The "invisible penetration" of stablecoins: a financial transformation not yet noticed by the general public

TechFlow Selected TechFlow Selected

The "invisible penetration" of stablecoins: a financial transformation not yet noticed by the general public

We are witnessing the early stages of a payment system migration that could reshape the global business landscape within the next five years.

Author: Thejaswini M A

Translation: Block unicorn

Introduction

Yes, stablecoins are hot right now. Circle's stock is soaring. The GENIUS Act is moving through Congress. But that’s not the point.

The real shift is hiding in plain sight. Stripe just acquired a crypto wallet company. Shopify has made stablecoin payments the default option. Amazon and Walmart are reportedly building their own stablecoins.

When the world’s largest retailers start bypassing traditional banks to save billions in fees, this isn’t just about cryptocurrency adoption.

It means the entire payment system is being disrupted by companies we already trust. There are four clear signs that crypto is going commercial.

1/ Privy Is More Important Than You Think

Stripe’s acquisition of Privy isn’t just another routine deal in the crypto space.

Why? Because they’ve bought the final missing piece of the digital payments empire.

Earlier this year: Stripe acquired Bridge (stablecoin infrastructure) for $1.1 billion.

Bridge is the infrastructure that enables stablecoins to work seamlessly for businesses like traditional money. Its API allows instant conversion between U.S. dollars and stablecoins, so companies can make instant global payments without dealing with crypto wallets or complex blockchain technology. Bridge is essentially the bridge between traditional banking and the new digital dollar economy.

This week: Stripe acquired Privy (crypto wallet integration).

Privy enables wallet connections through familiar interfaces—like email addresses—without users ever needing to handle private keys or seed phrases. For Stripe’s massive user base, this means access to crypto payments without having to learn how crypto works.

What do I see? An end-to-end crypto payment stack—from wallet to settlement.

This acquisition signals Stripe’s commitment to making stablecoin payments as easy as traditional card processing. Companies already using Stripe (which processes over $1 trillion annually) can now offer crypto payments without building new infrastructure or asking customers to download wallet apps.

