NFTFi Sector Overview: Can NFTs Replicate DeFi's Rise?

TechFlow Selected TechFlow Selected

NFTFi Sector Overview: Can NFTs Replicate DeFi's Rise?

Current NFTFi sector subcategories, along with brief introductions to some representative projects.

Author: Mushroom

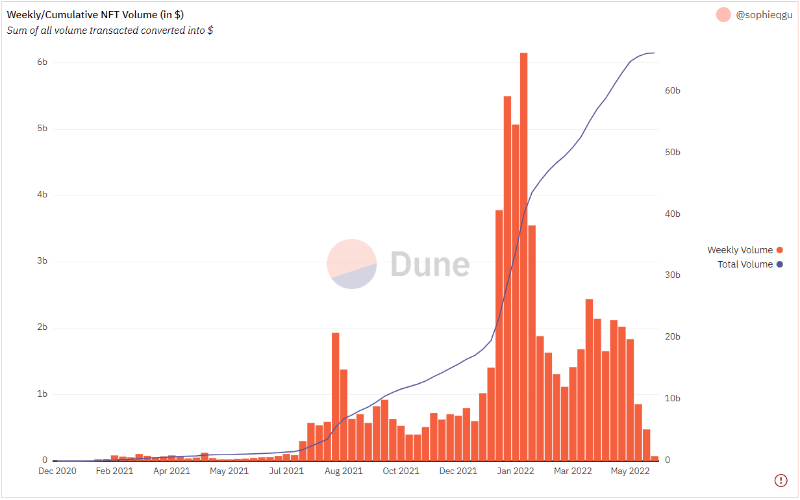

The NFT market began its explosive growth in January last year and remained a leading trend throughout the year.

According to data from Dune Analytics, weekly trading volume in the NFT market reached $6.15 billion in January this year. To date, cumulative trading volume in the NFT market has exceeded $60 billion. During this period, numerous popular NFTs emerged, such as Meebits, CryptoPunks, and BAYC. NFTs have also helped the blockchain industry break into the mainstream once again—many friends outside the crypto space have started using NFTs as profile pictures, reflecting the market's popularity.

However, as the broader cryptocurrency market turned bearish, the NFT market was inevitably affected, with trading volume and value beginning to decline rapidly.

As overall market conditions tightened, the already illiquid NFT market cooled down quickly, leaving early investors in a difficult position. The main reasons for poor market liquidity include the following:

1. High Entry Barrier. Prices of currently popular blue-chip NFTs have become extremely high, deterring average investors due to the steep cost. As a result, assets circulate mostly among users with large capital, leading to insufficient liquidity due to the lack of broad-based participation.

2. Difficulty in Price Discovery. NFT transactions are primarily peer-to-peer. Due to the non-fungible nature of NFTs, each one is unique—even within the same collection, prices vary significantly.

There is currently no strong consensus on NFT valuations, especially since most blue-chip NFTs are image-based, making pricing highly subjective. Different users estimate values very differently, and there are few effective tools for value discovery. Without fair market pricing, peer-to-peer trades are hard to execute and often take a long time to match. Additionally, valuation systems for blue-chip versus non-blue-chip NFTs differ greatly, making it difficult to generalize.

3. Most NFTs Lack Utility. Holders typically buy NFTs hoping to resell at a higher price, but limited use cases make trading difficult.

Low liquidity and difficulty in price discovery reinforce each other. Lack of price consensus reduces transaction frequency, while improving liquidity could increase trading activity and facilitate better price discovery.

To improve NFT market liquidity and unlock value for investors holding NFTs, the NFT finance (NFTFi) sector has emerged.

Financialization transforms illiquid assets into security-like products, granting them liquidity. Having observed the development of traditional finance and the rise of DeFi, can the NFT sector follow a similar path? How can NFT holders extract greater value and achieve higher capital efficiency?

Below, we outline the current landscape of the NFTFi sector and introduce several representative projects.

