Messari: Review and Analysis of Avalanche's Performance in Q3 2022

TechFlow Selected TechFlow Selected

Messari: Review and Analysis of Avalanche's Performance in Q3 2022

The third quarter was a period of building and executing Avalanche's strategy and vision. Although the quarter lacked the excitement seen during last year's bull market, the network's core user base and its ability to advance its market position have emerged.

Author: James Trautman, Messari Research Analyst

Translation: TechFlow

Introduction to Avalanche

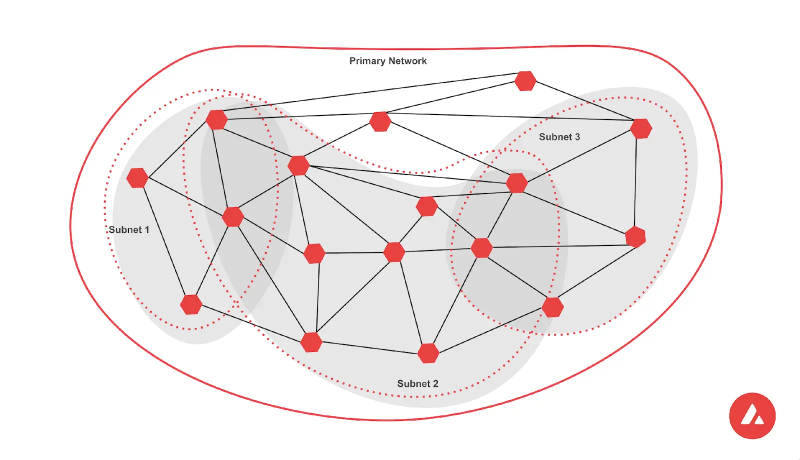

Avalanche is a PoS smart contract platform providing infrastructure for decentralized applications. Avalanche distinguishes itself by creating and implementing a new consensus algorithm called the "Avalanche Consensus." After years of research, Avalanche’s mainnet launched in September 2020, introducing a multi-chain framework consisting of three chains: the P-Chain, X-Chain, and C-Chain. Each chain plays a critical and unique role within the Avalanche ecosystem while collectively operating as a single network, commonly referred to as the Primary Network.

The Avalanche Consensus and Primary Network are designed to support sovereign, interconnected blockchains known as subnets.

Subnets consist of a subset of validators from the Primary Network that run the same Virtual Machine (VM) and operate under their own rules.

Subnets enable different attributes such as reliability, efficiency, and data sovereignty. They provide the ability to create custom blockchains tailored for specific use cases while isolating high-traffic applications from congestion on the Primary Network.

Narrative of the Third Quarter

Despite the overall market downturn in Q2, Avalanche remained focused on realizing its vision of digitizing all assets, enhancing network capabilities, and scaling horizontally through architectural design and subnets. It improved user access with Core, a Web3 operating system.

Its ecosystem continued expanding into DeFi and other areas with the launch of NFT markets like Trader Joe's Joepegs and GameFi developments. This represents a continuation of Avalanche’s ecosystem growth, with the network still prioritizing long-term development.

Performance Analysis

Network and Financial Overview

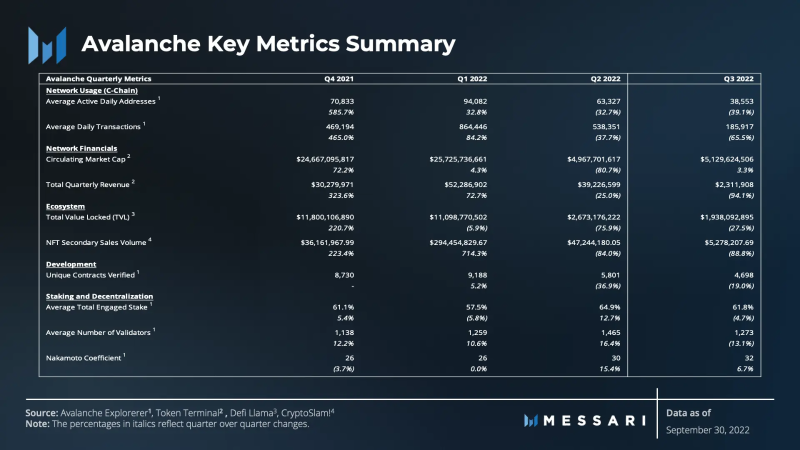

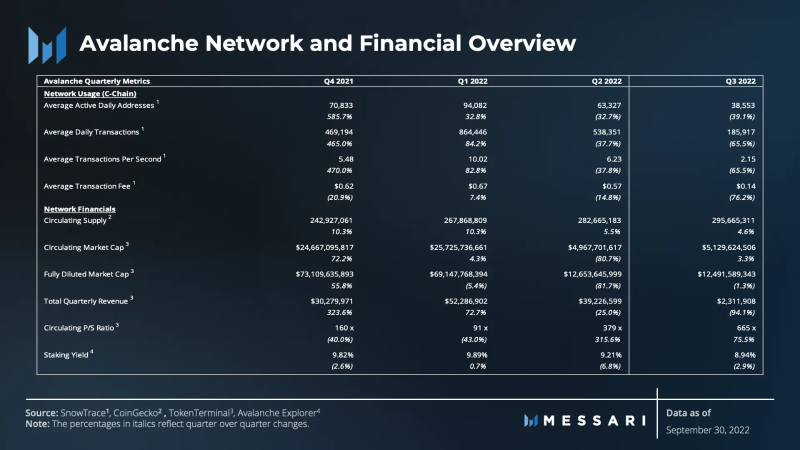

Data used to evaluate the quantitative aspects of the Avalanche network comes from the Primary Network, specifically the Avalanche C-Chain.

Subnet activity is also considered alongside the C-Chain but is not listed in the data tables because each subnet has its own sovereign security, native token, and value accrual mechanism. In contrast, the C-Chain remains the primary driver of AVAX value at present.

Similar to Q2, Avalanche’s C-Chain saw declines in both network usage and financial performance during Q3, except for a slight increase in circulating market cap (i.e., network value).

