Dragonfly Investor: Analyzing the DeFi Cycle Narrative — Why Has It Lagged So Far Behind L1?

TechFlow Selected TechFlow Selected

Dragonfly Investor: Analyzing the DeFi Cycle Narrative — Why Has It Lagged So Far Behind L1?

Although L1s were able to surpass DeFi in the previous cycle, none of them can advance further if we don't figure out where new users are coming from.

Written by: Celia Wan, Dragonfly Capital

Translated by: TechFlow intern

You know a cycle is ending when people begin to question everything they believed during the bull market.

This crypto cycle began with Compound launching COMP and popularizing single-token staking, and officially ended with Terra’s collapse—killed by Anchor’s promise of 20% yields and the hyperinflation of LUNA.

This crash triggered a wave of introspection about the validity of every other DeFi project—even Bitcoin:

Typically, when trends collapse, bubbles evaporate too. Take Terra—one of DeFi and L1's biggest success stories. Its failure dimmed the appeal of single-token staking, reset expectations, and adjusted prices accordingly.

Although many tokens are now at all-time lows, the market is converging toward new price levels—not based on hype, but on a more realistic assessment of what we actually achieved in the last cycle. The bear market is an excellent time to reflect on the past year and our real progress.

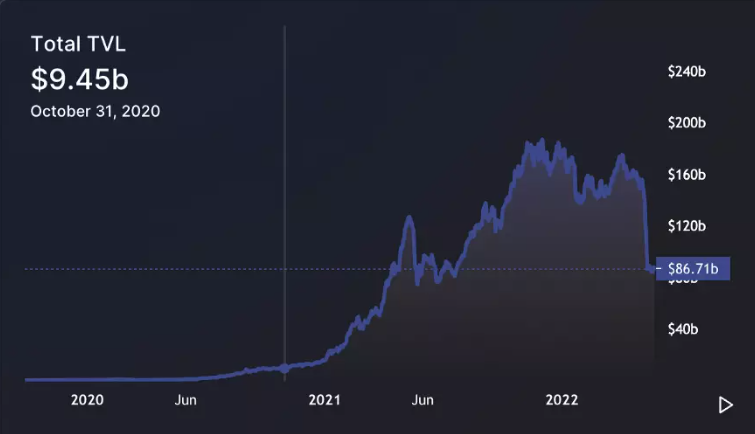

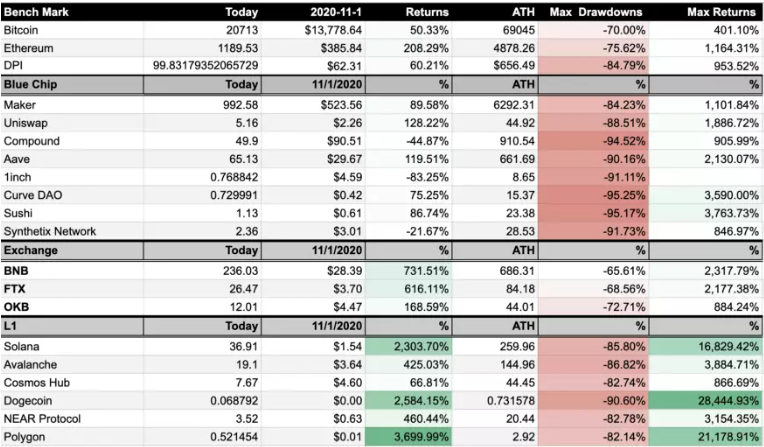

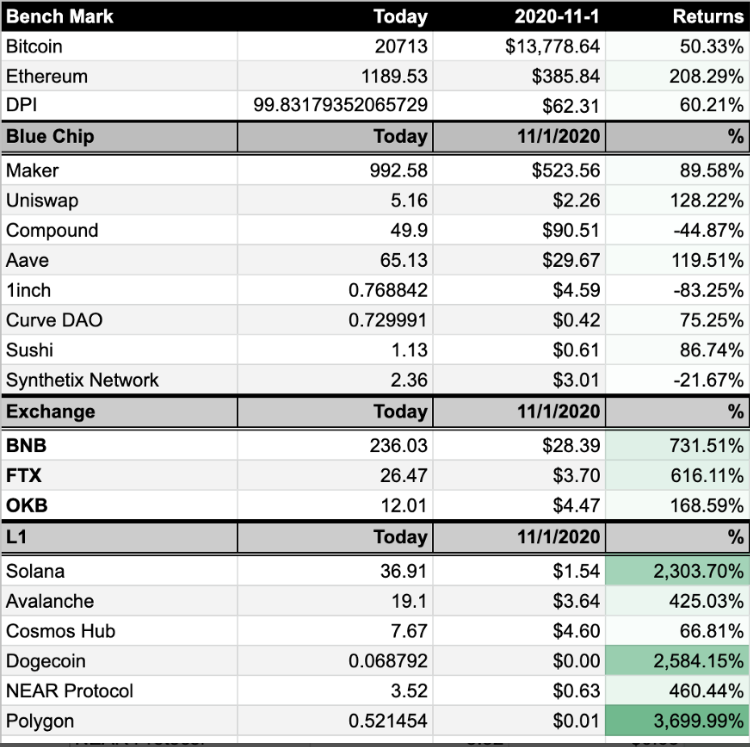

To contextualize this against the previous price cycle, we compared current prices of notable DeFi and L1 projects to their all-time highs (ATH), as well as to their prices on November 1, 2020. We chose this date because it marked the early phase of the cycle—when DeFi and L1 narratives were beginning to form, but the bubble was still small. At that point (November 1, 2020), Uniswap