Analyzing Strategy's new financing plan: An "infinite ammo depot" for buying Bitcoin?

TechFlow Selected TechFlow Selected

Analyzing Strategy's new financing plan: An "infinite ammo depot" for buying Bitcoin?

This time, instead of relying on debt or selling stocks, the strategy uses an 8% interest, perpetual "super credit card."

Author: Scof, ChainCatcher

Recently, Strategy (formerly MicroStrategy) officially filed documents with the U.S. Securities and Exchange Commission (SEC), planning to issue up to $21 billion in 8% Series A perpetual preferred stock. This move has drawn significant market attention, as it not only involves a large-scale capital raise but could also profoundly impact Strategy’s Bitcoin acquisition strategy.

According to the official filing, each share of the preferred stock will have a par value of $100, carry an annual dividend rate of 8%, and pay dividends quarterly in cash, common stock, or a combination thereof. Additionally, the preferred shares are convertible into common stock at a ratio of 10:1—meaning every 10 preferred shares can be converted into one common share.

The offering will follow a "market issuance program," allowing the company to directly sell preferred shares on the open market, similar to an ATM (at-the-market) offering for common stock. This means Strategy now has simultaneous ATM financing capabilities for both common and preferred shares.

How does this preferred stock offering differ from previous financings? Could this innovative funding method introduce new dynamics into the Bitcoin market? This article provides an in-depth analysis.

The Evolution of Strategy’s Financing Methods

Before analyzing Strategy’s latest financing approach, let's briefly review its historical methods of purchasing Bitcoin.

In the early stages, Strategy—a software company—used idle cash on its balance sheet to buy Bitcoin. During this phase, the first three investments acquired 40,700 BTC.

As the company increased its commitment to Bitcoin, it began raising funds through convertible senior notes (convertible bonds). These instruments allow investors to convert debt into company stock under certain conditions, offering downside protection (principal and interest repayment upon maturity) while retaining upside potential if the stock price rises. This method funded the purchase of 119,481 BTC.

Besides convertible bonds, Strategy also issued secured senior notes—debt instruments backed by collateral, which carry lower risk than convertibles but offer more fixed returns. This model enabled the acquisition of 13,005 BTC.

With the rise of MSTR’s stock price, starting in 2021, the company increasingly adopted at-the-market (ATM) equity offerings—a widely used U.S. financing mechanism that allows public companies to issue new shares directly into the market at prevailing prices to raise capital.

On February 20 this year, Strategy issued $2 billion in convertible preferred notes—a financing method requiring a more complex and time-consuming review process, leading markets to speculate that its pace of Bitcoin buying would slow down.

However, the newly filed $21 billion perpetual preferred stock offering has reignited market expectations that Strategy may return to aggressive “buy mode.”

