Iron Curtain Falls: Stablecoin Alliance Battles 2025

TechFlow Selected TechFlow Selected

Iron Curtain Falls: Stablecoin Alliance Battles 2025

Yiwu and Hangzhou are close; what flows between them is not just mineral water, but also stablecoins.

Author: Zuo Ye

From underground economies across Asia, Africa, and Latin America to Indian expatriates in the Arabian Sea, an iron curtain has descended across the Third World continent.

Behind this curtain lie the fortresses of all banks and FinTechs—Bank of America, JPMorgan, Goldman Sachs, non-bank institutions, Wall Street, K Street, China's Big Four state-owned banks, Washington, and Silicon Valley.

All these renowned strongholds and capital flows reside within TradFi territory. In one way or another, they have not only fallen under stablecoin influence but are increasingly controlled by USDT and Sun Guo.

Tether's Unfocused Strategy

Messari has just released its 2025 stablecoin report. Beyond a sky full of logos and saturated sponsorships, it also serves as an opening speech for the stablecoin war. Whether it’s payment stablecoins, cross-border settlements, or C2C remittances, everything is built upon the alliance between USDT and Tron, with only USDC and CPN (Circle Payment Network) barely holding ground.

Yet the USDT stablecoin empire isn't stable. Sun Guo dominates the Tron chain alone, while Tether itself is too restless. On one side, USDC shares revenue with Coinbase and Binance to devour market share; on the other, Ethena uses a "bribery mechanism" to bind CEXs and capture hedging profits.

Caption: Tether's non-stablecoin businesses, Image source: @MessariCrypto

Gold Dollar → Petrodollar → Stablecoin Dollar

After Tether’s net profit of $14 billion in 2024 surpassed BlackRock, stablecoins officially shed the shadow of the UST collapse, re-entering mainstream global attention. This is the direct reason behind the GENIUS Act’s focus on regulating stablecoins—not just because stablecoins can generate profit, but because they’ve already overtaken real-world economies like Germany to become new underwriters of U.S. Treasuries.

The classic dollar-and-Treasury combo appears to be petrodollar-driven on the surface, backed by military hegemony underneath. But stablecoins are altering short-term Treasury sales dynamics, becoming not just supplements to the dollar, but a new form of the dollar itself.

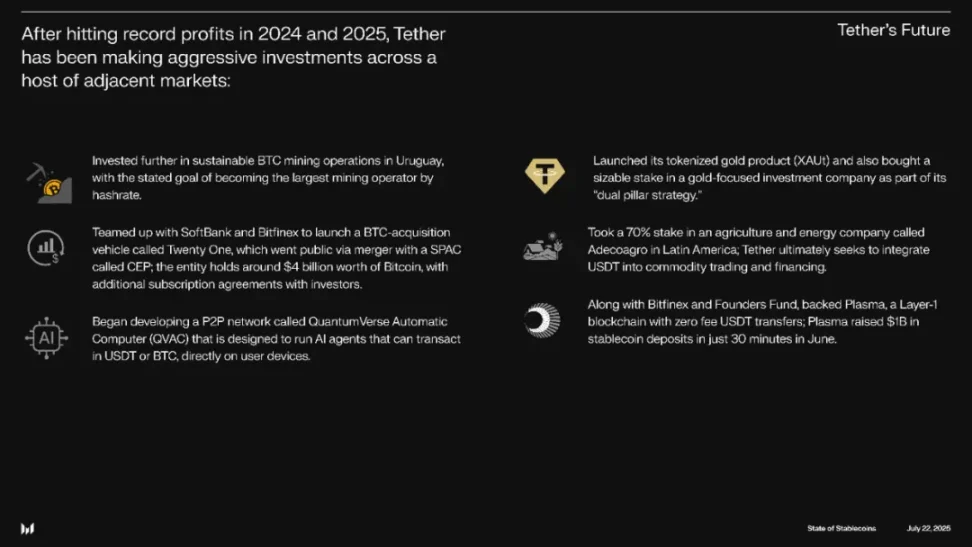

Yet Tether isn’t focused on challenging or reconciling—it’s into Bitcoin mining, password managers, African solar nodes, leveraging Plasma to enter institutional settlement markets, and sharing Twitter co-founder Jack’s passion—scaling up Bitcoin.

