Buying crypto: the new wealth code for U.S.-listed Chinese companies

TechFlow Selected TechFlow Selected

Buying crypto: the new wealth code for U.S.-listed Chinese companies

On the path of imitation, there are crowds of newcomers.

Written by: TechFlow

On May 27, an obscure small-cap stock caused a stir in the Nasdaq trading hall.

SharpLink Gaming (SBET), a small gambling company with a market cap of just $10 million, announced it would purchase approximately 163,000 ether (ETH) through a $425 million private investment in public equity (PIPE).

Upon the announcement, SharpLink's stock price skyrocketed, surging over 500% at one point.

Purchasing crypto may be becoming a new wealth playbook for boosting valuations among U.S. publicly traded companies.

The origin of this story is naturally MicroStrategy (now renamed Strategy, ticker MSTR), the pioneering company that boldly bet on Bitcoin back in 2020.

Over five years, it transformed from an ordinary tech firm into a "Bitcoin investment pioneer." In 2020, MicroStrategy’s stock traded for just over $10; by 2025, it had surged to $370, with its market capitalization surpassing $100 billion.

Buying Bitcoin not only inflated MicroStrategy’s balance sheet but also turned it into a darling of the capital markets.

In 2025, this trend intensified.

From tech firms to retail giants and small gambling operators, U.S. listed companies are using cryptocurrencies to ignite a new engine for valuation growth.

What secrets lie behind this crypto-buying playbook for inflating market value?

MicroStrategy: The Textbook Case of Stock-Crypto Integration

It all began with MicroStrategy.

In 2020, this enterprise software company kicked off the U.S. stock market’s crypto-buying wave. CEO Michael Saylor stated that Bitcoin was a “more reliable store of value than the U.S. dollar.”

Strong conviction makes for great narrative, but what truly set this company apart was its financial engineering in the capital markets.

