Exploring the Evolution of Innovation Cycles: Why Are Excess Returns Often Captured by Second-Movers?

TechFlow Selected TechFlow Selected

Exploring the Evolution of Innovation Cycles: Why Are Excess Returns Often Captured by Second-Movers?

When new primitives emerge, it's important not only to examine their direct impact but also to identify who is best positioned to facilitate, optimize, and scale the behaviors they enable.

Author: Saurabh Deshpande

Translation: Felix, PANews

If you're watching what's happening on-chain firsthand, it might feel like the apocalypse is near. You could even argue that AI has already overtaken crypto as the breeding ground for future tech. There’s truth in all these claims—but it helps to zoom out and take a broader view.

This article explains how innovation cycles evolve step by step until technology finds product-market fit. Today’s story dives into the common thread linking Uber, Pendle, and EigenLayer. Hopefully, it will help dispel the doom-laden narratives flooding Twitter and offer you a fresh perspective.

For thousands of years, human flight was considered impossible. In just 112 years since humans first took to the skies, we’ve now figured out how to catch rockets returning from space. Innovation, it seems, is a gradual force spanning generations.

The true magic of technology rarely lies in the initial invention, but in the ecosystem that grows around it. Think of it as compound growth—but with innovation instead of money.

While pioneers who create new things grab headlines and VC funding, it’s often the second wave of builders who extract the most value—those who spot untapped potential within existing foundations. They see possibilities others miss. History is full of innovators who never predicted how their inventions would reshape the world. They simply tried to solve immediate problems—and in doing so, unlocked possibilities far beyond their original vision.

The best innovations aren’t endpoints; they’re launchpads that enable entirely new ecosystems to take off. This article explores how this phenomenon plays out in Web3—starting with GPS, something we use daily, then tracing back through re-staking and points systems into the crypto realm.

A Weekend That Changed the Internet

GPS has been about precise Earth positioning since its inception in 1973. But Google Maps went much further—it made raw location data accessible, usable, and understandable for billions.

Google Maps began in late 2004 with three strategic acquisitions.

First was Where 2 Technologies, a small Australian startup operating out of a bedroom in Sydney. They built “Expedition,” a C++ desktop app using pre-rendered map tiles for smooth navigation. Compared to MapQuest’s clunky interface, the user experience was vastly superior.

At the same time, Google acquired Keyhole (satellite imagery) and ZipDash (real-time traffic analytics), integrating core components of its mapping vision. Together, these acquisitions formed the foundation of Google Maps: merging interactive navigation, rich visual data, and dynamic information into a single application.

Expedition was a desktop app, but Larry Page insisted on a web-based solution. Early attempts were slow and uninspired. Bret Taylor, a Stanford graduate and former Google VP of Product Management, stepped in to fix it.

Taylor rebuilt the entire frontend using Asynchronous JavaScript and XML (AJAX)—an emerging technology that allowed websites to update content without reloading the whole page. Before AJAX, web apps were static and sluggish. With AJAX, responsiveness matched desktop software. Maps became draggable; new tiles loaded seamlessly—revolutionary UX in 2005.

The real genius came when Google released the Maps API later that year, transforming the product into a platform. Developers could now embed Google Maps and build atop it, sparking thousands of “mashups” that evolved into full businesses. Uber, Airbnb, and DoorDash exist because of one decisive weekend when Bret Taylor made maps programmable.

Taylor’s intuition reflects a recurring pattern in tech: the deepest value rarely comes from the base layer, but from what others build on top. These “second-order effects” represent the true compounding magic of innovation—one breakthrough empowering an entire ecosystem, spawning unforeseen applications.

Once Google Maps became programmable, ripple effects followed. Airbnb, DoorDash, Uber, and Zomato led the charge, embedding GPS at the heart of their services. Pokémon Go pushed further, layering augmented reality over location data, blurring lines between physical and digital worlds.

But behind it all? Payments. Because what good is on-demand service without seamless payment?

The GPS tech they relied on wasn’t new. But GPS alone couldn’t create miracles. It was the culmination of decades of technological evolution—satellite positioning, mobile hardware, AJAX, APIs, and payment rails—all quietly converging.

This is why second-order effects are so powerful. They rarely attract attention in real time. But one day, you look up and realize your daily life is coordinated by an invisible network of innovations accumulating silently for years.