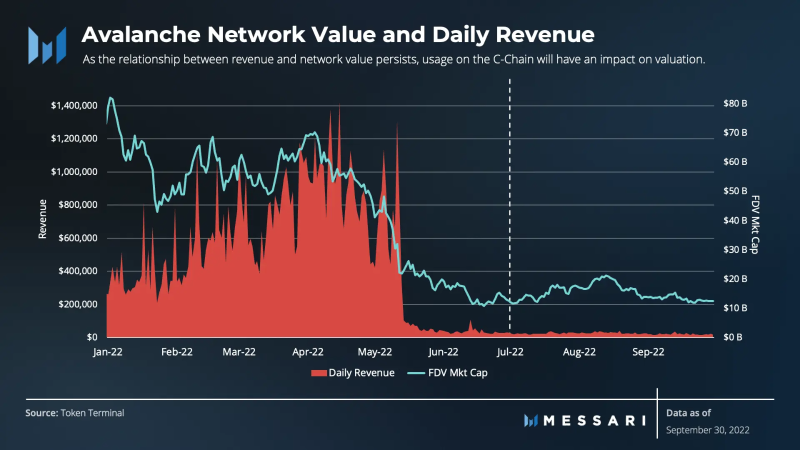

While network value increased slightly (3.3%), usage and revenue generation declined sharply. Daily transaction volume dropped by 65.5%, and total revenue fell by 94.1% as transaction fees declined by 76.2%. From a valuation perspective, the relationship between network value and revenue (price-to-sales ratio) continued to deteriorate, rising from 379x to 665x.

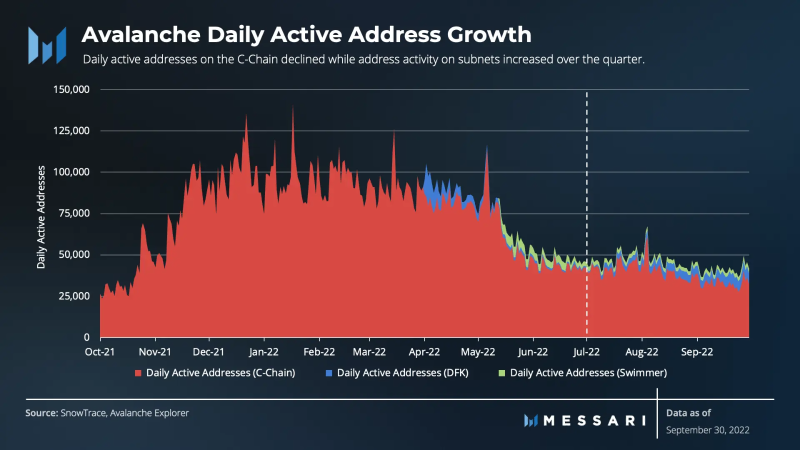

Daily active addresses also continued to decline, averaging 38,000 per day compared to 63,000 in Q2. Outside the C-Chain, however, daily active addresses on the DeFi Kingdoms (DFK) and Crabada (Swimmer) subnets showed an upward trend.

Address activity on DFK and Swimmer subnets reflects prior usage patterns observed on the C-Chain.

Nonetheless, address activity on the C-Chain remains four times higher than it was a year ago. The growing activity on subnets indicates healthy subnet functionality.

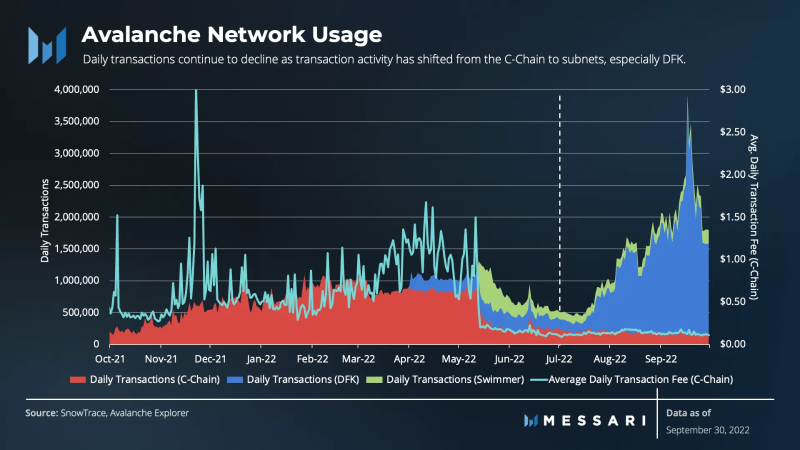

Transaction activity on the C-Chain declined more sharply than daily active address activity. Avalanche’s average daily transactions dropped from 540,000 in the previous quarter to 186,000 in Q3. As transaction activity shifted from the C-Chain to subnets—particularly DFK—daily transaction volume on the C-Chain continued to fall.

Previously, DFK and Crabada were major drivers of transactions and revenue on the C-Chain. Now, these subnets generate an average of 1.5 million transactions per day on their sovereign networks. Overall, during Q3, over 1.7 million transactions occurred daily across Avalanche’s infrastructure, peaking at 45 million transactions in August. However, the shift of transactions from the C-Chain to individual subnets continues to exert downward pressure on Avalanche’s transaction fees (by design) and significant downward pressure on revenue.

Balancing the relationships among security, transaction fees, revenue, and network value has been a constant challenge for Avalanche since inception.

Throughout 2021 and Q1 2022, daily average transaction fees fluctuated as network usage and financial metrics grew. Several Apricot Phase 5 upgrades and Avalanche Go (Apricot Phase 6) implemented during Q3 jointly contributed to lower average transaction fees.

Because subnets generate traffic on their own networks, transaction fees on the Primary Network declined even further. This was intentional and part of Avalanche’s horizontal scalability strategy. However, the result was a corresponding decline in total revenue due to falling transaction fees.

Revenue remains a key focus for many participants in the ecosystem because Avalanche burns all revenue (transaction fees) from the network’s circulating supply. In theory, this increases scarcity and creates value for all AVAX token holders.

Due to the burn mechanism, increases or decreases in C-Chain revenue impact AVAX’s market value upwards or downwards. As demonstrated throughout last year, peaks and troughs in daily revenue coincided with peaks and troughs in fully diluted valuation (FDV). Given the persistent relationship between revenue and network value, C-Chain network usage and revenue will continue to influence network value.

In the short term, subnets clearly exert downward pressure on revenue and some short-term pressure on network value. The ongoing relationship between revenue and value raises a question: do subnets negatively affect the utility of the AVAX token and the value of the Avalanche Primary Network (C-Chain)?