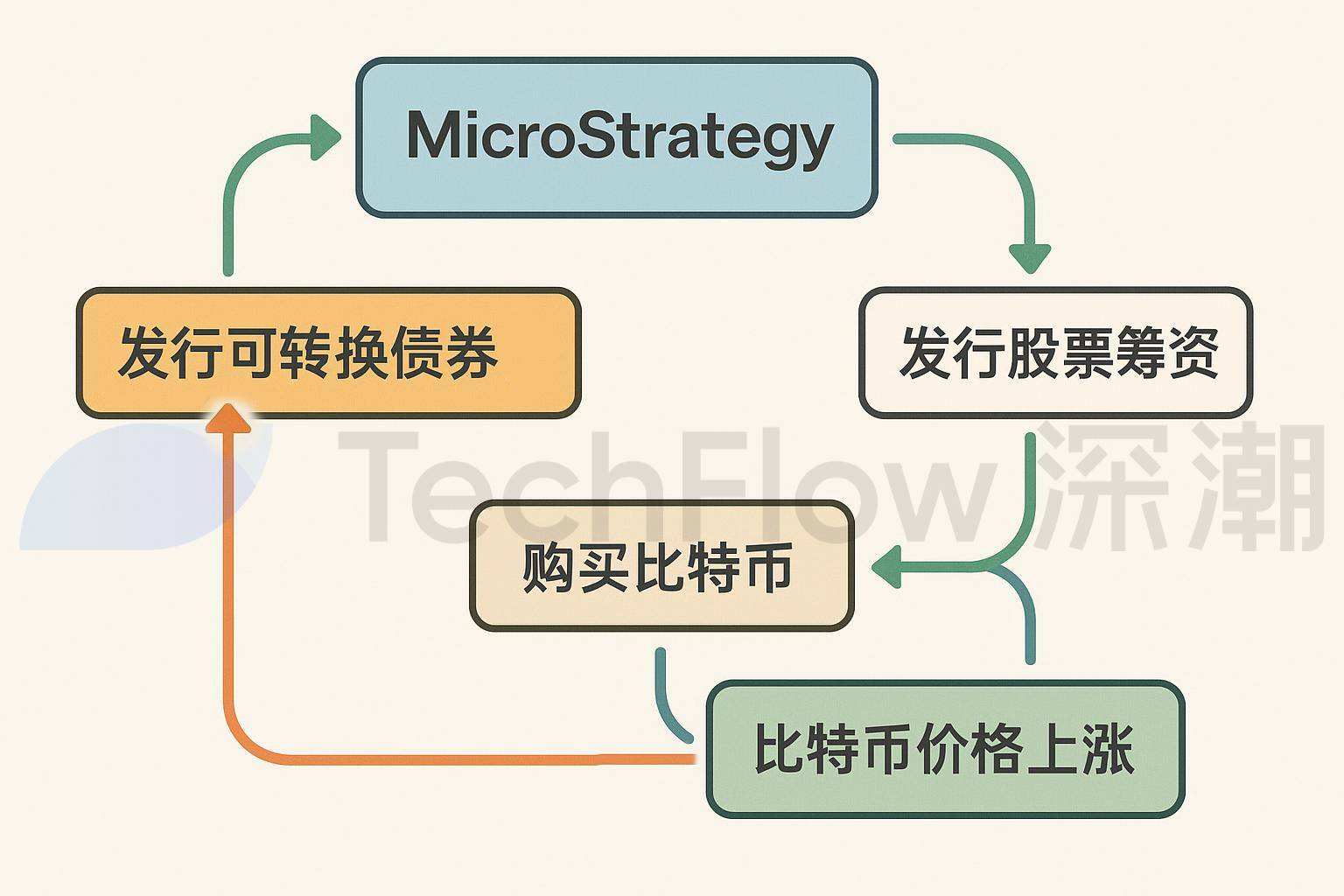

MicroStrategy’s strategy can be summarized as a combination of “convertible bonds + Bitcoin”:

First, the company raises funds by issuing low-interest convertible bonds.

Starting in 2020, MicroStrategy has repeatedly issued such bonds at rates as low as 0%, far below market averages. For example, in November 2024, it raised $2.6 billion via convertible bonds at nearly zero financing cost.

These bonds allow investors to convert into company shares at a fixed future price—effectively granting them a call option, while enabling the company to access cash at extremely low cost.

Second, MicroStrategy allocates all raised capital into Bitcoin purchases. Through multiple funding rounds, it continuously accumulates Bitcoin, making it a core component of its balance sheet.

Finally, MicroStrategy leverages the appreciation of Bitcoin to trigger a “flywheel effect.”

As Bitcoin rose from $10,000 in 2020 to $100,000 in 2025, the company’s asset value soared, attracting more investors to buy its stock. Rising share prices then enable MicroStrategy to issue new bonds or shares at higher valuations, raising even more capital to buy more Bitcoin—creating a self-reinforcing capital cycle.

The core of this model lies in the combination of low-cost financing and high-return assets. By borrowing at near-zero cost through convertible bonds and investing in volatile yet long-term bullish Bitcoin, the company amplifies its valuation by leveraging market enthusiasm for cryptocurrencies.

This strategy has not only reshaped MicroStrategy’s asset structure but also provided a textbook template for other U.S. listed companies.

SharpLink: The Shell Game Isn’t About Gambling

SharpLink Gaming (SBET) refined the above playbook, substituting Ethereum (ETH) for Bitcoin.

Yet beneath the surface lies a clever fusion of crypto-native forces and traditional capital markets.

Its strategy can be described as a “shell play,” centered on leveraging a public listing shell and a compelling crypto narrative to rapidly inflate valuation.

SharpLink was originally a struggling company teetering on delisting from Nasdaq, with its stock once below $1 and shareholder equity under $2.5 million, facing severe compliance pressure.

But it held one key asset—the Nasdaq listing itself.

This “shell” caught the eye of crypto heavyweights: ConsenSys, led by Ethereum co-founder Joe Lubin.

In May 2025, ConsenSys teamed up with major crypto venture firms (such as ParaFi Capital and Pantera Capital) to lead SharpLink’s takeover via a $425 million PIPE investment.

They issued 69.1 million new shares at $6.15 each, swiftly securing over 90% control—bypassing the lengthy IPO or SPAC processes. Joe Lubin was appointed chairman, and ConsenSys clearly stated its intent to collaborate with SharpLink on an “Ethereum treasury strategy.”

Some call it an ETH version of MicroStrategy, but the mechanics are even more sophisticated.

The real goal isn’t to improve SharpLink’s gambling business; it’s to turn the company into a beachhead for crypto capital entering traditional markets.

