Crypto Trader’s Self-Reflection: “All My Friends Are Leaving—What’s Left to Do in This Industry?”

TechFlow Selected TechFlow Selected

Crypto Trader’s Self-Reflection: “All My Friends Are Leaving—What’s Left to Do in This Industry?”

For professionals working in the crypto space, it only makes sense to work at stablecoin fintech firms, trading platforms, or novel reverse startups.

Author: donn (@tzedonn)

Translated by TechFlow

TechFlow Intro: Only 12 projects still generate over $50 million in annual revenue. As DeFi turns into a minefield under AI-powered attacks, and on-chain gold rushers remain stuck on a battlefield that’s already ended—every crypto professional should ask themselves the same question: What can I still do here?

Many of my friends have already left—or are actively considering leaving—the crypto industry. So I’d like to share some broader reflections on the market: What remains viable in crypto today?

The core issue is that crypto is stuck across three critical dimensions: (i) a lack of innovation—nothing meaningfully new has emerged in the past 2–3 years; (ii) advances in quantum computing threaten Bitcoin’s viability by 2029; and (iii) large language models like Claude Mythos have increased attack frequency, rendering DeFi’s risk/reward profile unattractive.

This leads directly to the question: What’s left to do in crypto?

VCs and Liquidity-Token Investors

Owing to this innovation drought, the VC sector has been unusually quiet—especially in token trading. Every crypto VC will tell you how dull things have become, unless they’re running larger Series B+ rounds or funding stablecoin-payments startups.

The few top-tier VCs I’ve spoken with are investing in contrarian verticals—for example, quantum startups (e.g., Project Eleven, Oratomic) or novel concepts (e.g., Shift Foundation, PostFiat, Ambient).

I think this is perfectly normal: we’ve largely figured out what works and what infrastructure is needed, so genuinely exciting new things are increasingly rare. We’re now in the adoption phase for payments and remittances. The endgame—and institutional participation—has arrived.

Similarly, for professionals working in crypto, meaningful opportunities exist only at stablecoin fintech firms (e.g., Circle, OpenFX, Tempo, Arc, Plasma), prediction markets or derivatives platforms (e.g., Polymarket, Kalshi, Hyperliquid), or novel contrarian startups (as above). Working at an L1 foundation may pay well, but it’s a career dead end with no long-term upside.

The VC sector’s lack of “cool new things” means fewer high-quality tokens will reach the market—and less VC capital will flow into liquidity markets.

Thus, long-term liquidity-token investors who evaluate tokens based on growth, fundamentals, and value accrual now likely have fewer than 10 quality candidates—and this number seems unlikely to grow in the near term.

