"Buying Coins" in US Stocks 2025: Madness, Premiums, and Arbitrage

TechFlow Selected TechFlow Selected

"Buying Coins" in US Stocks 2025: Madness, Premiums, and Arbitrage

In the Era of Premiums: The Future Direction of Micro-strategies from a Professional Trader's Perspective

By Jaleel, BlockBeats

Summer 2025 is the summer of crypto stocks.

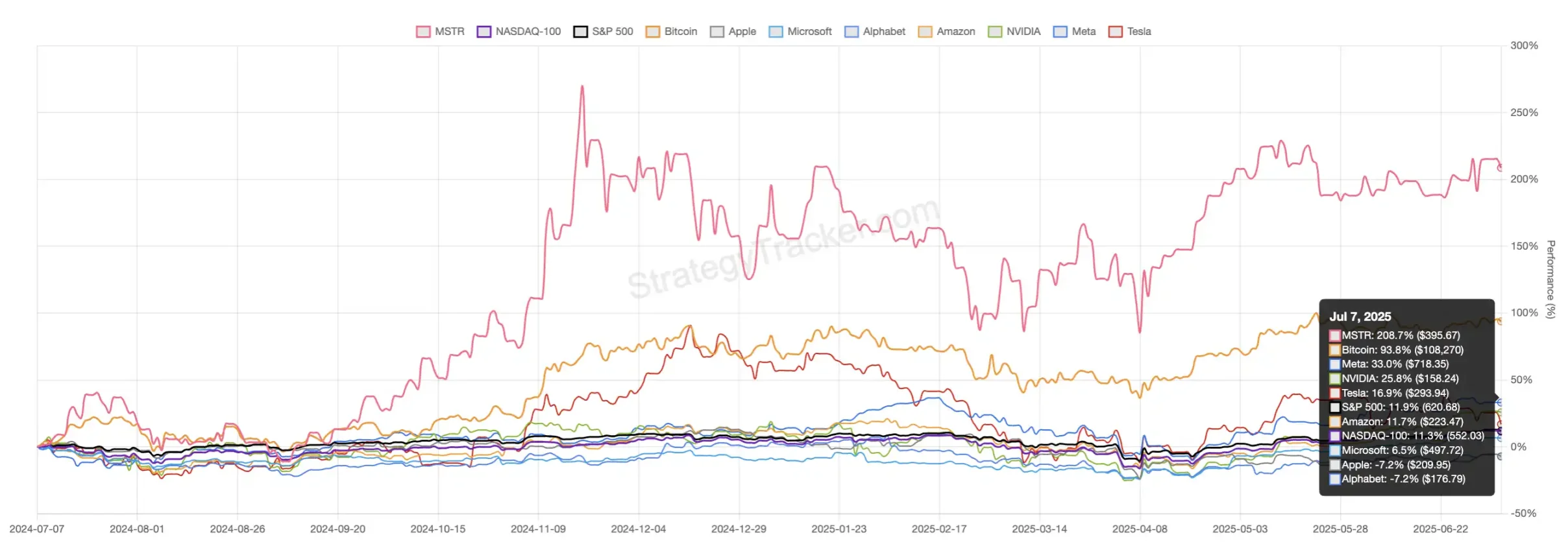

Looking at capital markets, the true headliners this year aren't Meta, nor NVIDIA, and certainly not traditional tech giants. Instead, it's U.S. equities that have strategically placed Bitcoin on their balance sheets—"strategic hodl" stocks. The chart below vividly illustrates MicroStrategy's (MSTR) frenzy.

Over the past year, Bitcoin has surged nearly 94%, outperforming most traditional assets. In contrast, even top-tier tech giants like Meta, NVIDIA, and Tesla saw maximum gains no higher than 30%. Giants such as Microsoft, Apple, and the S&P 500 index have mostly hovered around flat levels—or even declined.

Meanwhile, MicroStrategy’s stock price skyrocketed by 208.7%.

Behind MSTR, a growing cohort of crypto-holding U.S. and Japanese stocks are weaving their own valuation myths. Market-to-crypto net asset value premium (mNAV), securities lending rates, short interest, convertible bond arbitrage, and even GameStop-style short squeezes—all these forces simmer beneath the surface of capital markets. Faith intertwines with structural bets; institutions and retail investors diverge in mindset. On this new battlefield of "crypto stocks," how do traders decide when to advance or retreat? What hidden logics are shaping the market?