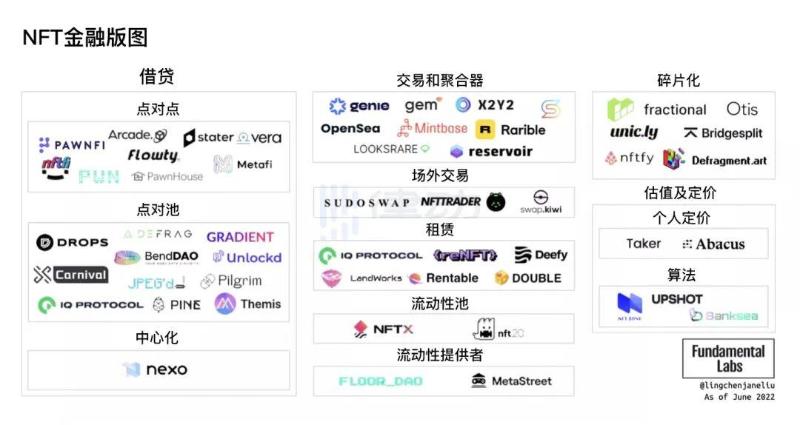

Current NFTFi Ecosystem Overview

Image source: Fundamental Labs

The NFTFi sector currently includes several key areas: NFT marketplaces and aggregators, over-the-counter (OTC) trading, lending, leasing, liquidity pools, liquidity providers, fractionalization, and valuation/pricing.

1. Marketplaces and Aggregators

Marketplaces and aggregators serve as platforms where users buy and sell NFTs. This is the earliest and largest segment of the NFT market, with leading platforms including OpenSea and LooksRare. As shown in the chart below, most NFT trading activity is concentrated on these two platforms.

Daily NFT trading volume across platforms

2. Over-the-Counter (OTC) Trading

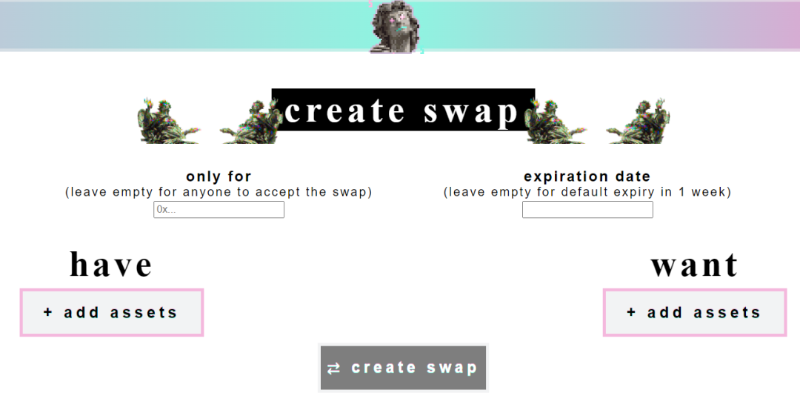

OTC trading refers to direct transactions between parties without going through a third-party platform. Users can create trade requests and wait for others to accept or negotiate. They can also initiate targeted trades with specific counterparties. Trade details are discussed via chat, and once agreed, both parties send their assets to an escrow smart contract that automatically executes the trade without requiring intermediaries. Notable projects in this space include Sudoswap, X2Y2, and tader.xyz.

Sudoswap

Sudoswap is a non-custodial trading platform with no platform fees, optimized gas costs, and support for trading both ERC-20 and ERC-721 assets.

Users can create private swap offers directed at specific wallet addresses, specifying the assets they hold and those they want in return, then share a swap code with the counterparty to complete the exchange.

Sudo has launched SudoAMM, an automated market maker (AMM) contract focused on NFT liquidity. Similar to Uniswap’s liquidity pools, anyone can create an NFT-ETH liquidity pool, provide NFTs or ETH as liquidity, and trade NFTs for ETH or vice versa within the pool.

