First-time token sale, delisting, coin stocks are no longer crypto貔貅

TechFlow Selected TechFlow Selected

First-time token sale, delisting, coin stocks are no longer crypto貔貅

DAT mode still carries risks and should be approached with caution.

Author: kkk,律动

If the previous cycle was ignited by MicroStrategy's embrace of Bitcoin, then the driving force behind this market upswing is undoubtedly the "altcoin microstrategy." Companies like SBET and BMNR building Ethereum treasuries have not only pushed ETH’s price from $1,800 in early May to as high as $4,700—an increase exceeding 160%—but also emerged as new leaders shaping market sentiment. Meanwhile, major altcoins such as SOL, BNB, and HYPE have followed suit, spawning a wave of companies centered on treasury accumulation narratives, further amplifying market expectations for continued gains.

However, as this model spreads, risk signals are beginning to emerge. Recently, Wint, the BNB treasury company, faced delisting risks, while LGHL, the Hype treasury company, became embroiled in controversy over token sales, triggering market skepticism about the sustainability of the "treasury strategy." What hidden risks lie beneath this buy-heavy approach? And what underlying concerns should investors be mindful of when chasing high returns? This article provides an in-depth analysis.

Corporate Competition: Capital Only Backs a Few Winners

The race among "treasury companies" resembles a cutthroat market elimination game.

Windtree Therapeutics (WINT) made headlines in July announcing its strategic BNB reserve, but due to weak fundamentals and persistently declining stock prices, it received a Nasdaq delisting notice on August 19. After the news broke, WINT's share price plummeted consecutively, crashing 77.21% in a single day. It now trades at just $0.13, down 91.7% from its post-announcement peak of $1.58. For a small biopharmaceutical firm already in clinical stages without commercialization and with widening quarterly losses, delisting practically means complete market marginalization.

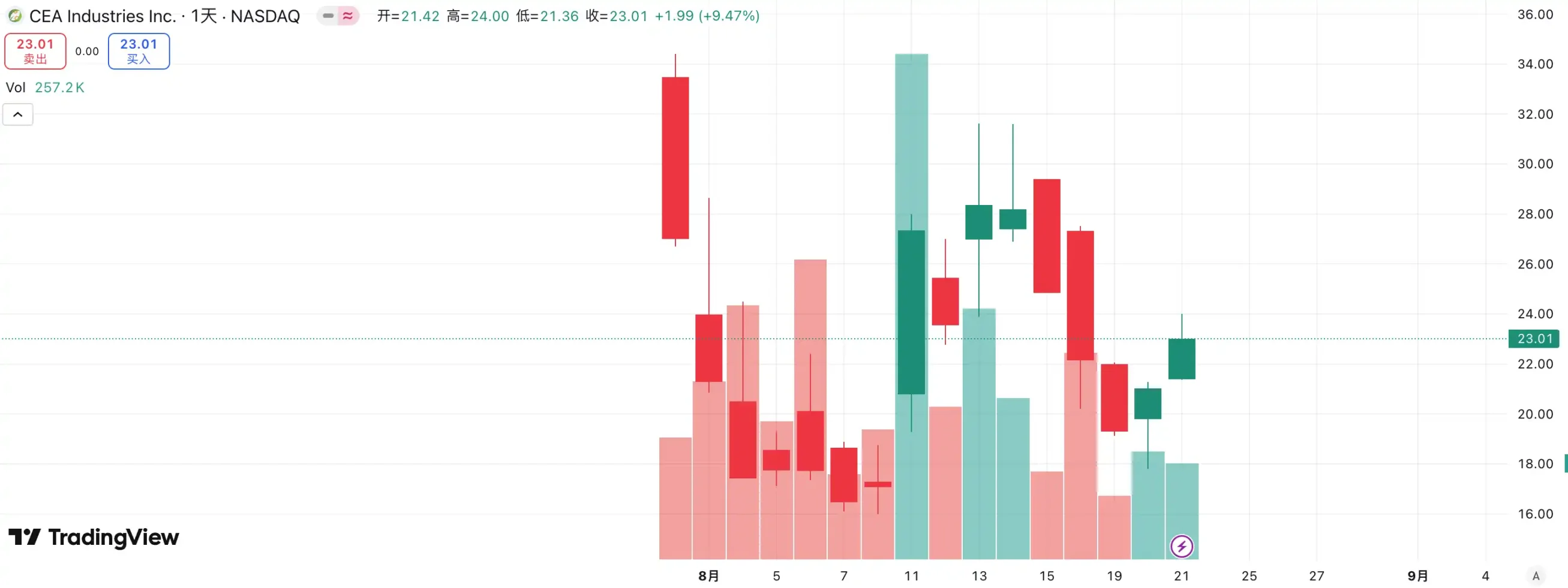

In stark contrast stands a rising newcomer—BNB Network Company (BNC, formerly CEA Industries). Backed by YZi Labs, BNC secured a $500 million private placement between late July and early August, with CZ personally involved and 140 investment firms participating, including top-tier names like Pantera Capital, Arrington Capital, and GSR. The company appointed David Namdar, former co-founder of Galaxy Digital, as CEO, and Russell Read, ex-Chief Investment Officer of CalPERS (California Public Employees' Retirement System), to lead investment decisions—transforming overnight from a small-cap traditional stock into the "official BNB treasury company."