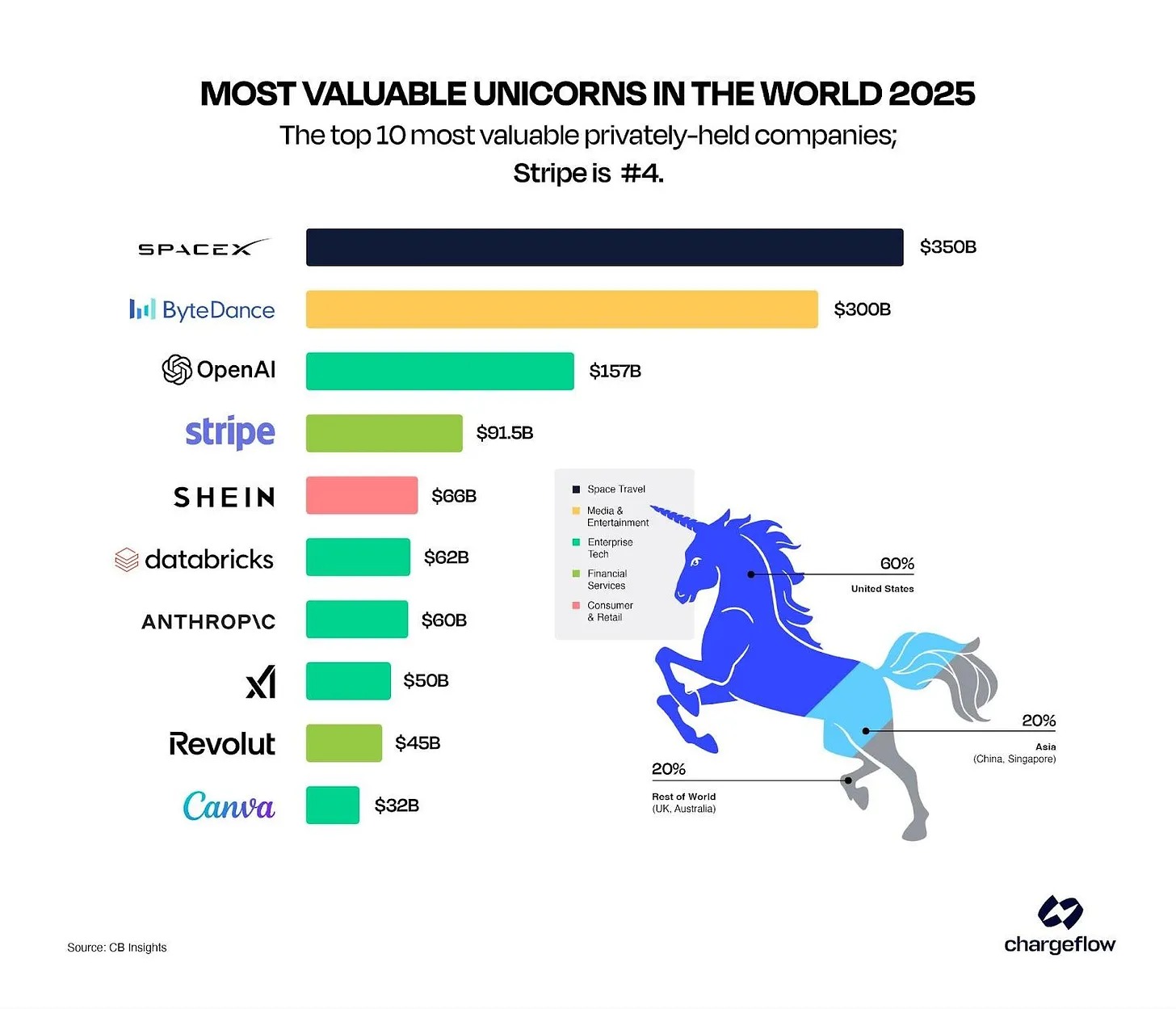

That matters because Stripe powers payment processing for millions of businesses worldwide.

Stripe’s reach is staggering: according to Chargeflow, 1.4 million active websites and 90% of adults have transacted via Stripe. On Black Friday alone, the company processed over 465 million transactions.

When they integrate stablecoin support, it won’t be just one company adopting crypto—it will push adoption across an entire ecosystem.

Privy supports 75 million accounts across more than 1,000 developer teams. Stripe is effectively betting that crypto payments will become as ubiquitous as credit cards.

2/ When E-Commerce Disrupts Itself

Shopify just announced a move that could send chills down the spine of traditional payment processors: USDC payments are rolling out to millions of merchants, and unless sellers opt out, stablecoin payments will be the “default option.”

What happens next?

A partnership with Coinbase and deployment on Base will create a full-stack payment system handling everything from wallet creation to settlement. Customers paying with USDC get 1% cashback, while merchants enjoy faster settlements and lower fees than traditional credit cards.

What does this mean?

