Downturn or Opportunity? The Crypto Market Enters a “Repricing Moment”: Macroeconomic Logic Behind the Downturn, Structural Transformation, and Future Turning Points

TechFlow Selected TechFlow Selected

Downturn or Opportunity? The Crypto Market Enters a “Repricing Moment”: Macroeconomic Logic Behind the Downturn, Structural Transformation, and Future Turning Points

This article systematically analyzes the current downturn in the cryptocurrency market based on macroeconomic conditions, institutional behavior, market structure, and industry trends. Drawing on HTX Research’s perspective, it offers forward-looking insights into potential future turning points and long-term trends, aiming to provide market participants with a more structured framework for judgment.

Since 2026, the cryptocurrency market as a whole has faced mounting pressure, with Bitcoin and major assets correcting in tandem and market sentiment cooling significantly. Behind this phase of underperformance lies a critical question: Is this the end of a cycle—or the prelude to structural reconfiguration? In its recently released 2026 Digital Asset Trends White Paper, HTX observes that digital assets are completing their historic establishment as an asset class, and the market’s driving logic has shifted comprehensively from “price cycles” to “structural trends.” This assessment provides a crucial interpretive framework for the current market—beneath short-term volatility lies a profound restructuring driven collectively by macro liquidity conditions, institutional participation, regulatory evolution, and upgrades to technical infrastructure. The white paper further posits that the central question for 2026 is no longer “Do digital assets hold value?” but rather “What allocation weight should they command within global portfolios?” Core assets such as Bitcoin are gradually embedding themselves into traditional financial systems, forming new portfolio structures alongside U.S. Treasuries and gold; meanwhile, the rise of stablecoins, real-world assets (RWA), and on-chain yield-bearing assets is reshaping how capital flows internally within the crypto ecosystem.

Against this backdrop, the current market “downturn” is fundamentally a transitional growing pain—the inevitable friction accompanying the shift from a high-volatility growth phase toward a mature financial system. This article systematically reviews the causes behind the current crypto market slump through the lenses of macroeconomic conditions, institutional behavior, market structure, and industry trends. Drawing on HTX’s research perspective, it also offers forward-looking analysis of potential turning points and long-term trajectories, aiming to provide market participants with a more structured analytical framework.

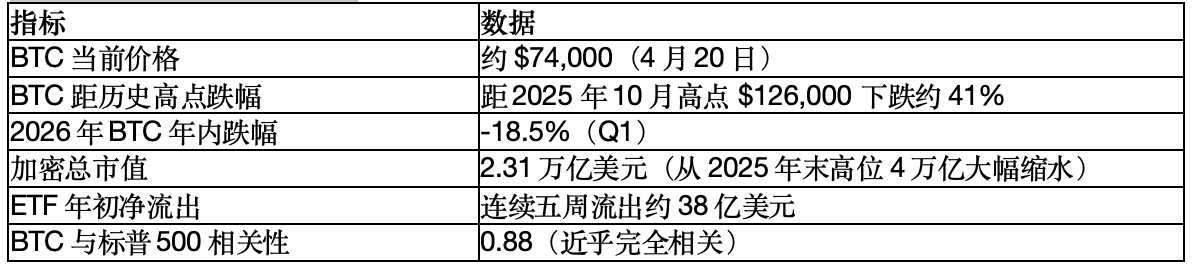

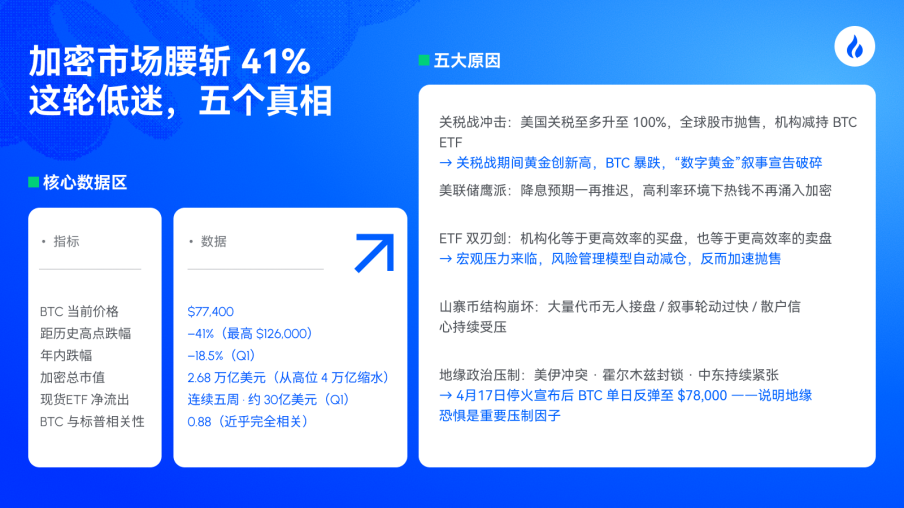

I. Current Market Overview

II. Core Drivers of the Market Downturn

1. Macroeconomic Pressure (Primary Driver)

The Trump tariff war represents the largest external shock since 2025.

