How to value a DAO token?

TechFlow Selected TechFlow Selected

How to value a DAO token?

This article focuses on the valuation of DAO tokens and various token-specific factors that may be considered in the valuation process.

Author: Kristof Lommers

Compiled by: TechFlow

In this article, we discuss a valuation framework for decentralized autonomous organizations (DAOs). While building upon concepts from corporate finance, we introduce native DAO valuation concepts.

*Note: The proposed DAO valuation framework is preliminary, as we are only beginning to understand the specificities of DAOs and how market participants value them.

Valuing DAO tokens represents a distinct framework compared to valuing the development companies behind DAOs. This valuation framework enables communities to assess DAO performance in creating value for token stakeholders and promotes greater accountability for the development teams behind DAOs.

This article focuses on the valuation of DAO tokens and various token-specific factors that may be considered during valuation.

DAO Token Valuation

First, we need to properly define what we are pricing. In this article, we view DAOs as organizations operating autonomously on smart contracts and governed by stakeholder communities. Many protocols adopt a dual company-DAO structure, where a company acts as the developer and operator of the underlying protocol. The company behind the protocol is often established before the DAO and retains ownership of relevant intellectual property and assets. For example, Uniswap can be viewed as a DAO with a governance token (UNI), while development is handled by Uniswap Labs.

Web3 leverages tokenomics to align equity and token incentives, enabling appropriate decentralization. Tokens are also used as part of the solution to the cold-start problem, where token incentives reward users for desired behaviors. Fundamentally, token value is derived from community membership, utility within the ecosystem, and associated governance rights. Value created by DAOs is typically not distributed directly among token holders but rather used to provide utility and enable governance participation.

Without addressing the unresolved securities classification issue, DAOs have generally been cautious about directly distributing value to token holders, as this could lead to tokens being classified as securities.

Value created by DAOs can flow indirectly to token holders through various channels. For instance, one might value staking benefits, community perks, membership privileges, and overall growth of the DAO (or its components). Depending on the case, some protocols may also directly distribute value to token holders.

Valuation Approaches

There is no universal valuation method, as DAOs encompass diverse models. For example, Hennekes (2022) categorizes DAOs into eight types: protocol DAOs, grant DAOs, charity DAOs, social DAOs, collector DAOs, venture DAOs, media DAOs, and sub-DAOs.

Friend With Benefits DAO represents a community-driven effort where much of its value stems from social capital, whereas Orange DAO functions as a collective venture investment vehicle.

Therefore, each DAO requires a tailored valuation approach, with different factors carrying varying importance depending on the DAO type.

Nevertheless, we can offer a general valuation framework that, with appropriate adjustments, broadly applies across different DAOs.

We believe DAO token valuation primarily involves fundamental valuation or comparable analysis.

-

In fundamental valuation, one attempts to evaluate DAO tokens based on fundamentals related to token utility and expected token value.

-

In comparable analysis, one seeks to compare DAO tokens using various metrics.

As the names suggest, fundamental valuation aligns more closely with attempting to price tokens based on intrinsic fundamentals, whereas comparable analysis represents a more market-oriented valuation approach.

Fundamental Valuation Model

One can conceptualize the fundamental valuation model for DAO tokens as follows:

Valuation is both an art and a science, requiring judgmental estimates and assumptions for many subcomponents.

A) Discount Rate

The discount rate can be estimated using the weighted average cost of capital (WACC), calculated as the weighted average of its sources of financing. These sources may include debt or equity (tokens). WACC is computed as follows:

Where D represents the value of debt in the DAO, and T represents the total value of the DAO's tokens.

For the cost of debt, one should take the value-weighted average of interest rates charged on debt. However, in most cases, DAOs have no leverage in their capital structure, meaning WACC essentially equals the cost of token capital.

We can estimate the cost of token capital by calculating expected returns within a DAO-native factor model framework. Literature (e.g., Liu and Tsyvinski, 2021) suggests that the cryptocurrency market is an independent asset class with limited correlation to other macro asset classes, though correlations with equities—particularly tech stocks—are relatively strong and increasing. This is especially relevant for DAO tokens, which can be seen as representing stakes in Web3 organizations.

While concepts from equity asset pricing can be borrowed, given the unique nature of this asset class, a DAO-native modeling approach is necessary. Factor models are widely used in equity markets to estimate expected returns and discount rates.

Prior research indicates that a three-factor model captures a significant portion of systematic returns in cryptocurrencies. Principal component analysis from Botte and Nigro (2021) shows the first three factors account for approximately 70% of co-movement, consistent with the three-factor model in equities.

We observe that the cryptocurrency market has evolved from one where token returns were highly correlated with Bitcoin to one where tokens increasingly decouple from Bitcoin. Thus, there is greater idiosyncratic risk-return within the crypto market, and DAO tokens may exhibit higher correlation with the broader DAO token market and lower correlation with the overall crypto market over medium to long horizons.