In this article, TechFlow dissects the mania and博弈 surrounding "strategic hodl" stocks through three professional traders: from MSTR’s premium swings to new entrants’ covert arbitrage plays, from retail fantasies to institutional calculations—unfolding layer by layer the cycle of this new capital narrative.

The Truth Behind “Strategic Hodl” Stocks

Bullish on BTC, bearish on MicroStrategy—this appears to be the consensus among many traditional financial institutions and traders.

The first trader interviewed by TechFlow, Longxinyan, adopts exactly this strategy: "These companies exhibit vastly different implied volatilities (IV). I buy Bitcoin options over-the-counter via SignalPlus software while selling call options on these stocks—say, MSTR—when U.S. markets open."

In Longxinyan’s words, this “long BTC + short MSTR” volatility spread strategy delivers consistent returns.

"This strategy essentially bets on 'premium reversion to range,'" says Hikari, another conservative-leaning trader: "For example, if the current premium is 2x and you expect it to fall to 1.5x, once it drops there, you lock in profit. But if market sentiment turns overly euphoric, pushing the premium to 2.5x or even 3x, you’ll face unrealized losses."

"Premium"—a term every trader inevitably encounters when discussing "strategic hodl" stocks.

mNAV (Market Net Asset Value), put simply, refers to the ratio between a company’s market cap and the actual net value of its crypto holdings.

This metric rose to prominence largely due to MicroStrategy’s (MSTR) aggressive Bitcoin buying spree starting in 2020. Since then, MSTR’s share price has closely tracked Bitcoin’s movements—but consistently trades at a significant premium above its underlying crypto net asset value. Today, this mNAV "premium phenomenon" has been replicated across more and more crypto-holding U.S. and Japanese stocks like Metaplanet and SRM. In other words, capital markets are willing to pay far more than just the sum of “coin-denominated assets plus core business.” That extra amount reflects bets on hodling, leverage, future fundraising potential, and speculative imagination.

mNAV Premium Index: The Truth Mirror for MicroStrategy-Like Stocks

Reviewing the trajectory of MicroStrategy’s mNAV premium index: from 2021 to early 2024, the premium fluctuated between 1.0x and 2.0x, with a historical average around 1.3x—meaning investors were on average willing to pay a 30% premium over MSTR’s actual Bitcoin holdings.

But starting in late 2024, MicroStrategy’s mNAV premium began climbing, hovering around 1.8x. By the end of 2024, as Bitcoin repeatedly approached $100,000, the MSTR mNAV premium surged along with it, breaking records and reaching an all-time high of 3.3x on some extreme trading days.

In the first half of 2025, the mNAV index oscillated within a 1.6–1.9x range. Clearly, each shift in the premium band reflects changing capital expectations and rising or falling speculation.

As Longxinyan puts it, this mirrors the concept of operating leverage in traditional enterprises—the market evaluates these firms’ future funding capacity, which drives their premium: "MSTR has raised capital multiple times, with creditors spread throughout Wall Street. This ability to raise funds and issue shares is its real competitive edge. The market believes you can keep raising money—that’s why it grants a higher premium." In contrast, small, newly listed "hodl stocks," no matter how loudly they shout, struggle to earn the same level of trust and valuation boost from capital markets.

What Level of Premium Is Justified?

Butter, a quintessential quant and data-driven trader, bases all decisions on historical percentiles and volatility.

"A 2–3x premium for MicroStrategy is reasonable," Butter states after analyzing the concurrent changes in Bitcoin and MSTR’s stock prices over the past year.

From early 2024 to March, as Bitcoin climbed from ~$40K to ~$70K—a 75% gain—MSTR rocketed from $55 to nearly $180, surging over 220%. During this phase, MSTR returned roughly triple that of Bitcoin.

From November to December 2024, as Bitcoin tested the $100K mark again, rising about 33%, MSTR jumped from $280 to ~$520—an 86% increase, more than double Bitcoin’s return.

However, during the subsequent pullback from December 2024 to February 2025, when Bitcoin fell from $100K to $80K (~20% drop), MSTR also corrected by approximately twice that magnitude, declining around 50%.

Similarly, from March to May this year, Bitcoin rebounded ~35% to ~$108K, while MSTR gained nearly 70%—again about 2x.

Beyond the premium index, Butter also tracks annualized volatility. His analysis shows that in 2024, Bitcoin’s daily return standard deviation was ~4.0%, translating to an annualized volatility of ~76.4% under 24/7 trading. Over the same period, MSTR’s daily return standard deviation was ~6.4%, leading to an annualized volatility of ~101.6% during U.S. market hours. In 2025, BTC’s annualized volatility cooled to ~57.3%, while MSTR remained elevated at ~76%.

