Goldman Sachs warns: AI boom may repeat 1999 internet bubble, five warning signs worth noting

TechFlow Selected TechFlow Selected

Goldman Sachs warns: AI boom may repeat 1999 internet bubble, five warning signs worth noting

While the entire market is celebrating the future of AI, Goldman Sachs strategists are sounding the alarm.

Author: Jinshi Data

The market is now concerned that echoes of 1999 are reappearing in the U.S. tech stock sector. Despite intense debate over whether AI is a bubble, history offers some signals revealing exactly what investors should watch.

Goldman Sachs strategists say they believe the market's AI frenzy faces growing risks of repeating the early-2000s dot-com crash.

Dominic Wilson, senior advisor to the firm’s global markets research team, and macro research strategist Vickie Chang wrote in a report to clients on Sunday that U.S. equities don't yet appear to be at the 1999 stage. However, they noted that the risk of the current AI boom increasingly resembling the early-2000s mania is rising.

"We see increasing risks that imbalances accumulated in the 1990s will become more apparent as the AI investment boom continues. Recently, we’ve seen some echoes of the turning point of the 1990s boom," the bank said, adding that current AI-related trading resembles tech stocks in 1997—several years before the bubble burst.

Wilson and Chang highlighted several warning signs that appeared before the early-2000s internet bubble burst, which investors should monitor closely.

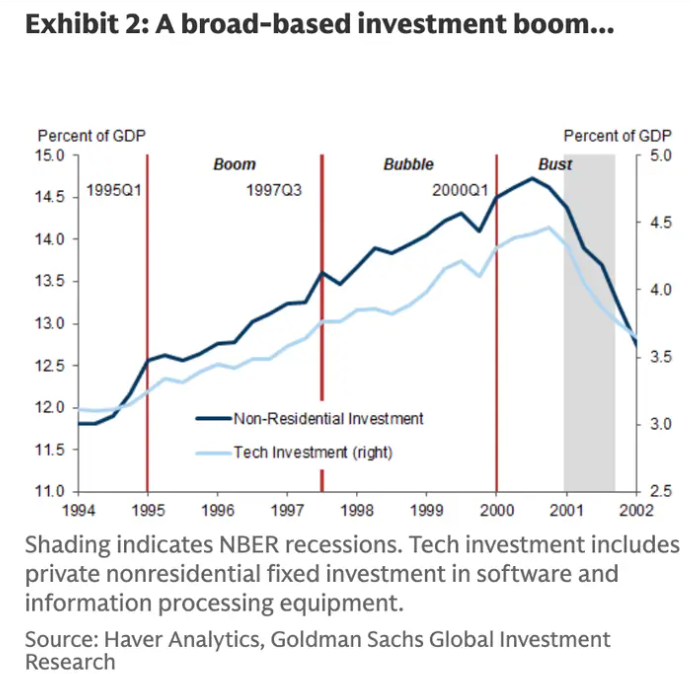

1. Investment spending peaks

In the 1990s, investment spending on technology equipment and software rose to "unusually high levels," peaking in 2000 when non-residential investment in telecom and tech sectors accounted for about 15% of U.S. GDP.

According to Goldman Sachs' analysis, investment spending began declining in the months leading up to the dot-com collapse.

"Thus, high asset valuations had a significant impact on real spending decisions," the strategists said.

This year, investors have grown increasingly wary of massive spending by large tech companies on AI. Amazon, Meta, Microsoft, Alphabet, and Apple are expected to spend approximately $349 billion on capital expenditures in 2025.

