Bitget UEX Daily Report | U.S.-Iran Talks Reveal New Disagreements, Oil Prices Surge Again; Google in Talks with Marvell to Develop New Chips

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S.-Iran Talks Reveal New Disagreements, Oil Prices Surge Again; Google in Talks with Marvell to Develop New Chips

Overall, geopolitical risks and the AI theme will be the market’s main drivers this week. Investors are advised to monitor how negotiation developments impact volatility and position themselves in technology and AI-related stocks with diversified supply chains.

Author: Bitget

I. Top News

Federal Reserve Updates

Warsh Faces Critical Senate Confirmation Hearing

Absent any new escalation in the Iran situation, domestic U.S. attention will shift to Kevin Warsh’s Senate confirmation hearing. Originally postponed due to “document delays,” the Banking Committee hearing has now been scheduled for Tuesday, April 21.

However, a more significant obstacle than document issues may hinder Trump’s nomination of Warsh as the next Federal Reserve Chair. Warsh requires unanimous support from all Republican senators on the committee to proceed—but Senator Thom Tillis (R-NC) continues to threaten blocking the nomination unless the Department of Justice halts its investigation into current Fed Chair Jerome Powell and the White House abandons its legal efforts to remove Powell.

Given that Trump is unlikely to accept these conditions, the nomination process risks stalling—just one month before Powell’s term expires—introducing fresh uncertainty into markets. (Finance Journal)

International Commodities

U.S.-Iran Negotiations Deepen Divide; Oil Prices Surge Again Over Weekend

- Over the weekend, Trump repeatedly stated that the U.S. had proposed a “fair and reasonable” agreement, announced that the U.S. delegation arrived in Islamabad on the evening of April 20 to launch a second round of face-to-face talks, and warned that if no agreement is reached by April 22, the U.S. would destroy Iranian power plants and bridges while maintaining port blockades. Iranian media, however, exclusively clarified that reports of a “second round of negotiations” are false, emphasizing that Tehran refuses to resume talks so long as maritime blockades persist—the core disagreements remain centered on enriched uranium disposition, suspension of nuclear activities, and control over the Strait of Hormuz.

- The ceasefire agreement expires on April 22, heightening uncertainty.

- Analysts note that Friday’s market optimism about peace was extinguished over the weekend by renewed discord. Traders are preparing for Monday’s opening volatility, with oil prices likely to rebound again amid near-term geopolitical uncertainty.

Macroeconomic Policy

U.S. Customs Launches Large-Scale Tariff Refunds on April 20

- U.S. Customs and Border Protection (CBP) has completed Phase I development of its new customs declaration system and officially launched tariff refund operations on April 20. Tariffs previously imposed under the International Emergency Economic Powers Act (IEEPA) will be refunded in stages.

- This follows February’s U.S. Supreme Court ruling and March’s U.S. Court of International Trade decision, both holding that IEEPA does not authorize the President to impose broad-based tariffs.

- The move delivers tangible benefits to importers, potentially alleviating prior tariff pressures and boosting confidence in related trade sectors.

II. Market Recap

Commodities & FX Performance

- Spot Gold: Down 1.01% to ~$4,781/oz.

- Spot Silver: Down 1.69% to ~$79.45/oz.

- WTI Crude: Up 6.87% to $88.23—surging again over the weekend amid renewed U.S.-Iran negotiation tensions.

- Brent Crude: Moved closely in line with WTI, rising to $95.75.

- DXY (U.S. Dollar Index): Slightly up 0.21% to ~98.33, pressured by improved risk sentiment and geopolitical factors.

Cryptocurrency Performance

- BTC: Down 1.75% over 24 hours to ~$74,335.

- ETH: Down 2.83% over 24 hours to ~$2,282.

- Total Crypto Market Cap: Down 2.3% over 24 hours to $2.58 trillion.

- Liquidations: ~$415 million liquidated over 24 hours, including ~$337 million in long positions.