Thus, Butter’s core thesis is clear: "Fluctuations within a 1.5x–3x premium range provide a strong trading signal." Combining volatility and mNAV premium, he distills a “simplest trading logic”: go long when both volatility and premium are low; go short when both are high.

Hikari’s approach echoes Butter’s, though he layers in options strategies: sell puts to collect premiums during low-premium periods; sell calls to capture time decay during high-premium phases. He cautions retail investors: "Keep margin accounts separate. If you use leverage on both sides, extreme moves can easily blow up your position. Heavy positions, leverage, and options arbitrage all require strict risk management."

Convertible Bond Arbitrage: Wall Street’s Mature Playbook for MSTR

If premium arbitrage and options trading are staples for retail and quant players in the "crypto stock" world, large institutional players focus instead on the deeper layer of convertible bond arbitrage.

On October 30, 2024, Michael Saylor officially unveiled the "21/21 Plan" during an investor call: to gradually raise $21 billion over three years via ATM (At-The-Market) equity offerings, all to fund continued Bitcoin purchases. In reality, MicroStrategy achieved the first phase within just two months—issuing 150 million shares, raising $2.24 billion, and acquiring 27,200 BTC. Then, in Q1 2025, the company doubled down with another $21 billion ATM offering, alongside $21 billion in perpetual preferred shares and $21 billion in convertible bonds—bringing total financing firepower to $63 billion within six months.

Butter observes that this relentless issuance has weighed heavily on MSTR’s share price. Although the stock briefly touched $520 in November 2024, anticipation of further dilution drove it steadily lower, dipping below $240 by February 2025—approaching the lower end of its premium range during Bitcoin’s correction. Even occasional rebounds were often suppressed by follow-up preferred and convertible bond issuances. To him, this explains why MSTR’s stock is extremely volatile in the short term yet structurally prone to sustained fluctuations over time.

Yet for many institutional hedge funds, the focus isn’t directional betting ("up" vs. "down"), but capturing volatility through convertible bond arbitrage.

"Convertible bonds typically carry higher implied volatility than equivalent options, making them ideal for 'volatility arbitrage.' The typical setup: buy MSTR convertibles while short-selling an equivalent amount of common stock, maintaining a near-zero net Delta exposure. Each time the stock swings sharply, adjust your short position—buy low, sell high—and harvest profits from volatility," explains Butter. "This is one of Wall Street’s most mature arbitrage games."

Behind the scenes, a group of hedge funds are quietly playing this classic Wall Street game—“Delta neutral, Gamma long.”

He adds that MSTR’s short interest once reached as high as 14.4%, but much of that isn’t driven by fundamental bearishness—it’s from arbitrageurs using shorts to dynamically hedge convertible bond positions. "They don’t care whether Bitcoin goes up or down—as long as volatility is high, they can repeatedly buy low and sell high to pocket arbitrage spreads," summarizes Butter.

Indeed, MSTR’s convertible bonds function, in effect, as call option derivatives.

Hikari also combines options and convertible bond strategies in practice. He likens buying options to buying lottery tickets—occasionally hitting big, but usually just paying “premium tuition” to the market. Selling options, by contrast, is like running the lottery shop—earning steady income from collected premiums.

"Unlike spot or leveraged futures, options unlock the dimension of time. You can choose expiries—1 month, 3 months, 6 months—each with distinct implied volatilities, enabling countless combinations. Build layered, three-dimensional strategies so that no matter which way the market moves, you keep risk and reward within acceptable bounds."

This philosophy lies at the heart of mainstream Wall Street derivative arbitrage. With MSTR, such structured plays have become the primary battleground for smart money.

Can You Short MicroStrategy Now?

Yet for ordinary investors and retail participants, this seemingly festive arbitrage feast may not be cause for celebration. As more hedge funds and institutions continuously extract value via “issuance + arbitrage,” common shareholders often become the last ones holding the bag. They lack the tools to dynamically hedge like professionals and struggle to detect signs of premium reversion or dilution risks. When massive share issuance occurs or extreme market conditions hit, paper gains can vanish overnight.

For this reason, “shorting MicroStrategy” has become a popular hedging choice among traders and structured funds in recent years. Even staunch Bitcoin bulls may face larger drawdowns holding MSTR stock versus holding BTC directly during periods of high premium and volatility. Managing this risk—or profiting from MSTR’s eventual premium contraction—has become an unavoidable challenge for anyone navigating the "crypto stock" market.