For traded DAO tokens with sufficient history, factor models can be used to estimate expected returns. For non-traded tokens (or those with insufficient data), one can use a set of comparable DAO tokens and adjust for relevant factors such as size and illiquidity.

Factor models are constructed in two steps:first, constructing factor returns; second, regressing DAO token returns against these factors. Factor returns are estimated as returns of long-short portfolios, rebalanced monthly and value-weighted.

However, Jiasun Li and Guanxi Yi (2020) find that long-side factors carry greater significance in cryptocurrencies. This may be due to the relatively high cost of shorting in crypto, resulting in less downward pressure.

A standard practice in factor research is to use value-weighted portfolios, yet in crypto, certain tokens dominate in market cap, skewing value-weighted portfolios toward a few large tokens.Therefore, we recommend using a log-value weighting scheme to acknowledge top tokens’ market caps without overly concentrating the portfolio on a few selected tokens. Additionally, factors should be estimated on datasets free of survivorship bias and including failed DAO projects.

We propose using DAO market, ecosystem, size, value, liquidity, and momentum as factors in a DAO factor model—a traditional five-factor model supplemented with a blockchain ecosystem factor.

-

The market factor reflects broad cryptocurrency market risk and is calculated as the average return across the universe of DAO tokens.

-

The ecosystem factor reflects systemic correlation with Layer-1 ecosystem tokens (e.g., Ethereum, Solana, Avalanche). A DAO token’s existence is fundamentally tied to its host ecosystem. For example, Ethereum-based DAOs rely on the Ethereum network to execute smart contracts and typically issue ERC-20 tokens.

-

The size factor reflects size-related risk, computed as the return of a portfolio going long small-cap DAO tokens and short large-cap ones. The traditional value factor is difficult to define for DAOs. One could construct a value factor using some of the metrics discussed in the comparables section, as they represent value measures based on financial and business variables.

-

The liquidity factor reflects liquidity risk, typically calculated as the return of a portfolio long low-liquidity DAO tokens and short high-liquidity ones. Various liquidity measures can be used, such as trading volume, bid-ask spread, or Amihud illiquidity measure.

-

The momentum factor reflects momentum or trend risk, calculated as the return of a portfolio long top-performing DAO tokens and short bottom performers.

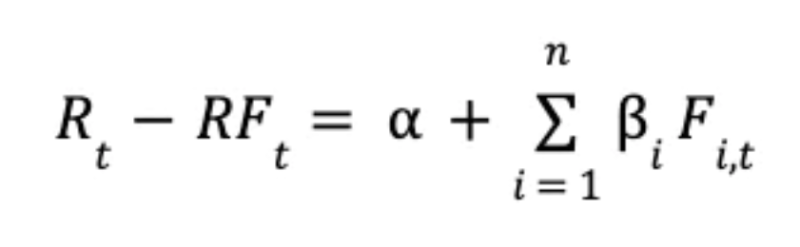

Finally, the regression of DAO token returns on factor returns is defined by the following equation:

Where Rt denotes the return of the DAO token, RFt denotes the risk-free rate or funding rate return, α represents the DAO token’s alpha return, βi represents the DAO token’s exposure to factor i, and Fi,t denotes the return of factor i.

The “risk-free” funding rate reflects liquidity costs. For example, within the Ethereum ecosystem, liquidity is managed via ETH, where staking yields on ETH can be considered the base funding rate. The estimated beta coefficients can then be used to calculate appropriate expected returns and discount rates.

B) Valuation of Future Token Flows

One of the most prevalent fundamental valuation models is the discounted cash flow (DCF) model, which values an entity based on discounted future (free) cash flows. Using a similar logic, one can consider discounting token flows, calculating the DAO’s free cash flow. The DCF model relies on three main components: cash flows, discount rate, and assumptions about future expected cash flow growth. In the case of DAOs, we can introduce the term Free Token Flow (FTF), representing actual token liquidity generated by the DAO, calculable using net income, asset depreciation, changes in working token liquidity, and system token expenditures. More specifically, free token flow can be calculated as:

Net income, asset depreciation, working capital liquidity, and capital expenditures can be defined according to traditional accounting and corporate finance conventions.

*Note: The field of DAO accounting is still nascent—see Lommers, Ghanchi, Ngo, Song, and Xu (2022), who discuss DAO accounting and suggest various methodological adjustments based on crypto accounting and DAO specifics.

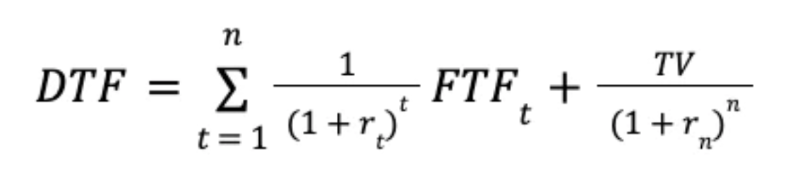

The discounted token flow (DTF) can be calculated as:

Where FTFt represents the free token flow in year t, rt represents the discount rate in year t, and TV represents the terminal value.