Goldman says tech investment peaked in the early 2000s, coinciding with the start of the internet stock bubble burst

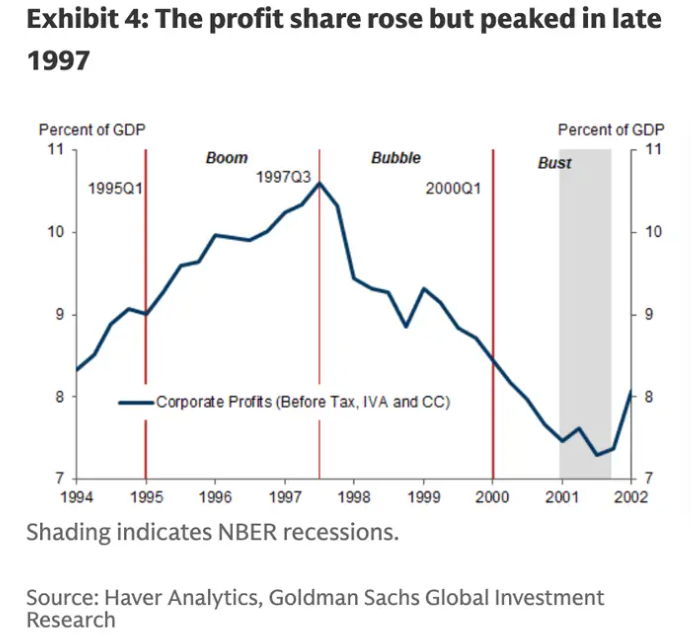

2. Corporate profits begin to decline

Corporate profits peaked around 1997, then started to decline.

"Profitability peaked long before the boom ended," Wilson and Chang wrote. "While reported profit margins remain strong, during the late stages of the boom, weakening profitability in macro data occurred alongside accelerating stock price gains."

Currently, corporate profits remain strong. According to FactSet, the blended net profit margin for the S&P 500 in Q3 was approximately 13.1%, above the five-year average of 12.1%.

Corporate profits peaked at the end of 1997, several years before the bubble burst

