From Utopian Narratives to Financial Infrastructure: The “Demystification” and Pivot of Crypto VCs

TechFlow Selected TechFlow Selected

From Utopian Narratives to Financial Infrastructure: The “Demystification” and Pivot of Crypto VCs

Financial infrastructure is the true reason venture capital invests in the crypto space.

By Suvashree Ghosh and Matt Haldane

Translated by Saoirse, Foresight News

Not long ago, the crypto industry was chanting “blockchain, not Bitcoin,” proclaiming that distributed ledger technology would transcend finance and fundamentally reshape the internet. Yet recent funding trends suggest that, in the real world, cash remains king.

Since the Web3 and NFT boom faded in the early 2020s, investor enthusiasm for the crypto sector has noticeably cooled. However, one niche has bucked the trend, attracting growing venture capital—stablecoin payments.

Stripe’s $1.1 billion acquisition of Bridge last year signaled early interest from traditional financial institutions in stablecoin-based payments. Since then, startups including ARQ, KAST, and RedotPay have raised new funding rounds to build cross-border payment rails and stablecoin-native financial services. Mastercard’s recent $1.8 billion acquisition of BVNK further underscores strong market interest in this space.

“Startups focused on stablecoins are arguably the hottest area for VC funding right now,” said Rob Hadick, General Partner at Dragonfly Capital. “Stablecoins have effectively decoupled from the broader crypto ecosystem and emerged as one of the few truly breakthrough applications with widespread real-world adoption.”

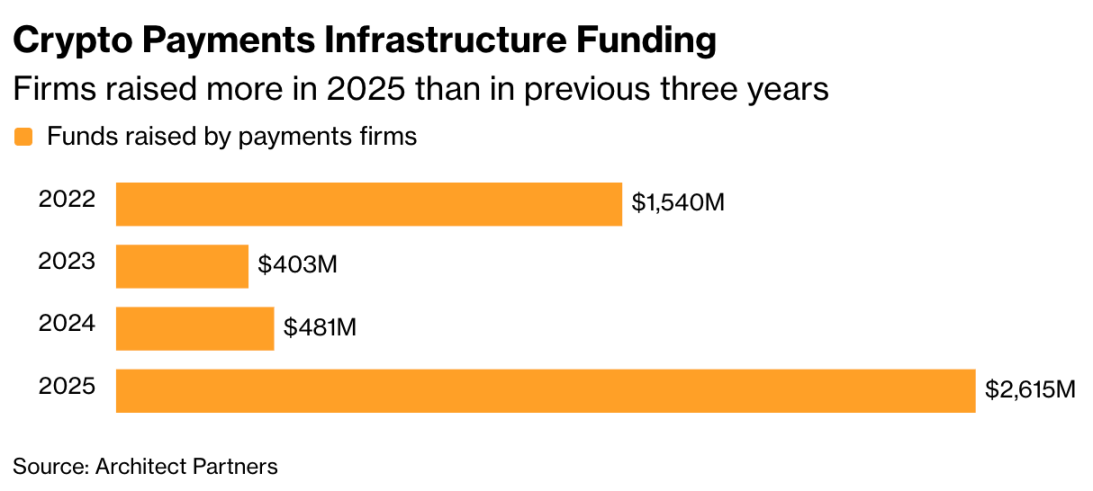

According to Architect Partners’ annual crypto funding report, total funding for crypto payment companies surged to $2.6 billion in 2025—exceeding the combined total for the previous three years. Fueled by Mastercard’s acquisition of BVNK, this figure is expected to rise further this year.

Crypto Payment Infrastructure Funding: 2025 Funding Totals for Individual Companies Exceeded the Sum of the Previous Three Years

Meanwhile, overall private funding for crypto companies rose from nearly $13 billion in 2024 to $20.4 billion in 2025—still below the $27.6 billion peak recorded in 2022.

Total Funding for Crypto Companies: The Number of Crypto Funding Deals Rose Last Year, Though It Has Not Yet Reached the 2022 Peak

Today, the two largest recipients of private capital are “investment and trading infrastructure” and “brokerage and exchange” businesses—both squarely financial in nature. Payment infrastructure ranks third. In stark contrast, blockchain gaming—the core of the Web3 and NFT boom—has vanished as a standalone category in funding reports, having dropped from $3.76 billion (roughly 14% of total funding) in 2022 to zero representation in 2025.

In fact, decentralized applications (“Web3 functional layers”) collectively raised $5.2 billion in 2022; by 2025, only consumer-facing dApps remain tracked in the report—and their funding totaled just $864 million.

Funding by Crypto Subsector: Payments Has Joined the Top Three Subsectors Attracting Funding in 2025

Stablecoins are building out more robust financial infrastructure on blockchains. Typically pegged 1:1 to the U.S. dollar, their value is anchored to underlying assets. Under the pro-crypto policies of the Trump administration, market enthusiasm for stablecoins reached unprecedented heights last year.

According to Artemis Analytics, total stablecoin transaction volume surged 72% in 2025 to $33 trillion. The two largest stablecoins today are Tether’s USDT and Circle’s USDC.

Circle’s stock posted its largest-ever single-day decline on Tuesday as investors assess potential regulatory shifts in the U.S. stablecoin landscape and intensifying industry competition. Yet the core appeal of stablecoins remains clear: moving money as efficiently as possible.

Cross-border payments remain slow, expensive, and highly capital-intensive. Despite decades of fintech advancement, cross-border transfers still rely heavily on pre-funded accounts held across multiple jurisdictions.

“Stablecoins have completely transformed this paradigm,” said Prajit Nanu, Co-Founder and CEO of cross-border payments firm Nium. “They enable real-time global value transfer without commensurate losses in capital efficiency—precisely why investors view them as foundational infrastructure for next-generation payments.”

The industry still contends with powerful “gatekeepers.” Major payment networks like Visa and Mastercard control access to point-of-sale terminals. As Eric F. Risley, Founder and Managing Partner of Architect Partners, wrote in his report, distribution channel challenges “haunt every stablecoin and payments-related company.”

Binance Spot Trading Market Share Trend

As of February this year, Binance’s share of Bitcoin spot trading volume had fallen to 27%(figures may vary depending on methodology), while its share across all cryptocurrencies declined from 52% to 32%. Its most profitable derivatives business also saw a sharp drop, falling to 34% market share.

Franklin Templeton and Ondo Finance have jointly launched tokenized ETF products, tradable around the clock via crypto wallets—bypassing decades-old reliance on brokerage accounts and time-limited trading windows for fund investments.

Industry Voices

“The irony of holding this event in Las Vegas is almost overwhelming,” said Ben Johnson, Head of Client Solutions at Morningstar. “This industry has crossed the line between investing and gambling—irreversibly and without recourse.”

ETFs, originally designed to simplify investing, have become vehicles for America’s newest form of financial gambling. Bloomberg Intelligence data shows that 36% of the 1,000 new funds launched last year were either leveraged products or crypto-related funds.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News