How Re-Staking Sparks Products

In June 2023, EigenLayer launched “re-staking” on Ethereum mainnet, reshaping Ethereum’s security landscape. The concept was novel yet simple enough for any crypto enthusiast to grasp: “What if you could stake your ETH twice?”

In traditional staking, your ETH earns steady but modest returns—3.5% to 7%. Re-staking essentially makes the same ETH do double duty: securing both the Ethereum network and the EigenLayer protocol simultaneously—same capital, multiple income streams, higher capital efficiency.

By April 2024, EigenLayer had evolved from theoretical innovation to fully operational system with massive adoption. The numbers speak: 70% of new Ethereum validators opted in immediately. By end of 2024, over 6.25 million ETH (around $19.3 billion) was locked in re-staking. If ranked by GDP, it would sit around #120 globally.

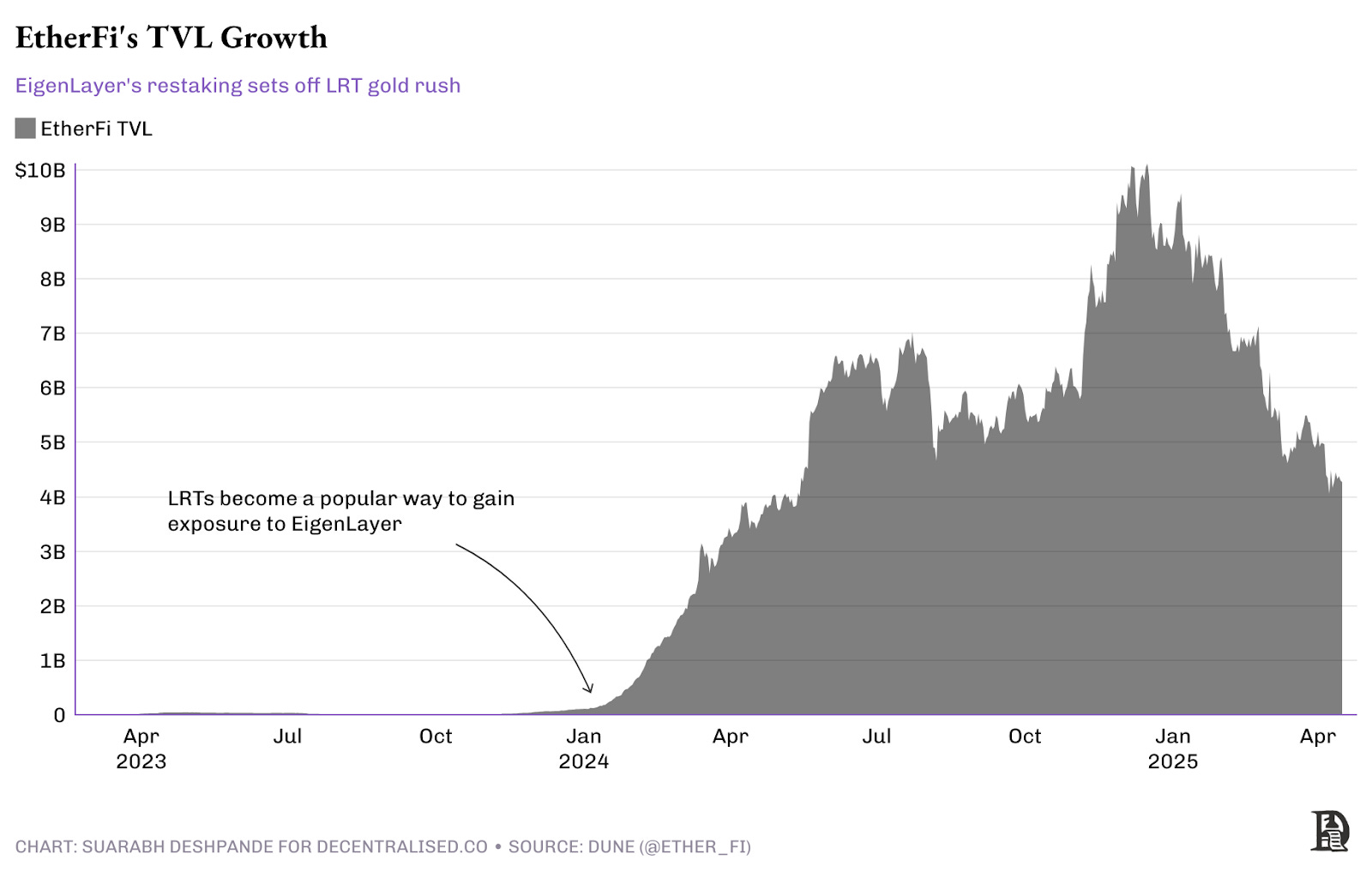

But the interesting part isn’t just that EigenLayer made re-staking possible—it’s that others quickly followed. EtherFi, a liquid staking provider, quietly launched in early 2023.