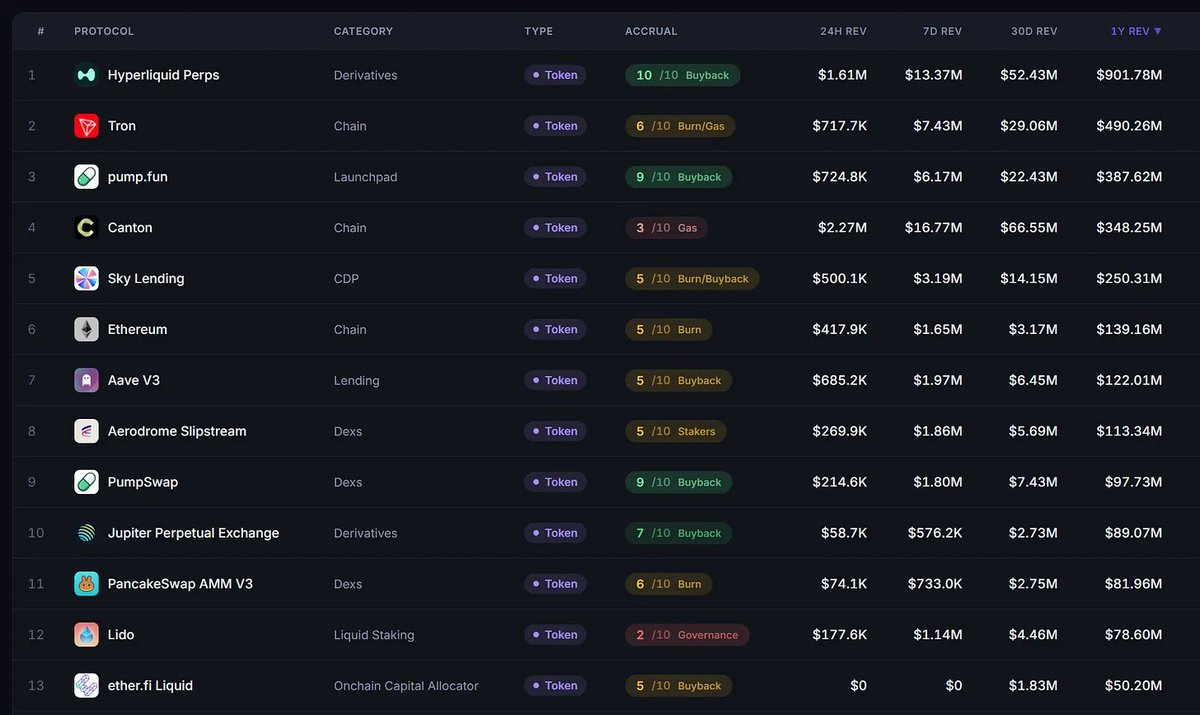

Only 12 token projects generate over $50 million in annual revenue. Of those, only three score ≥7 on value-accrual metrics (HYPE, PUMP, JUP). Even if you expand your assessment to include teams demonstrating strong growth trajectories and improving value accrual, you might add only another 5–10 tokens to the list (e.g., MORPHO, SYRUP).

The market cap of “OTHERS” has fallen from ~$450 billion to ~$180 billion, while equity markets are experiencing speculative frenzies in high-bandwidth memory, photonics, quantum computing, peptides, and more.

Subjective and Systematic Traders

You might argue crypto is primarily about narrative and momentum trading—making it ideal for discretionary traders who go long/short based on narratives or catalysts/news. That’s my domain—and the one I know best.

Deep in bear markets, catalyst-driven trading has consistently been more profitable—though many such trades demand alertness and rapid reaction. There are real edges and solid trade setups here.

Nonetheless, there have still been numerous event-driven trades over the past three months, for example…

Shorting TAO as the Templar subnet exited—dropping from $330 to $260 within five hours (April 9)… Long TAO during Chamath and Jason Cal’s endorsements (with mixed success)

No trade occurred, but notably WLD didn’t rally on the Tinder/Zoom partnership announcement—it fell 8% over two days

Shorting AAVE following the KelpDAO hack—first reported on Twitter ~1 hour after the exploit began at ~1730 UTC (April 19)

Shorting AAVE when Marc Zeller’s ACI departed (March 3)

Shorting TRUMP’s pullback after the Trump dinner announcement (March 12)

Shorting ACX back to its “conversion price” after its token-to-equity conversion announcement (March 11)

Shorting DRIFT during its exploit—down 40% within one hour (April 1)

Shorting RESOLV during its exploit—down ~10% (March 22)

Long ALGO on Google’s quantum breakthrough (March 31)

Long LDO on its buyback announcement—up ~17% over ~5 days (March 27)

Long/short pump-and-dump scams like RAVE, SIREN, STO, PIPPIN, POWER (which I prefer to avoid entirely)

Still, open interest has dropped ~60% since October 10, and market reactions to news are often muted. You must be highly selective—choosing which news to trade and whether others care—since retail interest is minimal (they’re typically the slowest to react to headlines), meaning you’re mostly competing head-to-head against other news traders.

I’m seeing more subjective traders spend increasing time on prediction markets and equities/commodities trading—Hyperliquid makes this transition far easier.

As for systematic and basis traders: traditional strategies grow less profitable as volumes and funding rates decline. To stay engaged, they’re turning to HIP-3 markets, arbitraging prediction markets, trading Pendle PT/Boros, or arbitraging new perpetual-contract DEXs (with limited liquidity).

Yield Farmers

Rising DeFi hacks have pushed yield farmers (or, institutionally, TVL traders) into hibernation—or outright exit—this year. The last decent yield opportunities were Plasma and USDai. FlyingTulip might work in a bull cycle, but launched with little fanfare.