• In October 2025, U.S. tariffs on Chinese imports rose to 100%, while “Liberation Day” retaliatory tariffs were launched against multiple countries.

• Tariff announcement → Global equity sell-off → Institutional reduction of BTC ETF holdings → USD strength → Rising Treasury yields → Leveraged liquidations cascade → Sharp BTC decline

• During the tariff war, gold hit an all-time high amid BTC’s sharp drop—shattering the “digital gold” narrative entirely.

• Concurrently, the IMF downgraded its 2026 global economic growth forecast, reinforcing recession fears and suppressing risk appetite.

Fed policy remains persistently hawkish.

• High interest rates make traditional savings more attractive, discouraging speculative “hot money” inflows into crypto.

• Expectations for Fed rate cuts have been repeatedly delayed; the window for liquidity easing remains unopened.

2. Institutional ETFs: A Double-Edged Sword

ETFs enable traditional institutions to sell Bitcoin as easily as equities. Institutionalization implies not only higher-efficiency buying but also higher-efficiency selling. When macro pressures mount, pension funds and registered investment advisors (RIAs) automatically reduce positions per their risk management models—accelerating sell-offs.

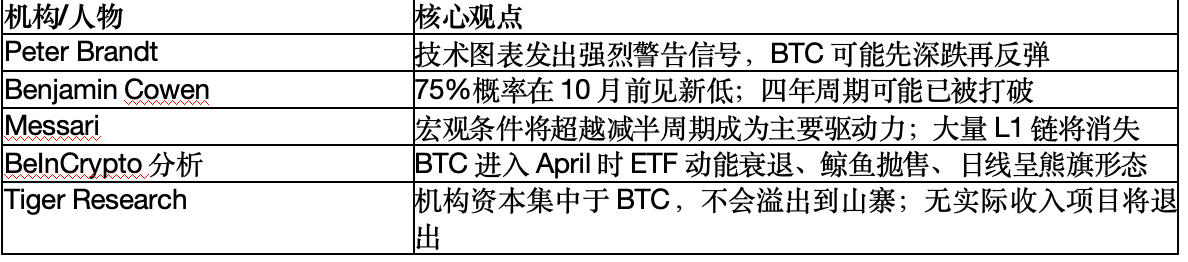

3. Debate Over Halving Cycle Reliability

Bearish view (Benjamin Cowen): Predicts a 75% probability that BTC will hit a new low before October 2026; the Pi-Cycle Top indicator shows no crossover signal, suggesting the October 2025 peak may be merely a local top.

Bullish view (Tom Lee): Post-halving liquidity trends have yet to manifest; structural institutional accumulation will surge following the Fed’s pivot later this year; price target: $200,000.

4. Structural Collapse in the Altcoin Market

• A large number of tokens issued in 2024–2025 have fallen into illiquidity traps with no buyers.

• Retail confidence remains suppressed by prior failures like FTX and Luna.

• Rapid rotation across AI- and meme-themed narratives has led to user fatigue.

• Tiger Research forecasts mass exits for projects unable to generate sustainable revenue.

5. Geopolitical and War Risks

• Persistent Middle East tensions (U.S.–Iran temporary ceasefire, continued closure of the Strait of Hormuz, Iran–Israel conflict, Lebanon–Israel conflict).

• Heightened trilateral tensions among the U.S., Israel, and Iran continue to suppress risk assets.

• Following Iran’s April 8, 2026 ceasefire announcement, Trump declared the Strait of Hormuz “temporarily open” on April 17—BTC surged intraday to $78,000, underscoring geopolitics as a key suppression factor.

III. Key Views from Institutions and Analysts

Bullish Camp

Bearish/Cautious Camp

Neutral/Structural Views

IV. Stablecoins: A Bright Spot Amidst the Downturn

Conclusion: During tariff-related panic, capital did not exit crypto—it migrated into stablecoins for safe haven purposes. This reflects rising trust in crypto infrastructure, even as tolerance for volatile assets declines.

