Huobi Growth Academy | In-depth Research Report on Stablecoins: The Anchor Asset of the Next Financial Revolution

TechFlow Selected TechFlow Selected

Huobi Growth Academy | In-depth Research Report on Stablecoins: The Anchor Asset of the Next Financial Revolution

This article will conduct a systematic study focusing on stablecoin types, development trends, regulatory landscape, sovereign dynamics, and investment opportunities.

1. Introduction: The Systemic Role of Stablecoins is Reshaping Global Financial Logic

Over the past five years, stablecoins have evolved from supplementary tools for crypto trading into core assets within on-chain finance, gradually integrating into the global financial system. Against a backdrop of the Federal Reserve's interest rate hike cycle nearing its end, challenges to dollar hegemony, and demands for efficiency improvements in cross-border payment systems, the role of stablecoins as "on-chain dollars" is gaining widespread acceptance. From the U.S. passing the GENIUS ACT bill in July 2025, to G7 nations recognizing stablecoins as "digital dollar alternatives," to emerging markets incorporating stablecoins into foreign exchange policy considerations, a financial race centered on "pegged assets" has already begun. Stablecoins are not only liquidity engines in DeFi but also key bridges connecting Web3 with the real economy. This article presents a systematic study focusing on stablecoin types, development trends, regulatory landscapes, sovereign competition, and investment opportunities.

2. Market Status: A Multi-Billion Dollar Market, Structural Diversification, and an Explosion in Use Cases

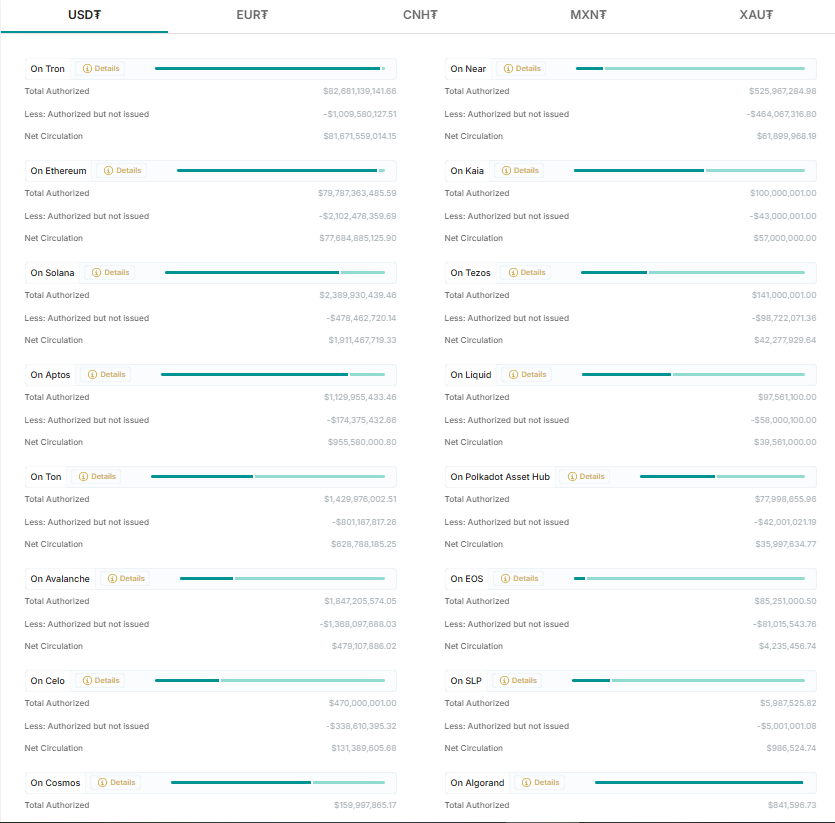

The overall stablecoin market has now surpassed $250 billion in size, exhibiting a highly concentrated structure. Tether’s USDT dominates this space with a market capitalization of $150.335 billion, accounting for 61.27% of the total—effectively supporting nearly half of the entire sector. Following closely is Circle’s USDC, valued at $60.822 billion, representing 24.79% of the market. Together, they control approximately 86.06% of the entire stablecoin market, forming a classic "duopoly" monopoly. This structure is deeply embedded in the infrastructure of crypto finance, where USDT and USDC have each established robust usage networks and trust foundations across different regions and ecosystems.