When asked about shorting MSTR, Hikari becomes notably cautious.

He admits he’s “been burned” before. He even wrote a public post-mortem on his WeChat channel—last year, he initiated a short on MSTR at $320, only to watch it surge to $550, enduring immense psychological pressure.

Though he eventually broke even when MSTR pulled back to the $300s, he describes the experience of fighting against high premiums and mounting drawdowns as “indescribable to outsiders.”

This trade fundamentally reshaped Hikari’s approach. He now insists that if he ever shorts again, he won’t use naked short sales or direct call writes. Instead, he’ll prioritize defined-risk instruments like buying put options—even if more expensive—refusing to confront the market head-on. "You must strictly contain risk within tolerable limits," he concludes.

Still, as noted earlier and emphasized by Butter, MicroStrategy has dramatically expanded its authorized common and preferred shares—from 330 million to over 10 billion—while frequently issuing preferred shares, convertibles, and conducting continuous ATM offerings. "These actions lay the groundwork for potentially unlimited dilution. Especially with ongoing ATM issuance and premium arbitrage, as long as the stock trades above book value, management can ‘risk-free’ accumulate Bitcoin—at the expense of common shareholders facing persistent dilution."

Particularly if Bitcoin undergoes a sharp correction, this model of “high-premium financing + continuous buying” will face severe stress. After all, MicroStrategy’s entire playbook depends on sustained market confidence and elevated premiums.

To this end, Butter mentions two dedicated double-inverse ETFs designed to short MicroStrategy: SMST and MSTZ, with expense ratios of 1.29% and 1.05% respectively. "But these are better suited for experienced short-term traders or investors hedging existing positions. Not for long-term holders—leveraged ETFs suffer from 'decay' over time, leading to worse-than-expected returns if held too long."

Could Crypto Stocks Trigger a GameStop-Style Short Squeeze?

If shorting MSTR serves as a risk hedge for institutions and veterans, then “short squeezes” represent the ultimate narrative climax in any market cycle. Over the past year, several institutions have publicly criticized MicroStrategy and Metaplanet—so-called “hodl stocks.” Many investors naturally recall the GameStop saga that shook Wall Street—could similar crypto stocks ignite a comparable short squeeze?

While their analytical angles differ, all three traders converge on similar views.

Longxinyan argues that from an implied volatility (IV) standpoint, MSTR and similar names show no sign of being “overpriced.” Greater risks stem from external shocks—policy shifts or tax changes—that could disrupt the core logic behind the premium. He jokes: "The real shorts have probably moved to CRCL already."

Hikari offers a more direct analysis. He believes a firm like MicroStrategy, with a market cap in the tens of billions, is unlikely to experience a GameStop-style extreme short squeeze. Simple reasons: its float is too large, liquidity too deep—retail or speculative capital cannot collectively move its entire market cap. "In contrast, a small-cap like SBET, initially valued at just tens of millions, stands a chance." He notes SBET’s May rally as a textbook case—its price soared from $2–3 to $124 within weeks, market cap exploding nearly fortyfold. Low-liquidity, hard-to-borrow small caps are fertile ground for short squeezes.

Butter agrees, elaborating further to TechFlow on the two key signals of an impending squeeze: first, an extreme single-day price spike placing the move in the top 0.5% historically; second, a sharp drop in available borrowable shares, forcing short covering.

"If you see a stock suddenly surge on heavy volume, while lendable shares dwindle, short interest remains high, and borrowing costs spike—that’s the brewing signal of a short squeeze."

Take MSTR: as of June, its short volume stood at ~23.82 million shares, or 9.5% of float. Earlier in May, it peaked at 27.4 million shares, with short interest hitting 12–13%. Yet from a lending supply perspective, MSTR’s squeeze risk isn’t extreme. Current annualized borrow cost is only 0.36%, with 3.9–4.4 million shares still available to borrow. Despite notable short pressure, a genuine "squeeze" remains distant.

In stark contrast, SBET (SharpLink Gaming), a U.S. stock hoarding ETH, faces a drastically different landscape. Its annualized lending rate has spiked to 54.8%—making borrowing extremely difficult and costly. Approximately 8.7% of its float is shorted, and all short positions could be covered within just one day’s trading volume. High cost plus concentrated shorting means that if sentiment reverses, SBET could trigger a classic "rolling squeeze."