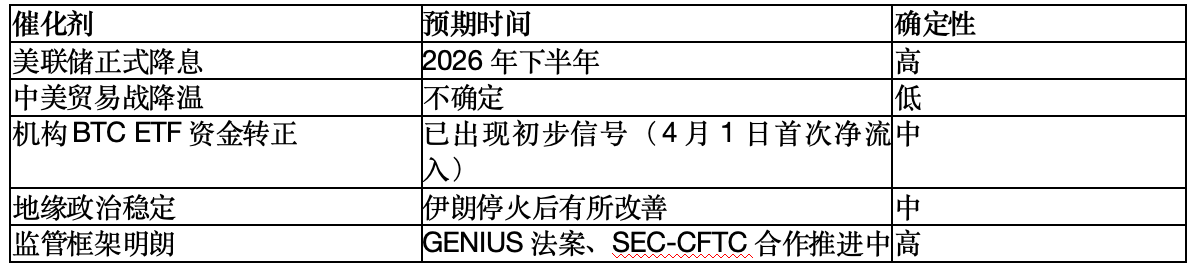

V. Catalysts for Recovery (When Will the Downturn End?)

VI. HTX Perspective

6.1 Core Assessment of the Current Downturn

HTX believes: The current downturn is not an endpoint—but growing pains during a structural transition.

“Digital assets are undergoing a fundamental shift—from price-cycle-driven to structure-driven markets. Macro liquidity, regulatory frameworks, institutional participation, and technological advancement are now the core determinants shaping the industry’s long-term landscape. Short-term price fluctuations will persist, but what truly defines the industry’s trajectory is the formal recognition of digital assets as an asset class, the maturation of infrastructure capabilities, and the restructuring of global capital allocations.”

6.2 Structural Interpretation of the Downturn’s Causes

A. Liquidity Rebalancing Is Fundamental

• The Fed continues to weigh inflation moderation against labor market resilience—its rate-cut timing remains uncertain.

• Weak European growth momentum and Japan’s progression toward interest rate normalization are altering global arbitrage fund structures.

• Digital assets are now deeply embedded in the global liquidity architecture—their pricing logic increasingly aligns with traditional macro assets. This explains BTC’s strong correlation with the S&P 500.

B. Institutionalization Reflects Maturity—not Risk

“In 2026, the market’s central question is no longer ‘Do digital assets hold value?’ but ‘What allocation weight should they command in portfolios?’ This shift marks the industry’s entry into maturity.”

The short-term volatility intensification resulting from rising institutional share is an inevitable stage in the industry’s maturation—increasing institutional ownership transforms market structure, boosts long-term capital share, and ultimately lowers overall volatility.

C. Stablecoin Growth Validates Infrastructure Value

“Stablecoins are becoming the ‘on-chain printing press’ of the dollar system—their liquidity dynamics serve as a leading indicator of market risk appetite and capital flows.”

With stablecoin supply exceeding $300 billion and monthly trading volume surpassing that of the U.S. banking network, their scale stands as proof of enduring trust in crypto infrastructure.

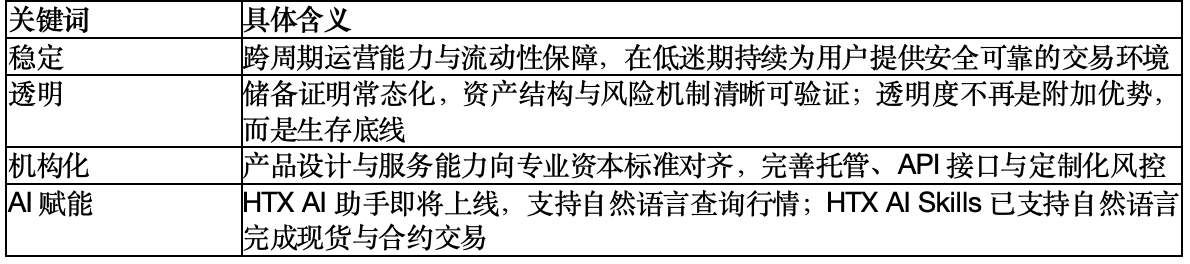

6.3 HTX’s 2026 Strategic Keywords

6.4 HTX’s Five Core Trend Forecasts

Trend One: BTC’s “Digital Gold” Status Becomes Entrenched

BTC will exist as a structural portfolio asset, with volatility converging, long-term holder share rising steadily, and pricing power shifting further toward medium- and long-term capital.