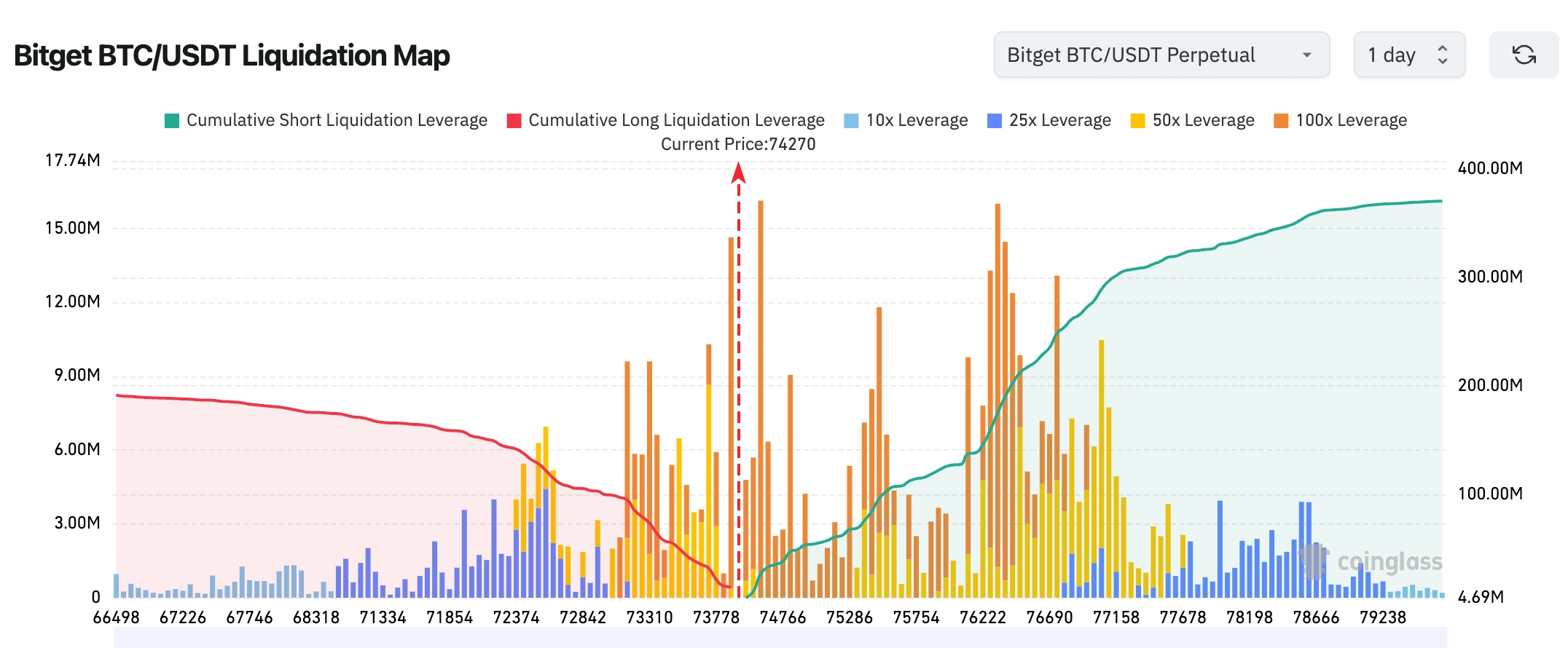

- Bitget BTC/USDT Liquidation Map: A large concentration of short positions remains clustered between $75K–$77K. A breakout above this range could trigger cascading short squeezes. Long positions have largely been liquidated and show little sign of re-entry, leaving limited liquidation-driven downside pressure in the near term—overall structure remains biased upward.

- Spot ETF Net Flows: As of last Friday’s close, BTC spot ETFs recorded net inflows of ~$664 million; ETH spot ETFs saw net inflows of ~$127 million.

- BTC Spot Flows: $1.593 billion flowed in and $1.698 billion flowed out yesterday, resulting in a net outflow of $104 million.

U.S. Equity Index Performance

As of last Friday’s close:

- Dow Jones Industrial Average: Up 1.79% to 49,447.43—extending strong gains; the small-cap Russell 2000 also hit an all-time high.

- S&P 500: Up 1.2% to 7,126.06—reaching a new record high.

- Nasdaq Composite: Up 1.52% to 24,468.48—marking 13 consecutive gains (tying the longest streak since 1992), primarily driven by tech sector catch-up rallies.

Tech Giants’ Performance

As of last Friday’s close:

- Apple (AAPL): Up 2.59% to ~$270.23—boosted by AI and consumer recovery expectations.

- Amazon (AMZN): Up 0.34% to ~$250.56—cloud business growing steadily.

