BlackRock Report: This AI Rally Has Reached the "Halfway Point" of the 2000 Internet Bubble, One Indicator Is Flashing Red

TechFlow Selected TechFlow Selected

BlackRock Report: This AI Rally Has Reached the "Halfway Point" of the 2000 Internet Bubble, One Indicator Is Flashing Red

This moment, just like that moment?

Author: Monday, TechFlow

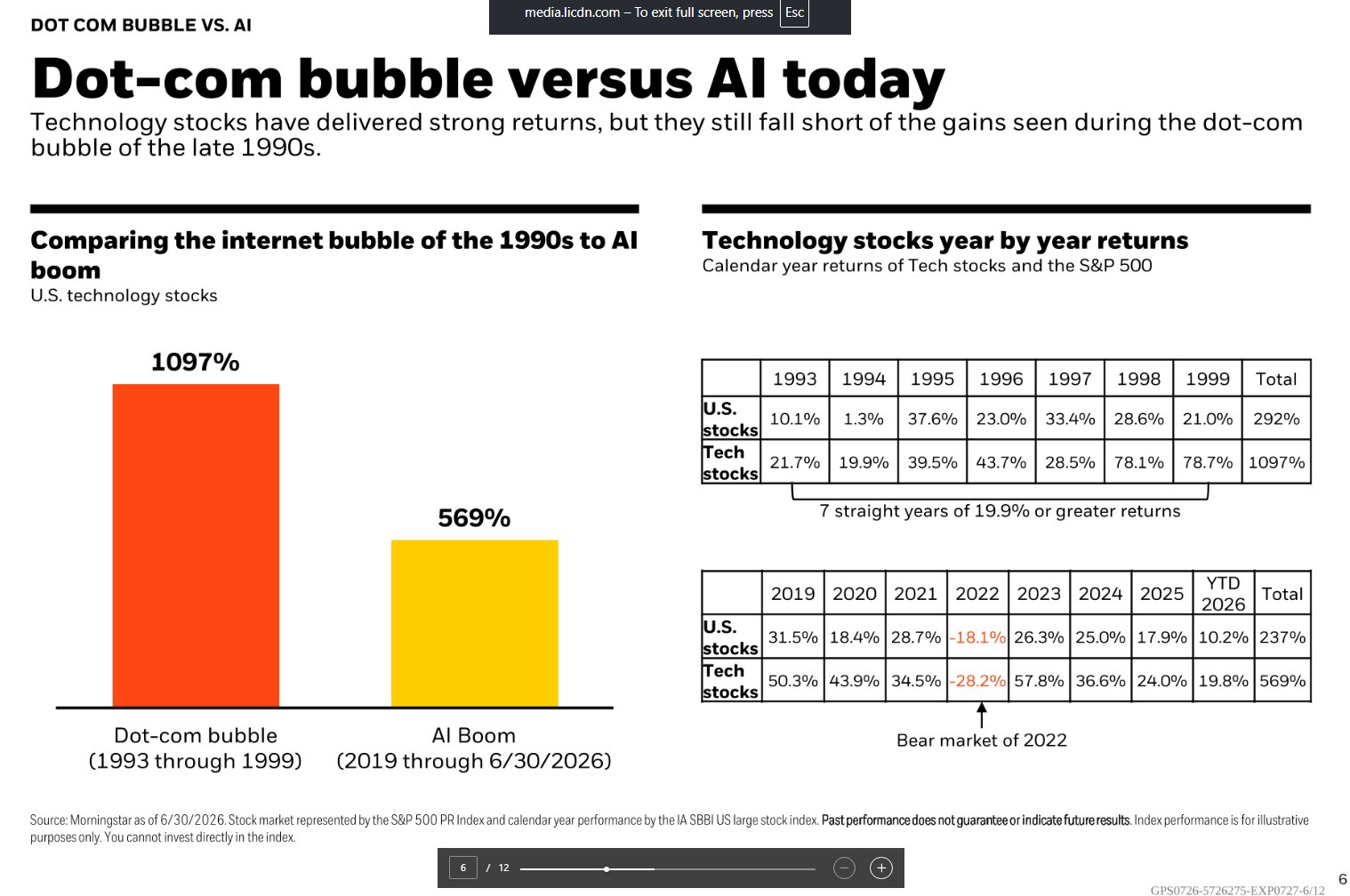

TechFlow Editor's Note: BlackRock's latest report directly compares the current AI bull market with the 1990s internet bubble: from 1993 to 1999, U.S. tech stocks cumulatively rose 1097%, while from 2019 to present, the AI rally has cumulatively gained 569%. The gain is only half of that period, but the S&P 500 Shiller CAPE has returned to 40x (level with the 2000 bubble peak), and the proportion of tech stocks in the U.S. stock market cap has exceeded 37.5%, surpassing the internet bubble period.

BlackRock's conclusion is: AI is not a bubble, but the premise is that earnings growth must be realized.

In the latest weekly commentary released on July 7, BlackRock directly responded to the market's hottest question: Is AI a bubble?

The answer given by this world's largest asset management company is: the key does not lie in where valuations stand relative to history, but in whether earnings growth can sustain. Meanwhile, analyst Mike Zaccardi shared a data comparison chart from a BlackRock internal presentation file on the X platform, making a visual comparison between the 1993 to 1999 internet bubble and the AI rally from 2019 to present. Data source is Morningstar, as of June 30, 2026.