had launched its token just two months earlier, but price momentum hadn’t kicked in yet; DeFi TVL was nearing $10 billion but hadn’t seen exponential growth; projects like Avalanche, Solana, and Terra hadn’t started their liquidity mining programs, and few were talking about them.

These data points reveal three key insights:

1) The maximum possible return from investing since the start of the cycle;

2) A project’s ability to retain value by the end of the cycle;

3) The drawdown each token experienced from ATH to cycle end.

It turns out both DeFi and L1 performed worse than Ethereum and Bitcoin in terms of drawdown. This isn't surprising—ETH and BTC enjoy the strongest market consensus, which is less sensitive to market swings. For the same reason, Ethereum and Bitcoin delivered lower peak returns compared to most DeFi and L1 tokens.

Meanwhile, in terms of peak returns, L1s were clearly the winners of this cycle. The top two projects—Solana and Polygon—gained fame through generous ecosystem funding and liquidity mining incentives. Both delivered five-digit returns, far surpassing other L1s like Avalanche and Near.

Overall, L1s outperformed DeFi, and even blue-chip DeFi projects lagged behind (though they still achieved impressive four-digit gains). COMP and SNX performed worse, possibly because their price cycles don’t align with the one under discussion (SNX launched in 2018; COMP was already active before November 1, 2020).

This pattern tells us one thing: In the past cycle, DeFi did not generate much alpha over the beta of L1s.

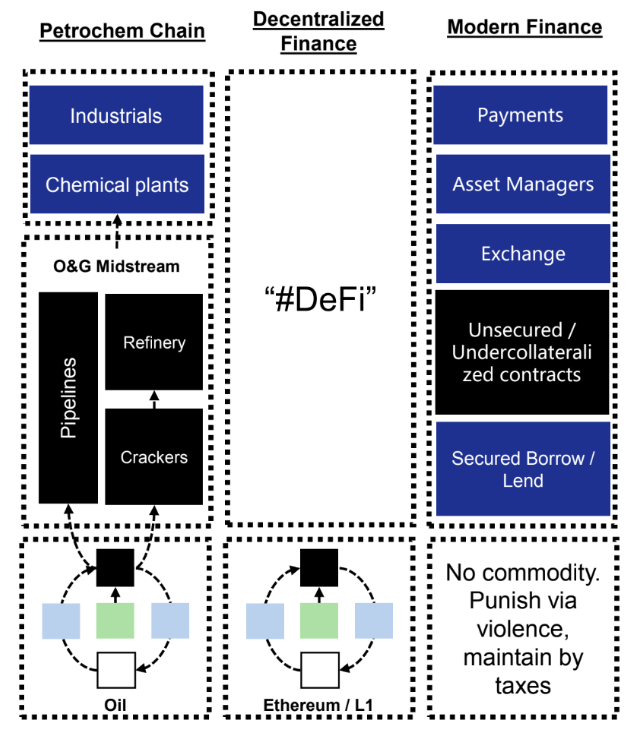

Jason Kam proposed a useful mental model for this. During the 2020 DeFi Summer, he asked a thought-provoking question: “If ETH is like the energy commodity used to build a petrochemical value chain (DeFi), is it better to invest in oil or in petrochemical/industrial stocks?”

