The Best Comparison to the "Trump Shock": What Happened in the 1971 "Nixon Shock"?

TechFlow Selected TechFlow Selected

The Best Comparison to the "Trump Shock": What Happened in the 1971 "Nixon Shock"?

The "Nixon shock" not only failed to achieve its intended goals, but also became a key driver of the severe inflation in the United States during the 1970s.

By Zhu Xueying, Wall Street Insights

As reported by CCTV News, former U.S. Treasury Secretary Summers stated in an interview that claims "tariffs have positive effects" are "fraudulent," and markets now worry that Trump's tariff threats could trigger a replay of Nixon's 1971 financial shock, posing a historic challenge to the dollar.

Nick Timiraos, known as the "new Fed whisperer," has already clearly raised this concern in an article published Thursday: the United States is attempting to dismantle the global trade order it built itself, ushering in an era of uncertainty. He argues that if these tariff policies are maintained long-term, their impact could rival President Nixon’s 1971 decision to abandon the gold standard, which ended the postwar financial architecture established by the U.S. and its WWII allies.

Huw van Steenis, vice chairman at Oliver Wyman, also highlighted this historical parallel in a weekend article. At that time, Nixon detached the dollar from the gold standard, imposed a 10% import surcharge, and introduced temporary price controls.

Steenis noted that the “Nixon shock” not only failed to achieve its intended goals but also eroded business confidence and led to stagflation. Nixon’s wage and price controls were a major failure, causing goods shortages and fueling a wage-price spiral—key drivers behind the severe inflation the U.S. experienced in the 1970s.

Like Trump’s tariffs today, Nixon’s measures aimed to pressure other countries into changing trade terms to help reduce America’s trade deficit. Then-Treasury Secretary John Connally’s mindset, as conveyed to Nixon, bears a striking resemblance to current administration trade logic:

“Mr. President, my view is that all foreigners are out to screw us, and our job is to screw them first.”

In such circumstances, more investors shift assets toward gold and physical holdings for preservation, while businesses and savers increasingly move activities away from banks and into bond markets.

Dollar Instability Drives Investors Toward Gold and Physical Assets for Protection

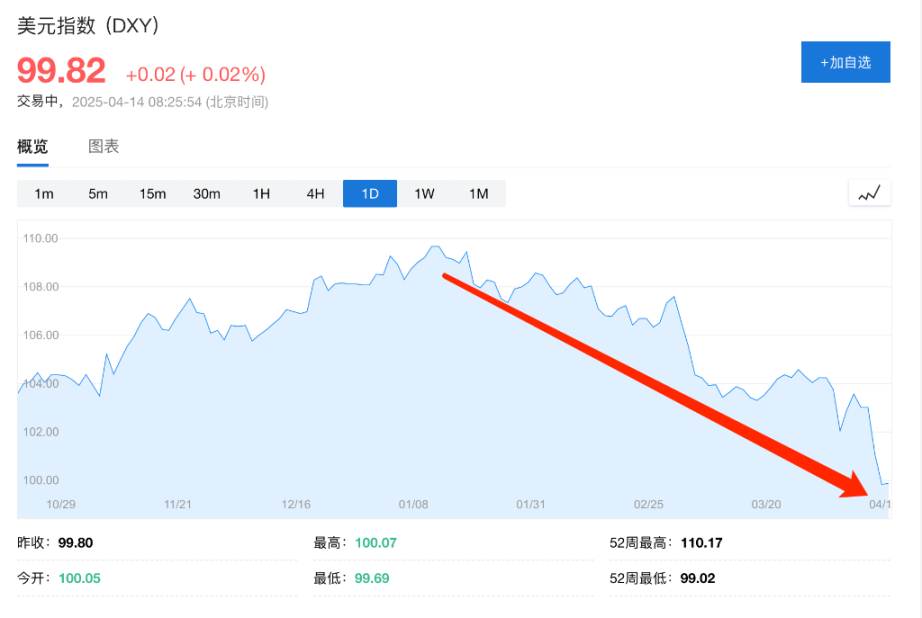

With the dollar index falling from its intraday high of 110.18 on January 13 to 100.10—a cumulative drop of 9.1%—investors are re-evaluating their strategies. According to Steenis, the inflation pain following the 1970s “Nixon shock” triggered profound changes in financial behavior and regulation.

Investors reallocated assets toward gold and tangible holdings for value preservation. At the same time, businesses and depositors shifted activities from banks to bond markets. Since then, the share of bank lending in total economic credit has steadily declined. In short, the modern financial system was forged in the early 1970s.

Steenis believes we may now be witnessing a similar market transformation.

Some investors are already moving capital out of the U.S., reassessing the dollar’s role as a reserve currency amid an accelerating de-dollarization trend. While the dollar historically benefited as a safe-haven asset during market volatility, U.S. stocks, bonds, and the dollar are now being sold off simultaneously—indicating waning investor confidence in American assets.

Tariff Impact: Short-Term Political Tool, Long-Term Economic Pain

Steenis pointed out that Nixon’s four-month tariff may have briefly supported dollar appreciation but ultimately failed to meet its objectives and had little discernible effect on imports. Yet, the economic ripple effects lasted decades—and even contributed to the eventual creation of the euro.

Whether we’ll see a digital euro or deeper European capital markets remains uncertain, but history suggests the consequences of this latest shock could persist for years.

Nixon Pressured the Federal Reserve

Steenis also noted that in today’s hyper-financialized world, bond markets can force policy changes much faster than in 1971. Nixon’s tariffs were lifted after four months via the Smithsonian Agreement, but today’s market reactions could be swifter and more intense.

Notably, the Nixon administration exerted significant pressure on the Federal Reserve to adopt expansionary monetary policies to cushion the shock.

According to Nixon speechwriter William Safire, the administration pressured then-Fed Chair Arthur Burns through anonymous leaks, even proposing to expand the size of the Fed so Nixon could appoint new members supportive of his agenda.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News