Ways Subnets Accumulate Value

Subnets are not only a method of scaling the entire network—they are also a compelling value proposition for developers.

Subnets allow decentralized applications to leverage the Avalanche consensus and infrastructure, enabling developers to easily launch uniquely customized blockchain environments.

When evaluating the quantifiable metrics of the Primary Network, there are opportunity costs that are difficult to quantify. Would DeFi Kingdoms and Crabada have built on Avalanche and generated activity on the C-Chain without subnets as their ultimate solution?

Perhaps they would have found alternative solutions.

Assuming subnets are the ideal solution for DFK, Crabada, and hundreds of other projects currently being developed on the Fuji Testnet—and assuming the rationale described by game developers like Pulsar for building within subnets is valid—then value accumulation would manifest in validator growth, as each subnet requires staking 2,000 AVAX and validating on the Primary Network.

In other words, without the appeal of subnets, the Primary Network’s infrastructure might lack inherent growth momentum. In that case, the number of validators staking 2,000 AVAX would also be reduced. Thus, the value generated from expanding validator count differs significantly in time horizon from the value generated via revenue and burned transaction fees on the C-Chain.

Other value accumulation mechanisms include fees paid in AVAX for creating new subnets and blockchains, allowing AVAX to indirectly capture value through its burn mechanism.

Additional value may come from subnets’ demand for AVAX liquidity and the use of AVAX as gas for final cross-subnet communication. Finally, subnets can also choose to use AVAX as their native token.

Several strategies to boost C-Chain adoption remain unchanged. Many applications may opt to build entirely on the C-Chain because it better suits their needs.

They could also start building on the C-Chain and later migrate to their own subnet, as DFK and Crabada did.

Ultimately, each option involves trade-offs, giving developers sufficient flexibility at the product or business solution level.

The rollout of subnets may have had short-term impacts on C-Chain network activity and value.

However, as more subnets go live, the Primary Network’s value in terms of scale, flexibility, and robust infrastructure should accumulate over the long term.

Ecosystem and Development Overview

- DeFi

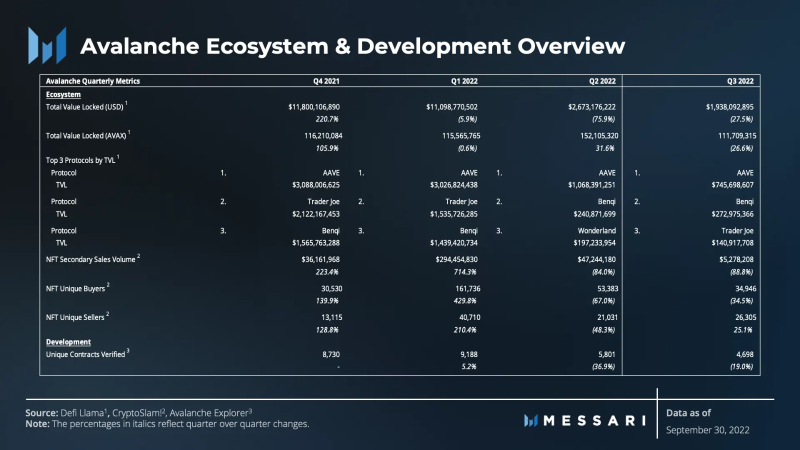

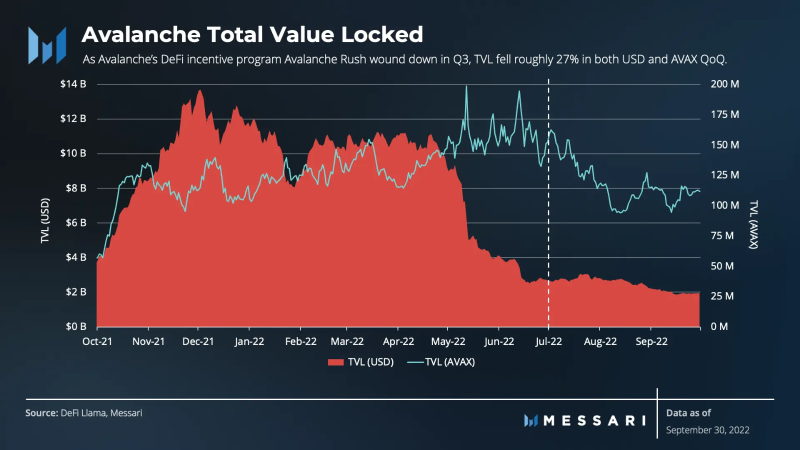

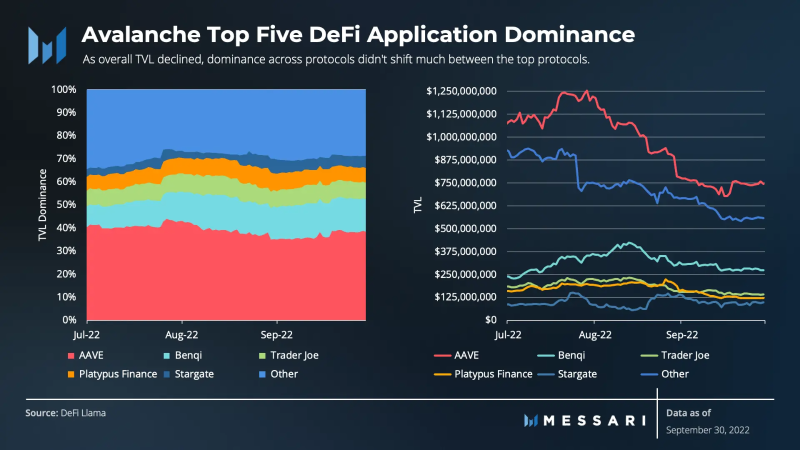

As Avalanche’s DeFi incentive program, Avalanche Rush, concluded in Q3, TVL measured in both USD and AVAX declined by approximately 27% quarter-over-quarter.

However, over the 12-month period of the Avalanche Rush program, the average TVL denominated in AVAX was 126 million, roughly equivalent to Q3’s average level.

From this perspective, AVAX-denominated TVL has remained stable. As TVL reverts to its mean, it reflects sustainable utility rather than value purely catalyzed by incentives.

During Q3, Avalanche’s two most important lending protocols, Aave and Benqi, saw their TVL move in opposite directions.