USDT is currently the most widely used stablecoin, with advantages extending beyond market cap and circulation volume. Its strength lies in its global deployment and extensive real-world applications. It operates across multiple major blockchains including TRON, Ethereum, BNB Chain, and Solana, with particularly high activity on the TRON network, which hosts over half of its total issuance. TRON’s relatively low transaction fees make USDT the preferred choice for OTC and CEX settlements in Asia, Latin America, and the Middle East. Additionally, USDT plays an irreplaceable role in cross-border remittances, value preservation, and providing DeFi liquidity in emerging markets. For example, in high-inflation countries such as Venezuela, Turkey, and Nigeria, USDT has become a de facto "alternative dollar," even serving as a settlement instrument within informal financial systems. This “on-chain dollar” function has allowed it to evolve from a mere transaction tool into a foundational currency, fulfilling functional roles as a "stable asset."

More importantly, Tether’s underlying profit model reflects strong financial capabilities and influence in capital markets. In the first half of 2025, Tether generated over $5.7 billion in net profits, making it one of the most profitable companies in the entire crypto industry. Most of these earnings come from its large holdings of short-term U.S. Treasury bonds, which not only back its stablecoin reserves but also give it tangible influence in short-term interest rate markets. Research indicates that for every 1% share Tether holds in the U.S. Treasury market, it may impact short-end rates by 3.8–6.3 basis points. Its structural penetration into the U.S. Treasury market even exceeds the bond holdings of some small-to-medium sovereign nations. Under these conditions, USDT is no longer just an on-chain utility token but is evolving into a “stablecoin financial institution,” with growing systemic influence over global financial markets.

In contrast, USDC’s development path emphasizes “compliance” and institutional friendliness. It enjoys higher trust and integration within the U.S. domestic market, financial service systems, and Web3 enterprise payments. Circle continues collaborating with regulators, advancing transparency audits, legal reserves, and stable yield distribution models, aiming to establish a “standard paradigm” in the stablecoin space. However, this cautious approach comes at a cost, making USDC appear relatively conservative when competing in fast-paced markets like Asia. It primarily serves as a secure, auditable “trusted stablecoin” within DeFi, favored by institutions bridging TradFi and CeFi, though it still lags behind USDT in grassroots circulation and transaction frequency.

Although the USDT-USDC duopoly appears unshakable in the short term, several new stablecoin projects have recently emerged as significant variables in the market structure. Among them, Ethena’s USDe stands out—a “synthetic stablecoin” supported by hedging ETH perpetual contract positions and yield protocols. Since its launch in early 2024, USDe’s market cap surged from $146 million to $4.889 billion—an increase of over 334x—making it one of the fastest-growing stablecoin projects in recent years. Its rise stems partly from the popularity of the “DeFi fixed income” narrative and demonstrates genuine market demand for non-custodial, contract-driven stable assets. Other tokens like USD1 and USD0 have also attracted investor attention across various thematic niches, gradually meeting specific use-case demands. Yet, in terms of market cap and user base, these emerging stablecoins have yet to develop sufficient strength to challenge dominant players, requiring further progress in risk management, market fit, and liquidity building.

Overall, the current stablecoin market has entered a phase marked by extreme concentration and clear leadership. USDT, through massive scale, powerful on-chain circulation, and penetration into macro financial instruments, has become one of the most systemically important assets in the crypto economy. USDC represents the compliant and transparent direction of stablecoin development, carrying stronger institutional trust value. Emerging stablecoins offer experimental and diversified options, injecting vitality into the market. As global crypto regulations gradually take shape, the stablecoin market will face both the challenges of compliance-driven consolidation and the benefits of the financial disintermediation wave. Whether USDT can maintain dominance, whether USDC can expand its reach, and whether new entrants can break through remain central themes in the market’s evolution over the coming years.