EtherFi anticipated that re-staking via EigenLayer would become one of DeFi’s hottest opportunities. You stake ETH, receive eETH tokens, then automatically re-stake on EigenLayer. And as a bonus, you can take your eETH and play in other DeFi sandboxes. Pendle is one such sandbox. It’s like getting paid multiple times for doing essentially the same thing—welcome to crypto finance, folks.

The results? Impressive. By May 2024, Ether.fi’s TVL surged to ~$6 billion. Their “Liquid Vault” offered around 10% APY, while regular staking felt underwhelming in comparison.

What Ether.fi did for re-staked ETH mirrors what Lido previously did for staked ETH. By creating liquidity, accessibility, and utility for re-staked ETH, they made re-staking practical, mainstream, and profitable.

Beyond yield chasing, there’s “points farming”—users pursue not only immediate rewards but accumulate “points” expected to convert into valuable tokens later. Call it a speculative flywheel if you like. As more users re-stake via Ether.fi, more eETH circulates and integrates deeply with other DeFi projects like Pendle, where future yields—and even points themselves—can be traded, giving rise to entirely new financial instruments.

As for points—the lifeblood of efficient capital mercenary activity in crypto. When protocols started rewarding points, hordes of users rushed in to maximize them, often gaming the system. The original intent was fairer, wider token distribution. But once it turned into a race, distortions emerged. The most active “miners” weren’t always the most aligned users. While many projects still use points for token distribution, the strategy no longer draws the same level of excitement.

So, as usual, the lesson isn’t just that innovation matters. More importantly, the biggest winners are rarely those who first create what everyone talks about. They’re the ones who come later, understand what’s actually happening, and build exactly the right thing at the right time.

Yes, EigenLayer laid the groundwork. But companies like Ether.fi and others who saw second-order effects also captured significant value—by mid-2024, claiming over 20% share of Ethereum’s staking market. In crypto, being first matters less than understanding what others are building on.