Aave followed the broader trend of the Avalanche DeFi ecosystem (-30%), while Benqi increased by 13%.

However, Benqi’s growth can be attributed to its recently launched liquid staking product, as TVL on its lending platform remained flat during the quarter.

Despite the overall decline in TVL, dominance among top protocols did not change significantly.

The broader DeFi ecosystem stabilized due to TVL growth from relatively newer projects in the Avalanche ecosystem: Synapse (139%), Stargate (14%), and GMX (6%).

Beyond existing DeFi, Avalanche made deliberate efforts in Q3 to bring in real-world assets (RWA).

Centrifuge, an on-chain ecosystem for structuring RWA credit, announced integration of Centrifuge Connectors with Avalanche.

Centrifuge Connectors is a hybrid cross-chain solution that brings Centrifuge’s real-world assets directly onto Avalanche.

Additionally, Intain (currently managing about $5 billion in assets on Hyperledger) announced it is building an Avalanche subnet to tokenize asset-backed securities (ABS). Intain cited Avalanche’s subnet architecture and its support for permissioned spaces—important for financial institutions—as key reasons for choosing Avalanche.

Finally, global investment leader KKR & Co. announced a partnership with digital asset expert Securitize. They plan to tokenize a portion of KKR’s Healthcare Strategic Growth Fund and offer it on Avalanche’s public blockchain.

- NFTs

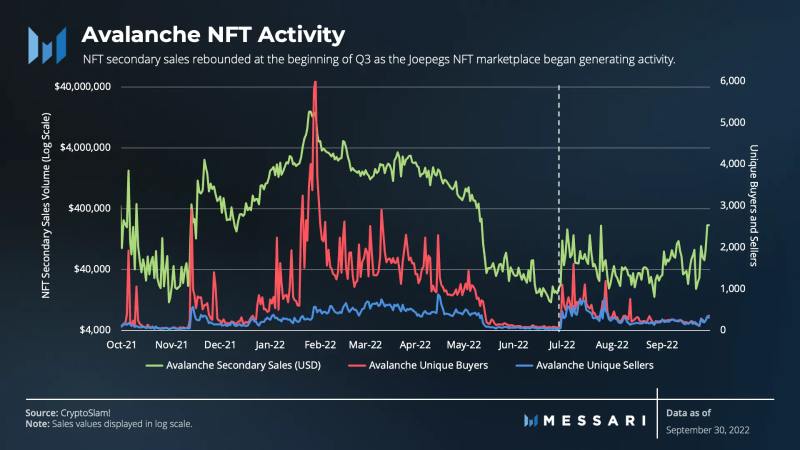

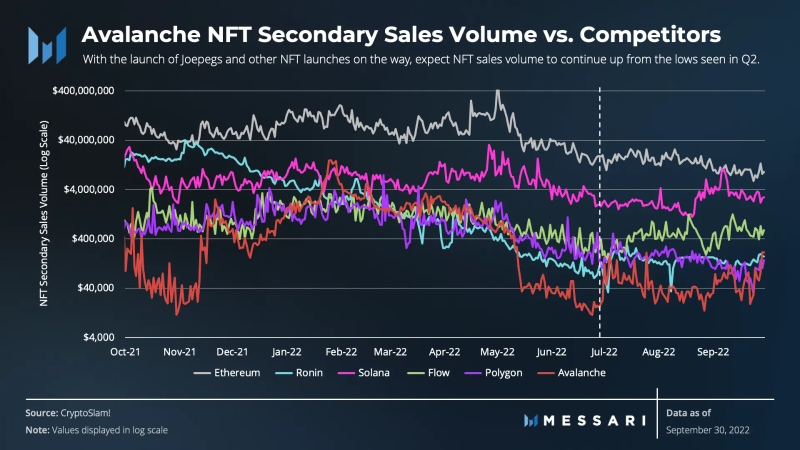

The downturn in TVL is not limited to DeFi. Avalanche’s nascent NFT market experienced declines in secondary sales volume (-88.8%) and unique buyers (-34.5%), while unique sellers increased by 25.1%.

However, notably, NFT sales rebounded at the beginning of Q3. Daily average sales rose from $25,000 in June to $70,000 in July. This represented a 180% increase from the lows at the end of Q2, largely driven by the launch of the Joepegs NFT marketplace in Q2 and the subsequent Conscious Lines sale, which sold out in 30 seconds and attracted interest from buyers like Paris Hilton.

- Gaming

While DeFi incentives may have slowed, Avalanche’s $200+ million ecosystem fund, Blizzard, remains active and continues to attract creators and GameFi projects.

Alongside RWAs, GameFi is clearly finding its place within Avalanche’s ecosystem.

Entering Q3, Razor—a gaming company with a strong player-centric hardware, software, and services ecosystem—announced a collaboration with SHRAPNEL.

SHRAPNEL is a AAA first-person shooter game built on Avalanche, developed by a team with backgrounds from Halo, Call of Duty, and HBO.

Celebrity host Steve Harvey of Family Feud announced his entry into Avalanche’s gaming world, allowing players to earn rewards in NFT form.

Beyond Razor, SHRAPNEL, and Steve Harvey, a series of games including Cosmic Universe (migrating from Harmony), OpenBlox, and Domi Online were also announced.

RWAs and GameFi could drive activity on the C-Chain and expand Primary Network validators via subnets in the coming months.

- Development

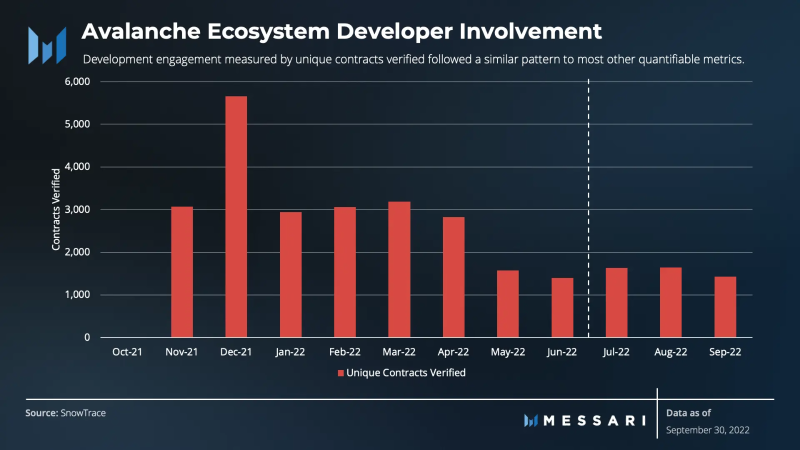

Developer engagement, measured by unique smart contract verifications, has not yet matched the progress seen in RWA and GameFi. Developers trigger smart contract verification to translate code into higher-level languages. This metric followed a similar pattern to most other quantifiable metrics, declining 20% quarter-over-quarter. Additionally, similar to address and transaction activity, smart contract verification has been rising on the DFK and Swimmer networks.