Capital has already delivered its verdict: WINT has become a "discard," while BNC emerges as the new market standard-bearer. Data shows BNC's stock rose 9.47% yesterday, currently trading at $23.01, reinforcing its leading position in the "BNB treasury company" space. This competition is not merely about fundamentals—it's a market vote on narrative strength and resource integration.

The race among ETH treasury companies is equally fierce. SBET, led by Joseph Lubin, was the first publicly traded company to promote the "ETH microstrategy" concept. Leveraging first-mover advantage and positioning itself as an ETH ambassador, it triggered massive FOMO early in the cycle, surging from $3 to over $120, becoming a benchmark case for the altcoin treasury model.

Yet BMNR's rise quickly reshaped the landscape. As a latecomer, it outpaced SBET in both purchase scale and funding size, boldly declaring its goal to hold 5% of all ETH, instantly elevating market imagination. More crucially, BMNR enjoys strong public backing from Wall Street veterans like Tom Lee and Cathie Wood, giving it dominant influence across institutional and media channels. In contrast, despite Joseph Lubin’s endorsement representing Web3 elite credibility, SBET clearly lags behind BMNR—backed by Wall Street “old money”—in terms of discourse power and impact.

This divergence is reflected in their stock performance. During August’s rally, SBET climbed from $17 to a high of $25—a roughly 50% gain—while BMNR surged from $30 to $70, exceeding a 130% increase, significantly outperforming SBET. As BMNR gradually gains recognition from mainstream capital and opinion leaders, the competitive dynamics among ETH treasury companies are clearly shifting.

The key takeaway is that the "treasury company"赛道 has entered a phase where the strong get stronger. With institutional investors and major capital players entering the arena, market resources are rapidly concentrating around a select few firms possessing capital integration capability, narrative momentum, and sound governance. Small companies struggle to survive under this model; even if they adopt the "treasury" label, they often fail to withstand market scrutiny on earnings and financial strength. Ultimately, only a handful of true winners capable of sustaining capital inflows and compelling narratives will remain, while bubbles and copycats will be swiftly eliminated.

Selling Risks: Strategic Reserves Don’t Mean Permanent Holding

If Bitcoin’s bull run benefits from Michael Saylor’s ideological conviction, the "altcoin treasury bull" appears far more pragmatic. Saylor consistently declares that MicroStrategy will "never sell" its Bitcoin holdings, continuously raising funds to buy more BTC, fueling steady demand and confidence. Still, whether MicroStrategy might eventually sell remains a constant topic of debate. Altcoin treasury companies may mimic the model, but none have committed to never selling—leaving markets inherently more uncertain about their stability.

Recently, Lion Group Holding Ltd., the HYPE treasury company, was detected selling $500,000 worth of HYPE tokens. Just one month earlier, the company announced launching its HYPE treasury strategy following a $600 million fundraising round, aiming to position $HYPE as a core reserve asset and build a next-gen Layer-1 treasury portfolio including $SOL and $SUI, explicitly stating future plans to continue accumulating these assets. Yet this recent reduction raises speculation about its allocation logic: Is this a tactical diversification move or a risk-averse reaction to recent market declines? Though the sale amount is negligible compared to the $600 million raised, it still serves as a warning signal.

Similar cases are not uncommon. Meitu once invested approximately $100 million in BTC and ETH, then cashed out near the end of 2024 when BTC surpassed $100,000, selling at nearly $180 million and realizing around $79.63 million in profit. While Meitu isn't a treasury strategy company, this illustrates how so-called "strategic reserves" can easily become tools for profit-taking once prices reach certain levels.

Currently, there’s no large-scale coordinated selling by treasury companies, but potential risks cannot be ignored. Whether driven by profit motives or fear of a downturn, treasury companies could become sources of downward pressure. Lion Group’s sale epitomizes this concern—as one of the earliest HYPE treasury players, its sell-off sounds the alarm: if the "treasury army" begins concentrated dumping, a stampede could erupt instantly, potentially halting the bull run under its own engine’s weight.

mNAV Flywheel: Infinite Ammo or Double-Edged Sword?