3. Regulatory Competition: Stablecoins as a New Variable in Financial Stability

The rapid growth of stablecoins is pushing what was once considered a “crypto peripheral tool” into the center of macroeconomic policy and regulatory discourse. As their scale expands and use cases multiply, stablecoins are no longer merely technological innovations or decentralized experiments—they are becoming real factors that could affect monetary policy, capital flows, and even systemic financial risks. Faced with this trend, global regulators are undergoing a subtle yet profound power restructuring: on one hand, attempting to set rules and boundaries to preserve traditional financial stability; on the other, acknowledging that stablecoins are filling critical gaps in existing financial systems—especially in cross-border payments, dollar substitution, and financial inclusion.

Currently, major economies have not converged on a unified regulatory approach toward stablecoins, instead showing clear strategic divergence. In the United States, regulators remain locked in prolonged policy debates. Multiple agencies—including the Treasury Department, SEC, and CFTC—hold differing views on the nature of stablecoins, with no consensus on core questions such as whether stablecoins are securities, part of a payment system, or should be issued only by banks. At the same time, the dominance of the dollar-based international financial order makes it impossible for the U.S. to ignore the potential impact of stablecoins on its monetary transmission mechanisms and global financial standing. Tether’s holdings of hundreds of billions in short-term Treasuries already exert measurable effects on money market rates, transforming stablecoins from a sidelined “crypto topic” into a genuine financial variable. Recently, the U.S. Congress has advanced the Clarity for Payment Stablecoins Act and strengthened a regulatory framework centered on “issuer licensing, reserve auditing, and bank custody,” aiming to provide clearer market expectations. However, due to political and technical complexities, this process is unlikely to conclude quickly.

In the European Union, the situation differs slightly. The EU pioneered a comprehensive crypto-asset regulatory framework, MiCA (Markets in Crypto-Assets Regulation), which establishes two distinct categories for stablecoins: “electronic money tokens (EMT)” and “asset-referenced tokens (ART),” imposing strict requirements on transparency, reserves, capital, and issuance caps. While MiCA is widely seen as one of the world’s strictest crypto regulations, its introduction sends a clear signal: regulators are no longer trying to suppress crypto but aim to incorporate it into the formal system through institutional constraints. For stablecoin issuers, accessing the European market will require local authorization and compliance with central bank-level oversight, raising entry barriers and potentially driving major issuers toward greater compliance.

Meanwhile, Asia’s regulatory landscape reflects a mix of pragmatism and competition. Jurisdictions such as Singapore, Japan, and Hong Kong maintain relatively flexible approaches, balancing risk management, user protection, and financial innovation. The Hong Kong Monetary Authority recently expressed support for fiat-backed stablecoins and even proposed the possibility of a “local Hong Kong dollar stablecoin,” signaling openness to regional on-chain currencies. Gulf states like the UAE and Saudi Arabia are actively introducing stablecoin settlement mechanisms, promoting coexistence between CBDCs and stablecoins to build next-generation cross-border payment networks. Clearly, amid regulatory uncertainty in the U.S. and EU, many emerging markets are leveraging stablecoins to compete for influence in shaping fintech governance rules.

The core of the regulatory battle over stablecoins reflects a deeper conflict: the irreconcilable tension among monetary sovereignty, financial stability, and technological innovation. For decades, currency issuance and payment clearing systems were controlled by central and commercial banks. Stablecoins, as privately-led digital currencies, have rapidly embedded themselves into global payments, transactions, financing, and savings—bypassing traditional monetary creation pathways. This disintermediation challenges the core logic of traditional finance and poses a latent threat to central banks’ role as lenders of last resort. During systemic crises or black swan events, if stablecoin users collectively redeem en masse without official backing, it could trigger severe liquidity risks for both on-chain financial ecosystems and issuing entities—potentially spilling over into TradFi markets and amplifying broader financial instability.