In previous reports, core developer participation was measured by tracking event data sources from Ava Labs’ GitHub repositories.

Data shows core developer involvement has grown over recent quarters, increasing by 33% in Q2 and 34% in Q3. By this measure, the network’s core contributors appear to be making meaningful progress in infrastructure development.

However, current data sources on developer activity are imperfect, employing flawed methodologies to collect core developer activity.

While evidence suggests core developers are contributing to Avalanche infrastructure, future reports aim to assess activity using more reliable data sources and methods to achieve accurate measurements.

Staking and Decentralization Overview

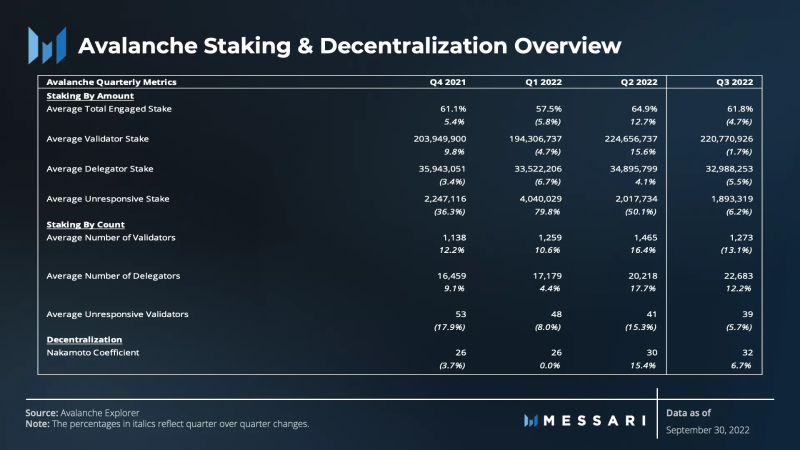

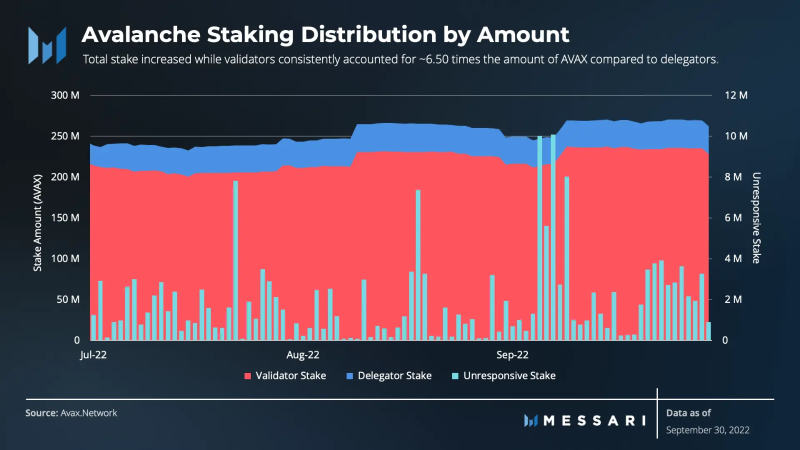

Despite the turbulent Q2, network staking and decentralization remained strong.

While average daily staked amounts and participation levels remained relatively flat quarter-over-quarter, total staked AVAX grew from 243 million to over 260 million. Validator staking remains 6.5 times higher than delegated staking, and inactive validator stake remained stable, indicating sustained participation, reliability, and network health.

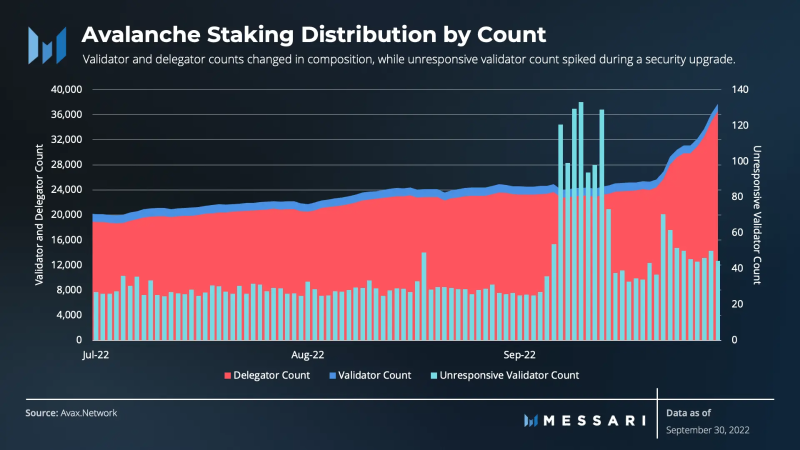

Unlike average staked amounts, the average number of validators and delegators changed significantly. The average number of validators decreased from 1,465 to 1,273 (–192 validators), representing a ~13% drop in participants securing the network. Given recent subnet onboarding, the average number of validators is expected to grow as more AVAX is staked.

While the average amount staked by delegators remained flat compared to the previous quarter, the average number of delegators increased substantially. The average number of delegators moved in the opposite direction of validators, rising from 17,179 to 20,218 (+3,039), an increase of approximately 12%. The number of delegators consistently exceeds the number of validators.

Technically, the number of inactive validators declined quarter-over-quarter, but as a percentage of average validators, it increased. Avalanche Go V1.8.0 (Apricot Phase 6), a mandatory security upgrade released during this period, required node operators to upgrade by September 6, or risk losing uptime. While not a severe issue, the upgrade appeared to be delayed by some validators.

Finally, low volatility in stake, validator, and delegator counts continues to indicate network health and progress toward greater decentralization.