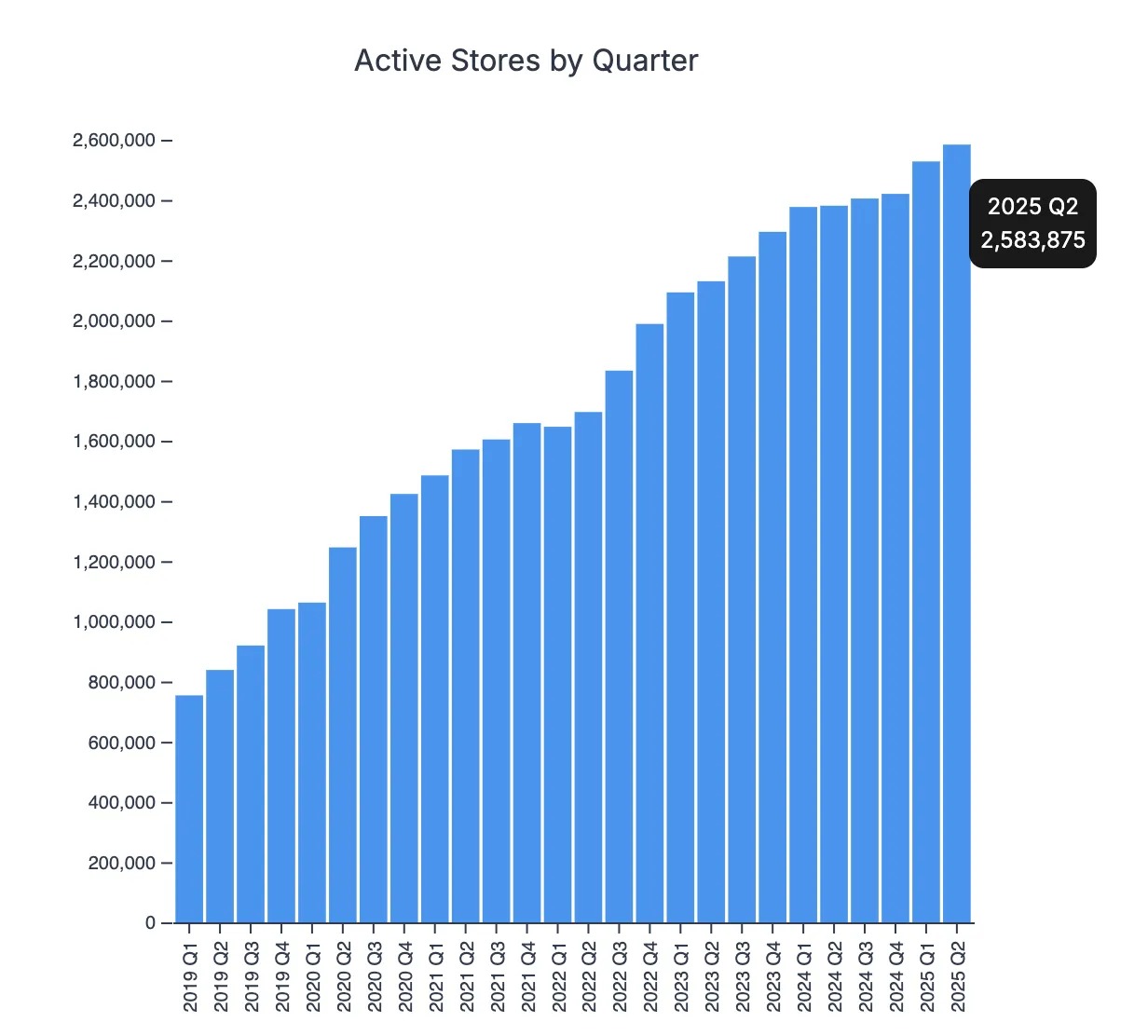

Shopify powers millions of online stores globally—2.6 million merchants across 150+ countries, ranging from solo entrepreneurs to Fortune 500 companies.

Image source: storeleads.app

When a single click enables all these merchants to accept USDC with 1% cashback rewards, I call that a “revolution”—and here’s why.

Traditional payment processors charge retailers 2%–3% per transaction, while stablecoin payments cost mere cents.

Take a $100 purchase:

-

Traditional payment: $2–$3 in fees.

-

USDC on Base: ~$0.05 in fees.

Multiply that across Shopify’s ecosystem, and you’re looking at billions in savings.

What does this mean for you as a customer? These savings won’t vanish into corporate profits. Retailers can either pocket the difference (boosting competitiveness) or pass the savings directly to consumers through lower prices.

Shopify is already offering a sweet incentive. They’re giving customers 1% local currency cashback when paying with USDC. So instead of paying extra for convenience, you get rewarded for using a cheaper payment method.

Once Shopify merchants start saving over 90% on payment processing, other e-commerce platforms will face a dilemma: adopt stablecoin payments or watch their merchants migrate to platforms that support them.

3/ When Retail Giants Build Their Own Stablecoins

According to The Wall Street Journal, both Amazon and Walmart are “considering issuing their own dollar-backed stablecoins for consumers.” Again, the scale we’re talking about is… enormous.

-

Amazon: $638 billion in annual revenue, $447 billion in e-commerce sales.

-

Walmart: Over $100 billion in annual e-commerce sales.

If either company launches its own stablecoin payment system, they could instantly redirect billions in cash flows away from bank partners.

What does this mean for customers?

-

Faster checkout – instant settlement instead of T+2 processing.

-

Lower prices – retailers can pass on savings from eliminated interchange fees.

-

Seamless international purchases – no fees or delays.

Once Amazon or Walmart customers experience buying products for $98 instead of $100 due to no payment processing markups, they’ll expect every other retailer to offer the same. Suddenly, every business will need to integrate stablecoins—or risk losing customers to competitors who can sell the same product at 2%–3% lower prices.

The network effect becomes unstoppable: customers demand savings, retailers must cut costs to stay competitive, and traditional payment processors watch their business model crumble.

4/ The Ultimate Irony: The Banks Themselves

In May, The Wall Street Journal reported that major financial institutions—including JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo—are exploring the creation of a consortium-backed stablecoin. The very banks that have long dismissed crypto are now teaming up to build the infrastructure they once rejected.

Now, JPMorgan—whose CEO Jamie Dimon has criticized Bitcoin for years—has just filed a trademark for “JPMD,” covering digital asset trading, exchange, transfer, clearing, and payment processing.

The bank that processes $1.5 trillion annually via its private JPM Coin is now building public-facing crypto services.

You know why this matters. It’s not because America’s biggest banks suddenly love technology—it’s because they see their payment monopolies ending and want to control the transition.

Banks earn billions from payment processing fees. Stablecoins threaten to eliminate those entirely—and clearly, that process has already begun.

Their choice? Build crypto infrastructure or become irrelevant. Yes, you can call it “surrender.”

Our Take

All these corporate stablecoin announcements aren’t happening in a vacuum. Businesses held back from investing billions into stablecoin infrastructure until they had regulatory clarity. The GENIUS Act provides that clarity—which is why we’re suddenly seeing all these headlines.

Regulatory momentum is paving the way for mainstream stablecoin adoption, removing the uncertainty that previously deterred corporate participation in other crypto assets.