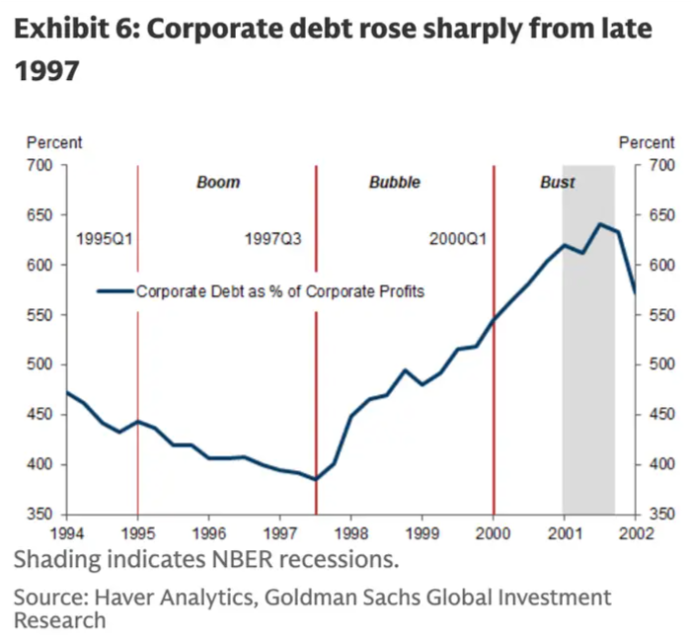

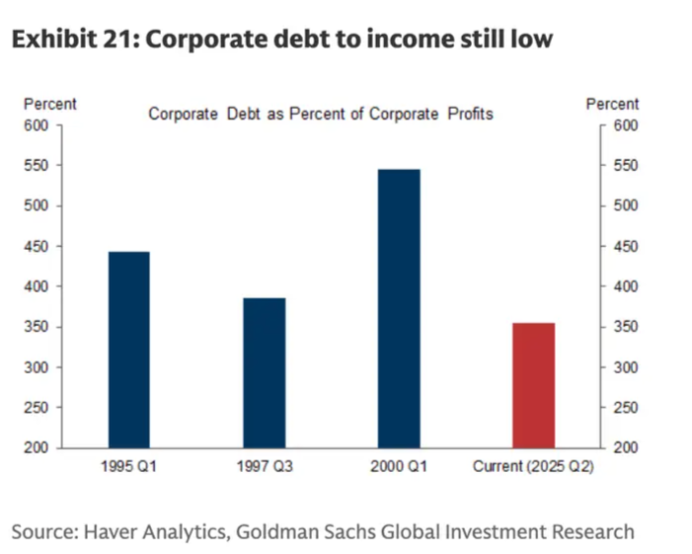

3. Rapid increase in corporate debt

The ratio of company debt to profits peaked in 2001

Prior to the dot-com crash, corporate leverage steadily increased. Goldman Sachs’ analysis shows that the percentage of corporate debt relative to profits peaked in 2001, precisely when the bubble burst.

"The combination of rising investment and falling profitability pushed the corporate sector's financial balance—the difference between saving and investment—into deficit," the strategists said.

Some large tech firms are financing part of their AI spending through debt. For example, Meta issued $30 billion in bonds in late October to boost its AI spending plans.

However, Goldman added that most companies today appear to be funding capital expenditures with free cash flow. The ratio of corporate debt to profits is also far below peak levels seen during the dot-com bubble.

Compared to 2000, the ratio of corporate debt to profits looks low

4. Fed rate cuts

In the late 1990s, the Federal Reserve was in a rate-cutting cycle, one of the factors fueling the stock rally. Goldman wrote, "Lower interest rates and capital inflows added fuel to the equity market fire."

The Fed cut rates by 25 basis points at its October policy meeting. According to CME Group's FedWatch tool, investors expect another 25-basis-point rate cut in December.

Other market professionals, such as Ray Dalio, have also warned that the Fed's easing cycle could inflate market bubbles.

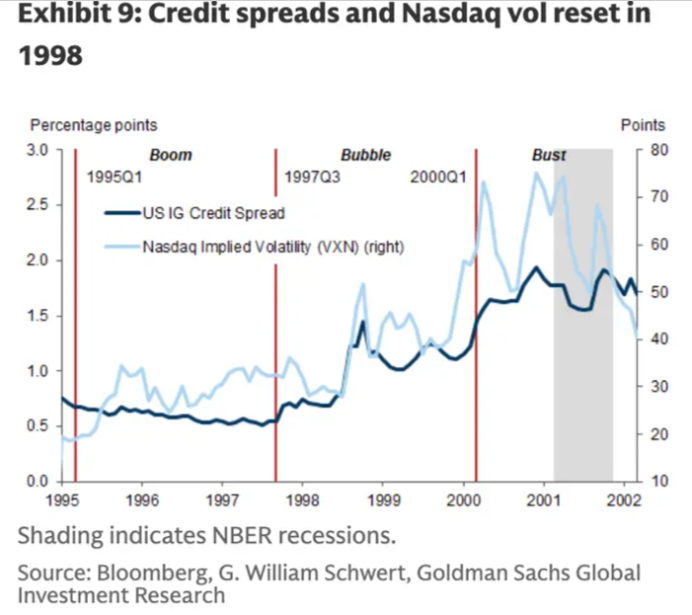

5. Widening credit spreads

Credit spreads widened in the early 2000s

The bank noted that credit spreads widened before the dot-com bubble burst.

Credit spreads—the difference between the yield paid on bonds or credit instruments and benchmark rates like U.S. Treasuries—widen when investors perceive higher risk and demand greater compensation.

Credit spreads remain historically low but have begun widening in recent weeks. The ICE BofA U.S. High Yield Index Option-Adjusted Spread rose to about 3.15% last week, up 39 basis points from a low of 2.76% at the end of October.

Wilson and Chang said these warning signs emerged at least two years before the actual burst of the 1990s internet bubble, and they added that they still believe there is room for AI-related trades to rise.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News