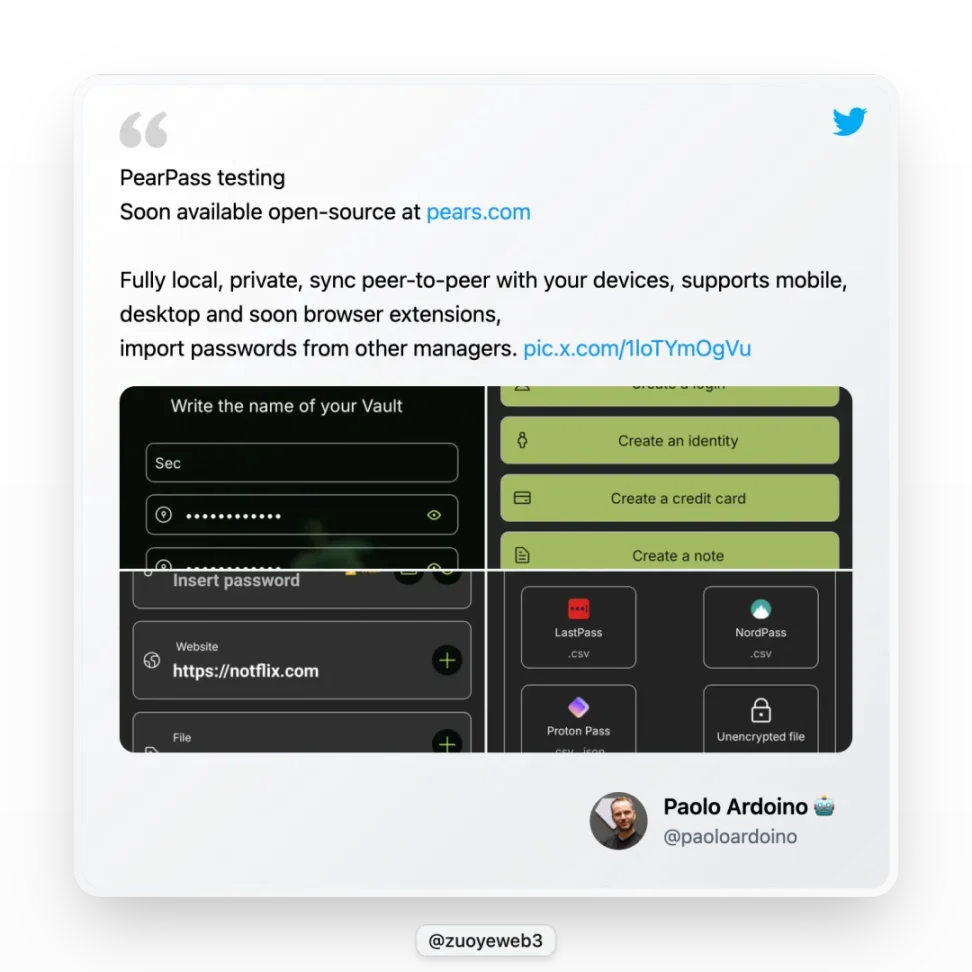

Caption: Tether launches password manager Pears, Image source: @paoloardoino

On June 29, Tether CEO Paolo launched Pears, an open-source, free password manager. This doesn’t directly strengthen Tether’s core business, but you can trust Tether’s technology and初心—they’re doing it purely out of love, not for money.

Tether’s relationship with Bitcoin? “She’s different.”

Of course, this is just rich men’s hobbyism. Within Tether’s diversified investments, building the Bitcoin ecosystem and payment networks remains key—the former reflects long-term belief in Bitcoin’s value, the latter a daily escape from Sun Guo.

A side note: Sun Guo and Tether are drifting apart. Sun Guo has tried TUSD, USDD, and FDUSD to reduce dependence on USDT, while Tether frequently experiments with emerging networks. Yet fate binds them tightly—Bitcoin is their true love; Sun Guo is merely an accident, yet separation is impossible.