For this reason, global central banks and regulators have yet to reach consensus on how to define stablecoins. They are neither electronic money in the traditional sense nor fully equivalent to bank liabilities. Rather, they resemble a “third form of money” suspended between traditional finance and crypto networks—one that cannot yet be fully integrated into existing legal frameworks. Around this ambiguity, regulatory battles will persist in the coming years. Simultaneously, some central banks are proactively developing CBDCs to compete with stablecoins in payments and value storage. Examples include China’s digital yuan, the ECB’s digital euro, and India’s e-rupee—all of which have entered testing and limited circulation phases. This trend reveals an emerging strategic dynamic of competition and cooperation between official monetary systems and on-chain stablecoins.

In essence, stablecoins are no longer mere “accessory tools” of the crypto world but are becoming bridges linking on-chain and off-chain, traditional and innovative systems. They may serve as solutions for financial inclusion, amplifiers of systemic risk, and catalysts for reshaping global financial power structures. In this context, regulation will play a decisive role: it may accelerate stablecoins’ shift toward compliance, enhancing their functionality as “new digital dollars,” or it may stifle innovation through excessive restrictions, pushing capital and technology toward more favorable jurisdictions. Therefore, the future of stablecoins depends not only on technological iteration and market adoption but also on the outcome of global regulatory competition. Stablecoins are not an isolated sector but a deep contest over the next generation of monetary forms and global financial rule-making.

4. Future Trends: Decentralization, Multi-Currency, and Protocol-Native Stablecoins

The stablecoin market is transitioning from its first phase—dominated by centralized dollar-pegged coins—into a second phase characterized by coexistence among decentralized, multi-currency, and protocol-native models. This evolution is not simply about increasing coin variety but involves a comprehensive reconstruction of stablecoin paradigms, governance structures, and monetary sovereignty models. The development of next-generation stablecoins reflects not only internal innovation in crypto finance but also proactive adaptation to traditional finance shortcomings, expanded application frontiers, and ongoing regulatory negotiations.

First, decentralized stablecoins are regaining momentum. Early models like DAI, based on over-collateralization and on-chain liquidation, were once hailed as censorship-resistant, trustless “ideal models.” But due to low capital efficiency and price volatility, they lost prominence. Since 2024, however, rising regulatory risks and settlement dependencies surrounding centralized stablecoins like USDT and USDC have led developers and DeFi protocols to reconsider DAI, sUSD, LUSD, and RAI as vital “alternative currencies” against regulatory suppression and payment censorship.

Notably, new projects avoid relying solely on pure over-collateralization or algorithmic stabilization, instead combining diversified asset pools, risk hedging, and on-chain interest rate adjustments. For instance, Ethena’s USDe integrates spot dollars with a delta-neutral strategy using short perpetual ETH contracts, introducing on-chain derivatives to support yield generation—a novel “yield-driven stablecoin” model. Its associated on-chain metric, DOR (DeFi Option Rate), aims to establish a native “yield curve” for stablecoins, assigning them a more accurate time value of money. These developments signal that stablecoins are no longer just asset tools but anchor points for on-chain interest rates, exchange rates, and liquidity.

Second, multi-currency pegging is accelerating. While dollar-pegged stablecoins dominate, global de-dollarization trends are pushing crypto markets to develop local-currency or commodity-pegged alternatives—backed by euros (EUR), yen (JPY), renminbi (CNY), Hong Kong dollars (HKD), or even gold. Such diversified stablecoins better serve localized payment needs and may become essential tools for residents in emerging markets to hedge against local currency depreciation and inflation. Projects like Stasis’ EURS, Monerium’s EURe, and various HKD stablecoin experiments are expanding non-dollar stablecoin ecosystems. In markets across Asia, Africa, and Latin America—particularly those with strict capital controls—stablecoins serve as crucial “intermediary currencies” in gray economies, crypto remittances, and e-commerce, creating real demand for multi-currency solutions.

At the same time, central banks are gradually exploring coexistence models with fiat-pegged stablecoins. Jurisdictions including Singapore, New Zealand, and Hong Kong are using regulatory sandboxes to test compliance paths for bank- or trust-issued stablecoins. A likely future scenario involves centralized dollar stablecoins serving global liquidity and trade, while compliant local-currency stablecoins enable “domestic on-chain settlements” for residents—forming a dual-track on-chain monetary system.