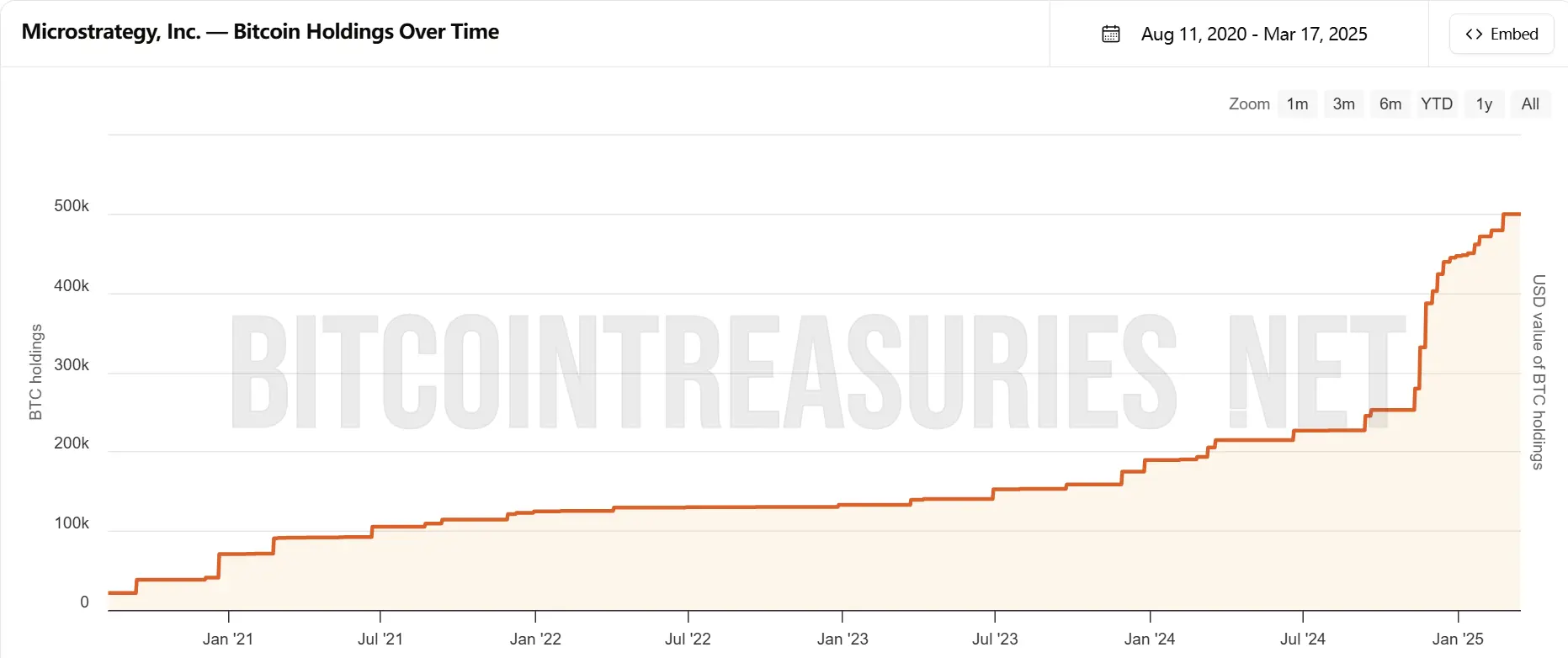

Bitcoin holdings of Strategy. Source: bitcointreasuries.net

What Makes Preferred Stock Different?

Compared to previous financing methods, the structure of the perpetual preferred stock that Strategy is now seeking approval for represents a clear departure. Historically, the company relied primarily on debt financing and common stock dilution to raise capital. This new preferred stock offering strikes a novel balance between traditional equity and debt financing.

The key difference between preferred and common stock is that preferred shares do not fully depend on corporate performance nor require principal repayment or have a maturity date. Instead, they function as a hybrid financial instrument—providing holders with regular fixed dividend income and, under specific conditions, the option to convert into common stock.

For Strategy, this means it can continuously raise capital by issuing preferred shares without bearing the repayment pressure associated with traditional debt. Compared to prior offerings such as convertible bonds and secured senior notes, this method offers greater flexibility and reduces short-term financial burdens.

That said, this model is not without cost. The 8% annual dividend rate is notably higher than the 0%-0.75% coupons on earlier convertible bond issuances and the 6.125% rate on secured senior notes. The central market question is how the company intends to cover this substantial dividend expense.

Analysts speculate that Strategy might use ATM common stock offerings to fill the funding gap—or even pay dividends directly in newly issued shares. While this enables rapid capital raising, it could also lead to further dilution of existing common shareholders’ equity.

Is This the Right Time to Bet Big?

If approved, Strategy’s perpetual preferred stock offering would undoubtedly inject fresh momentum into the Bitcoin market.

In simple terms, this preferred stock gives the company a more flexible and sustainable way to raise capital—money that will ultimately be used to buy Bitcoin.

Compared to issuing bonds or selling common stock, perpetual preferred stock has no maturity date, meaning Strategy can keep raising funds indefinitely without having to repay principal like traditional debt. Moreover, because this offering follows a model similar to common stock ATM programs, Strategy can sell preferred shares whenever market conditions are favorable—without waiting for bond approvals or securing specific investors.

This implies that Strategy’s future Bitcoin purchases could accelerate and become more consistent over time.

But is launching such an aggressive financing strategy appropriate amid the current market downturn?

James Carter, Senior Analyst at Goldman Sachs, stated, “Strategy’s $21 billion preferred stock proposal reflects Michael Saylor’s extreme optimism about Bitcoin. However, in the current weak market environment, such a highly leveraged move could amplify volatility risks.”

Michael Evans, Fintech Researcher at Citigroup, believes, “In the context of broad pressure across the crypto market, Strategy’s decision signals a strong conviction about future trends. If the market recovers, the returns could be extraordinary—but for now, investors should closely monitor capital flows and shifts in market sentiment.”

Given the complexity of the perpetual preferred stock structure, SEC approval may take several months. The ChainCatcher editorial team will continue to track developments.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News