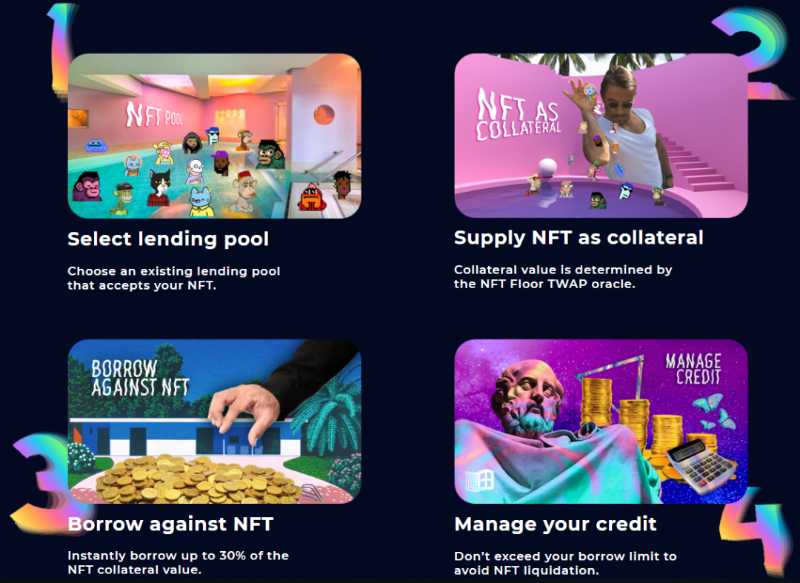

3. NFT Lending

Lending was one of the earliest and most explosive sectors in DeFi. As a core financial infrastructure, lending holds significant potential for future growth.

NFT lending allows users to borrow cryptocurrency by using NFTs as collateral through over-collateralization.

For an NFT to be accepted as collateral, there must be market consensus on its value—both that it holds value and that its price is widely acceptable. For this reason, only blue-chip NFTs like CryptoPunks are currently eligible as collateral.

Lending platforms rely on Loan-to-Value (LTV) ratios for risk management. When an NFT's value drops below the required threshold to cover the loan, the collateral is liquidated. Thus, accurate NFT valuation is foundational to lending. However, the persistent challenge of pricing NFTs remains a major bottleneck for the development of NFT lending.

Currently, NFT lending operates in three main models:

1) Peer-to-Peer (P2P)

2) Peer-to-Pool (P2Pool)

3) Centralized Platforms

Representative projects include NFTFi.com, DropsDao, and Nexo, respectively.

1) Peer-to-Peer (P2P)

In P2P lending, borrowers list their loan requests and seek matching lenders.

Current P2P interest rates are relatively high, ranging from 30% to 100%, with LTV ratios around 50%. For example, an NFT valued at 100 ETH can secure a loan worth approximately 50 ETH.

A key drawback is the long matching time between borrowers and lenders. When funds are urgently needed, lenders hold significant negotiating power. NFTFi.com is a leading platform in this model.

NFTFi.com

Launched in 2020, NFTFi.com allows borrowers to pledge their NFTs on the platform and specify loan terms such as amount, duration, interest rate, and preferred currency. Lenders browse available loan listings, select desired ones, negotiate terms, and disburse funds. Upon loan maturity, if the borrower repays, the NFT is returned. If not, ownership transfers to the lender.

2) Peer-to-Pool (P2Pool)

In the P2Pool model, NFT holders deposit their NFTs into a pool to instantly receive loans. Borrowers don’t need to wait for a matched lender, resulting in faster access to funds and higher capital efficiency. These platforms typically require over-collateralization, with NFT valuation based on the recent floor price of the collection. This model heavily depends on accurate NFT oracle pricing, as valuation directly determines loan size and platform risk exposure.

DropsDao

DropsDao offers instant loans using a pooled NFT lending model.

NFT holders deposit their NFTs into category-specific pools. The valuation is determined by the platform based on the market floor price of that category. Borrowers receive loans worth about 30% of the NFT’s value and pay interest to the platform.

Lenders earn interest by supplying major cryptocurrencies or stablecoins to the pool.