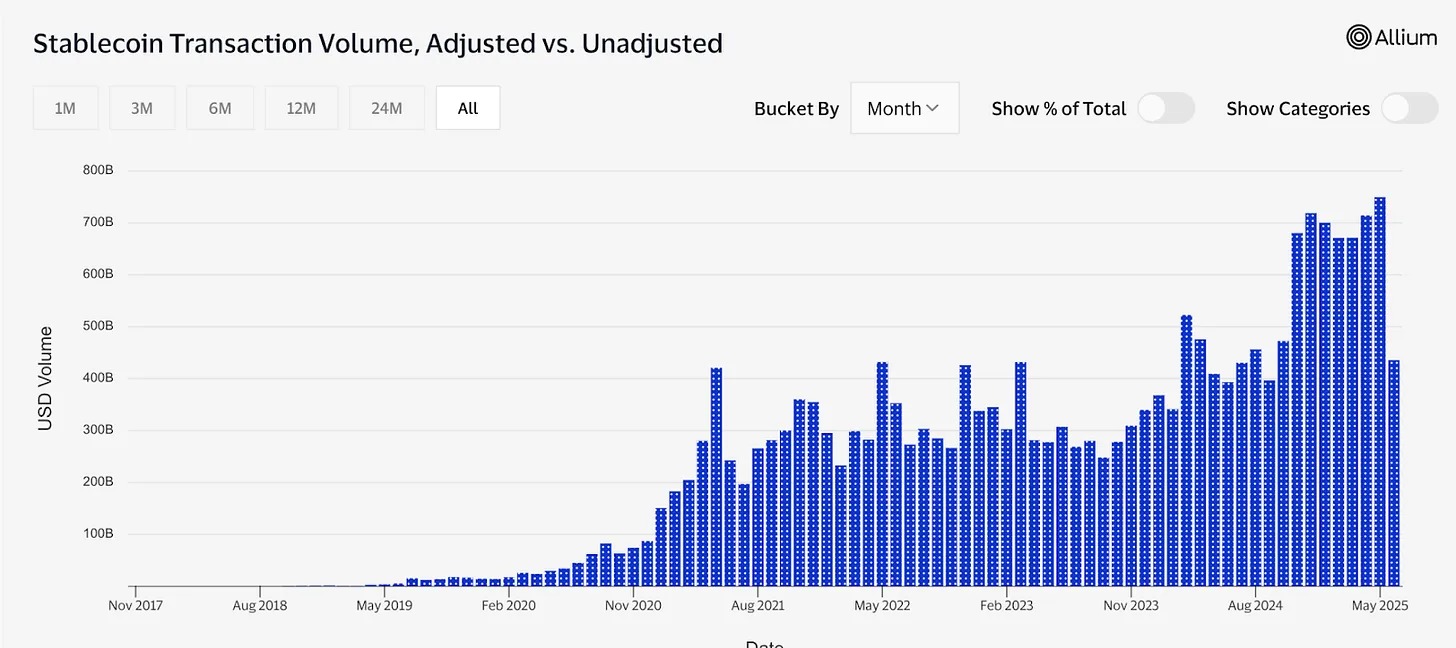

But let’s talk real scale. The data behind stablecoin commercialization reveals why traditional companies are finally paying attention. In May 2025 alone, stablecoin transaction volume hit $4 trillion, with a year-to-date total of $34 trillion.

Visa’s annual transaction volume is around $15.7 trillion; PayPal’s is about $1.7 trillion. This shows the growing importance and influence of stablecoins in global payments.

Image source: Visa

B2B cross-border payments using stablecoins now reach $3 billion monthly, compared to just $1.1 billion via traditional card networks. The speed and cost advantages of blockchain settlement are driving enterprise adoption faster than consumer adoption.

18% of U.S. mid-sized and small businesses now understand cryptocurrency and use stablecoins for business needs—up from 8% in 2024. This adoption is driven by utility, not speculative investment.

When Shopify (with millions of merchants), Amazon ($638B in revenue), and Walmart (over $100B in e-commerce) begin pushing stablecoin adoption, the numbers will quickly become staggering.

Even if just 10% of these companies’ total transaction volume shifts to stablecoins, annual stablecoin usage would increase by over $75 billion.

Once a critical mass of merchants accepts stablecoins, consumers will begin demanding them. Merchants will have to offer them—or lose business. We’re witnessing the early stages of a payment system migration that could reshape global commerce within the next five years.

The craziest part? Most people won’t even notice it happening. They’ll just wonder why their online shopping suddenly feels faster and cheaper.

Whether this represents crypto’s ultimate triumph or its transformation into something entirely different remains to be seen. But all of this suggests that crypto’s true impact may come not from disruption, but from evolution—by embedding so deeply into existing systems that its presence becomes invisible.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News