Treasury companies’ financing flywheel relies on the mNAV mechanism—an inherently reflexive logic that gives them seemingly "infinite bullets" during bull markets. mNAV refers to Market Net Asset Value ratio, calculated as a company’s market value (P) relative to its per-share net asset value (NAV). In the context of treasury strategy firms, NAV represents the value of their digital asset holdings.

When share price P exceeds per-share NAV (i.e., mNAV > 1), companies can continuously raise capital and reinvest proceeds into digital assets. Each issuance and purchase increases per-share holdings and book value, further boosting market confidence in the company’s narrative and driving share prices higher. Thus, a self-reinforcing positive feedback loop begins: mNAV rises → equity issuance → digital asset purchases → increased per-share holdings → strengthened market confidence → higher stock price. It is precisely through this mechanism that MicroStrategy has been able to keep buying Bitcoin over the years without severe shareholder dilution.

However, mNAV is a double-edged sword. Premium valuations reflect strong market trust but can also stem purely from speculation. Once mNAV converges to 1 or drops below it, the market shifts from a "value accretion" mindset to a "dilution" mindset. If token prices fall at this point, the flywheel reverses into a negative feedback loop, causing simultaneous erosion of market cap and investor confidence. Moreover, treasury companies’ ability to fundraise depends entirely on the mNAV premium. When mNAV stays discounted long-term, their capacity to issue new shares vanishes—undermining the entire business model, especially for small-cap shell companies already stagnant or nearing delisting. Theoretically, when mNAV < 1, a more rational choice would be to sell holdings to repurchase shares and restore balance. But exceptions exist—discounted valuations may simply indicate undervaluation rather than failure.

During the 2022 bear market, even when MicroStrategy’s mNAV briefly dipped below 1, the company chose not to sell Bitcoin or buy back shares, instead opting for debt restructuring to preserve its entire BTC stack. This "hold at all costs" approach stems from Saylor’s faith-driven vision of Bitcoin as a "never-to-be-sold" core collateral asset. However, this path isn't replicable for most treasury companies. Most altcoin treasury stocks lack stable core businesses—the shift to "buying coins" is merely a survival tactic, devoid of ideological conviction. Once market conditions deteriorate, they’re far more likely to dump assets to cut losses or realize profits, potentially triggering a cascade.

How to Mitigate Risks in the DAT Treasury Model?

Prioritize Companies That "Accumulate BTC"

Most current treasury models imitate MicroStrategy, with Bitcoin continuing to serve as the "industry cornerstone." As the world’s only widely accepted decentralized digital gold, Bitcoin’s value consensus is nearly irreplaceable. Whether traditional financial institutions or crypto-native giants, allocations to and expectations around Bitcoin have yet to reach long-term targets. For investors, choosing "BTC treasury companies" tends to be more stable and offers greater long-term confidence premiums compared to those merely mimicking altcoin treasury strategies.

Monitor Competitive Dynamics, Favor Leading Players

Ecological niche competition in capital markets is extremely brutal. Especially in narrative-driven models like the treasury strategy, markets often "remember only the first, forget the second." The rivalry between WINT and BNC clearly shows that once capital and official support consolidate behind one player, the other gets rapidly sidelined. Under these conditions, investors should focus on the "leader effect": the top player typically attracts more institutional funding, media attention, and market trust, while runners-up risk being overlooked.

For retail investors lacking confidence in individual stock picks, directly investing in the underlying coins may be simpler and more effective. In reality, despite fierce corporate competition, both ETH and BNB have reached new all-time highs unaffected.

Focus on Company Fundamentals

One core issue with the DAT model is that many treasury companies are essentially "shell entities," with stalled operations, weak profitability, and almost total reliance on "trading coins" for survival. This model may seem viable during bull runs, but once the market turns, lack of cash flow leads to rapid collapse. Therefore, investors must scrutinize:

Cash flow: Does the company have self-sustaining revenue generation?

Purchase cost: Is the average holding price sufficient to withstand market corrections?

Position size: Is the proportion of digital assets in total net assets excessively high?

Funding use: Are raised funds primarily used to buy coins, or do they support real business expansion?

Debt servicing capacity: Can the company remain resilient when convertible bonds mature or share prices face pressure?

Firms lacking internal cash generation may thrive during booms but possess extremely low resilience when liquidity dries up, making them prime candidates for early casualties in a market crash.

Conclusion

The treasury strategy has undoubtedly injected the strongest fuel into this bull market, channeling endless external capital into altcoins led by ETH. But the more something appears to offer "infinite ammunition," the more vigilance it demands against underlying bubbles and risks. History has shown that liquidity and narrative can ignite markets, but they cannot replace genuine value foundations. While the current market warrants optimism, investors must remain calm and cautious. Only by maintaining rationality amid the noise can one stand firm when the next bubble deflates.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News