“Yield trading” usually makes sense because you can sell governance tokens awarded as yield (as highlighted here)—but that assumes someone buys them from you. Without liquidity investors or subjective traders adding fuel, risk/reward rarely justifies the effort.

This holds true for past (OHM), present (XPL, ENA), and potential future cases (USDai’s CHIP). On-chain DeFi yield thresholds used to sit at 15–25% APY—factoring in ~0% Treasury yields and ~10–15% probability of hacks.

OHM was worth it then—not because risk was lower, but because returns were far higher.

Today, the threshold may approach 50–60% APY, given rising hack frequency ($795 million stolen from DeFi in Q1 2026 alone), added risks from Claude Mythos, and escalating quantum threats. With no buyers for newly minted tokens, achieving reasonable risk-adjusted returns is extremely difficult.

Most rational yield farmers have shifted almost entirely off-chain—even STRC’s 11.5% traditional-finance fixed-income notes offer better risk-adjusted returns (15–20%).

See: Rami poker, CBB, Sisyphus, delucinator, misaka

On-Chain Gold Rushers

Last but not least—the infamous on-chain gold rushers: those who buy at $1M market cap and sell at $100M. I believe these players persist, because the trenches remain the only place where 100x gains still occasionally emerge.

On-chain gold rushers also feel like WWII soldiers trapped in a cave—unaware the gold rush era has essentially ended.

Needless to say, meme coins peaked the moment our beloved President and First Lady launched their token. We’re nearing the euthanasia rollercoaster’s finale—things no longer rise like before, and value extractors are everywhere (“FNF Group,” “LA Vape Syndicate,” serial rug-pull factories, and exploitative trading fees).

Yet I still believe this niche won’t vanish entirely—a sliver of hope keeps people in the trenches. Over recent months, we’ve seen…

$GAS: GasTown surged from $100K to $60M market cap in 3 days (Jan 15), then crashed back to $1M in another 3 days—and now trades at $50K.

$RALPH: RalphWiggum rose from $500K to $55M in 2 weeks (Jan 21), then plunged 93% to $3M within 12 hours after developers abandoned it—and now trades at $50K.

$PENGUIN: Nietzchean Penguin hit $170M in 3 days (Jan 24), but now trades at $3M.

$MOLT peaked at $120M in one day (Jan 31), but now trades at $1M.

$WHITEWHALE reached $200M (Jan 10), but now trades at $7M.

$ASTEROID hit $200M yesterday (April 19) after Musk tweeted it could become SpaceX’s mascot—likely trending toward zero within days.

While these examples confirm occasional spikes, your odds of hitting one are probably <10%, and absolute peak upside is likely capped at a net 10x (e.g., $10M → $100M), since nothing reliably exceeds $100M anymore. And once you hit the top, you have only hours—not days—to exit, as >90% drawdowns occur within hours.

So… What Am I Doing?

I’m maintaining my arbitrage strategy on Polymarket, generating ~15% APY with a max capacity of ~$250K. Fully deployed, that earns only ~$3,500/month. Arbitrage opportunities have also declined since Polymarket introduced trading fees—and recent npm package poisoning has made me increasingly skeptical of the risk/reward (especially post-airdrop). My current plan is to shut it down post-airdrop.

I continue trading crypto—but far less actively than before. I’ve toyed with launching an AI hedge fund, but my exploration led me to conclude AI isn’t yet creative enough for discretionary trading (e.g., idea generation). However, it excels when given a task or methodology I’ve used before—and requiring modest logical reasoning.

So I’m spending time automating certain “hedge fund analyst” tasks—like automating the on-chain reconnaissance I previously performed manually for internal wallets on Polymarket. It’s highly procedural but requires light logical reasoning—exactly where Claude shines.

I’m also diving deeper into fine-tuning AI models—particularly using crypto and financial data. I’ve been reading widely outside crypto and find topics like the AI stack (social impact and full-stack equities), physical AI (world-action models, vision-language models, and data challenges), and “AI integration” (PE-style integration—but powered by AI) deeply intellectually stimulating—yet I haven’t found a problem compelling enough to dedicate my life to solving.

If you have anything interesting to discuss, feel free to reach out!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News