- Alphabet (GOOGL): Up 1.68% to ~$341.68—positively impacted by news on chip supply chain diversification.

- Meta (META): Up 1.73% to ~$688.55—synergy between advertising and AI businesses.

- Microsoft (MSFT): Up 0.6% to ~$422.80—robust cloud service demand.

- NVIDIA (NVDA): Up 1.68% to ~$201.68—sustained high demand for AI compute.

- Tesla (TSLA): Up 3.01% to ~$400.41—drawing attention due to progress on Robotaxi and other initiatives. Key Summary: The Magnificent Seven (Mag 7) have collectively rebounded over 20% from their March lows, recovering ~$4 trillion in market value. Valuation repair combined with renewed optimism around AI commercialization is fueling the tech sector’s “catch-up rally.”

Sectoral Momentum Observations

Semiconductor / AI Chip Sector: Up >2%

- Key Stocks: NVIDIA (NVDA) +1.68%, Broadcom (AVGO) +2.03%, TSMC (TSM) +1.97%.

- Catalyst: Google and Marvell are reportedly in advanced discussions to co-develop two new AI chips—a custom memory-processing unit (to complement Google’s existing TPUs) and a new-generation TPU—with design completion and pilot production targeted for next year. This accelerates supply chain diversification and reduces reliance on single suppliers.

Fiber Optic / PCB Sector: Strong upward momentum

- Key Stock: Kinpo Group (pre-market trading launched today).

- Catalyst: Domestic fiber optic prices have surged 650% YoY; top-tier firms report order backlogs extending into Q1 2025. Supply bottlenecks in preform rods suggest continued high industry activity through end-2027.

III. In-Depth Stock Analysis

III. In-Depth Stock Analysis

1. Alphabet (GOOGL) – Negotiating Development of Two New Chips with Marvell

Event Summary: Google is in deep negotiations with Marvell Technology to jointly develop two custom AI chips: a memory-processing unit (designed to complement Google’s existing TPUs) and a next-generation TPU. Design completion and pilot production are targeted for as early as next year. Google has long championed TPUs as alternatives to NVIDIA GPUs; this collaboration aims to further reduce dependency on NVIDIA and Broadcom, accelerating supply chain diversification across AI infrastructure. TPU sales now represent a core growth engine within Google Cloud revenue. Market Interpretation: Analysts broadly view this initiative as a major step toward optimizing Google Cloud’s cost structure while reinforcing its long-term competitive edge in AI compute. In the near term, the signal of supply chain diversification has bolstered investor confidence across the entire AI hardware sector. Multiple investment banks have raised their price targets for Google, highlighting this partnership as a pivotal milestone in tech giants’ strategic shift—from reliance on single suppliers toward building autonomous, controllable ecosystems. Investment Implications: Amid sustained long-term demand for AI compute, supply chain diversification is emerging as a core competitive advantage for tech leaders. Investors should focus on upstream and downstream opportunities along related value chains—and capture structural upside generated by self-reliant innovation from industry leaders like Google.

2. Anthropic – Launches Claude Design, an AI-Powered Creative Tool

Event Summary: Anthropic officially launched its experimental design tool, Claude Design, powered by its latest flagship model, Claude Opus 4.7. Designed specifically for users without formal design training, the tool enables visual creation, product prototyping, and presentation generation via simple natural-language prompts. It represents AI’s deeper penetration into multimodal design—from text and code generation to creative visual expression. Market Interpretation: Analysts see such tools dramatically lowering creative barriers, accelerating AI adoption across design, product development, and office productivity. Several banks point out that these tools not only expand AI’s application scope but may also reshape downstream creative industry ecosystems—providing short-term valuation upside for Anthropic and its ecosystem partners. Investment Implications: As AI use cases continue to broaden, downstream tooling products are driving ecosystem expansion. Investors should monitor how multimodal AI tools drive higher adoption rates across industries.

