b. Generally, this is a relatively reliable KPI, though it should be supplemented with measures of market depth (otherwise, tight spreads may still result in price fragility).

4. Minimum Bid and Ask Size (in USD)

a. Refers to the dollar value (in project token terms) the market maker commits to buying and selling.

b. This is an important KPI, ensuring a reasonable buffer against large orders that could cause dramatic price swings, preventing sudden spikes or crashes.

Comparing Compensation Models

Deciding which compensation model to adopt in a project is highly personalized and depends on the founder’s available capital, decentralization and governance goals, and the project’s stage.

Visualization of compensation mechanisms: Measured by “certainty” or “average cost,” fees generally offer higher certainty (in USD value) compared to options, though fees can vary significantly depending on market conditions. However, in bull markets, if the underlying token price surges, call options can rapidly appreciate to extremely high values.

Service fees (including setup and monthly retainers) represent a balanced arrangement but may require high upfront payments to secure liquidity support from top-tier market makers (MMs). However, setting vague targets with these fees is suboptimal. Combining performance-based fees with specific objectives—such as percentage spread—better aligns market maker behavior with project goals. Still, care must be taken during negotiations to avoid manipulable KPIs like trading volume.

——We recommend risk-averse teams combine service fees with KPI-based bonuses. Capital-constrained projects should seek proven, trustworthy mid-sized or small market makers. Well-funded projects should contract with top-tier MMs and negotiate primarily on fixed-fee terms.

Compensating via options may lead to overpayment and increased risk. Another negative outcome relates to governance: if founders issue large volumes of options at low strike prices to market makers, those market makers could accumulate significant circulating supply. This undermines protocol decentralization, especially since market makers tend to vote to maximize profits rather than align with the project’s vision.

——For capital-constrained but high-risk-tolerance teams, using a limited number of options in the compensation package may be acceptable—but the present value of those options must be carefully assessed. However, if a project has substantial cash reserves and a loyal user base, using options is generally not recommended and requires thorough scenario testing to avoid overcompensation.

Below is a summary of the above:

A framework for understanding the risks in market maker deals: As a founder, consider what the market maker stands to gain or lose if your token price increases 10x—or drops to zero.

Assuming market makers will always act to maximize profit, teams should understand the market maker’s incentives regarding price movement. Ideally, market makers should be price-agnostic, focused solely on providing liquidity.

Loan Terms

A common structure in market making agreements is for the asset issuer or liquidity requester to provide a loan to the market maker for use in trading and supplying liquidity. Several aspects of loan terms are significant:

1. Loan Term: The duration matters, as it determines how long the project must wait before the market maker returns the capital. This should be negotiated on a case-by-case basis according to the project roadmap and core team’s financial needs.

2. Interest Rate: These token loans are typically offered at 0% interest because market makers earn variable returns through trading. Charging fixed interest would make the arrangement unattractive.

3. Token Loan Amount and Value: Alignment is stronger when the loan uses the ecosystem’s native token. However, token-denominated loans create adverse incentives—if the token price falls, the market maker benefits because the repayment value decreases. Such contract terms resemble an “embedded option,” giving the market maker substantial downside potential before maturity.

4. Repayment Issues: The issuer should clearly define contractual obligations if the market maker fails to return tokens. Contracts often include clauses allowing repayment in BTC/ETH or stablecoins for any outstanding balance.

Termination Rights

1. Notice Period

Typically, either party can terminate the agreement with written notice within a specified period. As with many commercial agreements, termination notice periods usually range from 14 to 30 days. However, each issuer should assess how easily they can onboard an alternative market maker and adjust the notice period accordingly. Other termination conditions:

2. Asset Issuer

a. Right to terminate in case of material breach of obligations.

-

Market Maker: The market maker holds more critical termination rights, as they determine the conditions under which liquidity provision ceases. We outline four possible termination scenarios, along with key considerations for the core team (where applicable).

1. Breach of Payment Terms: The issuer should ensure safeguards such as grace periods to buffer the team during financial hardship.

2. Breach of Other Terms (e.g., confidentiality).

3. Conflict with exchange rules where liquidity is provided.

4. Legal and Regulatory Changes: Given the evolving regulatory landscape in crypto, market makers need protection if fulfilling their obligations suddenly becomes a criminal act. One source for potential legal due diligence is understanding how market making is regulated in traditional asset markets, which may set precedents for future Web3 regulation.

Liability

In most liquidity agreements with market makers, the market maker is typically exempt from liability related to token price fluctuations. This is expected, given the speculative nature of cryptocurrencies. Moreover, countless factors beyond the market maker’s control influence token prices, making it fundamentally unreasonable to hold them financially accountable for such volatility.

Conclusion

In summary, market making plays a vital role in ensuring liquidity and stability in cryptocurrency markets. This report aims to demystify the complexities of crypto market making and provide actionable insights for founders considering collaboration with market makers. Through analysis of real contracts and expert industry input, the report emphasizes the importance of evaluating the need for market makers, selecting suitable partners, and negotiating favorable terms.

We hope this report serves as a valuable resource for founders and stakeholders in the crypto ecosystem, helping them make informed decisions about market making and supporting the growth and stability of token economies.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News