More cutting-edge is the rise of **protocol-native stablecoins**, indicating that stablecoins are now deeply embedded within on-chain economies. Unlike standalone tokens like DAI or USDC, protocol-native stablecoins are endogenously issued by a blockchain or DeFi protocol, backed by internal assets (e.g., staking tokens, gas tokens, RWAs), and designed exclusively to serve the protocol. Notable examples include Curve’s crvUSD, Aave’s community-driven GHO, MakerDAO’s sDAI, Oasis’ USK, and potential restaking-based stablecoins in the EigenLayer ecosystem. These often integrate liquid staking, re-collateralization, governance rights, and revenue-sharing models, turning stablecoin issuance into a core component of protocol liquidity, governance, and value flow.

Protocol-native stablecoins exhibit several characteristics: stronger composability, higher native liquidity, built-in governance, and tight alignment with protocol growth. This design grants protocols autonomous monetary systems, reducing reliance on external stablecoins like USDC and fostering more stable, decentralized, and censorship-resistant financial ecosystems. Moreover, stablecoins can become tools for protocol “monetary policy”—adjusting collateral ratios, yield rates, and redemption mechanisms to manage liquidity and influence deflation/inflation cycles within the protocol economy, enabling true “on-chain sovereign currency experiments.”

In the long run, stablecoins will evolve along three parallel paths: **(1) Centralized stablecoins strengthening compliance to serve global payment markets; (2) Decentralized stablecoins enhancing censorship resistance and DeFi integration to become foundational on-chain currencies; (3) Protocol-native stablecoins acting as autonomous monetary units within vertical financial ecosystems, supporting growth and stability of specific on-chain systems.** These are not mutually exclusive but may coexist long-term, forming a dynamic structure of interpenetration, collaboration, and competition.

Ultimately, the future of stablecoins will not be determined solely by their peg mechanism but by three key factors: their ability to integrate into new financial systems, their global settlement capacity, and their resilience—maintaining transparency and flexibility under regulatory pressure. This is not merely a battle over crypto currencies but a fundamental restructuring of global financial architecture in the digital age. In this war, stablecoins are both strategic resources and cornerstones of a new order.

5. Investment and Risk: Who Will Win the Next Phase of the Stablecoin War?

Stablecoins have evolved from initial crypto safe havens into foundational infrastructure for on-chain financial systems, with rapidly increasing importance in market cap, use cases, financial integration, and even national policy. Yet as their influence grows, a “stablecoin war” is quietly unfolding. Future dominance will depend not only on technology, capital, and market share but on a multidimensional, multilayered systemic competition. From an investor’s perspective, we must ask: who will prevail in the next phase? And who might expose hidden risks amid apparent growth, exiting prematurely?

Currently, the stablecoin investment landscape can be divided into four categories: (1) Traditional centralized issuers like Tether and Circle; (2) Emerging compliant platforms such as Paxos, First Digital, and Monerium; (3) DeFi protocol-driven stablecoins like MakerDAO, Ethena, and Curve; (4) Chain-native or L2 ecosystem stablecoins such as Aave’s GHO, zkSync’s nUSD, and potential EigenLayer stablecoins.

In the traditional category, Tether (USDT) remains the undisputed leader. Leveraging exceptional market liquidity, a strong retail user base in Southeast Asia and Latin America, and high adaptability to informal financial environments, USDT’s market cap continues to rise—even growing counter-cyclically during Fed rate hikes. However, its investment appeal is constrained by limited disclosure transparency, heavy reliance on the banking system, and a legal structure operating in regulatory gray zones. From an investment standpoint, Tether functions as a “cash cow,” but its growth ceiling is evident, facing long-term systemic risks from regulatory shifts.