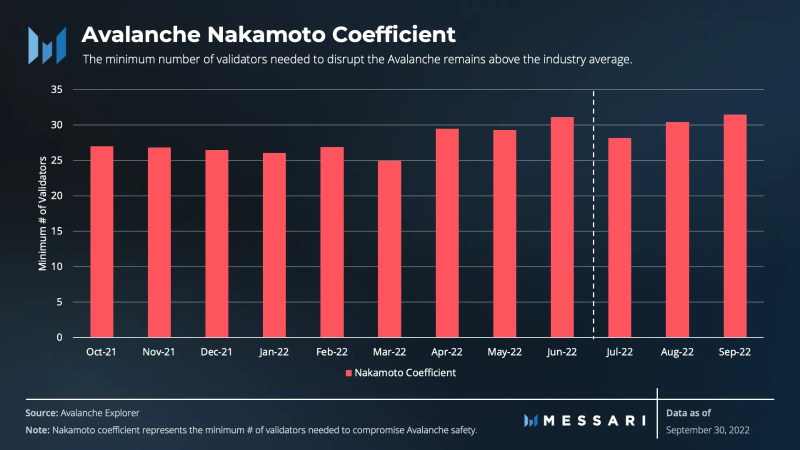

Avalanche’s Nakamoto coefficient continues to hover around 30, gradually improving over the long term. Similarly, as more subnets come online and validate on the Primary Network, the Nakamoto coefficient is expected to slowly increase.

Compared to other Layer 1 networks, this improvement keeps Avalanche above industry averages.

Competitive Analysis

Technical advancements, developer activity, and ecosystem growth strategies differentiate Layer 1 networks from one another.

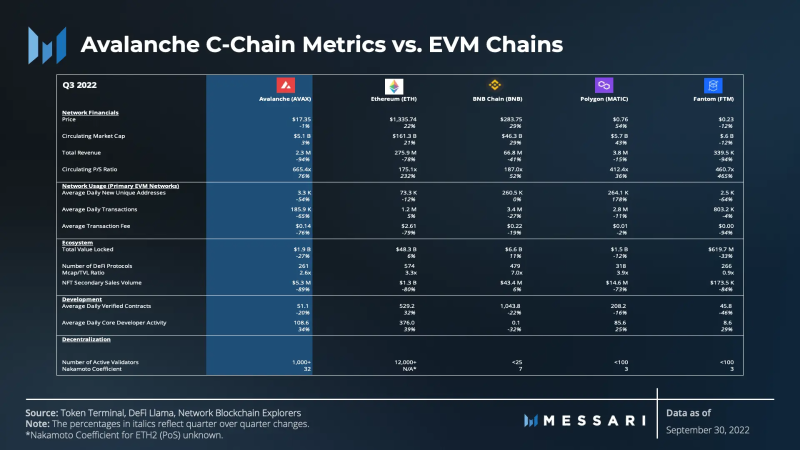

Here, we evaluate Avalanche’s key metrics against the top five EVM-compatible chains—including Avalanche—ranked by TVL and number of DeFi protocols.

This peer group consists of EVM chains with the highest TVL and most protocols, as DeFi remains the primary economic driver across each network.

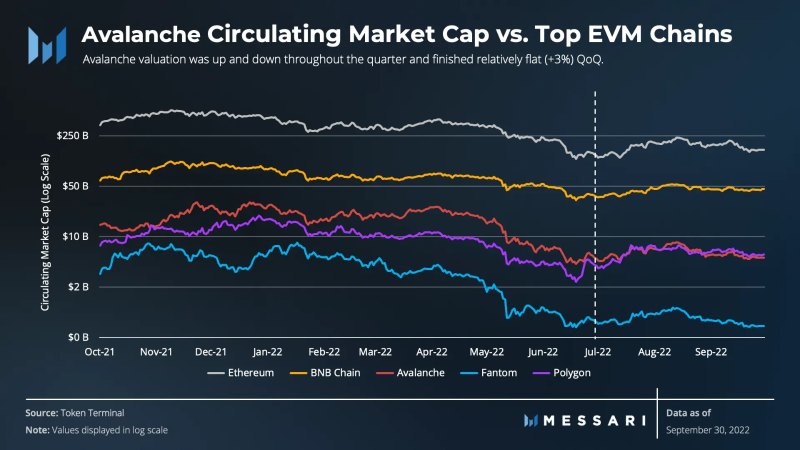

Avalanche’s valuation fluctuated throughout the quarter but remained relatively flat in market cap (+3%).

Ethereum, BNB Chain, and Polygon regained market cap dominance this quarter, achieving double-digit percentage gains.

Meanwhile, Fantom struggled significantly in price performance.

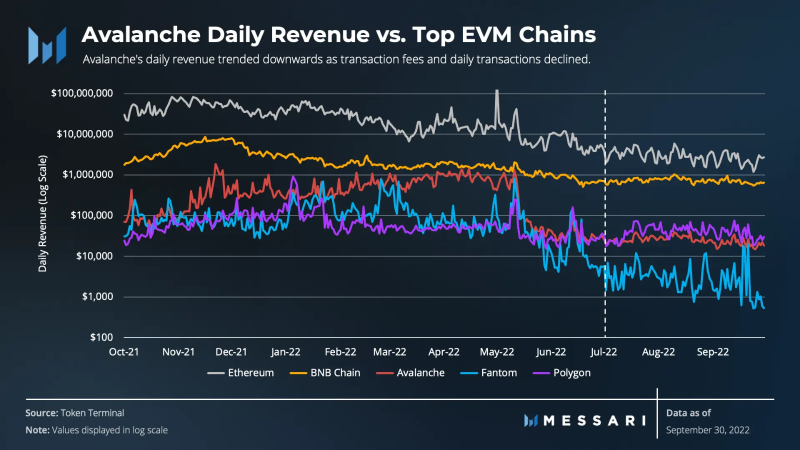

With declining average transaction fees and daily transactions, Avalanche’s daily revenue showed a clear downward trend.

Peers (excluding Ethereum) showed similar trends due to lower average transaction fees and daily transaction volumes.

Interestingly, Ethereum’s average transaction volume increased, but after the Merge, it experienced a sharp drop in transaction fees, reducing protocol revenue by ~80%.