Trend Two: ETH Emerges as the Core Yield-Bearing Asset

Driven by staking rewards and DeFi protocol revenues, ETH assumes the role of a “growth-oriented yield asset” in institutional portfolios—the primary vehicle capturing value from on-chain economic activity.

Trend Three: Stablecoin Scale Hits New All-Time Highs

Stablecoins will expand beyond transaction mediums into cross-border payments and on-chain settlement—becoming the third-largest channel for dollar circulation globally (after bank deposits and U.S. Treasuries).

Trend Four: AI Agents Take Center Stage in the Next Narrative Cycle

On-chain automated execution will become the next frontier of technological competition. HTX has pioneered AI Skills and AI-native interaction interfaces—among the first major centralized exchanges to integrate AI capabilities directly into exchange functionality.

Trend Five: RWA—A Resilient Sector Amidst Downturn

Tokenization of real-world assets is accelerating. RWA market size could exceed $1 trillion before 2030—serving as the pivotal bridge linking crypto markets with traditional finance.

VII. White Paper Lens: Corroboration and Extension of Long-Term Trends

Moreover, the 2026 Digital Asset Trends White Paper provides vital corroboration and extension of the above analysis. Chapter Eight, “Key Judgments for the Next Decade,” delivers a more forward-looking, systemic perspective on the market’s structural evolution. Regarding stablecoins, the white paper explicitly states, “Stablecoins are profoundly transforming the architecture of global payments and financial systems,” and forecasts that “if stablecoins maintain their current growth trajectory, their market size could reach several trillion dollars over the next decade—potentially emerging as the third-largest channel for dollar circulation, after the U.S. bank deposit market and the U.S. Treasury market.” This aligns closely with Section IV of this report (“Stablecoins: A Bright Spot Amidst the Downturn”)—the current migration of capital into stablecoins is not merely a short-term risk-avoidance tactic, but evidence of deeper recognition of crypto infrastructure’s functional value. As market participants—including institutions—increasingly adopt stablecoins as stores of value and transaction media rather than transient safe-haven tools, stablecoins are effectively transitioning from “crypto-market accessories” to the “third pole of global dollar circulation.” On the deeper logic of institutional participation, the white paper notes, “The short-term volatility intensification caused by rising institutional share is an inevitable stage in industry maturation—increased institutional ownership will reshape market structure, boost the share of long-term capital, and drive overall volatility downward.” This provides a broader macro lens for interpreting the ETF “double-edged sword”: the short-term selling pressure induced by institutionalization is essentially the extension of traditional financial risk-management logic into the crypto sphere—a process that accelerates bubble deflation without altering the industry’s long-term trajectory. Looking ahead to the next decade, the white paper identifies “the convergence of AI and blockchain” as one of the most consequential technological trends—and predicts that “as the number of AI agents grows, they may evolve into key participants in on-chain economies, and even become primary transactors in certain contexts.” This suggests that today’s rapid rotation across AI- and meme-themed narratives may represent only the earliest phase of AI–crypto integration; as AI agents gain greater autonomy on-chain, the fundamental composition of on-chain economic actors will undergo transformation—where “traders” may no longer be exclusively human investors. On the market’s long-term direction, the white paper’s core judgment reads: “The evolution of digital assets is, in essence, a journey from technical experiment to financial-system reconstruction. Over the past decade, blockchain technology completed foundational infrastructure development; over the next decade, digital assets may gradually evolve from an emerging asset class into a cornerstone of the global financial system.” In light of this report’s analysis of the current downturn, this judgment implies that today’s market correction is both the painful process of de-bubbling and the necessary passage through which digital assets transition from “high-volatility innovative assets” to “mature financial infrastructure.” Short-term price weakness has never invalidated long-term structural trends—the “more open, efficient, and globally integrated on-chain financial network” described in the white paper may well be the destination awaiting the industry once this downturn concludes.

Sources: BlockEden, Lao Danny, Tiger Research, Messari, Delphi Digital, a16z, Coinbase Research, BeInCrypto, CoinTelegraph, HTX’s “2026 Digital Asset Trends White Paper”

About HTX

Founded in 2013, HTX has evolved over 13 years from a cryptocurrency exchange into a comprehensive blockchain business ecosystem—spanning digital asset trading, financial derivatives, research, investment, incubation, and more.

As a globally leading Web3 gateway, HTX pursues strategic pillars of global expansion, ecosystem prosperity, wealth generation, and security & compliance—delivering comprehensive, secure, and reliable value and services to cryptocurrency enthusiasts worldwide.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News