3. MicroStrategy (MSTR) – Surging Bitcoin Holdings Drive Sharp Stock Rally

Event Summary: As the world’s largest corporate holder of bitcoin, MicroStrategy’s stock surged ~12% on Friday, and rose another ~2.6% today alongside BTC’s gain—keeping its strategic bitcoin accumulation in the spotlight. In early April, the company added to its holdings via equity offerings and other means, bringing its total bitcoin position to ~780,000 BTC, acquired at an average cost of ~$75,600 per coin. Recent BTC price appreciation has further lifted its asset valuation. Market Interpretation: Institutions widely treat MSTR as a leveraged bitcoin investment vehicle. Analysts have recently upgraded price targets en masse, recognizing its unique positioning in the crypto bull market. With continued inflows into bitcoin ETFs and broader adoption of corporate reserve strategies, MSTR’s “Bitcoin Standard” framework is gaining wider recognition—its valuation anchor poised to rise in tandem with BTC’s price and its own holdings. Investment Implications: Bitcoin-related equities exhibit high correlation with mainstream crypto assets. MSTR offers potential for outsized returns during periods of BTC consolidation at elevated levels. Investors may consider it a volatility amplifier for crypto market exposure.

4. SanDisk (SNDK) – Successfully Added to Nasdaq-100 Index

Event Summary: SanDisk (SNDK.US) was officially added to the Nasdaq-100 Index before market open on April 20, replacing Atlassian. This inclusion will directly attract substantial passive fund and ETF inflows, supporting strong share performance. Market Interpretation: Index rebalancing typically triggers significant capital flows. Analysts believe inclusion will meaningfully enhance liquidity and elevate the stock’s valuation benchmark. Combined with robust AI-driven storage demand, Citigroup, Jefferies, and others have raised their price targets to the $980–$1,000 range, underscoring long-term tailwinds from AI server requirements for high-bandwidth memory. Investment Implications: Nasdaq-100 membership provides a near-term catalyst. Investors should monitor ongoing passive inflows as a source of sustained price support—especially during the AI compute expansion cycle.

IV. Cryptocurrency Project Updates

1. On-chain analysts suggest the rsETH incident may impact Aave more severely than initially anticipated. Since the incident occurred early yesterday morning, funds have continuously flowed out of Aave—total deposits falling from $45.8 billion to $35.7 billion, a $10.1 billion outflow, of which $4.5 billion were stablecoins. This has kept Aave’s stablecoin deposit rate at 13.4% for an entire day. Earlier reports indicated that Kelp DAO’s rsETH cross-chain bridge was compromised.

2. According to Cointelegraph, heightened Middle East tensions have pushed bitcoin’s price down to ~$75,000. Markets fear escalating U.S.-Iran conflict—and possible closure of the Strait of Hormuz—reigniting concerns over oil price spikes and significantly increasing macro uncertainty. Data shows bitcoin briefly touched a near-10-week high of $78,400 before retreating under pressure. Analysts observe that geopolitical events and oil price volatility are currently dominating short-term shifts in risk sentiment.

Over the past 24 hours, ~$260 million in crypto positions were liquidated, with long positions bearing pronounced pressure. Meanwhile, bitcoin continues to stall near a key technical level—the 21-week moving average—suggesting near-term downward pressure. Market participants note that in this highly sentiment-sensitive environment, any unexpected news could rapidly reverse market direction—potentially intensifying short-term volatility.

3. Nomura Securities’ latest survey reveals persistent institutional interest in crypto assets: 65% of respondents identify them as portfolio diversification tools. The survey covered over 500 Japanese investment professionals.

4. Tokens including ZRO, H, and XPL face large token unlocks this week, with ZRO’s unlock valued at ~$40.4 million.

V. Today’s Market Calendar

Data Release Schedule

Key Event Preview

- Second Round of U.S.-Iran Talks: U.S. delegation arrives in Islamabad on April 20; key topics include enriched uranium disposition and Strait of Hormuz control—April 22 marks the critical deadline.

Institutional Views:

Multiple investment bank analysts note that the weekend’s U.S.-Iran negotiation rift threatens to unwind Friday’s “peace hope”-driven market rally. Near-term oil price uncertainty will support commodity prices—but the tech sector’s “catch-up” thesis remains solid: the Mag 7 have recovered $4 trillion in market cap, buoyed by revived AI commercialization expectations and 19% earnings growth. Institutions continue to favor the tech sector. Under dollar index pressure, gold and silver remain elevated, while crypto assets experience short-term pullbacks—diverging somewhat from broader risk assets—yet BTC/ETH ETF inflows remain robust. Overall, geopolitical risk and AI themes will dominate this week’s market narrative. Investors should monitor negotiation developments for volatility implications—and position for tech and AI-related stocks benefiting from supply chain diversification.

Disclaimer: The above content was compiled via AI search and verified manually for publication only—not intended as investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News