Founder of Delphi Labs: Two Weeks Immersed in China’s AI Scene—Shenzhen’s Hardware Left Me in Awe, While Software Valuations Scared Me

TechFlow Selected TechFlow Selected

Founder of Delphi Labs: Two Weeks Immersed in China’s AI Scene—Shenzhen’s Hardware Left Me in Awe, While Software Valuations Scared Me

Observations of Chinese founders overturned his previous understanding.

Author: José Maria Macedo, Co-founder of Delphi Labs

Translated by TechFlow

TechFlow Intro: A co-founder of Delphi Labs spent two intensive weeks touring China’s AI ecosystem, meeting numerous founders, investors, and CEOs of publicly listed companies.

His conclusions were unexpected: greater optimism about hardware than anticipated, deeper pessimism about software, and a set of observations about Chinese founders that overturned his prior assumptions.

The article also touches on valuation bubbles, the humanoid robotics sector, and information asymmetry between East and West.

Full Text Below:

I spent two weeks in China meeting a wide range of founders, VCs, and CEOs of publicly listed companies across the AI ecosystem. Before arriving, I was bullish—expecting to encounter world-class AI talent operating at valuations far below those in the West.

When I left, my view had shifted—becoming more specific: hardware proved stronger than I’d anticipated; software weaker; and several observations about Chinese founders surprised me.

The Founder Question

An enduring trait among the exceptional founders I’ve backed is independent thinking—rebelliousness, extreme focus, and unwavering conviction. They don’t follow orders. They keep asking “Why?” and reject secondhand wisdom. Their decisions often seem baffling to outsiders—but feel entirely natural to them. They possess an internal, irrepressible intensity, usually manifesting as long-term obsession and exceptional execution. As a VC who meets countless brilliant people daily, you spot these individuals instantly—their life trajectories carry a distinct “sharpness.”

Many founders I met in China were a different type—and that surprised me.

They are exceptionally accomplished—top-tier university degrees, stints at ByteDance or DJI, papers in Nature, multiple patents. In the West, such achievements mark only the absolute elite of technical talent; in China, they’re merely the entry ticket. They also outwork nearly everyone I’ve ever met—we held meetings across all hours, including weekends, and even flew between cities for back-to-back sessions. One founder came to meet us on the day his wife gave birth.

Yet independent thinking, rebellious spirit, and true 0-to-1 vision remain harder to find. Founders’ backgrounds are highly homogenous; pitch decks lean conservative; many ideas amount to impressive upgrades of existing products (“V2”), not genuinely original bets. Given the sheer scale of technical talent China produces, I’d expected far more people arriving with ideas I’d never heard before.

My interpretation: China’s education system excels at cultivating excellence—but leaves insufficient room for deviation. It produces top-tier executors adept at solving known problems—not people who show up with problems no one else even knew existed.

VCs Reinforce This Pattern

More intriguingly, local investors are amplifying this trend.

Most Chinese funds anchor their investment logic on a single premise: backing the very best people from ByteDance or DJI. They scrutinize resumes—not edge; background—not belief. Even the VCs themselves mirror this pattern—exiting from large corporations, consulting firms, or investment banks, much like European VCs did a decade ago.

The irony? Historically, China’s truly great company-builders rarely worked at large firms. Jack Ma was an English teacher who failed the college entrance exam twice before getting in. Ren Zhengfei founded Huawei at age 43 after serving in the military. Liu Qiangdong began by selling goods from a stall in a rural market. Wang Xing dropped out of his PhD program to start his first venture. More recently, Liang Wenfeng, founder of DeepSeek, has never held a job outside his own company. These people are outliers—those without “standard resumes”—precisely the ones today’s investment system is built to miss.

Finding such founders offers genuine alpha—but few seem to be looking there right now.

Shenzhen and the Hardware Ecosystem

The most astonishing thing I saw in China wasn’t any startup pitch.

It was Shenzhen’s underground hardware workshops—engineers systematically acquiring Western high-end products, disassembling them component by component, and rigorously reverse-engineering everything. When I walked away, I genuinely wasn’t sure whether most Western hardware founders understood what they were up against. Here, network effects aren’t theoretical—they’re physical, dense, and the product of decades of accumulation.

Founders we met confirmed this with data: over 70% of hardware R&D investment originates from the Greater Bay Area—and nearly 100% comes from within China—meaning iteration cycles are simply unmatchable by Western hardware firms.

Most founders we met adopt DJI’s playbook: dominating a niche consumer hardware segment—electric wheelchairs, robotic lawn mowers, next-gen fitness equipment—scaling revenue into the $80–90 million range, then leveraging either customer bases or core technologies to expand into adjacent categories. Some of these companies are already far larger than you might imagine. The strongest company I encountered was Bambu Lab—a 3D printing firm most Westerners have never heard of—reportedly generating $500 million in annual profit, doubling every year.

Bearish on Chinese Software

When I left, my skepticism about China’s software opportunity ran deeper than when I arrived.

At the model layer, China’s open-source contributions are indeed strong—but its closed-source models still lag noticeably behind the West’s best, and that gap may be widening. Capital expenditure disparities are massive. GPU access remains constrained. Western labs are increasingly cracking down on distillation. Revenue figures tell the full story: Anthropic reportedly hit $6 billion ARR in February alone. China’s top model companies operate in the tens of millions of dollars ARR range.