3) Centralized Platforms

Centralized NFT lending platforms mainly target institutional clients, offering financial services exclusively to large holders of blue-chip NFTs. A notable example is Nexo.io.

Nexo

Nexo is a centralized lending platform allowing users to borrow against NFTs or lend crypto assets to earn interest. Its NFT lending service targets institutions holding blue-chip NFTs like CryptoPunks or BAYC valued over $500,000. Approved users are assigned dedicated account managers and can receive instant loans.

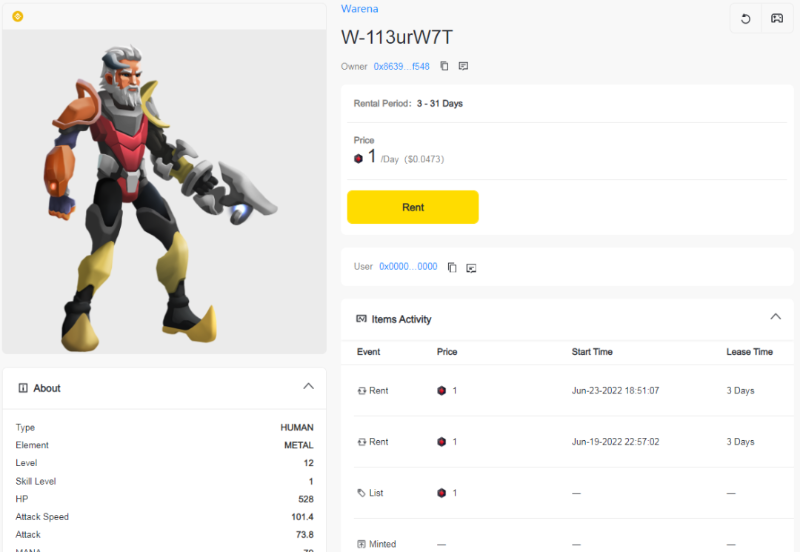

4. NFT Leasing

NFT leasing enables owners to retain ownership while temporarily transferring usage rights, unlocking value from idle NFTs.

Popular NFT types include profile pictures, domain names, metaverse virtual land, and gaming assets. While high prices limit trading liquidity, their utility makes short-term leasing a viable alternative. For lessors, leasing generates cash flow without selling; for lessees, it grants temporary access without full purchase.

Key projects include IQ Protocol and Double Protocol.

Double Protocol

Double Protocol is a leasing protocol primarily targeting gaming NFTs.

Its technical team proposed Ethereum Improvement Proposal 4907, which was later approved as the ERC-4907 standard. This standard defines leasing-related attributes in NFTs, such as user and lease duration, enabling separation of ownership and usage rights. It is the 30th ERC standard adopted on Ethereum. Before this, there was no universal NFT leasing standard, forcing projects to build custom contracts.

NFT owners can list their assets on Double Protocol, set minimum and maximum lease durations and rental fees, and publish listings. After selecting a term and paying rent, lessees receive a doNFT representing usage rights. Upon expiration, the contract automatically revokes access.

5. Liquidity Pools

Users can create NFT vaults and earn trading fees by providing NFT liquidity (depositing NFTs). Leading projects include NFTX and nft20.

NFTX

NFTX helps users convert hard-to-trade NFTs into more liquid ERC-20 tokens.

Users deposit NFTs into an NFTX vault and receive a fungible ERC-20 vToken. Each vToken can be redeemed 1:1 for an NFT from the vault—randomly by default, or a specific NFT for an additional 5% fee.

vToken holders can sell them on DEXs like Uniswap or Sushiswap for liquidity, or buy vTokens on DEXs and redeem NFTs from the vault.

NFTX’s PUNK Vault

When vTokens are traded in DEX liquidity pools, price discovery occurs. Since vTokens are backed 1:1 by NFTs in the vault, they effectively aggregate similarly valued NFTs. For instance, if a user believes a CryptoPunk is undervalued relative to the PUNK vToken price, they may deposit it into the vault, mint PUNK, and sell it on the market. This arbitrage mechanism helps converge toward a fair floor price for a given NFT collection.