Looking back at what we’ve achieved in the past cycle, the answer seems clear: The risk-return profile of base-layer tokens has been better than any application built on top—at least so far. Over the past two years, blue-chip DeFi tokens have suffered drawdowns similar to L1s during market downturns, but shown less upside potential during rallies.

Heuristically, this makes sense. So far, much of the hype around DeFi stemmed from its ability to bring “users” and “liquidity” to L1s. However, when users actually arrived on L1s, they were mostly drawn by staking incentives—and quickly realized these incentives were the only thing they could do on-chain. When yields dropped, they migrated to other L1s offering higher returns.

In this dynamic, DeFi adds no real value to L1s. DeFi exists to make L1s look good—it’s a means to inflate TVL and user counts, creating an illusion of “adoption.” Yet, many DeFi projects themselves haven’t benefited from different blockchains; some are even hindered by non-EVM-compatible chains and poor developer documentation.

As a result, these DeFi projects lack intrinsic drivers to sustain their market cap. Their growth depends heavily on L1 expansion, and their competitive edge is constrained by the ecosystems they belong to.

The most telling numbers come from comparing current token prices to those at the cycle’s start. These figures show how much value DeFi and L1 projects retained after the LUNA collapse washed away much of the froth.

The results show that while nearly all tokens posted double-digit gains during this period (except COMP, 1INCH, and SNX), DeFi did not outperform Ethereum or L1s in terms of value retention.

Take UNI, for example: it returned 128.22% from November 1, 2020, to today, while Ethereum returned 208.26% (UNI also received a recent price boost from acquiring Genie and announcing a new NFT roadmap). In other words, if you held ETH from the start of the cycle, you would have outperformed DeFi (“Hold” matters because ETH’s peak return was lower than UNI’s)—and the same applies to many other DeFi tokens.

This is a sobering view of what value remains when the cycle ends. The old playbook of using liquidity incentives and airdrops to attract users to DeFi no longer works. DeFi brought users to L1s without caring what those users actually did. The result? DeFi became part of a service industry that only serves itself—users participate in DeFi to participate in DeFi, not to use it for anything else. This self-service model sometimes devolves into Ponzi schemes.

Of course, price isn’t everything. Real innovation did happen in DeFi during the last cycle—progress that can’t be captured by token prices. For instance, Uniswap V3’s groundbreaking concentrated liquidity feature opened vast design space for new applications. Demand for blockspace spurred a wave of blockspace financialization protocols like Flashbots and Alkimiya.

Finally, some DeFi protocols launched their tokens late in the cycle and never had a chance to fully realize their potential. Projects like Lido, Ribbon, and dYdX have major product or industry upgrades coming that could further drive their growth.

Lido’s TVL will receive a massive boost post-Merge on Ethereum. Ribbon offers a range of structured products ideally suited for on-chain composability—but these remain largely unexplored. dYdX and other derivatives protocols still have a huge untapped market ahead, especially when compared to their off-chain counterparts in trading volume.

The truth is, although L1s outperformed DeFi in the last cycle, none of them can grow further unless we figure out where new users will come from.

When new categories emerge—ones that bring real users onto blockchains with actual financial needs that DeFi can serve—DeFi will become exciting again. The rise of NFTs and Web3 in the latter half of the cycle already signaled a demand distinct from over-leveraged tokens. These categories will attract new users and reconnect them to DeFi—that will be the story of the next cycle.

Until then, many questions remain unanswered, and teams need to focus on critical research within DeFi. The bear market gives them the time they desperately need to concentrate on building products, rather than rushing to launch and promote tokens.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News