On the software startup side, the prevailing profile is PMs and researchers from ByteDance building agentic or ambient consumer software for Western markets. Talent is strong—but many of these products sit squarely within functional domains that major labs will natively ship—rendering them obsolete with a single release. What shocked me further: China lacks large, fast-growing private software companies. In the West, beyond model companies, a cohort of startups is already achieving nine- or even ten-digit ARR—with explosive growth rates—Cursor, Loveable, ElevenLabs, Harvey, Glean. At this tier, breakthrough private software companies are virtually nonexistent in China—rare exceptions like HeyGen, Manus, and GenSpark have all relocated overseas after gaining traction.

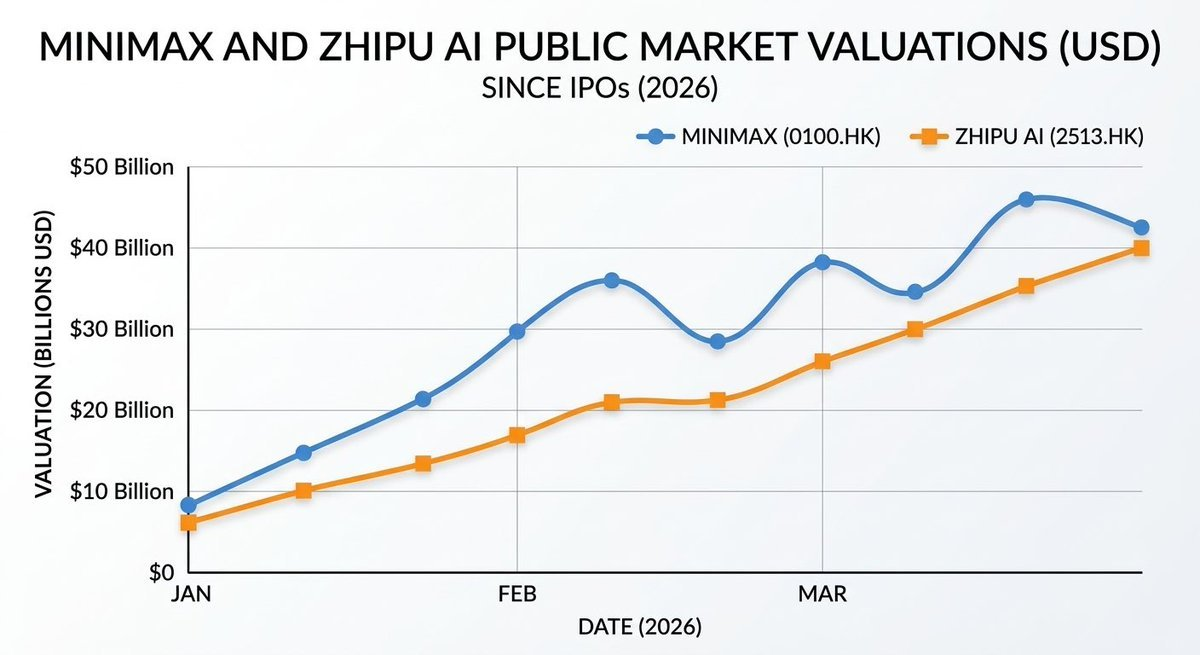

Valuation Bubbles

Despite the soft software landscape, bubbles are very real—at both early and late stages.

Early-stage: Top talent from ByteDance, DeepSeek, and Moonshot really *is* cheaper than their U.S. peers—but median valuations have already converged. Consumer startups with no product routinely command $100–200 million valuations. Pre-seed rounds exceeding $30 million are no longer unusual.

Late-stage numbers are even harder to justify. MiniMax trades publicly at ~$40 billion on under $100 million ARR—roughly 400x revenue. Zhipu trades at ~$25 billion on $50 million ARR. For comparison: OpenAI’s highest-valuation round priced at ~66x ARR; Anthropic’s at ~61x.

Private model companies like Moonshot use these public-market comparables to raise capital—jumping from $6 billion to $10 billion to $18 billion in just months. Crypto veterans will recognize this playbook: investors compare private valuations against “pre-unlock” public prices. Moreover, Zhipu and MiniMax sustain these valuations partly because they remain the only accessible proxies for “China AI narrative” exposure—a premium in itself. But as more companies list, that premium will dilute. Finally, IPO windows have one defining feature—they close abruptly, with zero warning. No one can guarantee you’ll exit your arbitrage before those benchmark prices shift.

The humanoid robotics sector mirrors this dynamic. China hosts roughly 200 humanoid robotics companies; about 20 have raised over $100 million; several now boast multi-billion-dollar valuations—nearly all with zero revenue, and most targeting Hong Kong IPOs in 2026 or 2027. If this market is real, China’s hardware advantage makes the long-term landscape fairly clear. But commercialization may arrive far slower than current funding rhythms suggest—and I doubt Hong Kong’s market can absorb dozens of multi-billion-dollar humanoid robotics firms lined up for IPOs. I’m staying away—for now.

Figure: Couldn’t resist sharing this video of a humanoid robot performing a front flip

Noteworthy Information Asymmetry

One thing caught me off guard: nearly every founder I met prioritized global markets *before* tackling China. They use Claude Code, listen to Dwarkesh’s podcast, and know San Francisco’s startup ecosystem inside out—often better than Western investors who haven’t kept close tabs.

Western hostility toward China clearly exceeds China’s toward the West. Chinese founders see no contradiction in combining China’s engineering execution and hardware depth with Western go-to-market savvy and product thinking. When this fusion crystallizes within the right founding team, truly extraordinary companies emerge.

Finding those founders—those who defy the “standard resume template” optimized by local VC systems—is exactly what we’re doing now.

Special thanks to @woutergort for opening his exceptional China network, @PonderingDurian for organizing this trip, and Claude for patiently editing my in-flight ramblings.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News