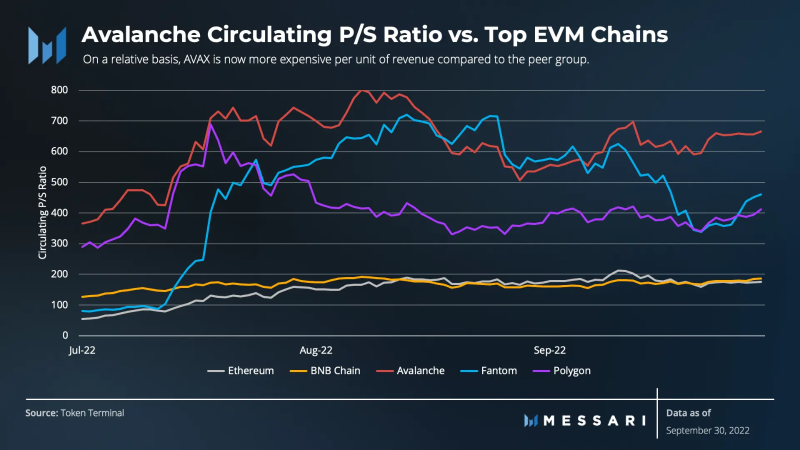

This quarter, Avalanche’s P/S ratio increased significantly compared to peers.

Changes in P/S measure a protocol’s revenue and give insight into the volume and pricing of transactions processed.

Ethereum’s P/S increase was not due to declining transaction volume but lower transaction fees, widely seen as positive.

In contrast, Avalanche experienced declines in both transaction fees and daily transaction volume, making its P/S rise more pronounced.

Dividing valuation (price) by revenue (sales) provides further insight into how much the native token is worth per unit of revenue.

On a relative basis, AVAX now commands a higher price per unit of revenue compared to its peers.

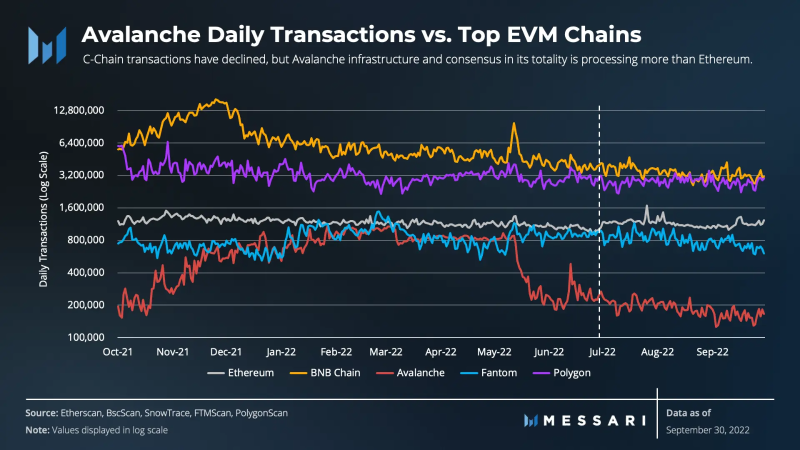

In early Q1 and Q2, Avalanche (C-Chain) reached daily transaction volumes comparable to Ethereum. With the launch of DFK and Swimmer subnets, daily transaction volume on the C-Chain plummeted and has since remained relatively stable. Ethereum’s transaction volume holds steady at around 1.15 million per day; earlier this year, Avalanche reached 74% of Ethereum’s volume but now hovers around 20%. Considering the holistic nature of Avalanche’s infrastructure and consensus, the network processes more average daily transactions than Ethereum. Overall, Avalanche’s entire infrastructure currently handles approximately 2.3 million transactions per day.

The crypto DeFi market performed modestly in Q3, starting and ending the quarter with total TVL around $54 billion. Avalanche ranked second among top EVM chains in TVL decline (-75%), with only Fantom falling more. Since TVL decline is typically measured in USD, falling asset values reflect price changes rather than actual DeFi utilization. Although USD-denominated TVL declined, the amount locked in AVAX remained relatively stable.

In early Q1 and Q2, Avalanche’s NFT sales rapidly surpassed those of Ronin, Flow, and Polygon.

However, secondary sales declined in May around the release of the Swimmer subnet.

Nevertheless, Avalanche NFT activity rebounded in Q3 and entered the top 10 by total sales volume over the past year.

With launches of Joepegs, Lost Worlds, and other NFTs, sales volume should continue its upward trajectory from Q2 lows.

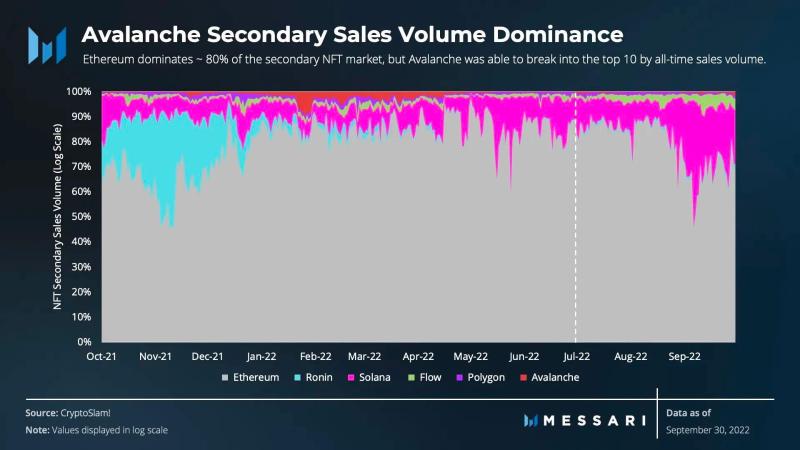

Although Ethereum still dominates about 80% of the secondary NFT market, Avalanche successfully broke into the top 10 by historical sales volume in early 2022.

Qualitative Analysis

Key Events, Catalysts, and Strategies for Ecosystem Growth

Like many networks during this bear market, the narrative for Q3 was relatively uneventful.

However, the Q3 narrative primarily revolved around building the Avalanche ecosystem and continuing to focus on executing its growth strategy.

As previously noted, the protocol made significant progress through the deployment of Blizzard and other initiatives to bring in real-world assets (RWA) and GameFi.