For collectors holding low-liquidity NFTs, depositing into a vault earns them a share of trading fees, and selling vTokens allows conversion into stablecoins, thereby unlocking liquidity.

6. Liquidity Providers

Decentralized NFT market-making protocols aggregate users’ NFTs, offer staking rewards, and supply liquidity to platforms like NFTX. Key projects include FLOOR.DAO and MetaStreet.

FLOOR.DAO

Image source: Fundamental Labs

FloorDAO involves three main roles:

a) Creditors

Users who contribute NFTs to the protocol receive $FLOOR tokens at a discount.

b) Stakers

Users who stake $FLOOR in the treasury earn rewards denominated in $sFLOOR.

c) Treasury

The FloorDAO treasury earns yield by providing NFT liquidity to NFTX vaults and token liquidity to Sushiswap, with all fees flowing back into the FLOOR treasury.

7. Fractionalization

As non-fungible tokens, each NFT is unique and indivisible like FTs, which limits liquidity. However, ownership of an NFT can be divided.

Fractionalization involves splitting a single NFT into multiple fragments—converting one NFT into thousands of fungible tokens (e.g., 1 NFT → 10,000 FTs). This lowers entry barriers and improves liquidity. Similar to stock "fractional shares" in traditional finance, it allows investors to own a portion of high-value assets without buying the whole unit—as seen with Robinhood allowing partial Tesla stock purchases. Notable projects include Fractional.art and Unic.ly.

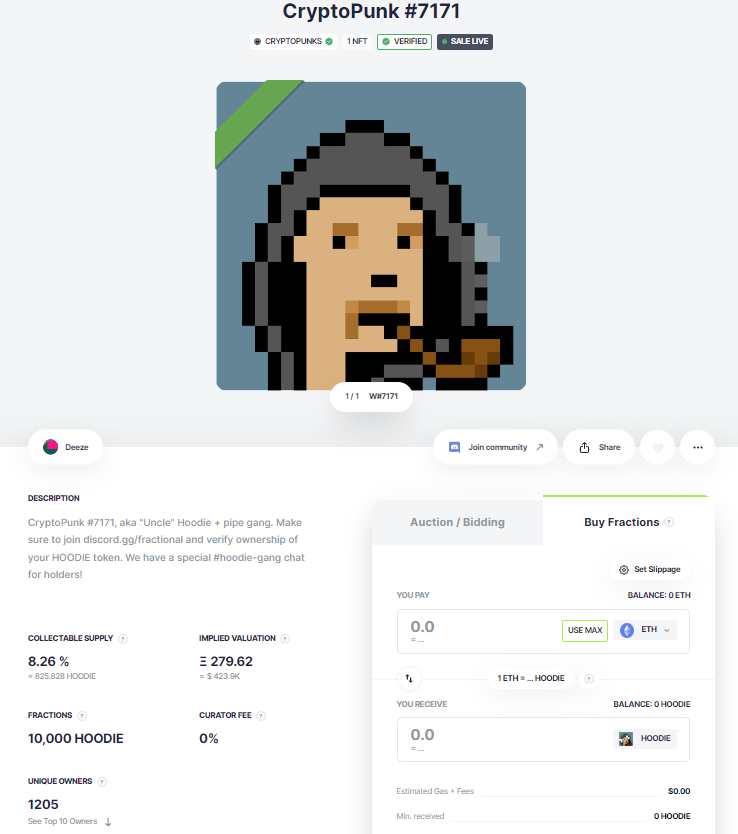

Fractional.art

Built on Ethereum, Fractional.art allows NFT collectors to lock their NFTs in a smart contract and issue ERC-20 fungible tokens representing shared ownership.