One might also assume the DAO will grow alongside its target market segment and use that growth rate to project future free token flows.

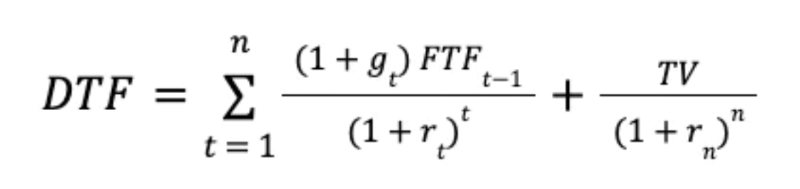

A recent McKinsey report (2016) advocates using discounted cash flow models to value tech startups. They recommend analyzing the expected long-term development of the startup’s target market segment and working backward from there. The DTF calculation becomes:

Where FTFt represents the free token flow in year t, rt represents the discount rate in year t, gt represents the growth rate in year t, and TV represents the terminal value. A key assumption in the model is the future growth rate, which can be addressed via scenario analysis (e.g., sustained growth, halved growth, doubled growth, etc.).

Such token flows can accrue directly or indirectly to token holders—for example, through buyback and burn mechanisms, direct distributions, and other value-enhancing activities.

C) Value of DAO Benefits

Token ownership in a DAO can confer various benefits, including community membership, certain membership rights, and governance rights. There is no one-size-fits-all approach in DAOs—different DAOs offer varying benefits through the range of options currently enabled. Agarwal (2021) argues that communities themselves are valuable, enabling community-based collaborative initiatives, shared resource utilization, knowledge and skill sharing, and more.

Governance rights are another common benefit of holding DAO tokens, reflecting the degree of community involvement in decision-making. To measure governance quality, Regner (2022) proposes various metrics such as number of proposals, proposal thresholds, proposal acceptance rates, and voting participation. Recently, there has been debate within the community on whether governance rights impact token value—Buterin (2022) argues they should not.

We believe governance rights' value depends on context: whether value is distributed to token holders, the extent of community involvement in DAO operations, and so on.

DAO benefits may vary based on token holdings. For example, Mnema DAO tiers its benefits based on token ownership, with top-tier benefits significantly exceeding those at the lowest tier.Large token holders enjoy strategic advantages in governance, akin to control premiums in traditional corporate finance.Each token holder may value DAO benefits differently, introducing discretion into the valuation process.

One could attempt to estimate an approximate average value of provided benefits, which could serve as a direction for future research.

The discounted value of benefits (DVB) can be calculated as:

Where DBt represents the value of DAO benefits in year t, rt represents the discount rate in year t, and TV represents the terminal value of DAO benefits after year t.

We can also assume DAO benefits grow alongside the market segment and use that growth rate to estimate future benefits. In this case, the DVB calculation becomes:

Where DBt denotes the benefit value in year t, rt denotes the discount rate in year t, gt denotes the growth rate in year t, and TV denotes the terminal value of benefits. A key model assumption remains the future growth rate, addressable through scenario analysis (e.g., sustained, halved, or doubled growth).

D) Expected Staking Rewards

Most Web3 projects with native tokens allow token holders to participate in blockchain consensus, tokenomic incentives, or protocol development, earning token rewards in return (Cong, He, and Tang, 2022).

From a financial perspective, this can be viewed as generating passive income by locking up capital for a period. Therefore, one can calculate the present value of expected staking rewards using an appropriate discount rate. As previously noted, ETH staking yield can be considered the liquidity cost in the Ethereum ecosystem. Thus, the liquidity cost for tokens within the Ethereum ecosystem can be viewed as equal to the ETH staking yield plus a risk premium.

The cost of staking primarily includes loss of flexibility, as tokens are locked for a period—exposing holders to native token price volatility, project failure, and potential platform hacks (Royal, 2022). It should be noted that in early stages, staking yields may be relatively high to incentivize early users. In such cases, staking yields may significantly exceed risk-adjusted liquidity costs.

Comparables

Assuming DAO token value is linked to the value of the DAO itself, we can use comparables based on various relevant metrics to assess the DAO entity. Comparable analysis uses ratios or metrics to derive valuation estimates. More importantly, it relies on valuations of similar competitors, making it a more market-consistent valuation method. Comparable analysis leverages basic accounting and business information to compute key metrics related to profitability, financial health, user engagement, and more. We argue that DAO-native metrics must be developed to evaluate organizations under this new paradigm.

Comparable DAOs can be defined by category and scale:

-

If no directly comparable DAO exists in the right category and scale, identify the closest match.