Tether has remained consistent in investing and building for Bitcoin. The earliest USDT was issued on Bitcoin’s Omni chain, which ultimately failed. Recently, it deployed on Rootstock, a Bitcoin sidechain, and its supported Plasma treats BTC and USDT as first-class citizens.

This fervor seems less about claiming legitimacy and more genuine passion. Personally, I’m not bullish on Omni or Rootstock’s future—Bitcoin should remain humanity’s digital gold. Plasma has market potential, but competition is fierce, nothing like USDT’s once unchallenged dominance in payments.

The Battle for Legitimacy: Scarface and the Hyena Coalition

Great empires fall due to internal strife. The USDT alliance is far from solid.

Who will succeed Tether—Plasma or Stablechain? Superficially, Plasma leads, but the relationship between USDT and USDT0 is ambiguous. USDT0 appears more like a hidden alternative path Tether nurtures beyond Plasma. The battle for succession will be intense.

Of course, this is internal conflict. Externally, USDC leads the charge toward compliance. The GENIUS Act clarifies regulatory details. Circle previously connected chains via CCTP and adopted ISO 20022 standards into SWIFT, achieving seamless on-chain and off-chain integration.

If Circle is Scarface, then USDG is the hyena coalition. Paxos, former issuer of BUSD, now issues USDG. Targeting clearing networks/chains like CPN, Stablechain, and Plasma, it launched the Global Dollar Network (GDN). Its ecosystem includes exchanges such as Kraken, Bullish (evolved from EOS’s parent company, holding 164,000 BTC), Bitcoin giant Galaxy, and hottest brokerage Robinhood.

Caption: GDN members, Image source: @global_dollar

In total, today’s stablecoin alliances mainly consist of four blocs:

-

USDT: Binance-Tron-Tether-Bitfinex

-

USDC: Coinbase-Circle-Binance

-

USDG: Paxos-Bullish-Galaxy Digital-Kraken-Robinhood

-

USDe: Ethena-Arthur Hayes-Bybit

These cover nearly every aspect of payment, settlement, and pricing. Yet their operations rely on something less than noble—mainly "bribery" mechanisms. Originating from Convex in the Curve Wars, and shining again during the Pendle War LST/LRT era through Penpie and Equilibria, such models prevail.

They don’t lobby stakeholders directly. Instead, they design mechanisms to attract more capital under unified management, gaining scale advantages over competitors, while capturing larger shares of rewards from Curve or Pendle to distribute to their own users.

An even blunter example is Lido, which removes barriers so retail investors avoid the cost of setting up validator nodes—just pay fees to Lido. In this sense, Lido is Ethereum’s largest bribery platform.

USDC operates similarly, giving 60% of revenue to Coinbase and Binance, securing second place behind USDT. Whether big or small earnings, it’s still profit. Such tight binding has benefits—when Silicon Valley Bank (SVB) collapsed and USDC depegged to 0.87, Coinbase still didn’t abandon it.

Ethena’s USDe follows the same model. Investors in USDe include nearly all major CEXs—Binance (YZi Labs), OKX, Bybit, Deribit, Bybit (Mirana), Gemini, MEXC—accepting virtually any exchange. This inclusiveness is its brilliance. These CEXs receive ENA tokens in return for hedging arbitrage and price stability with USDe.

Now cracks appear in the USDT alliance. In the trend toward institutional settlements, USDT not only lags behind USDC’s formal entry, but Ethena has already partnered with BlackRock to launch USDtb and collaborated with Securitize to issue the institutional chain Converge.

Following suit, USDG promises ecosystem participants 97% of issuance revenue—losing money if needed to claim third place behind USDT and USDC. As red, yellow, and blue delivery platforms fight,蜜雪冰城 laughs—so who will ultimately suffer in the stablecoin war?

Conclusion

The long stablecoin war, counting from USDT’s initial issuance in 2014, has entered its 11th year. RMB (offshore) stablecoins emerged no later than USDT, and their operational scale rivals it—Huobi once directly supported RMB-denominated trading, much like Kraken does with USD today.

Hopefully this time, the market can break the monopoly and prevent a repeat of Bitcoin’s hash rate control falling into single hands.

After all, water that flows away may return—but money, once gone, never comes back.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News