In contrast, Circle—the force behind USDC—is pursuing a “mainstream institutional path,” maintaining close ties with U.S. regulators and developing multi-chain issuance mechanisms (USDC is natively deployed on over ten chains). If it successfully goes public or introduces RWA yield-sharing to boost tokenized asset circulation, it could strengthen its compliance moat. However, USDC lacks advantages in informal offshore channels and sees declining usage in DeFi compared to USDT and DAI. Whether it can break beyond compliance circles into widespread “real-world use” remains unproven.

The most compelling developments lie in DeFi-driven new entrants. Represented by Ethena’s USDe, these projects bypass traditional fiat reserves, adopting on-chain yield models and algorithmic financial architectures. USDe’s success is no accident—it embodies a new stability paradigm combining “yield support + algorithmic pegging + derivative arbitrage.” These projects offer high scalability and composability; if validated by the market, they could spawn full financial ecosystems centered on yield trading, liquidity mining, and restaking.

Yet they carry three major risks:

Yield-driven stablecoins may harbor hidden Ponzi-like structures. If yield sources (e.g., shorting ETH perpetuals) suffer extreme market moves or liquidity collapse, price de-pegging or cascading redemptions could occur—triggering a “Algorithmic Stablecoin 2.0 crash.”

Increased complexity reduces system transparency. These models often require high trust in automated rebalancing and liquidation mechanisms, but under extreme conditions—chain congestion, oracle failures, or shallow DEX liquidity—stability mechanisms may fail.

Regulatory uncertainty remains high. By circumventing traditional fiat custodianship, such stablecoins risk being classified as “security-like instruments” or “unauthorized currency issuance,” leading to crackdowns or interface freezes (e.g., delisting from centralized exchanges or bridge shutdowns).

Protocol-native stablecoins like crvUSD, GHO, and sDAI are currently in an “ecosystem-coupled growth” phase. Their investment potential lies in capturing protocol growth via “governance token bonding.” For example, CRV or AAVE holders can vote on key parameters such as usage scenarios, liquidity incentives, and fee distributions for native stablecoins. Stablecoin issuance thus becomes not just a medium of exchange but a central node for governance rights and financial returns. This model offers investors clearer value capture pathways and may shift native token valuations from “pure fees” toward “on-chain monetary dividends.”

However, protocol-native coins are limited by their dependence on the parent protocol’s market position, risk management, and community engagement. In extreme cases, a negative feedback loop—“protocol decline → stablecoin liquidity collapse”—could emerge.

In the long run, victory in the stablecoin war hinges on five core capabilities:

A robust peg mechanism—whether through traditional fiat reserves, on-chain asset hedging, or hybrid structures—is the technical foundation for long-term survival;

User penetration—widespread adoption across exchanges, payments, lending, cross-chain transfers, and settlements—is essential to avoid becoming a “dead circulating token”;

Regulatory compliance and engagement strategies—especially in key financial hubs like Europe, Southeast Asia, and the Middle East—determine growth ceilings;

Synergy with on-chain ecosystems, particularly depth of DeFi integration and native liquidity support;

Sustainable value capture logic—whether through governance, yield distribution, or tokenomics—that instills long-term confidence in holders.

Stablecoins are not “decentralized dollars” but bridge assets in the restructuring of global monetary architecture. They must navigate the crossroads of regulation, liquidity, and trust while traversing turbulent waters of market volatility and technological evolution. The stablecoin war will not crown a single winner but will see multipolar breakthroughs across models, ecosystems, and user contexts. What truly matters to investors are those projects capable of weathering regulatory storms, building on-chain monetary systems, and ultimately connecting virtual finance with the real economy—these will become the “sovereign assets” of the crypto world.

6. Conclusion: Stablecoins as the "Sovereign Anchor" of On-Chain Finance

Stablecoins are not speculative assets but the core operational mechanism of the entire on-chain economy. They are the lifeblood of DeFi systems, the energy powering Web3 payments, and the safety harness for citizens in emerging economies hedging against local currency depreciation. Over the next five years, stablecoins will cease to be “supporting actors” in crypto markets and become pivotal components of a new digital capitalist order. Now is not the endpoint—but the starting point—for systematic investment in the stablecoin sector.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News