$6 billion acquisition of Cursor—SpaceX spent money it hasn’t raised yet

TechFlow Selected TechFlow Selected

$6 billion acquisition of Cursor—SpaceX spent money it hasn’t raised yet

Musk is buying goods that are rising in price with money that hasn’t even been printed yet.

Author: David, TechFlow

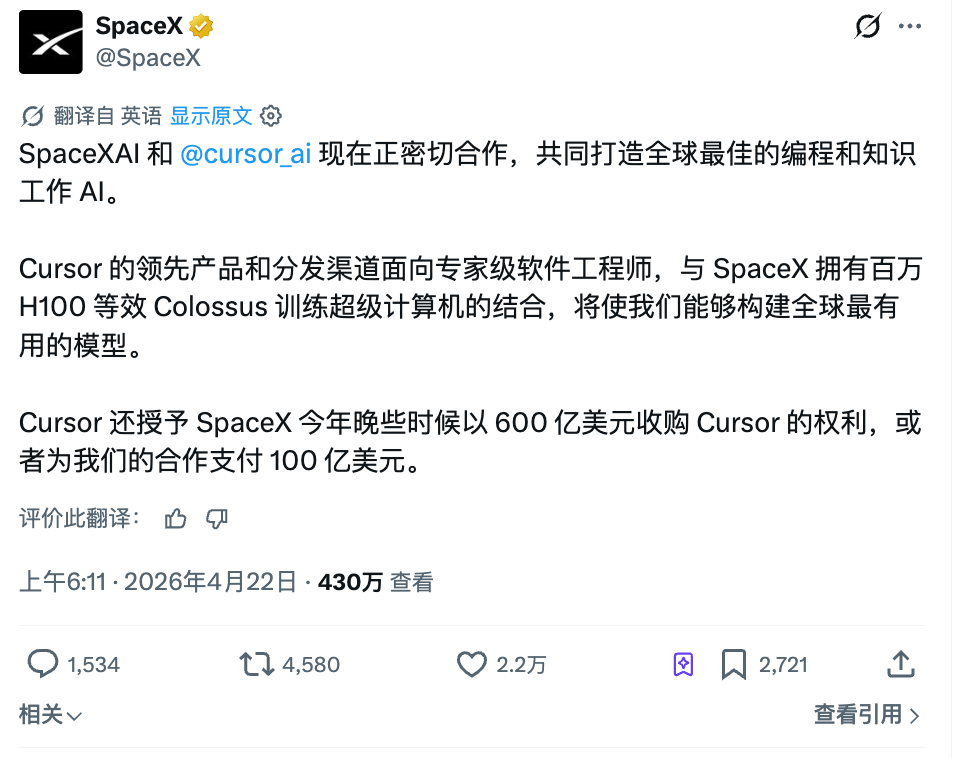

SpaceX posted an announcement on X last night revealing a partnership agreement with AI-powered coding tool Cursor.

The agreement grants SpaceX an option: later this year, it may either acquire Cursor for $60 billion—or pay a "$10 billion cooperation fee."

It’s a binary choice—but whichever path SpaceX chooses, the sum involved is enormous.

Those following the AI coding space over the past two years will recognize Cursor’s trajectory. It was once the most coveted coding tool among developers. Its annual recurring revenue (ARR) surged from $100 million at the start of last year to $1 billion by year-end—and according to Bloomberg, surpassed $2 billion as of February this year.

But the winds have shifted this year. Anthropic’s Claude Code entered the fray with $2.5 billion in annualized revenue and over 300,000 enterprise customers. OpenAI launched Codex. Microsoft even made its GitHub Copilot free.

Cursor now resembles the top performer from the previous wave of AI coding enthusiasm—yet the table has already been reshuffled for this new round.

And yet, SpaceX offered Cursor a $60 billion acquisition price tag. To put that in perspective: $60 billion exceeds Disney’s acquisition cost for 21st Century Fox—and the entire AI coding tools market is projected to reach less than $10 billion in total size by 2026, per publicly available research.

A rocket company offering six times the entire industry’s projected market size to acquire a code editor currently being overtaken by competitors?

Even the standalone $10 billion “cooperation fee” raises eyebrows. In standard M&A practice, if a deal falls through, the buyer typically pays a breakup fee—usually 1% to 3% of the agreed transaction value. At $60 billion, that would amount to $600 million–$1.8 billion.

Yet SpaceX’s announcement specifies $10 billion—a figure approaching 17% of the potential acquisition price—and labels it not a “breakup fee,” but a “cooperation fee.”

A rocket company reporting $16 billion in annual revenue (per public financial disclosures) paying more than half a year’s revenue for a “cooperation fee”—cooperating on what, exactly?

$10 Billion Buys a Call Option on an IPO

So why doesn’t SpaceX just buy Cursor outright? $60 billion isn’t astronomical for a space-focused company.

In reality, it simply can’t afford it—at least not yet.

SpaceX remains a private company. Elon Musk previously disclosed its full-year 2025 revenue as approximately $15.5 billion—and it holds no $60 billion cash reserve. That makes the “either/or” clause in this announcement particularly clever.