ConsenSys plans to use the $425 million to acquire around 163,000 ETH, branding SharpLink as an “Ethereum version of MicroStrategy” and positioning ETH as a “digital reserve asset.”

Capital markets thrive on “story premiums.” This narrative attracts speculative capital and offers institutional investors—who can’t directly hold ETH—a publicly traded proxy.

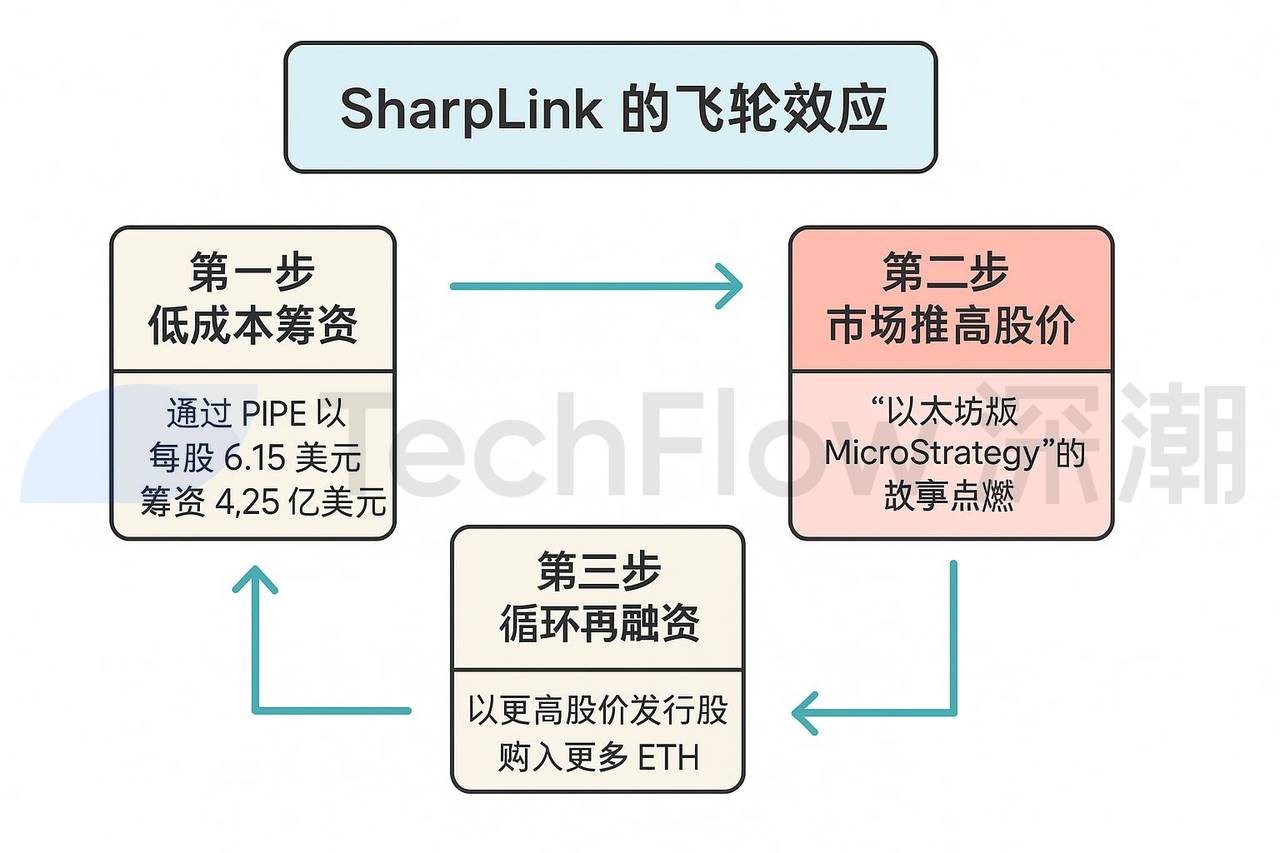

Buying crypto is just the first step. SharpLink’s true “magic” lies in its flywheel mechanism, which operates in three cyclical phases:

Step one: Low-cost fundraising.

SharpLink raised $425 million via PIPE at $6.15 per share—cheaper and faster than IPOs or SPACs, without roadshows or complex regulatory hurdles.