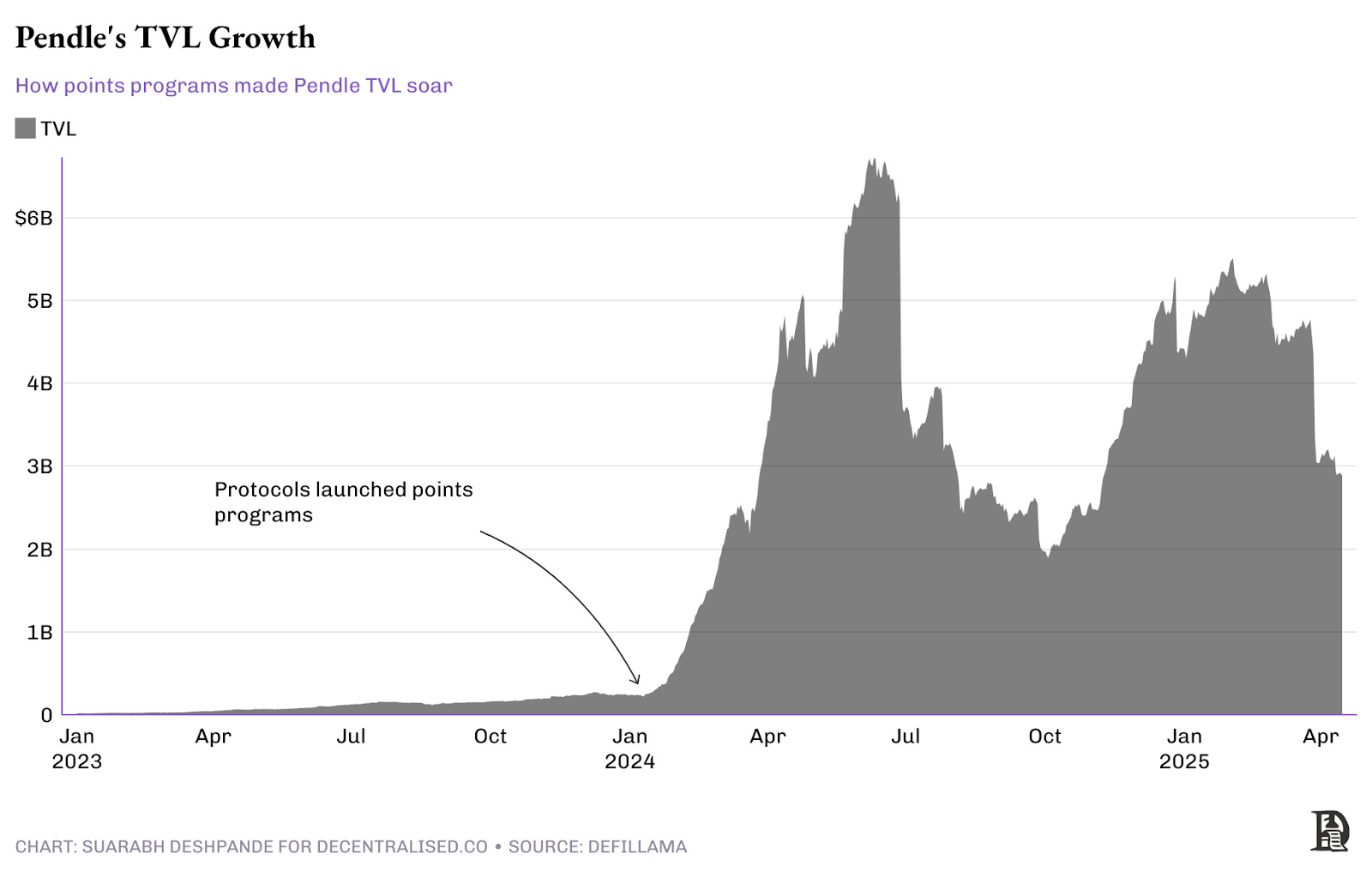

Points and Pendle

After Jito’s wildly successful airdrop, points entered the mainstream in December 2023. The Solana-based protocol debuted with a FDV exceeding $1 billion, igniting a gold rush. Suddenly, protocols across the ecosystem shifted from direct token distributions to points systems, rewarding users with points redeemable for governance tokens later. What began as a novel mechanism quickly became dominant strategy.

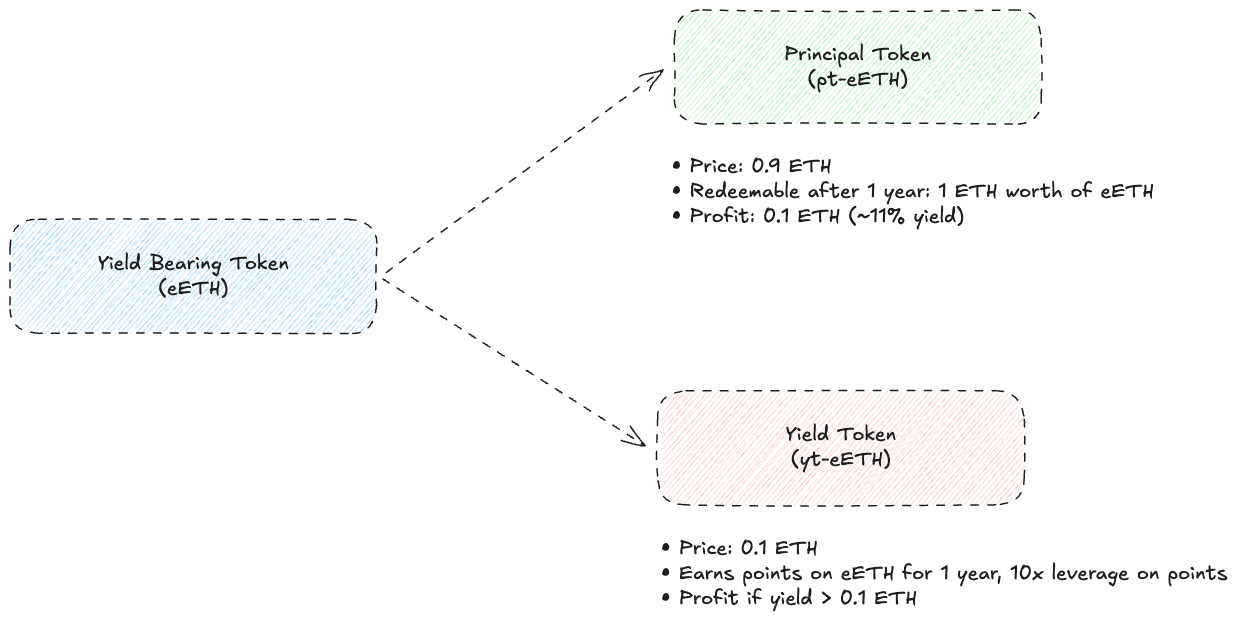

Pendle launched in June 2021, focusing on tokenizing and trading future yields. Its core innovation was elegant: splitting yield-bearing assets into two tokens—Principal Tokens (PT), representing the underlying asset, and Yield Tokens (YT), capturing future yield. This separation let users trade each component independently, enabling finer control over yield strategies than ever before.