Either acquire Cursor for $60 billion—or pay $10 billion as a cooperation fee. SpaceX chooses. Cursor cannot refuse the acquisition nor refund the $10 billion. The decision rests entirely with SpaceX.

This structure should look familiar to finance professionals.

You pay a fee now to lock in the right to purchase something later—and decide at expiration whether or not to exercise that right. SpaceX’s $10 billion payment is, in essence, an options premium.

Such arrangements rarely appear in conventional M&A deals. You negotiate a price, sign a contract, and close. So why insist on a “decide-later” window?

The issue likely lies in timing.

SpaceX remains private. Its 2025 revenue, per Musk’s prior disclosure, stands at ~$15.5 billion—and it lacks the $60 billion in cash needed to buy anything outright. Yet multiple media outlets report SpaceX is preparing for an IPO targeting a $1.75 trillion valuation, aiming to raise $40–75 billion, with a listing as early as June this year.

Post-IPO, everything changes. A $1.75 trillion company acquiring a $60 billion firm using stock would dilute existing shareholders by just 3.4%—a barely perceptible impact.

Hence, the timing of this deal is no coincidence. First, announce the Cursor partnership—adding another slide to the IPO roadshow narrative: “We’re not just a rocket company; engineers from nearly 70% of the Fortune 500 use our tools daily to write code…”

Once the IPO closes and the share price stabilizes, execute the acquisition using stock.

This explains the $10 billion premium. With plans to raise $40–75 billion via IPO, allocating $10 billion—roughly 15% of the anticipated proceeds—to secure exclusive rights to acquire Cursor represents a strategic investment in the leading player within the AI application layer’s “vibe coding” segment.

Put differently: Musk is spending money investors are about to give him, to secure something he’ll only need to fully pay for after going public.

Only one variable stands between plan and execution: whether the IPO succeeds—and whether the $1.75 trillion valuation is achieved.

If it is, the $60 billion acquisition will be settled in stock—effectively costing almost nothing. If not, the $10 billion cash outlay becomes tuition.

The sole collateral underpinning the entire Cursor transaction? An IPO that hasn’t happened yet.

Musk’s Valuation Matryoshka

Musk has deployed this playbook before.

In March 2025, xAI acquired social platform X via an all-stock transaction. Third-party valuations placed X at roughly $33 billion—down more than half from the $44 billion Musk paid for Twitter (later renamed X) just a year earlier.

Once folded into xAI, X no longer needed to justify its standalone valuation. It became “xAI’s data source and distribution channel.”

In February 2026, SpaceX acquired xAI in another all-stock deal, with a combined valuation of $1.25 trillion—and xAI valued at $25 billion. Just months earlier, xAI’s own funding round had pegged its valuation at $8 billion. Once merged into SpaceX, xAI no longer needed to explain why it’s worth $25 billion—it became “SpaceX’s AI capability layer.”

In April 2026, SpaceX secured an option to acquire Cursor for $60 billion. If exercised, Cursor won’t need to prove its coding tool can outperform Claude Code—it will become “the application layer of SpaceX’s AI ecosystem.”

Three transactions—identical logic.

Insert a company whose standalone valuation is unsustainable—or shrinking—into a larger entity, pricing it not as an independent business but as a narrative component.

If X were to list separately, investors would ask: How does it make money? Is advertising still viable? Within a $1.75 trillion SpaceX, no one asks—because X would constitute a negligible fraction of the total valuation.

If xAI listed independently, investors would ask: How does Grok compare to ChatGPT? When will losses turn profitable? Inside SpaceX, those costs are masked by Starlink’s profits.

To this author, the maneuver resembles asset packaging: selling individual items invites line-by-line market scrutiny; bundling them requires only one unified story.

A $1.75 trillion valuation resting on rockets and satellites alone may or may not convince investors. Add xAI—now three legs. Add Cursor—four.

More legs suggest greater stability. Whether each leg can stand independently is a question only relevant *before* packaging.

Pricing a Position

Among this year’s largest AI deals, buyer valuations increasingly resemble declarations—not calculations.

When Amazon pledged another $25 billion to Anthropic, no one quizzed Anthropic’s P/E ratio. When Meta spent billions acquiring Manus—just nine months after its launch—no one demanded unit economics. Now SpaceX offers $60 billion for Cursor—six times the AI coding market’s projected annual revenue.

These prices share a defining trait: they aren’t pricing a company’s current business—they’re pricing a position. Anthropic occupies the position of “one of the strongest closed-source models.” Manus holds the position of “entry point to the AI Agent application layer.” Cursor occupies the position of “the world’s largest AI coding tool for developers.”

A position’s price bears no relation to revenue—it depends solely on how close you are to that entry point.

If SpaceX’s IPO succeeds, it will have executed a textbook maneuver: locking up a top-tier AI coding asset via a single post, an options premium, and an IPO that hasn’t yet occurred—spending zero of its own profits. If it fails, Cursor still walks away with $10 billion.

Yet the real takeaway here isn’t success or failure.

The true inflection lies in the fact that AI company valuations are no longer calculated—they’re declared. Take the $60 billion acquisition figure: no financial model could derive it.

As long as you believe AI coding is the inevitable gateway for every developer, that position must be claimed—and whoever claims it sets the price.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News