The conclusion is straightforward: the AI rally has cumulatively risen 569%, only slightly more than half of the 1097% during the internet bubble period. But more important than the gain is the question of whether the fundamentals supporting this rally are more solid than back then.

Tech Stocks Rise 569% in 7.5 Years, Internet Bubble Rose 1097% in Same Period

According to BlackRock citing Morningstar data, over the 7 years from 1993 to 1999, U.S. tech stocks cumulatively rose 1097%, while the overall U.S. stock market rose 292% in the same period. Tech stocks had annualized returns of no less than 19.9% for 7 consecutive years, reaching 78.1% and 78.7% in 1998 and 1999 respectively.

In the AI rally cycle from 2019 to June 30, 2026, tech stocks' cumulative return was 569%, while the overall U.S. stock market return was 237% in the same period. During this time, there was a significant drawdown in 2022 (tech stocks fell 28.2% for the year), but rebounded 57.8% in 2023, rose 36.6% and 24.0% in 2024 and 2025 respectively, and rose another 19.8% in the first half of 2026.

The divergence between the two cycles is reflected in the latter half. The internet bubble accelerated towards the peak in the last two years, with cumulative gains close to 200% in 1998 and 1999; the acceleration phase of the AI rally appeared in 2023 (rebounding from the 2022 trough), but since then annualized gains have gradually narrowed. In other words, the pace of the AI rally is more restrained than the internet bubble, but how far it is from the "topping out" phase, market divergence is increasing.

Shiller CAPE Returns to 40x, But Forward P/E Is Only 21x

The S&P 500's Shiller CAPE has climbed to 40x, returning to the level of the internet bubble period. This is a classic indicator measuring whether long-term valuations are overheated, calculated using the average earnings over the past 10 years adjusted for inflation. 40x means investors are paying a price of $40 for every dollar of long-term average profit, a similar level historically reached only around 2000.

But BlackRock points out that the 12-month forward P/E provides a more balanced perspective. Currently around 21x, valuations look less exaggerated, the reason being earnings expectations rise in sync with stock prices.

S&P 500 second-quarter earnings are expected to grow 23% year-over-year, this is the seventh consecutive quarter recording double-digit growth. BlackRock emphasizes that this earnings growth rate is extremely rare in history. BlackRock Chief Investment Officer Rick Rieder revealed at the CNBC CEO Summit on June 2 that the Mag 7 tech giants' current P/E is 26x, earnings growth rate is expected to exceed 30% (composite growth rate about 27.6%), S&P 500 forward P/E 21x, one-year earnings growth forecast slightly higher than 20%.

The divergence between the two indicators constitutes the core contradiction of the current market: long-term valuation indicators have already issued bubble signals, but short-term earnings momentum is still providing support for high valuations.

Tech Stocks Market Cap Proportion 37.5%, Exceeding Internet Bubble Period

According to Morningstar data, as of May 31, 2026, the proportion of tech stocks in the U.S. stock market cap has reached 37.5%, exceeding the level of the late 1990s internet bubble period. This number does not include Alphabet and Meta classified as communication services sector, and Amazon classified as consumer discretionary. If adding these giants deeply involved in AI, the actual concentration is higher.

Market leadership is spreading from "Mag 7" to a broader group of AI beneficiaries. A new market acronym "MANGOS" has appeared, representing Meta, Anthropic, Nvidia, Google, OpenAI, and SpaceX. The Morningstar Global Next Generation Artificial Intelligence Index cumulatively rose about 45% in April and May 2026, subsequently fell back in June.

Concentration risk is one of the most similar characteristics between the current market and the internet bubble. In late 1999, a few companies such as Cisco, Intel, Microsoft, Oracle dominated the final sprint of Nasdaq. Although the current AI leadership profitability is far stronger than back then, once earnings growth fails to meet expectations, the stampede effect of concentrated holdings is equally unavoidable.

BlackRock's Core Argument: Judging "Bubble" Itself Is a Major Bet

BlackRock gave a thought-provoking statement in the weekly commentary: reaching the conclusion that AI has become a bubble is itself a major judgment, because it assumes AI technology will not bring lasting productivity and growth breakthroughs.

BlackRock believes AI provides the possibility of achieving "permanent growth breakthroughs" through accelerated innovation, but the investment needed to build the future is reinforcing scarcity. Based on this, BlackRock focuses on three themes in the mid-2026 outlook: AI scarcity (electricity, grid, chips, and data center bottlenecks), durable income (short-duration credit assets), and thematic investing beyond traditional asset classification.

BlackRock maintains an overweight position on U.S. stocks, preferring scarce inputs required by AI systems.

But opposing voices are equally clear. Morningstar pointed out in the latest market briefing that the concentration of tech stocks in the U.S. market has exceeded the internet bubble level, concerns over high interest rates, high valuations, and AI overinvestment are intertwining. Fidelity's research points out that the current capital expenditure to free cash flow ratio is below 1, meaning enterprises currently mainly use their own funds rather than debt to invest in AI. This forms a sharp contrast with the ratio close to 4x during the internet bubble period.

For investors, the core question has shifted from "how much can the AI rally rise" to "how long can AI earnings growth sustain". BlackRock bets on earnings realization, bears bet on earnings peaking. The earnings season in the second half of 2026 will be the key window to test these two judgments.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News