When the points race officially kicked off, Pendle found itself uniquely positioned—not because it planned for it, but because its architecture accidentally enabled leveraged points farming. Users could earn both floating yield and associated points simultaneously, amplifying their points accumulation without additional capital.

Here’s how it worked. Suppose Sid wants to farm points from a protocol like EigenLayer that rewards liquidity providers. Traditionally, he’d deposit ETH into EigenLayer’s staking contract, locking funds for weeks or months. With Liquid Restaking Tokens (LRTs) and Pendle combined, Sid could buy Yield Tokens (YT) that represent future yield and points—without directly depositing ETH into EigenLayer.

For example, say eETH trades at $2,000 and earns 24 EigenLayer points per day. pteETH represents the principal token (fixed yield), yteETH the yield token (floating yield + points), priced at $200. The pteETH holder gives up points for fixed return. The yteETH holder gets variable yield and points. Now, with just $2,000, Sid earns 240 points per day (worth 10 ETH) instead of just 24.

Pendle founder TN Lee analyzed this in detail on a podcast. His team didn’t build a meta-framework for points—they couldn’t have predicted it. Yet they built perfect infrastructure for this emergent behavior and reaped massive capital gains. Even as the trend cooled and TVL dropped to ~$2.5 billion, their valuation remained 10–15x higher than before points existed.

Memecoins, Pump.fun, and Raydium

Sometimes second-order effects emerge from the most unexpected places—and revitalize entire ecosystems in the process. The Solana revival of 2023–2024 is a prime example, showcasing crypto’s rapid evolution and how those positioned at key crossroads capture disproportionate value.

After FTX collapsed in late 2022, many wrote obituaries for Solana. The logic seemed sound. SBF and his firms exerted massive influence—providing funding, liquidity, and market support. Without them, Solana struggled. The tech suffered reliability issues, and “Solana down” jokes became memes. The blockchain once hailed as the “Ethereum killer” appeared on life support.

Yet an extraordinary transformation was underway. Throughout 2023, Solana steadily improved. Outages became rarer. Transaction finality and UX noticeably smoother. Developers drawn to Solana’s technical foundation—high throughput, low cost, sub-second finality—began returning, albeit cautiously.

By early 2024, a decisive reversal occurred. Amid growing disillusionment with traditional DeFi governance tokens and a broader shift toward so-called “financial nihilism,” user attention and capital flooded into memecoins. These tokens—often useful for little beyond community ownership and cultural signaling—captured market imagination. Solana, with its lightning-fast transactions and ultra-low fees, provided the ideal environment for this new wave.