-

If comparable DAOs exist within the same category but differ significantly in scale, estimate a size adjustment. For example, calculate the average valuation difference between large and small DAOs within the category and apply it as a correction. Where possible, consider multiple competitors to derive a valuation range.

Standard comparables include metrics such as revenue, profit, EBITDA, and margins. Numerous popular metrics are used for Web2 companies, including monthly unique visitors, bounce rate, average order value, active users, conversion rate, churn rate, cost per visitor, and viral coefficient (Corporate Finance Institute, 2022). These metrics allow comparison across companies and relative valuation. To build meaningful comparables, DAOs must be differentiated from traditional (Web2) tech companies.

As Hsu (2022) argues, Web2 valuation tends to focus on customer acquisition and user activity. We contend that relevant factors in DAOs (and Web3 broadly) include degree of decentralization, community engagement, protocol users, protocol development activity, integration with other protocols, blockchain ecosystem metrics, and protocol revenue.

Thus, we propose the following metrics for Web3 valuation: unique protocol users and token holders, protocol fees collected, token holder participation in governance, protocol transaction volume, token trading volume and velocity, community interactions (e.g., Discord), treasury spending and growth, protocol ecosystem expansion, cost of user acquisition via token incentives (e.g., vampire attacks), and user net present value (value received in tokens minus value provided), among others.

Comparable valuation is best conducted by examining different metrics, which may vary by DAO type.

-

For example, DeFi protocol DAOs require different metrics than social DAOs. Total Value Locked (TVL) is widely regarded as a core metric when analyzing DeFi protocols.

-

For example, Maker DAO (2021) proposed metrics including total outstanding risk assets, interest income correlation, net interest income, total outstanding DAI, DAI market share, on-chain DAI transaction volume, gross interest income, and number of active vaults.

One can compare DAOs across multiple dimensions of overvaluation/undervaluation and take a weighted average based on the relative importance of each dimension.

Additional Token-Specific Considerations in Valuation

Since token prices result from the balance of demand and supply, considering token supply is also important.

- Sustainable and sound tokenomics form part of the token valuation process. Protocol tokenomics should be structured to promote and optimally incentivize the creation of productive value.

-

Given that most circulating cryptocurrencies represent utility tokens, one might argue that token value should reflect the utility of holding the token and mirror the utility provided by the protocol ecosystem. Fundamentally, a sustainable tokenomic design fosters a tighter linkage between token value and ecosystem utility.

-

When comparing DAO tokens, future token supply should be adjusted for proper apples-to-apples comparison. For example, an "open" token supply introduces more uncertainty into future valuations compared to a fixed supply.

-

Token velocity must be considered when valuing tokens. (Samani, 2017) Ecosystem growth does not necessarily imply price appreciation, as high-velocity tokens—with little incentive to hold—experience less price uplift. Samani (2017) suggests methods to reduce velocity, such as introducing profit-sharing mechanisms, staking features, balancing burn and mint mechanisms, and gamification to encourage holding.

-

Most DAO tokens are listed on decentralized exchanges. Listing on centralized exchanges can be lengthy and costly. Especially for non-blue-chip tokens, liquidity may be thin, and trading can have significant price impact. This creates substantial risk of price volatility driven by abnormal trading activity. For example, if a large holder sells their position, it could significantly depress the token price. Relatedly, token distribution—particularly whale holdings—can pose major risks. However, one should abstract from tokens held in protocol treasuries or exchange pool contracts, as these are often stickier or pooled for specific purposes (e.g., market making).

-

Early investors and development teams often have vesting schedules preventing immediate token sales. Vesting schedules consistently signal potential price movements, as investors tend to take profits upon unlock. Therefore, valuation should account for vesting timelines, which may exert significant downward price pressure in the short term.

-

Liquidity within the treasury is important. As Regner (2022) notes, DAOs often hold large amounts of their own tokens in treasuries. Treasury operations require liquidity. Without other liquid assets, the treasury may need to sell its own tokens, creating downward price pressure. Particularly for small- and mid-cap DAO tokens with relatively thin liquidity, treasury sales can significantly impact price.

-

Providing value and engaging with the token holder community is also crucial. Many leading projects with utility or governance tokens perform poorly because they fail to deliver meaningful value to token holders. This ties back to the broader discussion about misaligned incentives between DAOs and enterprises.

As previously mentioned, in many protocols, the company behind the protocol is often established before the DAO and retains ownership of key intellectual property and assets. The protocol may experience strong growth, and the company behind it may see sharp valuation increases, while the token stagnates. This can create significant misalignment between the owners of the company (i.e., developers and investors) and token holders. However, as Walden (a16z) argues, protocols can gradually decentralize—starting centralized and progressively transferring control (including IP) to the DAO—a factor that should be considered in valuation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News