Avalanche’s strategy also includes several (albeit indirect) core elements, which can be summarized as follows:

- Technology integrations

- Core technology improvements

- Improved user experience (including user access)

- Expansion into unique domains and use cases

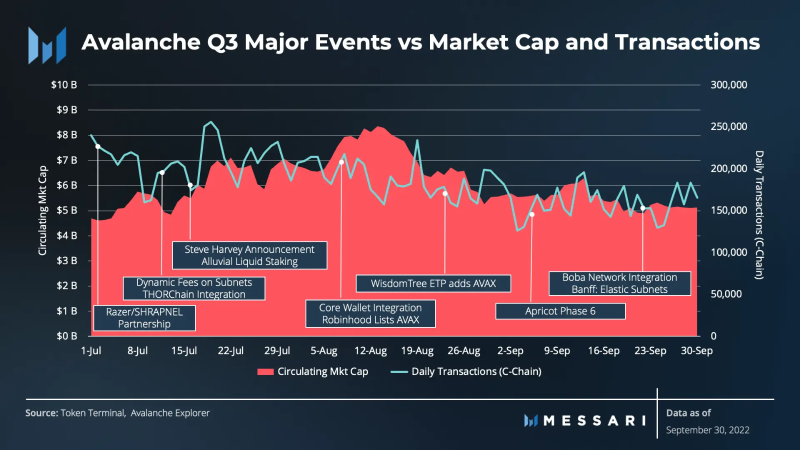

July 2022

In July, technology integrations aimed at enhancing user experience included THORChain’s integration with the Avalanche C-Chain. This integration allows C-Chain users to enter and exit the ecosystem without relying on cross-chain bridges. Additionally, Infura, a widely used blockchain developer toolkit, announced support for the C-Chain. This integration enables developers to use easy-to-use tools to leverage the C-Chain.

Moreover, institutional liquid staking solutions enhanced user experience. Alluvial Finance and Rome Blockchain Labs brought a standardized liquid staking solution to Avalanche. The platform will be managed in a decentralized manner and meet KYC and AML standards for regulated institutions.

Core technological enhancements were also introduced with configurable subnet fees. Since the launch of Subnet-EVM, one of the most requested features has been the ability to flexibly reconfigure fees without requiring network upgrades. Configurable fees became a reality in Q3, improving user experience and strengthening the value proposition of subnets.

Finally, unique use cases began emerging in July. Landslide Network, a subnet designed to reduce Tendermint consensus finality time, announced it would launch an incentivized testnet in Q4 2022. Beyond reducing Tendermint finality, it will enable Cosmos and Terra ecosystems to natively run any Tendermint-based application within the Avalanche ecosystem.

August 2022

Technology integrations continued in August. Non-custodial Web3 browser extension Core launched support for all blockchains running EVM and custom subnets. This integration enables seamless switching across all major blockchains, including Ethereum and Bitcoin. As demonstrated at Avalanche House Brooklyn, QuickNode allows builders to launch a node in seconds using its global RPC endpoint network.

Liquid staking solutions expanded user access. GoGoPool, a new deposit protocol that raised $5 million in seed funding, brought liquid staking to Avalanche. Specifically, it aims to reduce the cost and friction of launching subnets. Beyond additional liquid staking, partnerships with Shapeshift, Robinhood, and Wisdom Tree opened new avenues for AVAX adoption.

More unique use cases also emerged. CurateDAO launched a Pinterest-like database platform on Avalanche based on a “curate-to-earn” model, where participants earn by contributing to the database. Additionally, August brought Republic and the first tokenized film finance product (FFO) to Avalanche. FFO began accepting investment commitments in August, introducing a novel way to participate in film financing.

September 2022

As the quarter ended, additional integrations improved user access and experience. At the beginning of September, wallet provider Bitcoin.com announced AVAX support.

Another notable integration aimed at improving UX was with Boba Network. Boba Network, a Layer 2 scaling solution, became the first L2 on Avalanche’s C-Chain. The integration gives Avalanche developers another low-cost, high-speed, highly scalable option.

The most notable event in September was likely the launch of Banff, an upgrade to AvalancheGo that will bring elastic subnets to the ecosystem. Banff will enable subnet creators to activate Proof-of-Stake validation and runtime-based rewards. The upgrade will allow anyone to become a subnet validator by simply staking their native token on the P-Chain. This setup offers builders more flexibility when designing their subnets.

Ecosystem Challenges

No major adverse outcomes arose from technical challenges during Q3. However, the rollout of Apricot 6 did require attention. The mandatory security upgrade led to increased instances of unresponsive validators, though it did not jeopardize the network.

The Avalanche cross-chain bridge also encountered node instability issues, resulting in unprocessed transactions until resolved. Avalanche conducted node maintenance and quickly upgraded to the latest AvalancheGo version.

Beyond upgrade-related impacts, a vulnerability was identified and fixed during the quarter. Native asset call precompiles—a C-Chain-specific feature used to interact with Avalanche’s native tokens—were found to be exploitable. The issue was promptly addressed by disabling all vulnerable Avalanche contracts. AvalancheGo V1.9.0 will completely deprecate the precompile and introduce a more secure alternative to restore full functionality of Avalanche’s native tokens on the C-Chain.

Path Forward

To date, Avalanche has not provided a publicly available development roadmap. However, announcements regarding future plans are regularly communicated.

In the coming months, many subnets on the Fuji Testnet will begin transitioning to the Avalanche mainnet. P-Chain validators are expected to expand with this migration.

Following completion of the Apricot upgrade phases, the Banff upgrade cycle will accelerate. Banff will unlock interoperability value across the entire Avalanche ecosystem, similar to IBC completion on Cosmos. It will enable cross-subnet asset transfers, permissionless subnets, and reward subnet validators in their native tokens.

While Avalanche incentive programs may continue catalyzing ecosystem growth, major technological advances like Banff are expected to soon drive further expansion.

Closing Summary

Overall, Q3 was a quarter of building and executing Avalanche’s strategy and vision. While lacking the excitement witnessed during last year’s bull market, the network’s core user base and capacity to advance its market position have become evident.

For example, integration with Core increased user access and enhanced user experience.

Additionally, the ecosystem expanded beyond DeFi, embracing unique use cases such as NFT activity, real-world assets (RWA), GameFi, and FFO.

As network capabilities advance and subnet usage grows, Avalanche’s mission of adoption continues progressing.

Avalanche incentive programs may continue fostering ecosystem growth, and many subnets on the Fuji Testnet will begin migrating to the Avalanche mainnet, accompanied by validator and ecosystem expansion. Finally, major technological advancements like Banff are on the horizon and are expected to further stimulate growth.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News