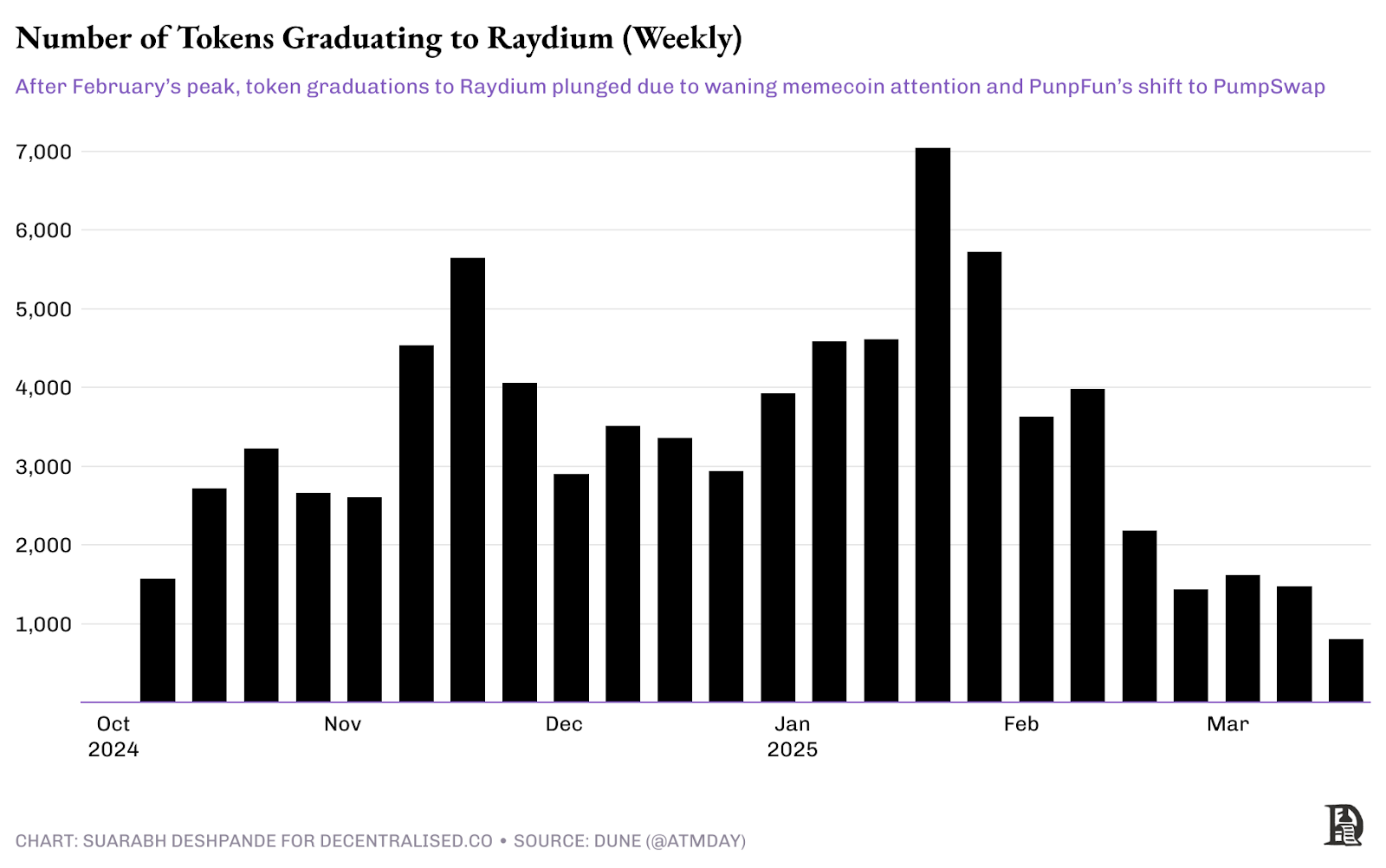

PumpFun launched in January 2024. This “memecoin factory” democratized token creation—once the domain of skilled developers—into a process taking minutes. PumpFun embodied the spirit of crypto’s financial experimentation. Almost overnight, thousands of new tokens like “BONK,” “Dogwifhat,” and “POPCAT” flooded the Solana ecosystem.

These seemingly frivolous tokens quickly revealed their potential as catalysts for complex value chains. They needed one critical thing: liquidity. Without trading venues, even the cleverest memecoin idea was worthless. Enter Raydium, Solana’s decentralized exchange, perfectly positioned.

Raydium had long aimed to be Solana’s leading DEX, focusing on capital efficiency and reduced slippage. It wasn’t built for memecoins. But its architecture—similar to Uniswap’s concentrated liquidity pools and permissionless listing—proved ideal for handling sudden surges of new assets.

Timing was perfect. Years of infrastructure development created the solid foundation needed for this unexpected use case.