Users set how many FTs to mint per NFT and define a reserve price. After depositing an NFT into a vault, they receive corresponding FTs. For example, a CryptoPunk holder can deposit CryptoPunk #7171 into the HOODIE vault and receive 10,000 HOODIE tokens. These can be kept or distributed. Full redemption of the NFT requires all FTs. Once a HOODIE-ETH liquidity pool is established on Uniswap, users can trade HOODIE tokens.

If someone bids above the reserve price for the vaulted NFT, an auction is triggered, and FT holders receive proportional proceeds.

8. Valuation and Pricing

As discussed, NFT valuation is critical infrastructure for the entire NFT finance ecosystem. Both trading and lending rely on accurate pricing, which plays a vital role in improving market liquidity. Robust pricing systems reduce transaction matching times and accelerate lending market development. Many projects are exploring this area, with several main approaches emerging.

a) Oracles

In DeFi, oracles are essential for connecting smart contracts to real-world data. Similarly, NFTFi widely uses oracles to link to external market prices.

Reliable oracles require trustworthy data sources and sound aggregation methods. The two most commonly used data sources in NFTFi are OpenSea’s API and NFTX’s floor prices. OpenSea, as the dominant NFT marketplace, offers valuable pricing signals, though listing-based pricing leaves room for manipulation. NFTX’s floor price mechanism, driven by arbitrage within pooled collections, tends to correct price deviations and reveal fair floor prices.

Most protocols combine prices from OpenSea, NFTX, and other sources using weighted averages to determine final reference prices.

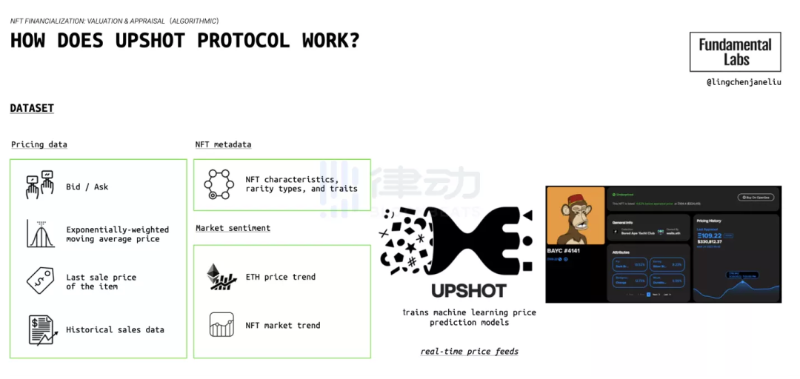

b) Machine Learning

Some protocols apply machine learning algorithms, training models on historical transaction data to predict NFT valuations. Notable examples include NFTbank, Upshot, and Banksea.

Like oracles, ML processes metadata to generate outputs. However, ML models first define NFT traits, group NFTs accordingly, analyze pricing patterns within groups, and then predict values based on feature similarity.

Image source: Fundamental Labs

c) P2P Lending Markets

Price discovery also occurs organically within P2P lending activities.

For a loan to be matched, borrowers and lenders must agree on an NFT’s value, effectively establishing market prices. Thus, lending platforms double as price discovery venues.

However, pricing here is subjective and influenced by borrowers’ urgency for funds, potentially causing price distortions. Moreover, once priced, the valuation remains static for the loan duration, limiting dynamic adjustment.

d) Rational Agents

Abacus Protocol uses profit-maximizing rational actors to determine NFT valuations.

Abacus establishes a liquidity-backed valuation system. Users create NFT pools and deposit ETH as liquidity. The total value of ETH locked in the pool at any time equals the collective value of the NFTs in that pool.

Conclusion

Insufficient NFT market liquidity has created demand for financialization. The market has explored various NFT financialization avenues—trading, lending, leasing, liquidity pools, fractionalization, and more. However, challenges such as pricing difficulties, lack of price consensus, and limited utility mean these efforts remain in early stages.

The NFT market continues to grow and has achieved initial mainstream adoption. Looking back at the evolution of traditional finance and DeFi, we believe NFTFi holds immense potential. With ongoing infrastructure improvements and innovation, more robust solutions will emerge, empowering the entire NFT ecosystem.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News