Step two: Market hype drives stock surge.

Investors are captivated by the “Ethereum MicroStrategy” story, sending the stock soaring. Market appetite far exceeds the intrinsic asset value, with investors paying a significant premium over the net value of its ETH holdings. This “psychological premium” rapidly inflates SharpLink’s market cap.

SharpLink also plans to stake these ETH tokens on the Ethereum network, earning 3%-5% annual yield.

Step three: Repeated refinancing. With a higher stock price, SharpLink can issue more shares to raise additional capital, buy more ETH, and repeat the cycle—growing its valuation like a snowball.

Behind this “capital magic,” however, lurks the shadow of a bubble.

SharpLink’s core business—gambling marketing—is virtually ignored. Its $425 million ETH investment plan is completely detached from fundamentals. The stock surge is driven largely by speculation and narrative momentum.

The truth is, crypto capital can exploit the “shell + crypto buying” model to inflate valuation bubbles rapidly through small- and mid-cap listed shells.

The real intention isn't the business itself—synergy is nice, but irrelevant if absent.

Mimicry Isn’t Foolproof

The crypto-buying strategy may seem like a “wealth code” for U.S. listed companies, but it’s far from universally effective.

The path of imitation is crowded.

On May 28, GameStop—the video game retailer famous for the retail vs. Wall Street short squeeze—announced it would spend $512.6 million to buy 4,710 bitcoins in an attempt to replicate MicroStrategy’s success. Yet the market reacted coldly: GameStop’s stock dropped 10.9% after the announcement, showing investor skepticism.

On May 15, Addentax Group Corp (ticker ATXG), a Chinese textile and apparel company, announced plans to purchase 8,000 bitcoins and TRUMP tokens via common stock issuance. At today’s BTC price of $108,000, this would cost over $800 million.

Yet, the company’s total market cap is only about $4.5 million—meaning its theoretical purchase cost exceeds 100 times its market value.

Almost simultaneously, another Chinese U.S.-listed company, Jiuzi Holdings (ticker JZXN), joined the crypto-buying frenzy.

It announced plans to buy 1,000 bitcoins within a year at a cost exceeding $100 million.

Public records show Jiuzi Holdings is a China-based company focused on new energy vehicle retail, founded in 2019, with stores mainly in third- and fourth-tier Chinese cities.

Its Nasdaq market cap stands at only around $50 million.

Yes, the stock price is rising—but alignment between market cap and purchase cost is critical.

For most followers, if Bitcoin prices fall and they actually buy in, their balance sheets will face immense pressure.

The crypto-buying strategy is no universal wealth formula. Overleveraged, fundamentally unsupported bets on crypto may simply be a gamble toward bubble collapse.

Another Way to Break Into the Mainstream

Despite the risks, the crypto-buying trend may still become the new normal.

In 2025, persistent global inflation and expectations of dollar depreciation have led more companies to view Bitcoin and Ethereum as “anti-inflation assets.” Japan’s Metaplanet has already boosted its market value through a Bitcoin treasury strategy, and more U.S. listed firms are accelerating their adoption of MicroStrategy-style plays.

Amid this macro trend, cryptocurrencies are increasingly visible in global politics and economics.

Is this the kind of “breaking into the mainstream” that crypto enthusiasts often talk about?

Looking at current trends, there are two main pathways for crypto to go mainstream: the rise of stablecoins and crypto reserves on corporate balance sheets.

On the surface, stablecoins provide a stable medium for payments, savings, and remittances in the crypto ecosystem, reducing volatility and promoting wider adoption. But in essence, they extend the dominance of the U.S. dollar.

Take USDC, for instance. Its issuer, Circle, maintains close ties with the U.S. government and holds substantial U.S. Treasuries as reserves. This not only reinforces the dollar’s role as the world’s primary reserve currency but also extends the reach of the U.S. financial system into the global crypto market through stablecoin circulation.

The second pathway is exactly what’s been discussed—the purchase of crypto by public companies.

These firms use crypto narratives to attract speculative capital and inflate stock prices. But beyond a few leading examples, it remains unclear how much these copycats actually improve their core business fundamentals—even as they grow their market valuations.

Whether viewed as exploitation or financial innovation depends on which side of the table you’re sitting—both perspectives are two sides of the same coin.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News