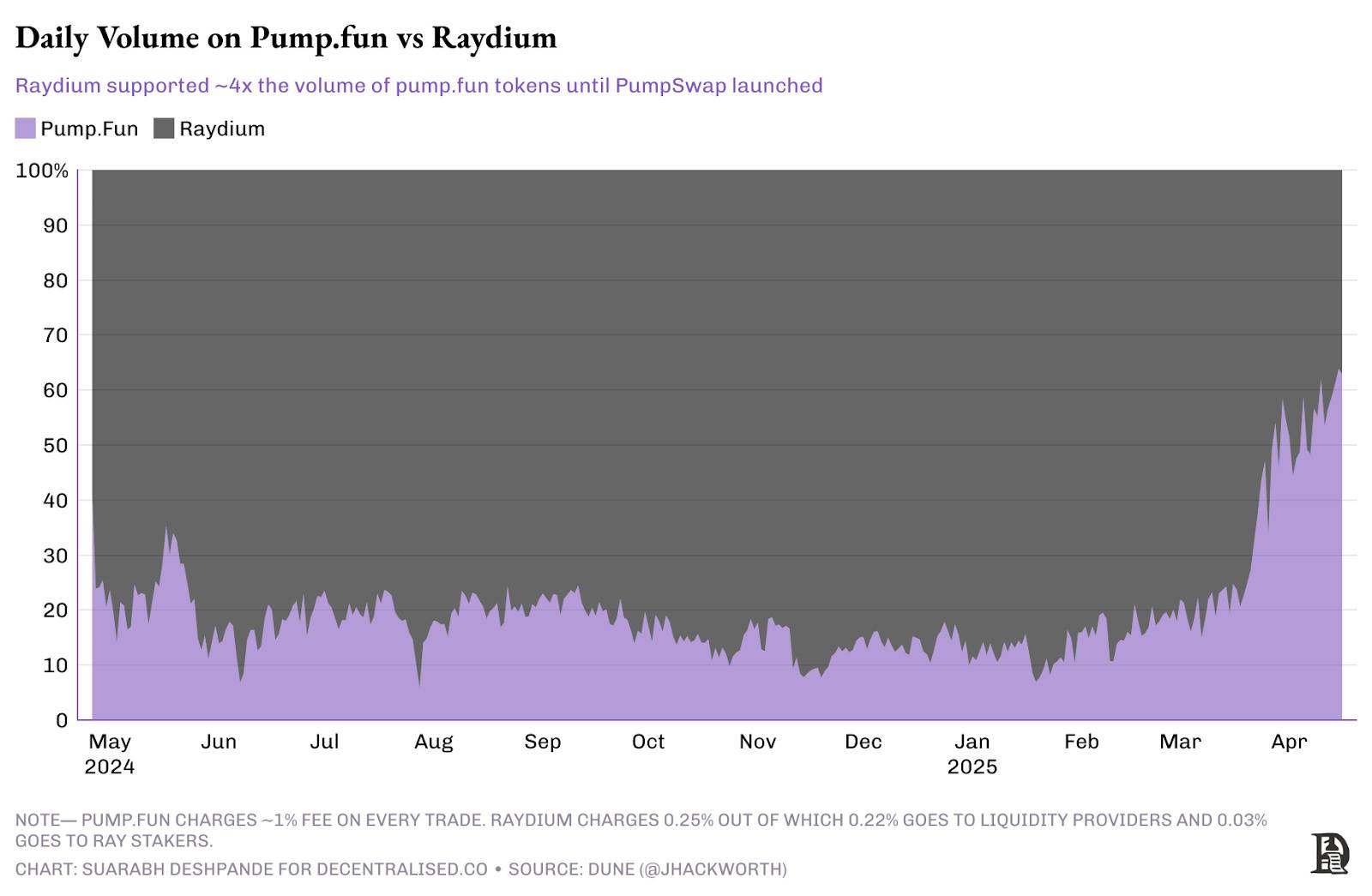

Listing on Raydium became a crucial milestone for emerging tokens, boosting credibility and visibility in a crowded market. By early 2025, the symbiosis became vital—over 40% of Raydium’s swap revenue came from tokens generated on PumpFun.

The relationship was mutually beneficial: PumpFun needed Raydium’s established liquidity pools to elevate its tokens from niche curiosities to tradable assets, while Raydium thrived on the explosive trading volume these tokens brought.

PumpFun’s economic model was impressive: it charged a 1% fee on exclusive trades of tokens launched on its platform, versus Raydium’s standard 0.25%. This meant Raydium needed to generate four times the trading volume to match PumpFun’s per-token revenue. Thanks to deeper liquidity and a broader user base, Raydium consistently surpassed this threshold from August 2024 to February 2025.

Raydium didn’t create memecoins nor invent the token factory concept. Yet by providing robust infrastructure for trading these assets and responding swiftly to competitive threats, it captured the lion’s share of ecosystem value.

The Solana memecoin saga illustrates a key aspect of second-order effects: value often flows not to those who create new behaviors, but to those who scale and facilitate them. PumpFun simplified token creation; Raydium enabled efficient price discovery and trading. Each innovation triggered further adaptation. PumpFun’s vertical integration efforts prompted Raydium to launch LaunchPad, sparking secondary effects that reshaped the entire ecosystem.