Then there’s SRM Entertainment (SRM), a U.S. stock stacking TRX—appearing even more extreme. Latest data shows SRM’s annualized borrowing cost reaches 108–129%, with only 600k–1.2 million shares available to borrow. Short interest sits at 4.7–5.1%. Though the percentage is moderate, the exorbitant financing cost severely constrains shorting flexibility. Any market reversal would exert tremendous pressure on funding.

Consider DeFi Development Corp. (DFDV), a U.S. stock strategically accumulating SOL—where borrow costs once soared to 230%, and short interest hit 14%, meaning nearly one-third of the float was sold short. Overall, while the "crypto stock" market possesses fertile ground for squeezes, those most likely to reach the tipping point of explosive "long-short warfare" tend to be smaller-cap, lower-liquidity, and more tightly controlled by capital groups.

There’s Only One MicroStrategy

"Say you have a $10 billion market cap, and the market believes you can raise another $20 billion to deploy—that 2x premium isn’t unreasonable. But if you’re newly listed with a tiny market cap, shouting ‘I’ll raise $500 million!’ from the rooftops won’t convince capital markets," points out Longxinyan, highlighting the critical divide among crypto-holding firms. Only those that truly scale up, demonstrating repeated fundraising and balance sheet expansion, deserve market-granted premiums. Smaller, newer players stand little chance of replicating MSTR’s valuation miracle.

Looking back over the past two years, "strategic hodl" companies have begun clustering across U.S. markets—some heavily loaded with Bitcoin, others investing in Ethereum, SOL, BNB, or even HLP. Some mimic MSTR purely to ride the "hodl premium" wave.

How should we assess their investment logic and market positioning? Longxinyan remains cool-headed: "This space is overcrowded. Companies with only a shell or a gimmick, lacking real operations, are too immature. Public markets aren’t QQ groups—you can’t just gather a few people and play high-stakes capital games." He stresses that capital markets have established rules and底线. Raw Web3 bravado and community hype alone won’t sustain longevity on U.S. exchanges.

Moreover, pricing for such firms varies significantly by region. Take Japan’s Metaplanet—a former hotel operator—now the world’s ninth-largest Bitcoin holder. Thanks to favorable domestic tax policies and limited crypto access for many Asian investors, stocks like MSTR and Metaplanet have become de facto “crypto ETFs” for some. In contrast, Hong Kong-listed firms attempting similar moves face fragmented liquidity and shallow markets, failing to capture the same U.S.-style momentum. Longxinyan bluntly states: "I’m not optimistic about Hong Kong stocks doing this."

Undeniably, placing vast amounts of Bitcoin on corporate balance sheets signals strength. But the market’s “rules of the game” remain unchanged—truly high-quality firms are rare. Most are merely chasing trends and valuation premiums. If Bitcoin crashes, leveraged firms without solid operations may find their refinancing channels dry up, forcing them to dump Bitcoin at bear-market lows—exacerbating downward pressure and triggering chain reactions akin to a “death spiral.”

In bull markets, these firms often exhibit a self-reinforcing loop—"left foot stepping on right foot": coin price rises → hodled assets appreciate → market cap surges → investor enthusiasm grows → fundraising flows smoothly. But in bear markets, everything reverses—valuation systems risk collapse overnight. Longxinyan’s rule is straightforward: "Never buy high-premium stocks; avoid recent converts; steer clear of immature ones; skip those with fewer than two funding rounds—afraid the early creditors might just be insiders, just like developers playing USD-denominated bonds in real estate."

During the interview, Hikari echoed Longxinyan: many emerging "strategic hodl" firms are simply copying MicroStrategy’s script—buy coins, raise funds, tell stories, inflate valuations via "hodl premium." Some are even VC-backed projects or crypto-native teams transitioning into public markets. Hikari admits candidly: "Many of these companies are here just to scam money."

"Ultimately, MSTR’s success stems from sheer scale—the volume of Bitcoin it holds is unmatched. It still has room to innovate: staking its Bitcoin at scale, deploying complex options strategies, monetizing assets. As long as it shares returns with shareholders via dividends, this model can endure."

He adds that beyond MicroStrategy, he only follows a handful of truly transparent, operationally sound "hodl stocks"—such as Japan’s Metaplanet and medical device firm SMLR (Semler Scientific). "As long as asset structure is clear and core business makes sense, these are worth watching."

As for how markets evolve and strategies adapt, Longxinyan, Hikari, and Butter all agree on one thing: no matter how narratives unfold, the most scarce and consensus-driven asset in crypto remains—Bitcoin.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News