This attention wasn’t just fleeting—it was actively monetized. As memecoin mania intensified, tokens like Trump and Libra likely launched purely for hype. Their strategy relied on narrative, timing, and virality. Trump tapped into political meme energy; Libra leaned into broader internet culture. Both gained massive attention and reached absurd valuations shortly after launch.

But the momentum didn’t last. Attention arrived fast and faded faster. Secondary markets cooled. Traders moved on. Communities dwindled. Their success proved how to capture attention at the right moment and turn it into speculative gold. But they failed to sustain market cap—lacking real utility or a roadmap for lasting development, they were flashes in the pan.

Still, they made a point: innovation can capture attention. And in crypto, attention is one of the most powerful raw materials. Used wisely, it can spark new waves; misused, it vanishes quickly.

For observers of crypto innovation, the lesson is clear: when new primitives emerge, don’t just look at direct impact—ask who is best positioned to enable, optimize, and scale the behaviors they unlock. That’s often where outsized returns materialize.

What Now?

By now, you might be wondering what the next second-order explosion will look like. Maybe you call it compound innovation, or tech convergence—the point is the same. This article is about multiple technologies colliding at once, creating ripple effects greater than the sum of their parts.

We’ve seen it happen: re-staking reshaped DeFi incentives, memecoin infrastructure revived an entire ecosystem, yield protocols unexpectedly enabled airdrop leverage. So what’s the next domino to fall? Maybe EVM experience. Perhaps. It’s being rewritten, redesigned, refined—to feel like real software, at least that’s the promise. Whether it becomes the next great compounding layer or just another incremental upgrade remains to be seen.

But if the pieces align, it could trigger an unprecedented chain reaction.

Beneath the noise of L2 debates and scaling wars, a quiet race is unfolding—not just to scale Ethereum, but to enhance its utility by improving usability. Real usability: letting others build on it without wrestling wallets, gas fees, or failed transactions. Because when friction disappears, innovation flourishes. And when innovation flourishes, compounding returns appear in the most unexpected places.

In recent months, I’ve met remarkable individuals leading this shift: Andre Cronje from Sonic, Keone Hon from Monad, and Shuyao Kong from MegaETH. Despite different approaches, their goal is identical: eliminate latency. Remove friction. Even remove wallets. Replace them with something faster, smoother, invisible. Build a real software experience, not a series of tedious clicks.

MegaETH and Monad both claim 10,000 TPS—Solana speeds with Ethereum semantics. Given crypto’s history of overpromising, this would be the first EVM chain to make Solana look slow on UX—if delivered. (Ironic, considering EVM chains have long suffered slow confirmations and hellish wallet popups.)

Andre’s focus isn’t pure speed but eliminating complexity. He argues Ethereum’s performance ceiling is nowhere near reached. Currently, it runs at about 2% of its potential capacity—not due to hardware limits, but because of how the Ethereum Virtual Machine (EVM) reads and writes data. Sonic’s new database structure has already cut storage needs by 98%. His roadmap bets on abstraction—abstracted fees, abstracted accounts, abstracted wallets. If all goes well, by year-end, users won’t even know they’re using blockchain, while retaining meaningful decentralization. And that’s the point.

So who wins in this new world? Probably not the infrastructure teams obsessing over TPS benchmarks, but the applications built atop them—like how PumpFun leveraged Solana’s infrastructure to earn $500 million in under a year. Social protocols may break through. Projects like Farcaster already show how to merge crypto’s permanence with native web ease: no more paying to post, no MetaMask popups—just sharing content.

Then there’s DeFi. Next-gen financial apps need better inputs. Andre puts it bluntly: “We don’t have on-chain volatility, implied volatility, or realized volatility.” When those data points arrive, expect real options markets, coherent derivatives, and properly structured perpetuals—the financial layer crypto has long pretended to have.

Perhaps most exciting are the applications we haven’t imagined yet. Because that’s always how it unfolds. In 2005, no one looked at Google Maps and said, “You know what this needs? Ride-sharing.” But once the foundation changed, everything on top changed too.

So personally, I’m skeptical. I’ve been in crypto long enough to know that promised 10x improvements usually deliver slightly better dashboards and more Discord pings. But I’m also excited. Because this time, the underlying tech feels real. And behind it, a new generation of builders is quietly working on the second-order magic that might just reshape everything. Because for every breakthrough primitive visible today, dozens of builders are already crafting the second-order applications that will reveal its true value.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News